Downgrade to ACCUMULATE with a lower target price of S$0.55 (prev. S$0.88).

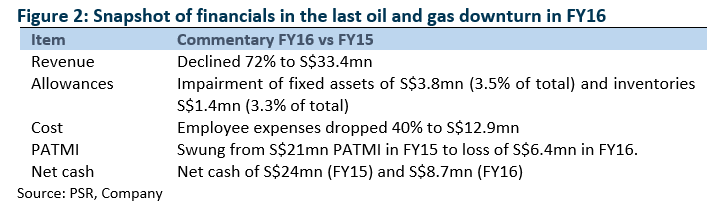

The biggest worry will be trade receivables and inventory of vessels built to stock. During such a stressed environment, the risk will be elevated from customers defaulting payments and inventory becoming unsold. In 2016 downturn, Penguin swung into losses and revenues plunged by 72% (Figure 2). The difference in this cycle is the larger net cash on the balance sheet (from S$24mn end 2015 to S$60mn end 2019) and a more diverse portfolio of vessels built.

With such an uncertain earnings outlook, we will use price to book as a gauge to valuations.

The 10-year price to book average is 0.7x, with a range of 0.5x to 1x. Penguin can ride out the downtrend in the industry with their large cash hoard.

The Positives

+ Net cash at a record $59.8mn or up 44% YoY. The cash represents 40% of the market capitalization. The high cash levels will enable Penguin to increase its build-to-stock vessel inventory. Cash from operations in FY19 more than doubled to S$30.6mn despite higher working capital needs, driven by higher inventory levels.

+ Orderbook proxy* doubled YoY to S$86.8mn. The doubling of inventory to S$42mn was attributed to an increase in build-to-stock vessels such as security boats, crewboats, windfarm vessel and ferries. The build-up of inventory is not an indication of excess stock but rather padding inventory in anticipation of sales. We think that the rise in other payables is driven by customer deposits for these vessels. It is indicative of the likelihood of a buyer for the inventory on hand.

*Recall that the company does not disclose the order book. We built an orderbook proxy using the combined value of inventory (vessels built to stock), held for sale assets (crewboats converted to security vessels for sale) and other payable (largely non-refundable customer deposits).

The Negative

- Charter growth was slower. Charter revenue was weaker than expected., only up 0.8% YoY. We believe charter revenues were hurt by the company’s preference to renew their fleet by selling older vessels (any gains recorded as under other income) and replacing the fleet with new builds. We expect the higher capex of S$22.2mn will go towards supporting the renewal of the existing fleet of crewboats (Flex-42X).

Outlook

The drivers to growth for Penguin are intact.

Maintain BUY with a lower target price of S$0.88 (previously S$0.93)

We maintain our BUY recommendation. We find the current valuations attractive at 3x PE (excluding cash), strong balance sheet and visible growth outlook for FY20e. Our target price is based on 5x PE FY20e (excluding cash and interest income). The industry had traded at an average of 5x PE in previous shipping building cycle. As charter income improves, there will be more scope to raise the valuation multiples, in our opinion. Charter income is more recurrent, scalable and enjoys higher margins. Penguin has cost and service advantages in charter business as designer, builder and operator. Our target price is lowered as FY20e earnings is reduced by 12%. We reduced our charter income estimates for FY20e.

The Positives

+ Revenue growth for both business segments. The more recurrent chartering revenue rose 16% YoY whilst shipbuilding revenue jumped 65% YoY. Penguin is looking to build up their charter fleet as it mentioned that charter rates and utilisation rates are improving.

+ Net cash at a record S$53.1mn. Net cash on hand stands at S$53.1mn, which is a record for Penguin. The cash constitutes 1/3 of the market capitalization and can support Penguin’s build to stock of vessels.

+ Inventory, assets held for sale and other payables rose a combined 14% YoY to S$61mn. As mentioned before, there is no order book disclosed. We use the combination of these three balance sheet items as a proxy to the status of the order book. The 20% YoY jump in inventory would suggest strong shipbuilding revenues for the next quarter, in our opinion.

The Negative

- Assets held for sale was zero. This implies no crewboats for conversion and other income will be light in the coming 4Q19e.

Outlook

Based on the status of the balance sheet, the outlook appears positive. Inventories at record levels are oddly positive. Management is conservative and builds to stock when there is sufficient visibility in orders. Inventory comprises of security boats, crewboats, passenger ferries and offshore windfarm crew transfer vessels (new category for Penguin). The two key oil and gas vessel markets for Penguin is Malaysia and Nigeria. After a lull, offshore rigs deployed in both countries is back to 4-year highs.

Maintain BUY with a higher target price of S$0.93 (previously S$0.61).

Sources of growth for Penguin is several: (i) tailwind from the recovery in oil and gas offshore activity; (ii) replacement of helicopters to crewboats; (iii) penetration into new vessel types (namely patrol boats, offshore wind farm support vessels and fire and safety vessels). Excluding cash, the stock is trading at PE of 3x FY20e.

The Positives

+ Shipbuilding revenue tripled during the quarter. Revenue was from the sale of ferries, security boats, patrol boats and fireboats. Other income declined due to fewer conversion and sale of crew boats into security boats. Charter income from crewboats grew on the back of an expanded fleet and higher charter rates. The company will be replacing older crew boats with their new Flex-42X series. The company has around 16 crew boats and could raise this to 20.

+ Strong balance sheet with net cash of S$43.8mn. The company exited end-June 2019 with net cash of S$43.8mn. In 1H19, cash from operations jumped by S$12.2mn. Bulk of the cash has been spent on expanding the crew boat fleet.

+ Inventory, assets held for sale and other payable rose a combined 46% YoY to S$55mn. Ironically having a large current asset/liabilities balance is positive for the company - higher inventories imply more vessels built to stock available for sale, higher assets held for sale would suggest the pending sale of converted crew boat; and when other payables rise, we are assuming an improvement in non-refundable deposits from clients.

The Negative

- Administrative expenses rose 30% YoY. The rise was in part due to the increase in headcount. We believe the company has been building up the product development team to expand the range of vessels that they can build.

Outlook

Without disclosing the order-book, we use the balance sheet as a precursor to the orders on hand. The key items on the balance-sheet (inventory, assets held for sale) point to a healthy order book for 2H19.

Maintain BUY with an unchanged target price of S$0.61.

We maintain our earnings forecast and target price. Penguin is riding on strong growth as it expanded shipbuilding expertise from merely crew/security boats into ferries, patrol boats and fire and safety vessels. Other drivers include competitors exiting or downsizing, recovery in oil and gas capital expenditure and crew boats replacing the more expensive helicopter mode of transport. Excluding cash, the stock is trading at PE of 3.5x FY19e.

Company Background

In 1995, Penguin International Ltd (Penguin) built its first aluminium boat. Listed on the SGX in 1997, it has since built more than 200 high-speed aluminium vessels, including 120 of its trademark Flex crewboats/security boats. The boats are sold under the Flex brand. Penguin has two shipyards, Tuas (Singapore) and Batam (Indonesia). A major milestone was reached when it sold its regional passenger ferrying ticketing business in 2011 to Sindo Ferry. This was a loss-making business which was highly exposed to fuel price volatility and intense competition.

Almost 80% of Penguin’s revenue now comes from shipbuilding and ship repair. The remaining 20% of revenue is from charter income. Penguin owns 15 crewboats for charter income and several passenger ferries, harbour launches and a landing craft for special projects in Singapore. The common feature of all Penguin boats is the aluminium material and the speed. Such boats can travel as fast as 30 knots as compared to 10-12 knots by a steel vessel of similar specifications. Penguin’s business model revolves around constructing vessels for their stock programme (i.e. built without an order). In addition, Penguin will opportunistically dispose crewboats on charter after converting them into security vessels when the prices are attractive.

Investment Merits

Outlook

We are positive on its outlook. The strong balance sheet has helped Penguin weather the offshore and marine downcycle of 2015-17. Several competitors have either exited the business or fallen under debt restructuring. The current upturn in oil prices and offshore rig activity is another positive for the company. We also see Penguin diversifying outside its primary oil and gas vessels into other categories, including government and offshore windfarm vessels.

Initiating coverage with BUY rating and target price of S$0.61

We initiate Penguin with a BUY and a target price of S$0.61. We value Penguin at 5x PE, excluding its S$41mn net cash. Shipyards of similar size traded at 5x PE on average back when the industry was in at steady state.

Revenue

Shipbuilding (77% of FY18 revenue): Penguin builds crewboats, security vessels, ferries and patrol boats. In recent years, it has ventured into constructing patrol boats and fire and rescue vessels. Vessels can either be built-to-order or built-to-stock. For the former, revenue is recognised on a percentage of completion method. Penguin does not disclose its order books. Built-to-stock ships are parked as inventory before disposal. The average selling price of a security boat is around US$5mn. In 2018, 59% or S$48mn of revenue was from the sale of stocked Flex crewboats/security boats. The balance S$33mn were newbuild orders.

Ferry and charter income (23% of FY18 revenue): Charter income from 30 vessels: 15 are crewboats and the rest specialised vessels utilised in Singapore for ferry support, landing craft and harbour motor launch. Its crew boats are deployed in Malaysia, mainly by the oil and gas industry to transport crews from shore to rigs or between rigs. Spot rental is US$4,000-5,000 per day. Most are rented for 180 days with a few under-3-year charters that come with lower rates. We expect the company to expand their fleet as demand is improving. Penguin also sells its crewboats as security vessels when prices are attractive. Gains are recognised as other income. In 2018, Penguin sold 3 Flex crewboats, which were converted into security vessels.

Types of boats built by Penguin:

The common feature of all these boats is the aluminium design and speed. We believe the capacity of the yard is 30 to 40 vessels per year. It requires 7 to 8 months to build a crewboat. Challenges in building aluminium vessels are the hull form design, weight management, space planning and selection of equipment, machinery and material.

Cost

Charter costs include the costs of crew on board (around eight per vessel) and vessel maintenance. Fuel costs are borne by customers. The largest cost component of crewboats is the engine. For instance, three Caterpillar C32 ACERT engines are required in one crew boat.

Cash-flow

Recurrent cash flow is derived from its chartering business. In shipbuilding, customers place 10-30% deposits upfront when they place orders. Built-to-stock vessels, once completed, are recognised as inventory. They are recognised as sales upon delivery and full payment. Penguin will build vessels for stock only with cash in hand and when they are not geared up.

Balance Sheet

Asset composition: plant and equipment 40% (buildings, motor launches, machinery), cash 20%, inventory 10%, trade receivables 10% and contract assets 7%. Contract assets are vessel-building costs yet to be recognised as revenue. There is also an original S$8mn invested in SGX-listed Marco Polo Marine. Its value had been written down to S$5.1mn as at end-December 2018.

Liabilities composition: 44% are other payables and accruals (bulk are accrued operating expenses and deposits received) and 33% is trade payables.

Industry

Since 2008, the top five largest aluminium crew boat manufacturers in the world are Penguin, Grandweld (Dubai), Strategic Marine, Marsun and NGV Tech. Of the top 10, around one-third are being liquidated or under some form of restructuring. These include Strategic Marine (owned by Triyards), NGV Tech and Nautic Africa. Meanwhile, competitors in ferry construction are Cochin Shipyard, Damen Shipyards (Netherlands), Grandweld and L&T.

In 2014-18, around 192 aluminium (30m to 50m-length) crewboats and crew/supply vessels were built globally. Around 68 were from Penguin’s yards. In 2014, there were 78 of such boats built. This dwindled to only 9 and 16 units in 2017 and 2018, respectively. Penguin’s share of all such vessels built in 2017/18 was 60%, the single largest market share.

Outlook

We are positive on Penguin’s outlook.

Firstly, improving oil prices have fuelled a revival in offshore activity. The number of offshore rigs globally has recovered from their low at end-2017 (Figure 7). The recovery is visible in countries where Penguin has a large presence, namely, Nigeria and Malaysia (Figure 8).

Secondly, the net cash balance sheet has allowed Penguin to weather the 2015-17 vicious oil and gas downturn. Several major competitors have left or downsized their activities. Over the past two years, Penguin has captured a large share of the crewboat and security boat market.

Thirdly, Penguin is securing more orders outside its crewboat and security boat business. It has successfully diversified outside this core business to secure new orders from patrol boats, offshore vessels and rescue and fire safety vessels.

Build-for-stock is not applicable for every type of vessel. It carries the risk of inventory overhang. For this model to work, the vessel must have a robust and ongoing demand. The advantage for such models are the higher margins and ability for customers to secure their vessels faster and in turn, expedite their own charter income.

Investment Merits

Valuation

We initiate coverage on Penguin with a BUY rating. As there are very few direct comparables, we use the PE ratios of two Singapore yards when the shipbuilding cycle was in a steady state cycle. During the normalised shipbuilding cycle of 2012-15, both Triyards (Figure 9) and Nam Cheong (Figure 10) traded at an average 5-8x PE. Although, they build different vessels and have more geared balance sheet profiles, both can be considered proxies for Penguin as their yard sizes are similar. We used the lower PE average of 5x to value the business and added back the net cash from FY19e.