The Positive

+ Market share gains and rising cash pile. PropNex shared that in 2023, its market share in new launches crept up 0.5% to 47.9%. Meanwhile, the share in resale rose a larger 6.8% points to 65.8%. HDB resale declined by 0.4% to 64.7%. It remains the largest real estate agency in Singapore, with 12,233 agents (or 66%). Cash continues to pile up in 2023 with a free cash flow of S$55mn (2022: S$49mn). The dividend payout ratio continues to rise to a record 93% in FY23.

The Negative

- Weakness in new launch revenue. Revenue in new launches declined by 36% YoY to S$128mn. The fall in sentiment post-cooling measure and the larger number of units available for resale affected demand. Gross margins contracted as new launches generate higher margins with the additional 0.5% commission paid to the agency.

The Positives

+ Strong market share gains. FY22 was a banner year for PropNex. Despite the drop in primary and secondary transaction volumes by 23% and residential leasing being down by 8% in 2022, revenue grew 8% to a record S$1bn. We believe there were market share gains, especially against the smaller agencies. A key differentiator has been their sales process and continuous efforts in engaging consumers that pivoted to the other segments, as primary sales were sluggish due to the collapse in new launches.

+ As expected, ample cash flow. FCF generated in FY22 was S$48.7mn (FY21: S$80mn). There was higher working capital of S$23mn tied up with receivables than a year ago. PropNex ended FY22 with net cash of S$138mn (FY21: S$145mn). The current dividend is around S$50mn p.a., well supported by annual operating cash flow and net cash.

The Negative

- Timing in recognition of commission. In 4Q22, PropNex made an impairment loss of S$5.5mn on receivables. The net impact on the income statement is offset by S$4.1mn derecognition of trade payable to agents. PropNex makes an impairment of its trade debtors for commissions not paid within 365 days. Two developers hit their 5% marketing fees limit. Both developer projects have been fully sold and the commission will be repaid when the projects reach their temporary occupation permit or completion.

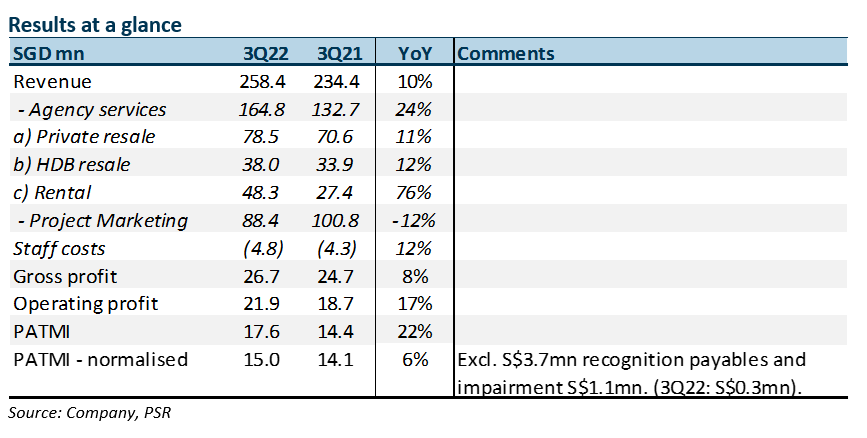

The Positive

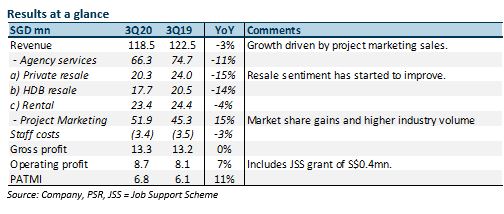

+ Resale bucked the trend. Despite the 28% YoY drop to 3,961 in total private resale volumes in 3Q22, PropNex managed to grow revenue by 11% to S$785mn. Reasons for the market share gains include the growth in the sales force and deliberate efforts to focus on resale. The price difference and lack of available units between new launches and resale helped stimulate resale volumes.

The Negative

- New launches are still a drag. Revenue from project marketing declined 12% YoY to S$88mn. The dearth of new launches and inventory has been a drag to revenue. New units transacted in Singapore (excluding EC) are down 38% to 2,187 units in 3Q22. With a balloting process, market share will also be determined by random chance.

Outlook

After two cooling measures and higher interest rates, we do expect some softening in buying interest from euphoric levels. Nevertheless, we remain upbeat that the key drivers supporting selling prices and demand are intact, namely rising residential population, low unemployment rates, new household formations (e.g. 25k marriages), rising land and construction cost, attractive HDB grants, low inventory level (1.5 years vs 3 year average) and return of foreign buyers. On the transaction volumes, the rebound in new launches for FY23 will support project market sales.

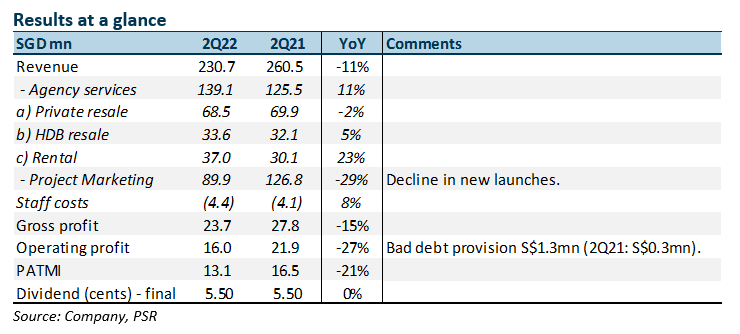

The Positive

+ Resilient revenue. Despite the weakness in new launches, other segments of the business managed to grow, less impacted by the December 2021 cooling measure. Rental income jumped 23%, followed by HDB resale.

The Negative

- Sluggish new launch revenue. There were only an estimated 1,548 new residential units launched in 1H22, a decline of 70% YoY from 5,222 units 1H21. As revenue from new launches are recognised typically six months after completion of the home sale, new launches may recover from a planned 5,183 units earmarked for 2H22.

Outlook

Property prices will remain elevated. We believe there is a virtuous cycle underway. HDB owners may enjoy gains that are used as equity (est. S$300k) to upgrade into the private residential market. Meanwhile, buyers of HDB resale include private property owners looking to cash out and move into HDB units. Other macro tailwinds include rising income levels, low supply, healthy developer balance sheet and higher priced land bids.

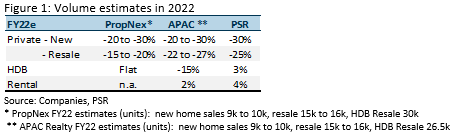

In terms of transaction volumes, new home sales are expected to decline more than expected in 2022, from a decline of 20-30% to 30-40%. No change in PropNex volume expectations for the other segments - private resale (decline 20-25%) and HDB resale (decline 5-10%).

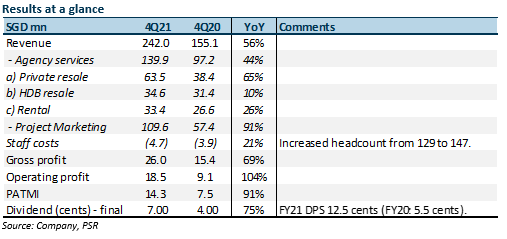

The Positives

+ Surge in revenue with operating leverage. The highest growth was registered in new home sales (+91% YoY) and resale (+65%). HDB resale was resilient with a 10% improvement in revenue. PATMI grew at a faster pace despite the increase in headcount due to operating leverage.

+ Jump in cash flow and dividends. The asset-light and highly cash generative business model was reflected in FY21. Operating cash flow in FY21 was S$83mn (FY20: S$42mn), driving up net cash on the balance sheet to S$146mn (FY20: S$106mn). The dividend of 12.5 cents in FY21 represents S$46mn. CAPEX in FY21 was S$0.5mn. Our DPS estimates for FY22 of 9 cents is based on a 77% payout ratio (FY21: 77%).

The Negative

- Nil.

Outlook

We expect a lull in transactions this year following the introduction of more cooling measures, namely the increase in stamp duties by 5% to 10% points and lowering of Total Debt Servicing Ratio (TDSR) from 60% to 55%. Nevertheless, we believe demand is generally healthy, especially for HDB:

Private new homes. New homes sales are expected to decline significantly due to the low unsold inventory, particularly in the popular OCR region. OCR inventory is only 3,972. The lowering of TDSR will cap the ability to leverage and turn pricing even more elastic. Another headwind will be the time lag for upgraders to purchase their units. The incremental 5% points of stamp duty to 17% for 2nd home purchase means an extra S$65-75k** of equity for an upgrader before securing a refund. This implies the upgrader will likely rent premises and collect proceeds before upgrading.

Private resales. The benefit of resale remains the lower price point to new launches. This should allow the decline in volumes to be less dramatic than new launches.

HDB resales. HDB will be the most resilient due to the attractive grants, delay in new units or BTO, healthy household formation and large MOP units available for sale.

Market share gains. An important catalyst to sustain revenue will be to increase PropNex’s market share. Since 2019, the number of agents has increased by around 50% to 11,125. PropNex disclosed that its recent market share for new launches post-cooling measures range from 53% to 57%.

Expectations are for prices to rise. Lower supply from developers, delay in HDB BTO units, rising construction costs and improving economic conditions will keep property prices elevated. PropNex expectations are for private residential home prices to rise 3-5% in 2022 (APAC Realty: +1-3%). HDB resale prices are expected to climb higher by 6-8% (APAC Realty: +4-8%).

Downgrade to NEUTRAL from ACCUMULATE with lower TP of S$1.74 (previous S$2.08)

Our FY22e PATMI is cut by 27% to S$43.5mn. Similarly, our DCF target price is lowered from S$2.08 to S$1.74. We raised our WACC modestly from 9.8% to 10% due to higher interest rates. Our terminal growth has expanded from 0% to 2% on our expectations of expanding long-term growth in property transactions.

The Positives

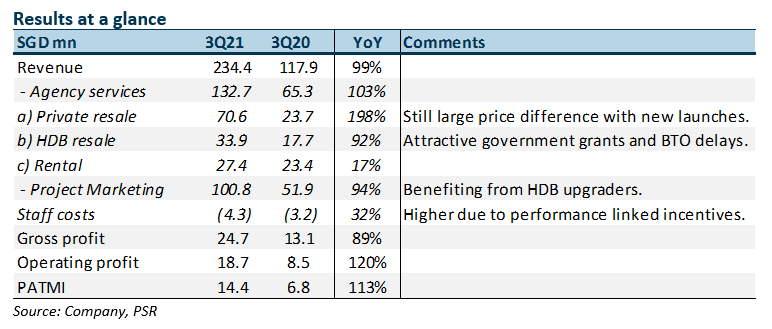

+ Broad based growth. The doubling of revenue was supported by growth in all segments. Revenue generated from the private resale and project marketing segments posted the highest YoY growth at 198% and 94% respectively. The buoyant resale market bolstered equity values for HDB owners and investors. HDB volumes were perked up by government grants and delays in BTO construction. Private resale demand was supported by the price differential between new and resale units and rising land and construction costs.

+ Full-year DPS guidance raised. PropNex guided FY21e dividends to be 75% to 80% of PATMI. This compares with the 70% payout in FY20. We raise our FY21e DPS by 17% to 13.5 cents per share, implying final dividends of 8 cents Our forecasted annual dividend payout of around S$50mn is well supported by operating cash-flows. 9M21 FCF was around S$57mn.

+ Net cash bulks up to S$123mn. Net cash stood at a record S$123mn as at Sep21. Cash generated from operations was S$23.9mn during the quarter (3Q20: S$9.6mn). Capital expenditure was a paltry S$25,000. The bulk of the cash generated in the quarter was to pay the interim dividend of S$20.3mn.

The Negative

- Nil.

Outlook

We expect the momentum in real estate transactions to sustain. Key drivers include low interest rates, BTO delays, rising land prices and construction costs and an expanding agency force.

Agency force. PropNex onboarded 2,000 new agents year-to-November, double the 924 new agents in 2020. This brings the number of agents to 10,324, one-third the market share of agents in Singapore. PropNex can tap on the network of the new sales force and enhance their outreach efforts. A large number of agents can further raise the company’s transaction market share.

Private new homes. PropNex raised its 2021 new home sales projection from 11k to 12-13k units. HDB upgraders form less than one-third of demand, with the bulk of the demand coming from upgrading of private property owners and investment-driven purchases. However, depleting developer landbanks may cause transactions to taper down next year to 11-12k units.

Private resales. PropNex raised its resale transactions guidance for the second time to 19k units, up from 16k and 18k previously. Resale prices, which can be 25% lower than new homes prices, are an important driver for demand. The price gap is likely to persist given the rising land prices. The lower price points are more palatable for HDB upgraders who prefer larger units.

HDB resales. FY21 transaction volumes are expected to come in at 30k units, up from 24.7k units in the prior year. Demand is driven by first-time home buyers looking to tap attractive government grants to circumvent BTO delays, as well as HDB owners looking to upsize or downsize their existing units.

New collective sales division. PropNex established this new division in 2021. Collective sales transactions are largely handled by property consultants. PropNex’s advantage is its intimate understanding of the market demand at various locations. This provides developers with the confidence that the en-bloc site can garner demand post redevelopment. So far, two en-bloc projects worth around $42mn have been completed. Another S$3bn of collective sales projects are at various stages of completion.

The Positives

+ Resale revenue recovered sharply. HDB and private residential resales rose a combined 37% YoY to S$62.5mn. HDB volumes were helped by government grants, delays in BTO units and a surge in units reaching their minimum occupation period. HDB resale revenue touched a record high. Private residential resales were bouyed by their large price discounts to newly launched units.

+ Even more cash. FY20 operating cash flows were S$42mn vs. meagre capex of S$0.5mn. Large cash inflows bulked up its net cash from S$81mn to S$105mn. Full-year dividend jumped 57% to 5.5 cents. A S$20.3mn payout is comfortably supported by operating cash flows and cash hoard on its balance sheet.

The Negative

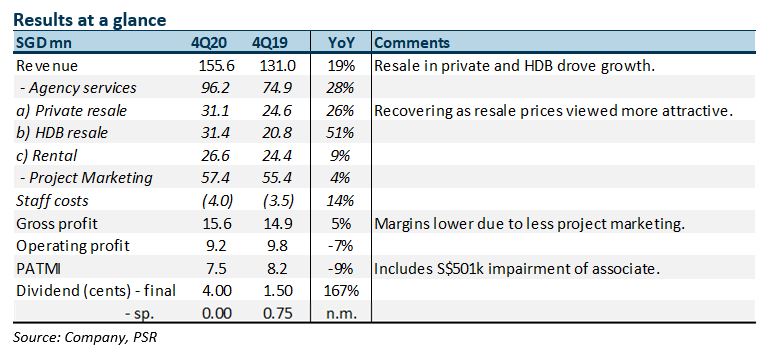

- Impairment of associate. There was an impairment of S$0.5mn for associate Soreal Prop and S$0.16mn for trade receivables in 4Q20.

Outlook

We expect another year of growth led by the resale market.

HDB resales. HDB resales have been stoked by enhanced CPF government grants for HDB purchases in late 2019 and a rise in the number of HDB units eligible for resale on the expiry of their minimum occupation period. An estimated 25,230 HDB flats will cross the minimum occupation period in 2021, higher than the 24,163 in 2020.

Private resales. Industry resale transactions advanced almost 20% in 2020 to 10,729, recovering from the dismal 8,949 transactions in 2019. During the peak years in 2017/18, transactions averaged 13,500. Improving sentiment and resale flats’ widening price differential with new launches supported their demand.

Private new homes. Volumes are expected to dwindle with a slowdown in new launches. But prices are expected to creep up on the back of improving demand and depleting unsold inventories. Inventories are tight especially in the Rest of Core and Outside Core regions.

Cooling measures. Investors were lately spooked by the prospect of new cooling measures from the authorities. The steepness of any rise in the property price index will be the obvious trigger. Before the last cooling measures in July 2018, the index had scaled 9.1% in a span of 12 months, over 2Q17-2Q18. In comparison, it is only up 2.2% in the past 12 months or 4Q19-4Q20. It is also only up 5.0% since the last cooling measures in 3Q18. To climb 9% over 12 months, the index would need to add 6% in the coming six months to 166 points.

Maintain BUY with higher TP of S$1.00, up from S$0.85

Our FY21e PATMI has been raised by 11% to S$30.8mn. Our FY21e revenue estimates was raised by 9%. We also lowered our WACC from 11% to 9.8% on account of a lower beta observed. An even stronger balance sheet, higher cash flows and reduced earnings volatility are reasons for the lower beta.

The Positives

+ Project marketing resilient. 2Q20 new home sales for the industry were down 27% YoY. We had expected the weakness to spill into this quarter as there is usually a lag of 2-3 months before revenue is billable. PropNex was resilient due to market-share gains, delays in prior sales due to options re-issuance and its ability to market projects virtually.

+ Cash kept piling up. 9M20 operating cash flow was S$30mn (9M19: S$21mn). As capex was minimal at S$0.2mn, cash buffer should be sufficient to meet our dividend forecast of S$14.8mn (DPU of 4 cents).

The Negative

- Nil.

Outlook

Resale volumes are recovering as consumer sentiment improves. HDB resales should be supported by enhanced grants for HBD purchasers introduced late last year and delays in BTO completions. Meanwhile, project sales could enter a near-term lull in October and November due to delays in new launches. In September, URA had restricted developers from re-issuing options. Potential buyers will likely need greater clarity and time before disposing of their existing properties and committing to new purchases.

Maintain BUY with higher TP of S$0.85, up from S$0.70

We raise our TP as FY20e/FY21e earnings have been increased by 40%/46% to factor in stronger than expected new-project revenue.