The Positives

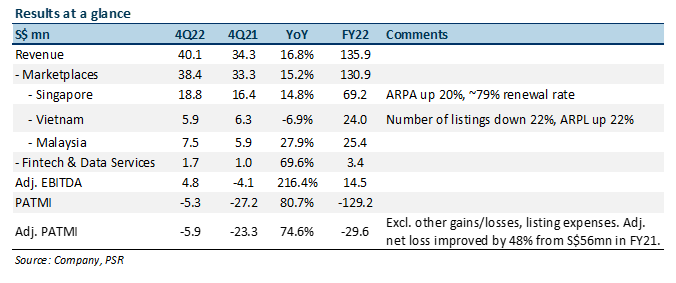

+ Revenue met company guidance. 4Q22 revenue grew 17% YoY to S$40mn despite the decline in the Vietnam market. Singapore Marketplaces revenue increased 15% to S$19mn with average revenue per agent (ARPA) up 20% while also maintaining a high renewal rate of 79%. The number of subscribing agents in the country also increased to ~15,500 from ~15,300 in 3Q22. Vietnam revenue declined by 7% YoY to S$6mn as the number of listings were down 22% in 4Q22 due to the credit tightening policy by the government. However, average revenue per listing (ARPL) increased by 22% to S$3.25 as a result of increased premium product adoption and longer listing period.

+ Improvements in profitability. Net loss for the quarter improved by 81% to S$5mn compared with 4Q21, bringing the FY22 total net loss to S$129mn, 31% lower than the net loss of S$187mn in FY21. Excluding other gains/losses from fair value changes and one-off IPO expenses, adj. net loss was cut by 48% from S$56mn in FY21 to S$29mn in FY22, demonstrating PGRU’s increasing operating leverage. We expect these costs to remain stable and PGRU to further increase its operating leverage as revenue grows.

The Negatives

- FY23 revenue guidance below our forecast. Management has guided for FY23e revenue to be S$160mn-S$170mn, a growth of 18-25% as PGRU continues to expect challenges from macroeconomic uncertainties in Vietnam and Malaysia. Specifically for Vietnam, PGRU expects the credit restriction policy to remain in place in 1Q23 with hopes of it easing in 2Q23. As such, PGRU is expecting a softer 1H23 for the Vietnam market with growth re-accelerating in 2H23. Meanwhile, the Singapore property market remains strong as prices increased despite a QoQ decline in transaction volume. It also has a strong supply pipeline in FY23.

The Positives

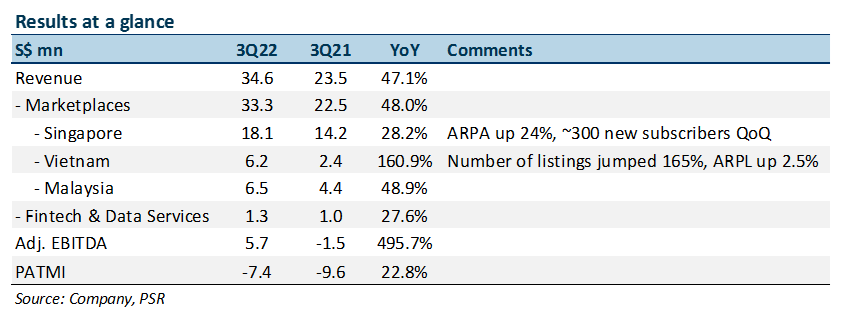

+ Marketplaces continued strong growth. Segment revenue grew 48% YoY to S$33.3mn, led by jumps in Vietnam and Malaysia. Vietnam revenue spiked 161% to S$6.2mn, benefitting from a favorable comparison and the easing of COVID-related lockdowns with number of listings surging 165% during the quarter. Revenue from Malaysia grew 49% to S$6.5mn, reflecting the benefits of its acquisition of iProperty. Singapore remained the largest contributor segment with revenue growing 28% to S$18.1mn. The company was also able to attract ~300 new subscribers QoQ, bringing the total number of agent customers in the country to 15,351.

+ Increasing monetization of agent customers. Average revenue per agent (ARPA) in the Singapore market rose 24% YoY to S$1,042 while the average revenue per listing (ARPL) in Vietnam increased by 2.5%, due to increase in premium product adoption and discretionary spendings by customers. PGRU was also able to achieve a high renewal rate of ~87% in 3Q22, up from 82% in 2Q22, despite the company raising its subscription prices by ~15% that took effect on 1 September 2022. PGRU also expects to raise prices in Malaysia in December.

The Negatives

- Macroeconomic headwinds and government initiatives to weigh on growth. Management has revised its FY22e revenue guidance to between S$134mn and S$138mn, a growth of 33-37%, down from the previous guidance of 44%, mainly due to macroeconomic uncertainties arising from cooling measures implemented by local governments. Singapore’s increased taxes and stamp duties; decreased maximum LTV loan ratios; and the 15-month wait period for private HDB buyers; as well as Vietnam’s credit restrictions for home buyers and developers are expected to reduce activity in the real estate market. Additionally, the election in Malaysia is also expected to put home buyers and developers on a more cautious stance. These factors can potentially impact the income of agents and businesses of developer customers, thus affecting their spending power.

Company Background

PropertyGuru Group Ltd. (PGRU) operates a digital real estate marketplace focusing mainly on Southeast Asian markets (Singapore, Vietnam, Malaysia, Thailand, Indonesia) serving property seekers, real estate agents, property developers, and banks & valuers. Its core business segments are Marketplaces, which is a property listing portal (97% of FY21 revenue), and Fintech and Data Services, which offers mortgage broking products, market intelligence and workflow automation platform (3% of FY21 revenue).

Investment Highlights

We Initiate coverage with a BUY rating and a target price of US$5.73 based on DCF valuation, with a WACC of 10.1% and terminal growth of 3%.

REVENUE

PGRU posted S$101mn in revenue for FY21 – increasing 23% YoY, with 97% of its total revenue coming from its Marketplaces segment and 3% from its Fintech & Data Services segment (Figure 1).

Marketplaces: Marketplaces is PGRU’s main business segment where it operates an online property classified listing portal. The platform allows property buyers/tenants to look for and real estate agents/developers to list available properties and new developments. PGRU earns revenue by: 1) charging property agents tiered annual subscription fees in Singapore, Malaysia, Thailand, and Indonesia; 2) per listing fees in Vietnam; 3) additional fees for optional features and add-ons across all markets; 4) charging developers digital advertising fees; and 5) software-as-a-service (SaaS) sales for process automation solution.

The main metrics used to track performance in this segment are Average Revenue per Agent (ARPA) and Average Revenue per Listing (ARPL). ARPA is applicable for agent revenues across all markets, except Vietnam, while ARPL is applicable for agent revenues specifically only for Vietnam.

Revenue from this segment was S$97.9mn for FY21, increasing 21% YoY. Singapore was the biggest contributor to the segment, making up 57% of the Marketplaces revenue, followed by Vietnam making up 19% (Figure 1). Singapore ARPA has increased quarter-on-quarter (QoQ) driven by increase in premium product adoption and subscription price in 4Q21 while Vietnam’s ARPL also grew QoQ as a result of increase in number of listings and penetration of premium services.

Fintech & Data Services: Launched in FY20, PGRU’s Fintech segment provides mortgage brokering services, which currently is available only in Singapore, by matching home buyers with suitable mortgages that are advertised by banks. The company has referral arrangements with major banks in Singapore and it earns revenue by: 1) charging financial institutions commissions on mortgage fulfillment; and 2) digital advertising fees.

Aside from mortgage brokering, PGRU also has data & software business (Data Services) where it provides B2B clients (including property valuers, banks, developers, agencies, auditors and consultancies) access to its proprietary information on the real eastate market and workflow automation solutions. Revenue is earned by charging clients subscription fees for platform usage.

Mortgage brokering business performance is measured by the amount of take rate, while the data services business is measure by the average price charged per consumer. Both Fintech and Data Services segments combined for a revenue of S$2.9mn in FY21, growing 179% YoY.

Revenue Growth: We forecast total revenue for FY22e to hit S$145mn, which would represent a 44% YoY growth, mainly driven by PGRU’s dominant presence that would enable it to continue capture demand, especially from new property agents entering the industry, and its strong pricing power coupled with high subscription renewal rate. Growth is also driven by agents’ increased adoption of premium subscription tiers and spending on discretionary products.