PRIME US REIT – Steady growth in occupancy

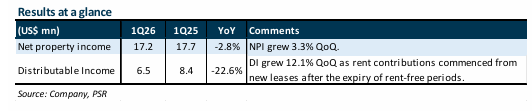

- 1Q26 NPI and DI declined 2.8% and 22.6% YoY to US$17.2mn and US$6.4mn, respectively, in line with expectations and forming 24% and 23% of our FY26e forecasts. The decline was due to lease expiries and rent-free periods associated with newly signed leases.

- Recovery remains on track, with portfolio occupancy improving to 83.1% (1Q25: 78.9%; 4Q25: 82.7%), marking the fourth consecutive quarter of growth. Leasing momentum also remained healthy, with 99k sqft (2.4% of NLA) of leases signed in 1Q26 at a positive rent reversion of 4% (4Q25: 188k sqft; +1.5%).

- Maintain BUY with an unchanged DDM-derived TP of US$0.32 and no change to our forecasts. Currently, only c.73% of occupancy is contributing cash rentals, with 463k sq ft of committed leases (11% of occupancy) scheduled to commence cash contributions progressively from 3Q26 onwards, supporting further growth in cash rental income. Leasing traction remains strong and we expect occupancy will exceed 85% by end-2026. Assuming a 65% payout ratio, the current share price implies an FY26e DPU yield of 7.3%. Prime continues to trade at a steep discount of 0.34x P/NAV, offering attractive dividend growth as the portfolio stabilises.

The Positive

+ Improving portfolio fundamentals. Portfolio occupancy has been on an uptrend since 1Q25,

rising 4.2 ppts to 83.1% in 1Q26. 99k sqft of leases were secured in 1Q26 at a +4% rental

reversion, including an 11-year lease for 40k sqft with S&P Global in March 2026, which lifted

occupancy at Village Center Station I from 63% to 80.1%. With 11% of occupancy staggered to

commence cash rentals from 3Q26 and only 5.4% of leases by rental income due for renewal in

FY26, Prime US REIT is well-positioned to deliver higher cash rental income and improved

earnings visibility going forward.

The Negative

- Expect all-in interest costs to edge up. The weighted average interest rate remained stable

QoQ at 5.4%, but is expected to rise, remaining below 6%, as 50% of hedges expire in June 2026.

Aggregate leverage was 45.2% while ICR was 1.6x, within MAS limits but with room for

improvement. We do not expect any refinancing issues for the 10% and 74% of total debt due

in 3Q26 and 3Q27, respectively, given supportive liquidity conditions in the US for quality assets.

PRIME US REIT – Higher payout ratio backed by cash flow visibility

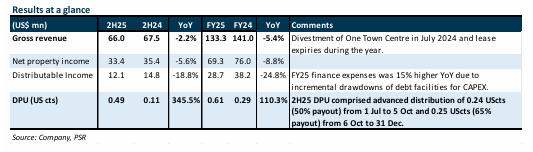

- 2H25/FY25 DPU of 0.49/0.61 US cents was in line, forming 80%/98% of our FY25e forecast, supported by a higher payout ratio (2024–1H25: 10%; Oct 2025: 50%; Dec 2025: 65%). FY25 revenue and NPI declined 5.4% and 8.8% YoY, respectively, due to the July 2024 divestment of One Town Centre and lease expiries during the year.

- 680k sqft (16% of NLA) of leases were signed in FY25 at a +5.6% rental reversion (FY24: 592k sqft; +1.8%), reflecting improved leasing momentum. Portfolio occupancy increased from 80.7% to 82.7% QoQ, and we expect it to reach at least 85% by end-2026. Portfolio valuations rose 3.5% YoY to US$1.4bn, indicating a turnaround in capital values.

- Maintain BUY with a higher DDM-derived TP of US$0.32 (prev. US$0.30) as we roll forward our forecasts. The payout ratio has been raised to at least 65% of distributable income, supported by improving committed occupancy and strong cash flow visibility, as new leases signed in FY24/25 (10.6% of portfolio occupancy) are staggered to commence cash contributions from 2026 onwards. Assuming a 65% payout ratio in FY26e, the current share price implies an FY26e DPU yield of 5.9%. Prime trades at a steep discount at 0.42x P/NAV, offering an attractive entry point with dividend growth as the portfolio stabilises.

The Positive

+ Higher payout ratio backed by improving portfolio fundamentals. Portfolio occupancy rose

from 80.7% to 82.7% QoQ (FY24: 80%) and is expected to reach at least 85% by end-2026, with

active leasing initiatives continuing. 680k sqft of leases were secured in FY25 at a +5.6% rental

reversion amid improving leasing momentum (FY24: 592k sqft; +1.8%). WALE increased to 5.6

years (FY24: 4.4 years), enhancing income visibility, while only 7.2% of leases by income are due

for renewal in 2026.

+ Portfolio valuations rose 3.5% YoY to US$1.4bn. 11 of 13 assets posted gains, driven by

stronger contracted cash flows and 25-50bps cap rate compression.

The Negative

- Two properties recorded valuation declines due to higher cap and discount rates. 171 17th

Street fell 6% following a comparable sale in May 2025 by a seller undergoing restructuring.

Tower I at Emeryville saw a sharp 48.7% decline after a nearby comparable transaction in Sep

2025 was completed at a c.10% cap rate, leading valuers to apply a c.200bps increase in both

cap and discount rates for the asset. It is located within the San Francisco Bay Area submarket,

where leasing remains subdued, though current conditions likely reflect a cyclical trough.

PRIME US REIT – Recovery on the horizon

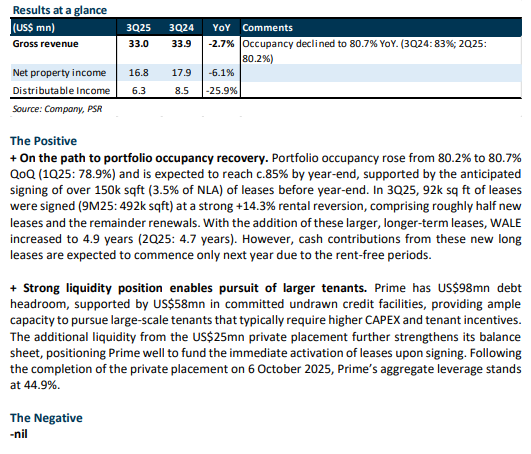

- 3Q25/9M25 distributable income declined 26%/28% YoY, in line with expectations at 21%/76% of our FY25e forecast. The weaker 3Q25 performance reflected a lower portfolio occupancy of 80.7% (3Q24: 83%) and higher finance costs following the Aug-24 loan refinancing.

- 92k sqft (2% of NLA) of leases were signed in 3Q25 at a strong +14.5% rental reversion (2Q25: +4.3%). Portfolio occupancy inched up from 80.2% to 80.7% QoQ, and is expected to reach c.85% by year-end with the signing of large leases totalling over 150k sqft (c.3.5% of NLA).

- Maintain BUY with an unchanged DDM-derived TP of US$0.30 and no changes to our forecasts. The payout ratio will be raised to at least 50% of distributable income from 2H25 onwards (10% payout ratio since 2H23), supported by improving committed occupancy and strong income visibility, as 10.8% of portfolio occupancy is staggered to start contributing cash flows from 4Q25 onwards. Assuming a 50% payout ratio in 2H25 and FY26e, the current share price implies FY25e/26e DPU yields of 3.1%/6.7%. Prime trades at a steep discount at 0.37x P/NAV, offering an attractive entry point with dividend growth as the portfolio stabilises.

PRIME US REIT – Raising capital to fund growth

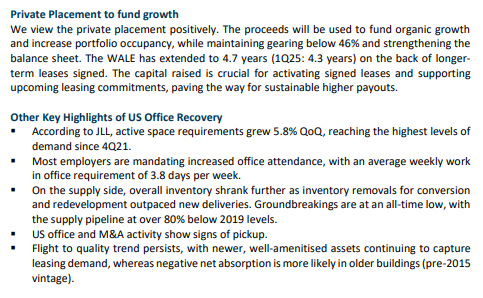

- Prime US REIT will raise US$25mn via a private placement, issuing 129mn new units (9.9% of current units) at US$0.1935 per unit (c.10% discount to 24 Sep 2025 VWAP). The proceeds will be used to fund capital expenditure, tenant incentives, leasing costs to attract/retain tenants, and meet existing tenant obligations.

- The payout ratio will be raised to at least 50% from 2H25 onwards (10% in 1H25), while retaining the balance of distributable income to cover ongoing capital and operational needs. With 10.5% of occupancy staggered to commence its cash contribution from 3Q25, management sees sufficient cash flow visibility to sustain the higher payout ratio going forward.

- Maintain BUY with a higher DDM-derived TP of US$0.30 (prev. US$0.21). We raise our FY25e DPU from 0.26 cents to 0.62 cents (2H25: 50 cents) on a higher 50% payout ratio (1H25: 10%) in 2H25. Our cost of equity is lowered to 10.5% (prev. 14.9%) amid signs of recovery in the US office market and cash flow visibility from new leases signed in FY24/1H25 (10.5% of occupancy yet to commence cash contributions). Prime is also in advanced negotiations to secure over 150k sqft (3.5% of NLA) of space, with portfolio occupancy expected to recover to 85% by end-2025 (1H25:80.2%). Additionally, we anticipate a slight portfolio valuation uplift at year-end, driven by the signing of new leases. The current share price implies an FY25e/26e DPU yield of 3.1%/6.65%, while trading at a steep discount at 0.37x P/NAV.

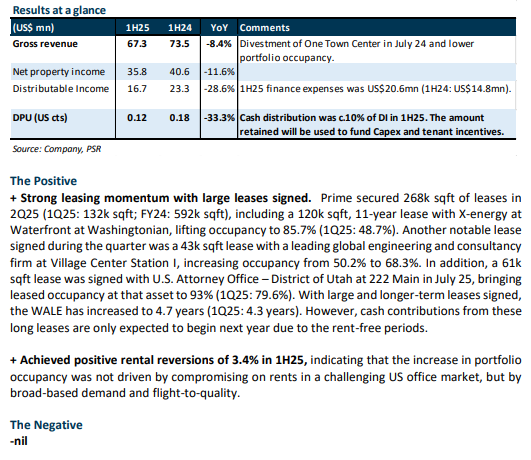

PRIME US REIT – Improving portfolio occupancy

- 1H25 DI/DPU were within expectations at 49%/46% of our FY25e forecast. 1H25 DI fell 29% YoY due to a 39% surge in interest cost from the Aug-24 loan refinancing, the divestment of One Town Center in July-24, and lower portfolio occupancy of 80.2% (1H24: 83.9%).

- Portfolio occupancy rose from 78.9% in 1Q25 to 80.2%, aided by stronger leasing momentum, including a 120k sqft (2.9% of NLA) 11-year lease signed at Waterfront at Washingtonian in June 25. 2Q25 rental reversions improved to +4.3% (FY24: +1.8%; 1Q25: +2.6%), supported by flight-to-quality and return-to-office trends. Occupancy should rise in 2H25, supported by a 61k sqft (1.5% of NLA) lease signed at 222 Main in July 25. Prime has no refinancing requirements in FY25.

- Maintain BUY with a higher DDM-derived TP of US$0.21 (prev. US$0.20). Our forecast remains unchanged, but we lower our cost of equity assumptions to 14.9% (prev. 15.95%) amid signs of recovery in the US office market. We assume a 10% payout ratio in FY25e, rising to 50% in FY26e, as new leases signed in FY24/1H25 (10.5% of occupancy) are staggered to start contributing cash rentals after rent-free periods from 3Q25 onwards. The current share price implies an FY25e/26e DPU yield of 1.5%/8.25%. Prime is currently trading at a steep discount at 0.31x P/NAV.

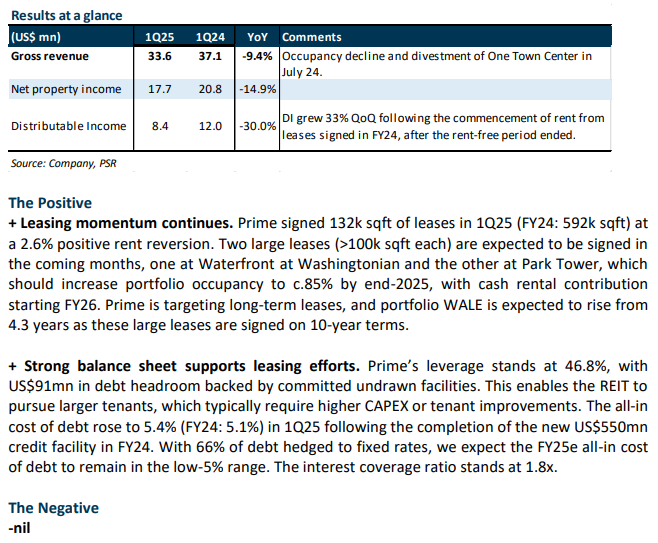

PRIME US REIT – Laying the groundwork for future growth

- 1Q25 NPI/DI were within expectations at 23%/25% of our FY25e forecast. DI declined 30% YoY due to lower portfolio occupancy (1Q25: 78.9% vs 1Q24: 80.9%), the divestment of One Town Center in July 24, and higher finance expenses.

- Leases signed in 1Q25 achieved a positive rental reversion of 2.6% (FY24: +1.8%). Two large leases (>100k sqft each) are expected to be signed in FY25, with cash rental collection commencing in FY26. These leases are expected to lift portfolio occupancy towards c.85% by end-2025. Prime has no refinancing requirements in FY25.

- Maintain BUY with an unchanged DDM-derived TP of US$0.20. Our estimates remain unchanged. We assume the 10% payout ratio continues through FY25e and a return to 100% distributions in FY26e, as new leases signed in FY24/1Q25 (6.4% of occupancy) begin contributing cash rentals after the rent-free periods. The current share price implies an FY25e/26e DPU yield of 1.8%/20.4%. Prime is currently trading at a steep discount at 0.25x P/NAV.

PRIME US REIT – Unexpected rise in portfolio valuations

- 2H24/FY24 DPU of 0.11/0.29UScts (-52%/-88% YoY) were below expectations at 33%/88% of our FY24e forecast. The YoY decline was due to: 1) the manager retaining c.90% of DI for capital expenditure, 2) the divestment of One Town Center in July 24, 3) Waterfront at Washingtonian’s asset enhancement initiative (AEI), and 4) higher finance expenses. 2H24/FY24 DI was 36%/93% of our FY24e forecast.

- Portfolio valuations rose 2.2% YoY to US$1.352bn, driven by stronger operating performance and positive leasing momentum, despite a slight increase in cap and discount rates. FY24 leasing volume grew 1.9% YoY, with leases signed at a 1.8% positive rental reversion.

- We maintain BUY with an unchanged TP of US$0.20. We lower our FY25e/26e DPU estimates by 21%/20% to reflect a lower NPI margin, aligning with FY24 levels as we roll forward our forecasts. Assuming the 10% payout ratio continues through FY25e and Prime resumes full distributions in FY26e, the current share price implies an FY25e/26e DPU yield of 1.7%/19.5%. We expect a return to 100% distribution in FY26e, supported by higher portfolio occupancy, lower capex and tenant incentive requirements, and cash contributions from leases signed in FY24/FY25 as rent-free periods and incentives phase out. With more employers mandating return-to-office five days a week, Prime is well-positioned to benefit from this trend and the improving leasing momentum. Prime is currently trading at a steep discount at 0.26x P/NAV.

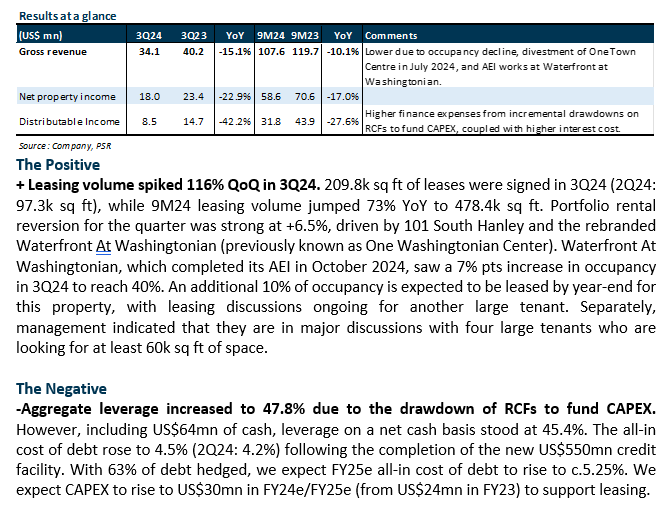

PRIME US REIT – Improving leasing volumes

- 3Q24/9M24 distributable income, down 42.2%/27.6% YoY, was in line with our expectations and formed 21%/77% of our FY24e estimates. 3Q24 distributable income fell 42.2% YoY due to: 1) portfolio occupancy decline, 2) divestment of One Town Centre, 3) AEI works at Waterfront at Washingtonian, and 4) higher finance expenses from RCF drawdowns to fund CAPEX, along with higher interest costs.

- Leasing volume spiked 116% QoQ in 3Q24, with a gross rental reversion of +6.5% for the quarter. Excluding Waterfront at Washingtonian, which completed its AEI in October 2024 and is currently 40.2% leased, portfolio occupancy fell by 0.9ppts QoQ to 83%.

- We maintain BUY with a lower TP of US$0.20 from US$0.22. Our estimates remain unchanged, but we now assume the 10% payout ratio will persist through to FY25e (prev. 100% in FY25e). Based on our assumption of a 10% payout ratio in FY24e, the current share price implies an FY24e DPU yield of 2.1%, which is still considered favourable compared to its peers, which are not paying any dividends. With further interest rate cuts expected and improving leasing momentum, we think there is potential for share price appreciation as Prime is currently trading at a steep discount at 0.27x P/NAV.

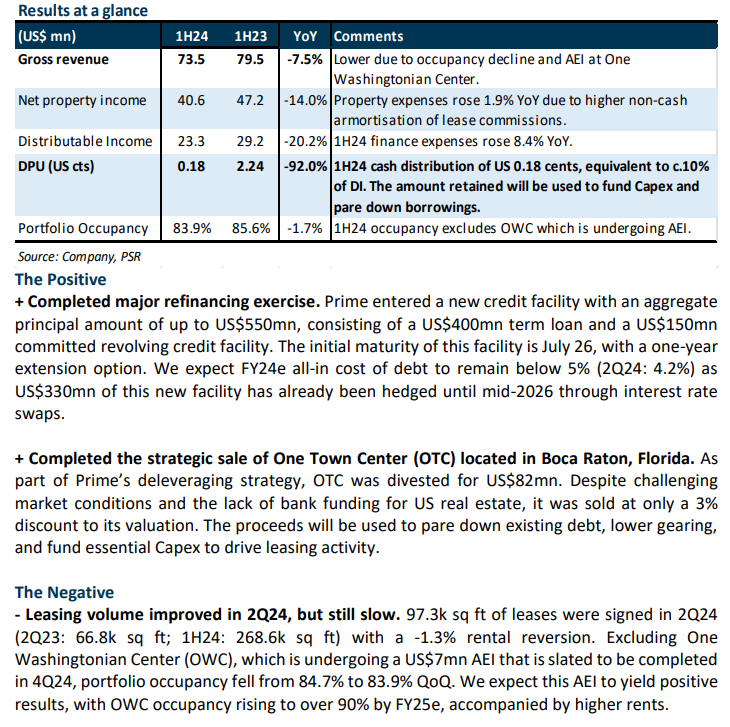

PRIME US REIT – Refinancing finally complete

- 1H24 results were within expectations. Gross revenue/distributable income was 47%/45% of our FY24e forecast. DPU of 0.18 US cents missed our estimates as Prime paid out only c.10% of DI in 1H24, compared to our initial assumption of 25%.

- Completed the major refinancing exercise on 9 August 2024 with a US$550mn credit facility. This new facility has an initial maturity in July 2026, with an option to extend for an additional year. The facility will be used to repay S$504.3mn of loans, with the balance for working capital and capital expenditure.

- We upgrade from ACCUMULATE to BUY with a higher TP of US$0.22 from US$0.12. We revert our valuation methodology back to DDM (cost of equity: 15.95%, g: 1.75%) from 0.2x P/NAV after the successful securing of a new secured

loan facility. We lower our FY24e DPU forecast by 68% after accounting for the divestment of One Town Center and a lower payout ratio of 10% (previously assumed 25% payout ratio). Based on our assumption of a 10% payout ratio in FY24e, the current share price implies an FY24e DPU yield of 1.8%, which is still considered favourable compared to its peers, which are not paying any dividends. We think there is potential for capital appreciation as Prime is currently trading at a steep discount at 0.32x P/NAV.

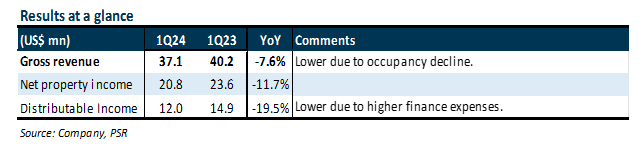

Prime US REIT – Pricing in some refinancing risk

- 1Q24 results were within expectations. Gross revenue/distributable income was 23%/22% of our FY24e forecast. DI was 19.5% lower YoY due to lower portfolio occupancy (1Q24: 80.9%) and higher finance expenses.

- Management is confident that it will refinance the US$480mn (69% of total) debt before its July 2024 maturity as: 1) Prime is in the final stages of securing the loan, 2) the lenders are a syndicate led by Bank of Amerca. US banks are relatively more comfortable with financing US commercial real estate on a 65% LTV and an ICR of 1.5x, and 3) Prime’s assets are still generating income and cash-flows. However, credit spreads and interest cost may widen.

- Downgrade from BUY to ACCUMULATE with a lower TP of US$0.12 from US$0.30. We peg our TP to 0.2x P/NAV (from DDM), in line with its peers. We are pricing in the refinancing risk by changing our valuation from DDM to P/NAV that is in-line with US office peers. We believe this is warranted due to the short two-month window to refinance the debt. Prime is now focusing on deleveraging and has set a target to execute US$100mn of deleveraging in 2024. A successful refinancing of the US$480mn loan maturing in July 2024 we believe will help narrow the discount to NAV to 0.3x P/NAV and a target price of US$0.18. Based on our assumption of a 25% payout ratio in FY24e, the current share price implies an FY24e DPU yield of 9.5%. Prime is currently trading at 0.19x P/NAV.

The Positive

+ Leasing volume more than doubled YoY. Over 171.3k sq ft of leases were signed in 1Q24 (1Q23: 64.4k sq ft; 4Q23: 304.1k sq ft). Rental reversion for 1Q24 was -1.8% due to a 31.8k sq ft 11-year lease renewal in Reston Square with rents below preceding rents but above market rents. Management indicated strong leasing momentum at some of its properties, with notable leasing discussions underway at One Washingtonian Center (OWC), Park Tower, and 101 Hanley, albeit with relatively longer lead times.

The Negatives

- Two months left to refinance US$480mn or 69% of total debt due July 2024. Management is actively discussing refinancing this loan with lenders and believes it will be completed before maturity. 79% of total debt are either on fixed rate or hedged, with US$330mn of the US$480mn debt due for refinancing in July 2024 already hedged till June 2026. The cost of debt rose 0.1%pts QoQ to 4.1%. Aggregate leverage stood at 48.1%, with an ICR of 2.9x.

- 1Q24 Portfolio occupancy fell to 80.9% (FY23: 85.4%) after Sodexo vacated OWC. OWC is now undergoing an asset enhancement initiative to rejuvenate the asset, which is expected to be completed in 2H24. Excluding OWC, occupancy was 84.7%.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report