The Positives

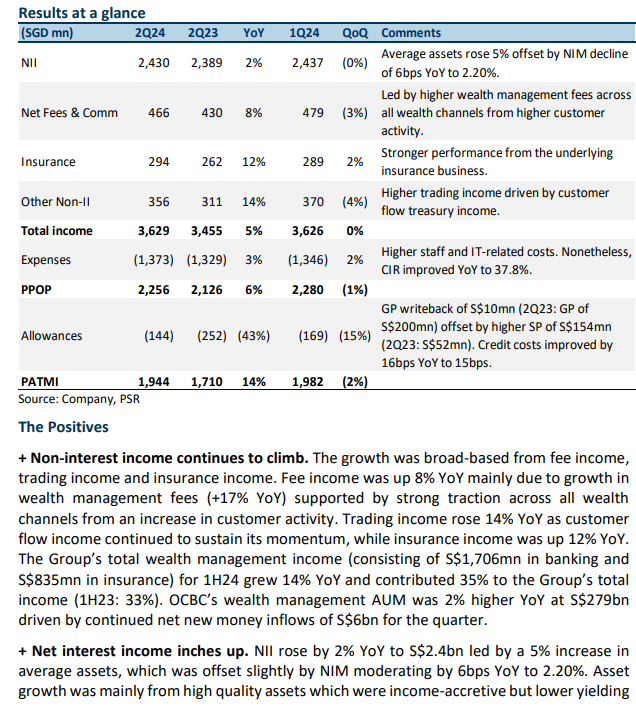

+ Non-interest income rises 17% YoY. The growth was broad-based from fee income, trading income and insurance income. Fee income was up 6% YoY mainly due to growth in wealth management fees (+20% YoY) offset slightly by lower loan and trade-related fees (-6% YoY), lower brokerage and fund management fees (-5% YoY) and stable investment banking fees. Trading income rose 45% YoY to a quarterly high of S$370mn from record customer flow income and improved non-customer flow income, while insurance income was up 13% YoY. The Group’s total wealth management income (consisting of S$873mn in banking and S$416mn in insurance) for 1Q24 grew 19% YoY and contributed 36% to the Group’s total 1Q24 income (1Q23: 32%). OCBC’s wealth management AUM was 1% higher YoY at S$273bn driven by continued net new money inflows of S$6bn for the quarter.

+ Net interest income up slightly. NII rose by 4% YoY to S$2,437mn; the growth was led by a 5% increase in average assets, which was offset slightly by NIM moderating by 3bps YoY to 2.27%. NIM moderation was mainly from higher funding costs, which offset the increase in asset yields. Loans grew 2% YoY to S$297bn from an increase in both corporate and consumer loans, mainly in Singapore. OCBC has provided FY24e guidance for NIM to be at the higher end of 2.20% to 2.25%, with 1Q24 exit NIM currently at 2.27%.

The Negatives

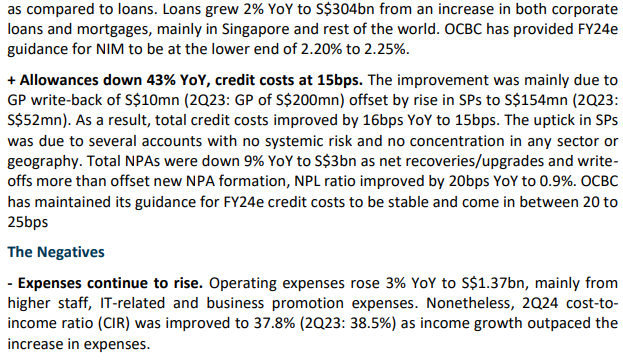

- Allowances up 54% YoY, credit costs at 16bps. Total allowances rose 54% YoY to S$169mn mainly due to a rise in SPs to S$180mn (1Q23: S$56mn) offset slightly by GP write-back of S$11mn (1Q23: GP of S$54mn). As a result, total credit costs rose from 4bps YoY to 16bps. The uptick in SPs was due to several accounts in ASEAN with no systemic risk and no concentration in any particular sector or geography. Total NPAs were down 9% YoY to S$3bn as net recoveries/upgrades and write-offs more than offset new NPA formation, NPL ratio improved by 10bps YoY to 1.0%. OCBC has maintained their guidance for FY24e credit costs to be stable and come in between 20 to 25bps.

- Expenses continue to rise. Operating expenses rose 8% YoY to S$1.35bn, mainly from higher staff costs due to higher variable compensation associated with income growth. Nonetheless, 1Q24 cost-to-income ratio (CIR) was stable YoY at 37.1% as income growth outpaced the increase in expenses. OCBC is guiding for CIR of around 40 to 45% for FY24e as costs are expected to grow while income moderates, resulting in higher CIR.

The Positives

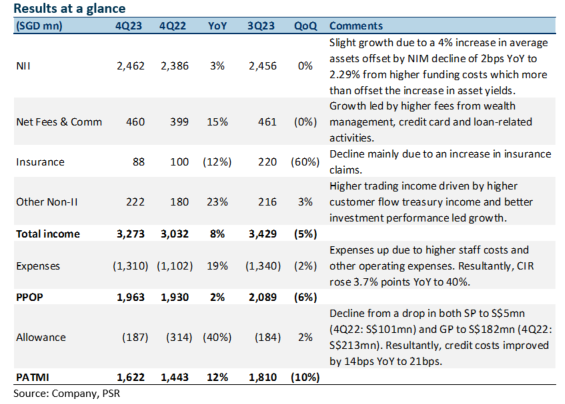

+ Net interest income grew 3% YoY. NII growth was led by a 4% increase in average assets, which was offset by NIM moderating by 2bps YoY to 2.29% and stable loan growth. NIM moderation was mainly from higher funding costs, which offset the increase in asset yields. OCBC has provided FY24e guidance for NIM to be in the range of 2.20% to 2.25%, with FY23 exit NIM currently at 2.26%.

+ Fee income continues to grow. Fee income rose 15% YoY to S$460mn. This was due to the broad-based growth in wealth management fees from increased customer activities, higher credit card fees, and loan and trade-related fees. Furthermore, the Group’s FY23 wealth management income grew 26% YoY to S$4.3bn and contributed 32% to the Group’s total income FY23 (FY22: 30%). OCBC’s wealth management AUM was 2% higher YoY at S$263bn driven by continued net new money inflows.

+ Allowances are down 40% YoY, and credit costs are at 21bps. Total allowances fell 40% YoY to S$187mn as SPs fell to S$5mn (4Q22: S$101mn) and GPs dipped to S$182mn (4Q22: S$213mn). Resultantly, total credit costs improved by 14bps YoY to 21bps. Total NPAs were down 16% YoY to S$2.9bn as new NPA formation fell 78% YoY to S$54mn, and the NPL ratio improved by 20bps YoY to 1.0%. Full-year FY23 credit costs were higher at 20bps (FY22: 16bps) from both impaired and non-impaired assets. OCBC has guided for FY24e credit costs to be stable and come in between 20 to 25bps.

The Negatives

- Insurance income down 12% YoY. Insurance income fell 12% YoY to S$88mn, driven by higher claims in Singapore and Malaysia, partially offset by higher contributions from the Singapore life business arising from better investment performance. FY23 total weighted new sales fell 12% YoY to S$1.66bn, as sales in Singapore declined, while new business embedded value (NBEV) declined 11% YoY to S$762mn. Margins saw a slight increase due to a more favorable product mix. Nonetheless, FY23 profit contribution from insurance rose 30% YoY to S$636mn, led by improved investment income.

- Expenses creep up. Operating expenses rose 19% YoY to S$1.31bn, mainly from higher staff costs and other operating expenses. The rise in staff costs was led by annual salary adjustments, headcount growth, and one-off support to help junior employees cope with rising cost-of-living concerns. Resultantly, the 4Q23 cost-to-income ratio (CIR) rose 3.7% points YoY to 40%. Nonetheless, full-year FY23 CIR improved by 4.2% points YoY to 38.7% as the rise in income outpaced the rise in expenses.

- CASA ratio continues to dip. The Current Account Savings Accounts (CASA) ratio fell 3.1% points YoY to 48.7% due to the high-interest rate environment and a continued move towards fixed deposits (FD). Nonetheless, total customer deposits grew 4% YoY to S$364bn, underpinned by strong growth in FDs. The Group’s funding composition remained stable with customer deposits comprising 81% of total funding.

The Positives

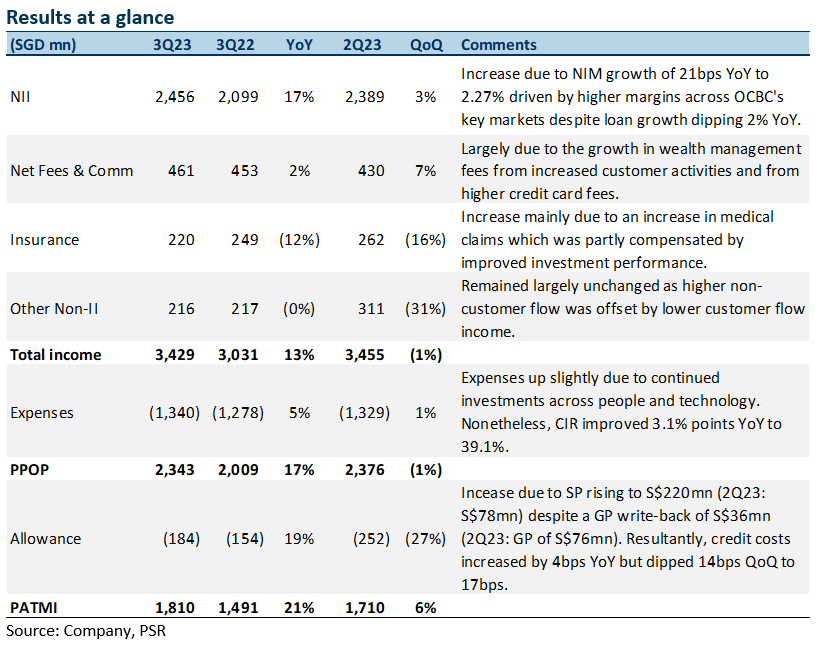

+ Net interest income grew 17% YoY. NII grew 17% YoY led by NIM improvement of 21bps YoY to 2.27% despite loan growth dipping 2% YoY. NIM expansion was mainly driven by higher margins across the Group’s key markets. However, NII only rose 3% QoQ as NIM rose 1bps QoQ as a rise in asset yields more than outpaced the increase in funding costs. Nonetheless, OCBC has increased its NIM guidance for FY23e from above 2.20% to around 2.25%.

+ Fee income grew to highest level in 4 quarters. Fee income rose 2% YoY to reach the highest level in 4 quarters. This was due to the growth in wealth management fees from increased customer activities, and from higher credit card fees. Furthermore, the Group’s wealth management income grew 16% YoY to S$1.12bn and contributed 33% to the Group’s total income in 3Q23. OCBC’s wealth management AUM was 8% higher YoY at S$270bn driven by continued net new money inflows.

The Negatives

- Insurance income down 12% YoY. Insurance income fell 12% YoY from an increase in medical claims, which was partly compensated for by improved investment performance. Nonetheless, total weighted new sales rose 5% YoY to S$419mn, driven by higher sales in Singapore, while new business embedded value (NBEV) was at S$184mn for the quarter.

- Allowances up 19% YoY, credit costs at 17bps. Total allowances rose 19% YoY to S$184mn as SPs grew to S$220mn (2Q23: S$78mn) partially offset by a GP write-back of S$36mn (2Q23: GP of S$76mn). The higher SP was from corporate accounts in various sectors and geographies all over ASEAN, and not to any specific account. OCBC said that it does not see any systemic risk. This drove credit costs up by 4bps YoY to 17bps. Total NPAs were down 16% YoY to S$3.1bn, and the NPL ratio improved by 20bps YoY to 1.0%. Notably, the rest of the world's NPAs rose 46% YoY to S$585mn, mainly due to the downgrade of one network corporate account in ASEAN in the construction sector.

- CASA ratio continues to dip. The Current Account Savings Accounts (CASA) ratio fell 9.8% points YoY to 46.3% due to the high interest rate environment and a move towards fixed deposits (FD). Nonetheless, total customer deposits increased 5% YoY to S$369bn underpinned by strong growth in FDs. The Group’s funding composition remained stable with customer deposits comprising 80% of total funding.

Outlook

Loan growth: Loan growth declined YoY in 3Q23, falling below the bank’s guidance for FY23e. However, management said that it expects a slower pace of economic growth and has lowered its guidance from low to mid-single to low-single-digit loan growth for FY23e. Management also sees further lending opportunities in the wholesale segment and sustainable financing. Mortgage pipelines in Singapore and Hong Kong are also healthy, with more drawdowns expected in the rest of FY23.

Fee income: With the re-opening of China, OCBC is positive on the broader outlook and expects the re-opening to support China-Southeast Asia trade and investment flows. OCBC has recently launched a private banking unit in Malaysia and mainland China to strengthen its WM services while also hiring for the business. We could expect high single-digit fee income growth for FY23e.

Commercial real estate office sector: Commercial real estate office sector loans are mostly to network customers in key markets with a proven track record and financial strength. Overall LTVs are low at around 50% to 60% and are mostly secured. Overall, the commercial real estate office sector loans make up 13% of the total loan book, with two-thirds of loans to key markets of Singapore, Malaysia, Indonesia, and Greater China. Loans to developed markets including Australia, the United Kingdom, and the United States are largely to network customers with strong sponsors.

The Positives

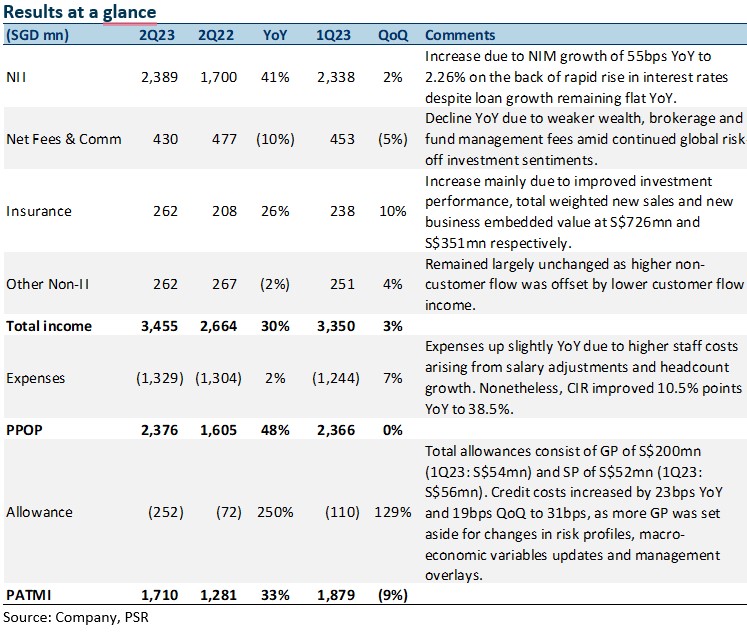

+ Net interest income surged 41% YoY. NII grew 41% YoY led by NIM improvement of 55bps YoY to 2.26% despite loan growth remaining flat YoY. NIM expansion was mainly due to the continued and rapid rise in interest rates during the year. However, NII rose only 3% QoQ as NIM declined 4bps QoQ as asset growth was partly offset by the lower NIM as higher funding costs outpaced the rise in loan yields. Nonetheless, OCBC has increased its NIM guidance for FY23e from 2.20% to above 2.20%.

+ Insurance income up 26% YoY. Insurance income grew 26% YoY and 10% QoQ. The growth was mainly attributable to improved investment performance and the adoption of SFRS(I) 17 reporting standard. Total weighted new sales and new business embedded value (NBEV) were S$726mn and S$351mn respectively, while NBEV margin improved to 48.4% (2Q22: 37.1%) due to favourable product mix.

The Negatives

- Fee income declined YoY and QoQ. Fee income declined 10% YoY and 5% QoQ as higher loan-related and investment banking fees were offset by softer wealth management-related fees from a decline in customer activities amid a risk-off investment environment. Nonetheless, the Group’s wealth management income grew 56% YoY to S$1.14bn (2Q22: S$729mn) and contributed 33% to the Group’s total income. OCBC’s wealth management AUM was 10% higher YoY at S$274bn (2Q22: S$250bn) driven by continued net new money inflows.

- Allowances up 250% YoY, credit costs at 31bps. Management set aside 31bps of credit cost for 2Q23 (1Q23: 12bps), the second highest in six quarters, even though asset quality is still benign, with new NPAs during the quarter only at S$289mn (1Q23: S$174mn) and NPL ratio at 1.1%. 2Q23 total allowances rose 250% YoY mainly due to an increase in GPs, which were mainly set aside for changes in risk profiles, macro-economic variables updates and management overlays (40% of GP or ~S$1bn). Notably, rest of the world NPAs rose 84% YoY to S$549mn mainly due to the downgrade of a corporate account in the Commercial Real Estate sector in the US, for which OCBC sees no systemic risk.

- CASA ratio continues to dip. The Current Account Savings Accounts, or CASA ratio, fell 15.6% points YoY to 45.3% due to the high interest rate environment and a move towards fixed deposits, FDs. Nonetheless, total customer deposits increased 7% YoY to S$372bn underpinned by strong growth in FDs. The Group’s funding composition remained stable with customer deposits comprising 79% of total funding.

Outlook

Loan growth: Loan growth was flat YoY in 2Q23, falling below the bank’s guidance for FY23e. However, management said that it expects a slower pace of economic growth and has maintained its guidance of low to mid-single loan growth for FY23e. Management also sees further lending opportunities in the wholesale segment and sustainable financing. Mortgage pipelines in Singapore and Hong Kong are also healthy, with more drawdowns expected in the rest of FY23.

Fee income: With the re-opening of China, OCBC is positive on the broader outlook and expects the re-opening to support China-Southeast Asia trade and investment flows. OCBC has recently launched a private banking unit in Malaysia and mainland China in order to strengthen its WM services while also hiring for the business. We could expect high single-digit fee income growth for FY23e.

Commercial real estate office sector: The commercial real estate office sector loans are mostly to network customers in key markets with a proven track record and financial strength. Overall LTVs are low at around 50% to 60% and are mostly secured. Overall, the commercial real estate office sector loans make up 14% of total loan book, with two-thirds of loans to key markets of Singapore, Malaysia, Indonesia, and Greater China. Loans to developed markets including Australia, the United Kingdom and the United States are largely to network customers with strong sponsors. The US accounted for less than 1% of total Group loans and mostly secured by Class A office properties.

The Positives

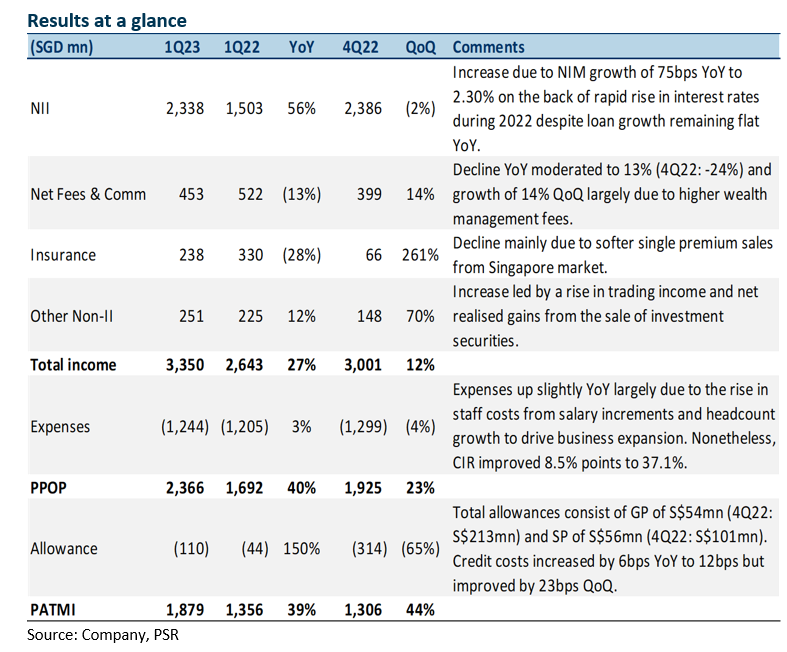

- Fee income YoY decline moderated, up 14% QoQ. Fee income YoY decline of 14% moderated from the previous quarter (4Q22: -24%) and dipped to S$453mn mainly due to a drop in wealth management fees as customer activities were subdued amid risk-off investment sentiments globally. Nonetheless, it saw its first QoQ increase in 6 quarters, growing 14% QoQ mainly driven by higher wealth management fees. The Group’s wealth management income was S$1.10 billion, 33% higher QoQ, and contributed 33% to the Group’s total income. OCBC’s wealth management AUM was higher at S$270bn (1Q22: S$251bn) mainly driven by sustained growth in net new money inflows and positive market valuation.

+ Net interest income surged 56% YoY. NII grew 56% YoY led by NIM improvement of 75bps YoY to 2.30% despite loan growth remaining flat YoY. NIM expansion was mainly due to loan yields rising faster than the increase in funding costs on the back of the rapid rise in interest rates during the year. However, both NII and NIM declined QoQ, the first decline in 6 quarters. This was mainly due to a rise in asset yields being offset by higher funding costs, as well as lower loans-to-deposits ratio as the increase in deposits outpaced that of loans. Nonetheless, OCBC has increased their NIM guidance for FY23e from 2.10% to 2.20%.

+ Trading income up 12% YoY. Trading income grew 12% YoY and 69% QoQ. YoY growth was largely driven by higher non-customer flow income as customer flow income remained flat. QoQ growth was driven by both higher customer and non-customer flow income, as well as higher net realised gains from the sale of investment securities of S$24mn (4Q22: loss of S$67mn).

The Negatives

- Allowances up 151% YoY, credit costs at 12bps. Total allowances fell 65% QoQ but were up 151% YoY to S$110mn. GPs of S$54mn (4Q22: S$213mn) and SPs of S$56mn (4Q22: S$101mn) were made during the quarter. The YoY increase was mainly due to higher allowances set aside for non-impaired assets. Total NPAs were down 5% QoQ and 23% YoY to S$3.33bn, and the NPL ratio improved by 30bps YoY to 1.1%. Credit costs increased by 6bps YoY but improved by 23bps QoQ to 12bps.

- CASA ratio continues to dip. Current Account Savings Accounts (CASA) ratio fell 15.6% points YoY to 47.1% due to the high interest rate environment and a move towards fixed deposits (FD). Nonetheless, total customer deposits increased 5% YoY to S$367bn underpinned by strong growth in FDs. The Group’s funding composition remained stable with customer deposits comprising more than 80% of total funding.

The Positives

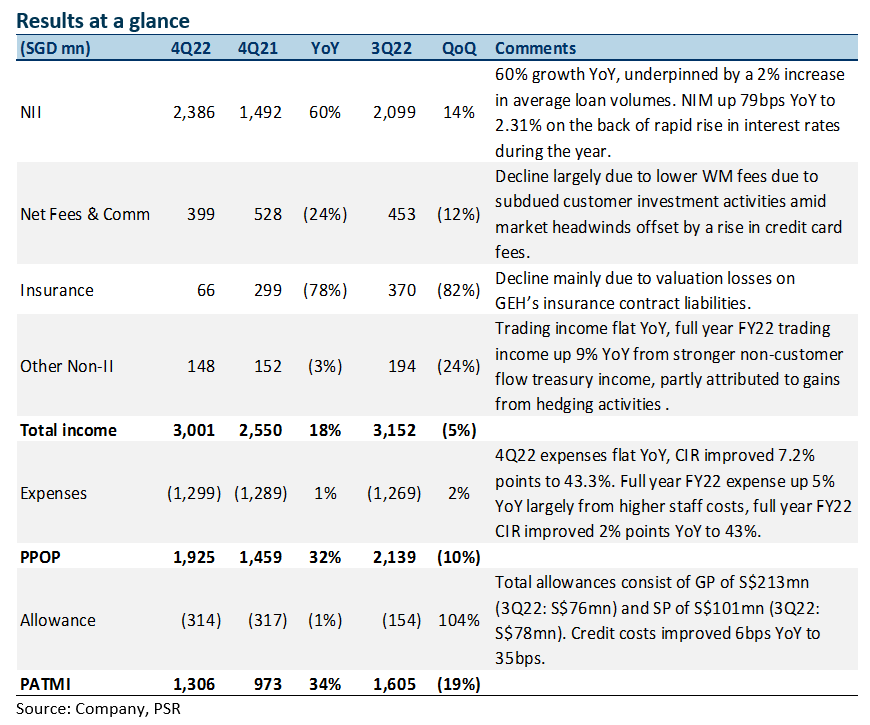

+ Net interest income surged 60% YoY. NII grew 60% YoY led by loan growth of 2% YoY and NIM improvement of 79bps YoY to 2.31%. Loan growth was largely driven by lending in Singapore, Australia, the United States and United Kingdom. NIM expansion was mainly due to loan yields rising faster than the increase in funding costs on the back of the rapid rise in interest rates during the year. OCBC has guided for a NIM in the region of 2.10% for FY23e.

+ Credit cost improved by 6bps YoY. Total allowances fell 1% YoY but were up 105% QoQ to S$314mn. GPs of S$213mn (3Q22: S$76mn) and SPs of S$101mn (3Q22: S$78mn) were

made during the quarter. Total NPAs were down 5% QoQ and 20% YoY to S$3.49bn, and the NPL ratio improved by 30bps YoY to 1.2%. Notably, there was an increase in Greater China NPLs by 21% QoQ mainly due to the downgrade of a corporate relationship in Hong Kong. Nonetheless, OCBC said that it is a fully secured customer with LTV of >60% and the risk is non-systemic and is not related to mainland China real estate. Credit costs improved by 6bps YoY to 35bps due to the better credit environment.

The Negatives

- Fee income fell 25% YoY. Fee income declined 25% YoY to S$399mn mainly due to a drop in wealth management fees as customer activities were subdued amid risk-off investment sentiments globally. Nonetheless, OCBC’s wealth management AUM was higher at S$258bn (4Q21: S$257bn) mainly driven by continued growth in net new money inflows which offset negative market valuation.

- Insurance and trading income fall. Life insurance profit from Great Eastern Holdings fell 78% YoY from lower net valuation gains in its insurance funds experiencing unrealised mark-to-market loss on its insurance contract liabilities. Trading income also fell 2% YoY and largely customer flow treasury income.

- CASA ratio dipped YoY. Current Account Savings Accounts (CASA) ratio fell 11.5% YoY to 51.8% due to the high interest rate environment and a move towards fixed deposits (FD). Nonetheless, total customer deposits increased 2% YoY to S$350bn mainly due to the growth in FDs. The Group’s funding composition remained stable with customer deposits comprising ~83% of total funding.