Pan-United Corporation Ltd – Project offtake drives 35% YoY growth in 2H25 PATMI

- 2H25 revenue was within our expectations, while 2H25 PATMI exceeded our expectations. FY25 revenue/PATMI were at 103%/112% of our FY25e forecasts. 2H25 PATMI spiked 35% YoY to S$30.1mn, the highest increase since 2H23. This was driven by an estimated 12% YoY higher ready-mixed concrete (RMC) volume delivered due to higher project offtake, and higher efficiency achieved from its proprietary technology system AiR Digital. An example is the use of AiR Digital system to reduce truck queuing duration and thus operational costs.

- The Building and Construction Authority (BCA) projected 2026e RMC demand to be 15-16mn cubic metres, 7% higher YoY and 30% higher than the 20-year historical average of 11.9mn cubic metres annually. Demand in 2026e is expected to be driven by Changi Airport T5 superstructure, MBS Integrated Resort (IR) expansion, New Tengah General & Community Hospital, HDB BTO, and MRT LTA line extension.

- We maintain BUY with a higher DCF-derived TP of S$1.73 (prev. S$1.34). Our WACC/growth rate assumptions are unchanged at 7.7%/1.5%. We raised our TP to reflect a 3%/22% higher FY26e revenue/PATMI forecast. Industry RMC prices rose 4% YoY in 4Q25 to an average S$125/cubic metre, the highest since 2008. We believe Pan-United can benefit from expanded margins given higher ASPs from favourable construction demand and from its in-house technology platform. Pan-United trades at an attractive FY26e dividend yield of 4.2%.

Pan-United Corporation Ltd – Margin expansion and project visibility

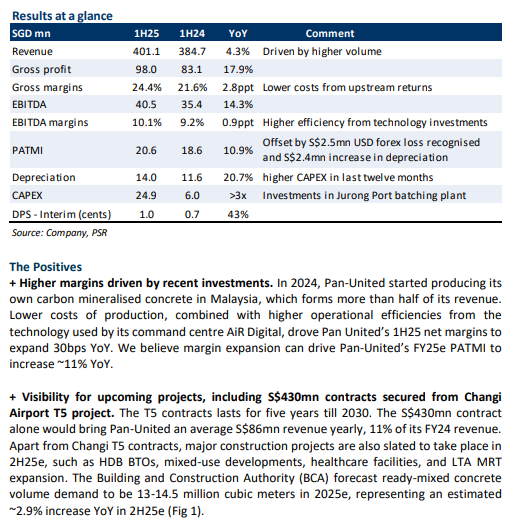

- 1H25 revenue/PATMI were within expectations, at 46%/46% of our FY25e forecast. 1H25 revenue increase of 4% YoY was driven by higher volume of ready-mixed concrete (RMC). 1H25 gross profit margins increased 2.8ppt because of lower costs of RMC from upstream facilities in Malaysia, driving 1H25 PATMI to increase 11% YoY.

- Pan-United’s operations are powered by AiR Digital, its in-house command centre. Recent investments in the technology enabled Pan-United to optimise its operations more efficiently, driving EBITDA margin expansion of 90bps YoY in 1H25. An example would be the use of AiR Digital system to manage mass pour operations, reducing truck queuing duration and thus operational costs.

- We maintain our FY25e forecast and BUY recommendation. Our TP is raised to S$1.34 (prev. S$0.75). We raised our FY25e working capital by 32% to S$19.2mn (prev. S$14.5mn) because of a S$6.2mn YoY increase in inventories sold in 1H25. We lower our WACC from 11% to 7.7% from the improved visibility of contracts secured by Pan-United, notably the S$430mn Changi Airport T5 contract. We believe the T5 project will ramp progressively over the next five years, with higher RMC demand towards the tail-end of the project when roads are paved. Based on the Building and Construction Authority (BCA)’s forecast, RMC demand is expected to increase ~2.9% YoY in 2H25e. This is driven by the progress of construction projects, such as HDB BTOs, mixed-use developments, healthcare facilities and LTA MRT expansion.

Pan-United Corporation Ltd – Still optimistic despite slower project take-off

- 2H24 revenue and PATMI were below expectations due to slower-than-expected project take-off. FY24 revenue/PATMI were at 94%/97% of our FY24e forecast. Gross profit/EBITDA were within expectations at 101%/101%. Final dividends jumped 28% YoY to 2.3 cents, bringing total FY24 DPS to 3.0 cents (FY23: 2.3 cents).

- Amidst the slower-than-expected project take-off, we expect the volume of RMC in 2025 to remain stable at 13.8mn cubic meter (2024:13.4mn cubic meter). We believe additional revenue from major construction projects will be reflected only in 2H25e.

- We maintain our BUY recommendation with a higher TP of S$0.75 (prev. S$0.68). We adjusted FY25e revenue/PATMI by -5%/+3% to reflect slower project take-off but higher profit margins. WACC is lowered to 11% (prev: 15%) to reflect healthier balance sheet and growth rate is raised to 1.5% (prev: 1%) to reflect Pan-United’s significant market share and future additional barriers to entry from the Jurong Port batching plant site. Pan-United trades at an attractive FY25e dividend yield of 4.9%.

Pan-United Corporation Ltd – De-carbonising drives up profits

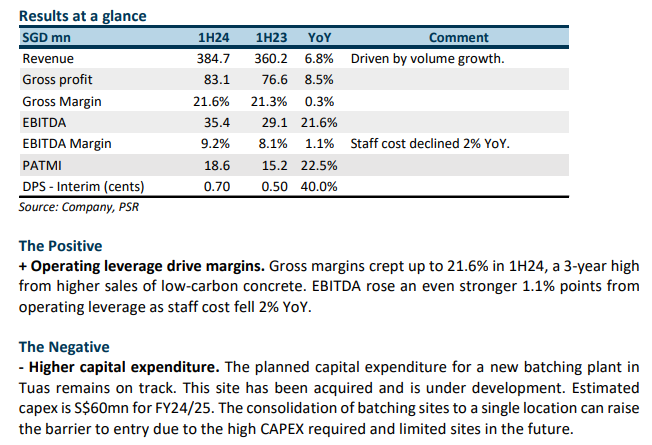

- 1H24 revenue and PATMI were within expectations at 44%/44% of our FY24e forecast. PATMI grew 22% YoY to S$18.6mn from revenue growth of 7% and a drop in staff costs. Gross margins crept up 30 basis points to 21.6%. Interim dividend jumped 40% YoY to 0.7 cents.

- Revenue growth was driven by higher volumes as selling prices were flat. Low carbon or carbon mineralised concrete is now more than 50% of revenue. There is rising demand from both property developers and the public sector for these carbon-saving materials.

- We maintain our FY24e forecast and BUY recommendation. Our target price is raised to S$0.68 (prev. S$0.55) as we lower our WACC from 20% to 15%. There is greater visibility and stability of construction contracts over the next five years. BCA expects construction demand to average S$34.5bn over the next five years (2024-28). This is 23% higher than the pre-pandemic average of S$28bn (2015-19). We believe Pan-United will benefit from this elevated multi-year construction spend with its ~40% market share in ready mix concrete industry. Another boost to market share will stem from rising demand for low-carbon concrete.

Pan-United Corporation Ltd – Tailwinds from construction demand, low-carbon solutions

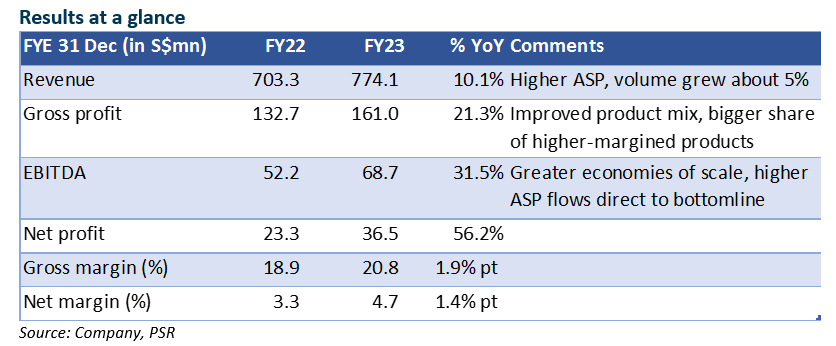

- FY23 net profit was 6% higher than our expectations. Net profit rose 56.2% YoY, lifted by higher ASP (we estimate +5%) and volume gain (+5%). Growth accelerated in 2H. 2H23 revenue gained 15% HoH, and net profit was +30%.

- Construction output in 2023 reached S$34.8bn, the highest since 2016. BCA projects output to be at S$34bn-37bn in 2024, driven by higher prices for materials and manpower. RMC volume could rise marginally to 12mn-13mn cum (average +1.6% YoY). Higher prices and higher sales of higher-margined products could sustain gross margin at 20%. The risk of customer default was reduced with about 60% of demand from public infrastructure projects, and the two integrated resorts.

- We maintain FY24e net profit estimates and a BUY recommendation. Our DCF-derived TP is raised to S$0.55 (prev. S$0.50) to reflect the strong cash flow. It increased FY23 dividend to 2.3 cents (FY22: 1.8 cents), delivering annual yield of 5.6%.

Positives

+ Achieved higher average selling price of +5% (our estimate), versus sector average of +1%., as it sold more higher-margined ready-mixed concrete products.

+ Gross margin strengthened further to 20.8% (+1.9% point YoY). We think the higher gross margin can be maintained, as low-carbon concrete products could gain wider acceptance, as a means to offset the higher carbon tax. In addition, demand for batching services, from which PanU earns a fee, is likely to be sustained. HDB has committed to launch 20,000 to 23,000 units per year through 2025.

+ ROE improved to 16.5% (FY22: 11.0%) despite net cash of S$43mn on its balance sheet. It generated FFO/share of 9.1 cents. We expect net cash to reach S$58mn at end-2024, even with higher projected capex of S$40mn to construct a new batching plant.

Negative

Nil

Pan-United Corporation Ltd – Volume catches up; surprise margin improvement

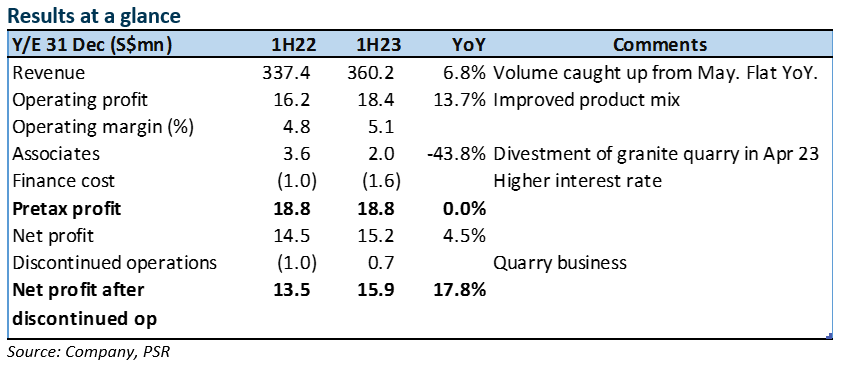

- 1H23 earnings beat our expectations, at 63% of FY23e, due to widening gross margins to 21.3% (+1.6% pt YoY) on improved product mix. Construction activities picked up from May, and PanU’s volume in 1H23 caught up to level that of 1H22.

- The company expects volume to rise in 2H23, with buoyant demand from public and private housing developments and infrastructure projects. We think the higher gross margin is sustainable, due to: 1) a higher mix of products which offer low-carbon solutions to the customers; and 2) higher fees from batching services offer to HDB construction work. Credit risks have risen with some construction companies facing distress. However, the impact on PanU is manageable as it supports mainly government projects.

- We raised our FY23e net earnings estimates by 36% to account for the higher margin. Maintain BUY with unchanged TP of S$0.50. The business generates strong operating cash flow, underpinning a dividend yield of 5%.

The Positives

+ Volume picked up from May despite the lull in the first four months, with the clampdown on construction work for safety checks. 1H23 volume was flat YoY.

+ Gross margin rose 1.6ppt to 21.3%. We think the improvement was derived from a better product mix as it sold more differentiated products such as those which offer low-carbon solutions, and higher fee income from batching services.

+ Net cash increased to S$18mn (Dec 22: S$10mn). Cash generation remains strong, with free cash flow of S$0.03/share. Receivable days have risen to 85 days (Dec22: 72 days) mainly due to the higher volume ramp-up at quarter end. While credit risk of the construction industry has risen, we think the impact on PanU is small as it supplies mainly to infrastructure projects.

The Negative

- Malaysia and Vietnam markets remained weak.

Pan-United – Muted FY23e outlook, a stronger FY24e

- Industry contract awards fell 13.5% in the first four months of 2023. At this rate, total contract awards for 2023 could come in at the lower end of BCA’s forecasts of S$27bn-32bn, and fall below 2022’s S$29.8bn. Lower contract awards will translate into lower construction output and building materials consumption in the following 6 to 12 months.

- A ramp up in the 2H 2023 government land sale programme will lift total supply of private housing units in 2023 to 9,250, nearly 50% higher than 2022. The development projects are expected to be awarded from early 2024, leading to an uplift in demand for building materials from 2H24e.

- We lower our FY23e net earnings estimates by 20% to factor in lower volume. Maintain BUY with lower TP of S$0.50 (prev. S$0.54). The business generates strong operating cash flow, underpinning a dividend yield of at least 4.5%.

Highlights

- Industry contracts awarded fell 13.5% in first four months of 2023 (Figure 1), after a 0.5% YoY decline in 2022. These contracts would translate into work performed and billed in 2H23e. We therefore expect slower revenue and profit growth in FY23e.

- Construction companies are turning more cautious in taking on new jobs as they face margin pressure from higher labour, material and safety compliance costs. We think this could have impacted tenders for larger projects with longer construction lead time.

- Consumption of RMC fell 4.6% in the first three months of 2023 (Figure 2). Selling price has also eased by 1.7% from the peak in June 2022 (Figure 3). Delivery of building materials have been affected by the authority-imposed heightened safety measures at worksites. These measures were lifted from June 2023.

- The GLS programme will yield about 9,250 private housing units in 2023, nearly 50% higher than 2022, and 2.5x the supply in 2021. The HDB also plans to supply up to 23,000 new Built-To-Order (BTO) flats in 2023 (2022: 23,184 flats). The construction contracts for these projects are expected to be awarded in the subsequent quarter, and translate into construction works over the next two years. We therefore expect an uplift in order delivery for building materials from 2H24e.

- Increased awareness and adoption of Pan-U’s low-carbon concrete solutions. The push towards sustainability construction has raised adoption of Pau-U’s low-carbon concrete solutions. These include the use of recycled, upcycled and waste materials, as well as carbon capture and utilisation (CCU) technologies such as CO2 mineralisation technology. Pan-U has supplied CO2 mineralised concrete to PSA’s Tuas Port and Capitaland’s building construction at 3 Science Park Drive. Greater industry adoption of these products would set Pan-U apart from its competitors.

- We lower our FY23e net profit estimates by 20% to factor in lower volume. Revenue and net profit growth in FY23e would be driven mainly by higher selling prices.

Maintain BUY with a lower TP of S$0.50

We maintain BUY with a lower DCF-derived TP of S$0.50 (prev. S$0.54). The operations generate strong FFO/share of S$0.0317 in FY23e, which underpins a dividend yield of at least 4.5%.

Pan-United Corporation Ltd. – Construction recovery slower than expected

- Workplace incidents hampered the recovery. As a result of the Heightened Safety period imposed by the Ministry of Manpower (MOM), local construction projects are, in general, progressing slower than expected. YTD22 contracts awarded is down 9.4% YoY.

- According to data from the Building and Construction Authority (BCA), demand for ready-mixed concrete (RMC) for the first nine months of 2022 was ~8.8mn cu/m, about 8% lower than our estimate and up 14.2% YoY.

- Maintain BUY with unchanged target price of S$0.54. We trim FY22e/FY23e earnings by 12%/11% respectively on account of the Heightened Safety period imposed. Our TP is unchanged as we roll forward our valuations, still based on 12x FY23e P/E, a 20% discount to its 10-year historical average P/E on account of the still uncertain business environment.

According to data from the BCA, demand for RMC for the first nine months of 2022 was ~8.8mn cu/m, about 8% lower than our estimate but higher than ~8.5mn cu/m in the same period last year (Figure 1). The construction recovery has slowed, with contracts awarded for the first nine months of 2022 5.3% lower than 2021. Construction progress payments for the same period, however, rose in 2022 by 14.2%.

No results update from PanU as it has moved to half-yearly reporting.

The Positives

+ Construction progress payments for first 9 months of 2022 rose 14.2% YoY. We believe construction progress payments were higher due to the relaxation of border restrictions on the inflow of migrant workers in 2022. This is an important metric, as it tracks work done in the sector.

The Negative

- Workplace fatalities hampered recovery. As of 1 Sept 2022, the number of workplace fatalities stands at 36 for the whole of 2022, up from the 28 workplace fatalities reported for the first six months of 2022, many of which were in the construction industry. As a result of the Heightened Safety period imposed by the Ministry of Manpower (MOM), local construction projects are, in general, progressing slower than expected. The time-outs and punitive measures imposed on the sector has slowed construction progress.

- Contracts awarded for first 10 months of 2022 9.4% weaker than 2021. Despite the strong pipeline of projects, contracts awarded slowed in 3Q22 as workplace fatalities hampered project progression rates.

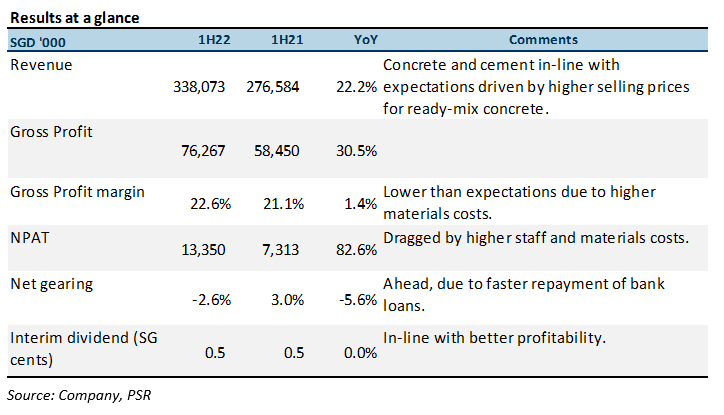

Pan-United Corporation Ltd. – Construction recovery hit slight snag in 1H22

- 1H22 revenue in line with our expectations, at 51%. Profit however, came in lower at 34% as result of higher staff and materials costs.

- Net profit grew 83% YoY driven by higher ASP of ready-mixed concrete (RMC) +18% YoY, higher GPM +1.4% and a higher share of results from associates of $3.6mn.

- Workplace fatalities and dengue hampered recovery. Volumes declined 10-15% as a result of the spate of stop-work orders issued by the authorities to construction sites.

- Maintain BUY with lower target price of S$0.54, from S$0.68. We trim FY22e/FY23e earnings by 26%/11% respectively on account of higher staff, utilities and materials costs. Our TP is based on 12x FY22e P/E, a 20% discount to its 10-year historical average P/E on account of the still uncertain business environment.

The Positives

+ 1H22 net profit grew 83% YoY, driven by construction recovery and better GPM. We estimate that higher demand +5% (Figure 1) and ASP of RMC +18% higher YoY (Figure 3) drove revenue growth of 22% YoY for 1H22. The Group also saw better GPM during the period as it successfully passed on cost increases to its customers. Overall, the construction sector continued to see a healthy recovery in the 1H22 (Figure 2) in part due to the relaxation of border restrictions on the inflow of migrant workers.

+ Higher contributions from associates of $3.6mn +168% YoY lift profits. The uplift in contribution was from the sale of coal from PT Lanna Harita Indonesia, which benefitted from higher coal prices during the period. Coal prices in 1H22 averaged US$300 and are up 182% YTD.

The Negative

- Workplace fatalities and dengue hampered recovery. In the first six months of 2022, the Ministry of Manpower (MOM) reported 28 workplace fatalities, many of which were in the construction industry. This led to a call for companies to conduct a safety time-out on 9 May 2022. In addition, in 1H22, more than 12,000 cases of dengue cases were reported, far exceeding the 5,258 cases logged in the whole of 2021. This resulted in a spate of stop-work orders issued by the authorities to construction sites, which impeded construction progress. Management guided that the volume decrease as a result of such stop-work orders adversely impacted volumes by 10-15%.

ESG

Pan-United has committed to supplying only low-carbon concrete by 2030 and pledged to offer carbon-neutral concrete products by 2040. It is committed to reducing its carbon output by 50% from 2005’s level by 2030. The company has already started its journey towards being more carbon-neutral. In 2021, it provided Surbana Jurong with concrete that was created with carbon mineralisation technology. As the concrete is mixed, carbon dioxide is injected to form calcium carbonate. This not only captures and stores carbon, but also strengthens the material.

We believe its move to more green products is not only more sustainable for the environment but also opens up new markets for them. In January this year, the Group signed a memorandum of understanding with Shell to collaborate on ways to repurpose carbon dioxide and industrial waste from the oil major’s Singapore operations as raw materials to produce low-carbon concrete.

Outlook

Construction sector sees faster pace of recovery in 1H22; tailwinds remain intact. HDB has announced that it will ramp up the supply of new build-to-order (BTO) flats over the next two years to meet the strong housing demand from Singaporeans. It plans to launch up to 23,000 flats per year in 2022 and 2023, which represents a significant increase of 35% from the 17,000 flats launched in 2021. Changi Airport’s Terminal 5 project will resume after being put on hold for two years due to the Covid-19 pandemic.

BCA’s forecasts of average construction demand over 2022-2026 of $25-32bn will support construction demand in the next few years.

In the near term, projects in the pipeline that will likely support the group’s growth are the Singapore Science Centre’s relocation, the Toa Payoh integrated development, Alexandra Hospital redevelopment, Bedok’s new integrated hospital, Phases 2-3 of the Cross Island MRT Line and the Downtown Line’s extension to Sungei Kadut.

With an approximately 40% market share in the industry, we continue to see PanU as a key beneficiary of the construction sector recovery. PanU’s batching plants still have capacity to take on a 10-15% increase in RMC demand in Singapore.

Maintain BUY with a lower TP of $0.54, from $0.68. We trim FY22e/FY23e earnings by 26%/11% respectively on account of higher staff, utilities and materials costs. Our TP is reduced to $0.54 from S$0.68 based on 12x FY22e P/E, a 20% discount to its 10-year historical P/E on account of the still uncertain business environment. Stock catalysts are expected from higher contract volumes and better margins.

Pan-United Corporation Ltd. – Construction recovery gaining pace

- According to data from the Building and Construction Authority (BCA), demand for ready-mixed concrete for the first three months of 2022 was 5% higher than the same period in 2021.

- The price of ready-mixed concrete (RMC) has also risen by 8.4% from Dec 2021 to April 2022 driven by a combination of higher raw materials costs and demand. The average daily charter hire of the Supramax and Handysize has risen from an average US$28,650 per day in 2021 to US$31,150 today.

- Supply-chain disruptions and volatile freight costs continue to hamper growth recovery. We believe the rising cost of RMC is a potential concern, though this is mitigated by the Group’s ability to pass-through these costs to the customer.

- Maintain BUY with higher target price of S$0.68, from S$0.46. We raise FY22e/FY23e earnings by 35%/26% respectively on account of the higher demand for ready-mixed concrete brought about by the construction recovery. Our TP is based on 12x FY22e P/E, a 20% discount to its 10-year historical average P/E on account of the still uncertain business environment.

According to data from the Building and Construction Authority, demand for ready-mixed concrete for the first three months of 2022 was 5% higher than the same period in 2021 (Figure 1). The construction recovery remains on track with progress payments billed for 2021 32.5% higher than 2020 (Figure 2). Contracts awarded for the first three months of 2022 was also 33.2% higher than 2021.

The price of RMC has also risen by 8.4% from Dec 2021 to April 2022 (Figure 3) driven by a combination of higher raw materials costs and demand. The higher cost of its components like sand, freight and bunker fuel cost have all driven up the price of RMC. For instance, the average daily charter hire of the Supramax and Handysize has risen from an average US$28,650 per day in 2021 to US$31,350 today.

The Positives

+ Construction recovery ahead of our expectations; we upgrade forecast of total RMC volume to 13.5mn m3 for 2022 vs. 12.8mn previously. With the construction sector recovering at a faster pace in the first quarter of the year than we expected, we upgrade our forecast of total RMC volume for the year. We expect construction demand to remain robust for the next few years, supported by strong demand for public housing and the backlog of projects from Covid-19 delays. BCA has forecasted annual construction demand of $25-32bn from FY23-26 and these forecast do not include the resumption of Changi Airport T5.

+ Manpower shortage resolved. With Singapore’s borders gradually reopening, work permit holders have returned to the hardest-hit sectors such as construction and marine shipyard. According to the Ministry of Manpower, work permit holders in these sectors now account for more than 90% of pre-pandemic levels. We expect that the manpower tightness at PanU has now been fully resolved and staffing can be ramped up should the Group require it to meet the rising demand in the next few years.

+ Strong operating results to drive Group into net cash position by 1H22e. With the faster pace of recovery in 1Q22, we have revised upwards our forecast for the Group. We now expect PanU to report free cash flows of ~$14mn for 1H22, which will be used to repay down ~$5mn in loans. We expect this to accelerate the Group’s move into a net cash position by 1H22e.

The Negative

- Supply-chain disruptions and volatile freight costs squeeze margins. With the rapidly rising price of RMC, we continue to watch for receivables risk in the sector. GP margin was slightly weaker for 2H21 as raw materials price rose at a faster pace than the average selling price. Apr-22 ASPs are 8.4% higher vs. Dec-21 at S$113/cu m. PanU also faced disruptions in raw-material supplies and had to search for alternatives. Supplies from new sources require lead times of a month for BCA testing before they can be imported. This hampered its ability to fulfil contracts. With coal prices up 135% YTD, we believe cement prices will remain elevated. We believe the rising cost of RMC is a potential concern, though this is mitigated by the Group’s ability to pass-through these costs to its customer and trade credit insurance.

Outlook

Construction sector sees faster pace of recovery in 1Q22; expects escalation of activity for rest of 2022. HDB has announced that it will ramp up the supply of new build-to-order (BTO) flats over the next two years to meet the strong housing demand from Singaporeans. It plans to launch up to 23,000 flats per year in 2022 and 2023, which represents a significant increase of 35% from the 17,000 flats launched in 2021. Minister for Transport S Iswaran also recently announced that Changi Airport’s Terminal 5 project will resume after being put on hold for two years due to the Covid-19 pandemic.

BCA’s forecasts of average construction demand over 2022-2026 of $25-32bn will support construction demand in the next few years.

In the near term, projects in the pipeline that will likely support the group’s growth are the Singapore Science Centre’s relocation, the Toa Payoh integrated development, Alexandra Hospital redevelopment, Bedok’s new integrated hospital, Phases 2-3 of the Cross Island MRT Line and the Downtown Line’s extension to Sungei Kadut.

With an approximately 40% market share in the industry, we continue to see PanU as a key beneficiary of the construction sector recovery. PanU’s batching plants still have capacity to take on a 10-15% increase in RMC demand in Singapore.

Maintain BUY with a higher TP of $0.68, from $0.46.

We raise FY22e/FY23e earnings by 35%/26% respectively on account of the higher demand for RMC brought about by the construction recovery. Our TP is raised to $0.68 from S$0.46 based on 12x FY22e P/E, a 20% discount to its 10-year historical P/E on account of the still uncertain business environment. Stock catalysts are expected from higher contract volumes and better margins.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report