The Positives

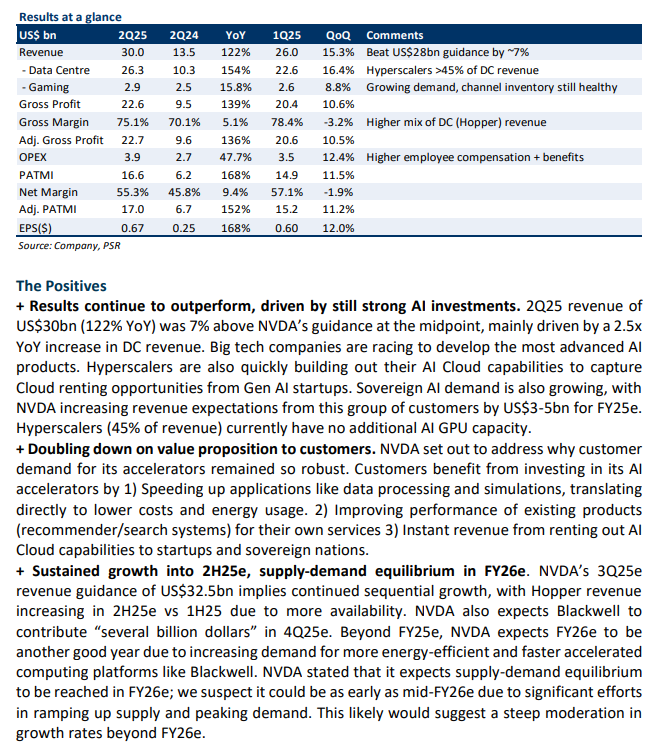

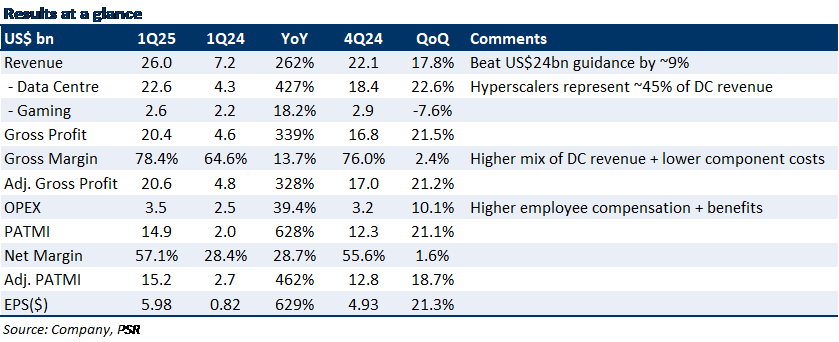

+ Revenue outperformed again, led by 5x YoY growth in Data Centre (Hopper) demand. NVDA’s US$26bn in revenue for 1Q25 outperformed again, beating its own guidance by 9% (US$2bn). Growth more than tripled YoY for a 3rd straight quarter, led mostly by a 5x/3x YoY increase in demand for its DC compute/networking products like Hopper/InfiniBand – from Cloud hyperscalers and consumer internet companies. Inferencing made up ~40% of DC revenue, with sequential DC growth driven by Tesla’s 35K H100 GPUs expansion. NVDA’s gaming segment also grew 18% YoY due to strong end-customer demand for AI PCs equipped with its GeForce RTX GPUs and normalized channel inventory levels.

+ NVDA working hard on increasing supply, 1Q25 results imply ~US$4bn sequential ramp. NVDA’s DC revenue of US$22.6bn implies a sequential increase of ~US$4bn. Given NVDA’s comments on trying to acquire more supply, coupled with current demand-supply dynamics, we assume that most of this came from an increase in chip supply from TSMC. Since 1Q24, DC revenue has also increased sequentially at this US$4bn-US$5bn rate. We expect this rate of increase to continue at least until the end of the year given the 1) current strength in demand and 2) Blackwell shipments beginning in 2Q25e (higher ASPs vs Hopper), which would imply ~US$113bn-US$115bn DC revenue for FY25e – 30% higher than our previous estimates.

+ Aggressive yearly product launch beyond FY25e, low risk of product transition. CEO Jensen Huang reiterated its focus on launching new products at a faster cadence (annually) as it looks to continue outpacing its competitors, announcing a new AI GPU chip after Blackwell that is slated to launch next year officially. Concerns over the risk of customers waiting for newer chips were also alleviated as Hyperscalers average into newer technologies given the early stages of their accelerated compute build-out. In addition, newer platforms like Blackwell are backward compatible, meaning no transitional issues from Hopper.

The Negative

- Nil.

The Positives

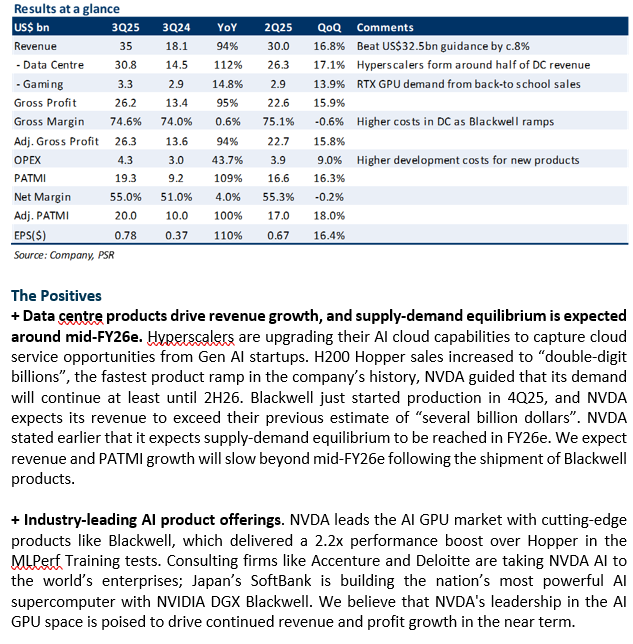

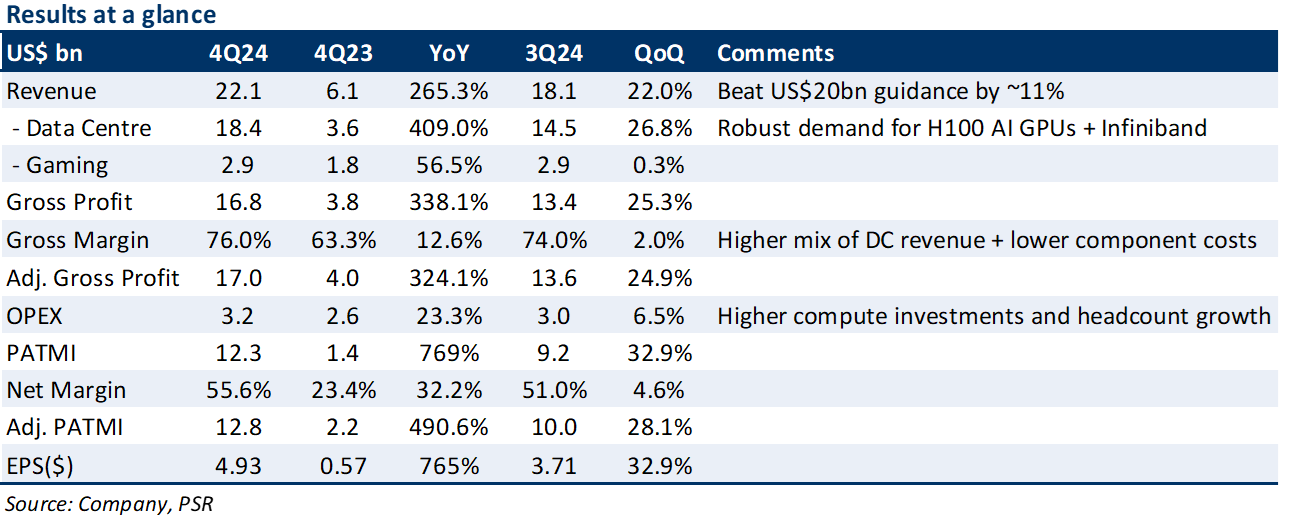

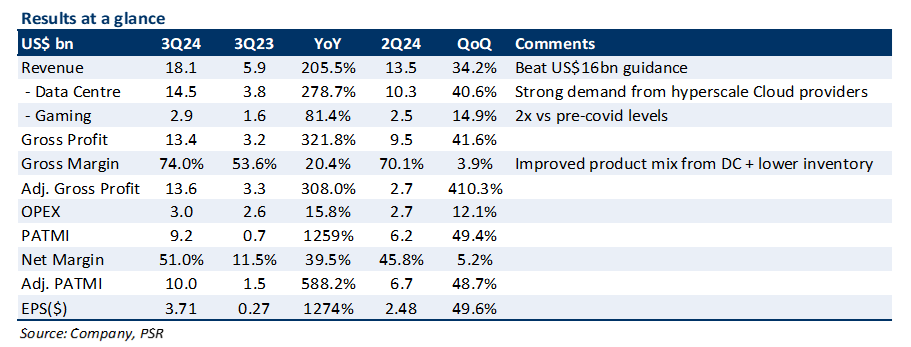

+ AI demand still exceptional, driving outperformance. Revenue of US$22.1bn beat guidance again by ~11%, with most of the outperformance driven by DC gains (409% YoY). Demand from consumer internet companies (META, GOOGL, etc.), Cloud Hyperscalers (CSPs), and sovereign nations remain robust, with NVDA also seeing growth across various industries – auto, healthcare, and financial services. Supply is improving, although it is still unlikely to meet the excess demand for high-spec AI GPUs anytime soon. Near-term demand remains supported by transition to accelerated computing for Gen AI applications (recommender systems), inferencing LLMs (ChatGPT, Gemini, etc.), expanding sovereign AI infrastructure.

+ Gross margin beat by 150bps, forward guidance pointing to more upside. NVDA’s gross margin (76%) continued to improve for the 6th quarter. Driven by higher-margin DC revenue mix (83% of total revenue) and lower component costs, which are expected to flow into 1Q25e, NVDA guided to a 76.3% gross margin. Prior to FY24, gross margins had historically been ~60%. NVDA also guided 1Q25e revenue to US$24bn +/- 2%, implying a 234% YoY improvement driven predominantly by DC (H100 + Infiniband). We expect DC revenue to easily cross US$20bn as NVDA works through improving supply to fulfill its order backlog.

The Negative

- China is still a question mark. US export restrictions were a significant headwind, with DC revenue from China (incl. Hong Kong) dropping to ~5% of total DC revenue in 4Q24 from ~22% in 3Q24. NVDA began shipping its lower-spec H20 GPU chips for market sampling, although management did not seem too optimistic about competing with local Chinese semicon companies like Huawei, given the ceiling imposed on GPU specifications.

Outlook

Guidance: NVDA guided to 1Q25e revenue of US$24bn (+/- 2%), implying a further acceleration in YoY growth. Gross margins were guided to 76.3%, a sequential 30bps expansion due to a more favourable shift in mix to higher-margin DC products and lower component costs. Gross margins are expected to contract for the rest of FY25e to 73-74% as the benefits from lower component costs fade. Operating expenses are expected to increase 40% YoY.

Outlook: Robust near-term growth expectations look sustainable with demand far outpacing supply. NVDA dominates the AI GPU market (~90% market share) with multiple growth drivers from 1) increasing investments from enterprises for training and inferencing LLMs, deep learning, recommender systems, and generative AI applications; 2) hyperscale CSPs expanding into new market opportunities; 3) sovereign nations building their own AI infrastructure to; and 4) growing AI adoption across multiple industries – auto, healthcare, industrial, telco, etc. In addition, NVDA has a strong product lineup for FY25e (H200, B100, Spectrum-X, etc.), each of which are expected to drive incremental growth in ASPs and margins.

The main risks to growth remain: 1) inability to compete with other Chinese manufacturers on its H20 chips, market share may be permanently lost; 2) insufficient supply to meet the growing demand for high-end GPUs and components as the world transitions towards higher accelerate computing.

RULE OF 40

The “Rule of 40” was first introduced as a benchmark to measure the balance between the growth and profitability of SaaS companies, taking into account both revenue growth as well as profitability (Revenue Growth + EBITDA Margins), with the addition of both metrics needing to exceed the 40% threshold. We have modified this slightly by averaging revenue growth over a

3-year period compared with just a single period growth rate. Adding together NVDA’s 3-year average revenue growth of 54% and its EBITDA margin of 63%, the total of 117% is more than our required threshold of 40% (Figure 2).

Maintain BUY with a raised target price of US$970 (prev. US$685)

We raise our FY25e revenue/PATMI by 29%/35% to reflect continued demand for Data Centre products. NVDA dominates (~90% share) AI GPUs that are growing 5x YoY, with demand driven by a global shift to accelerated computing for more intense workloads (Gen AI/LLMs). We maintain a BUY rating with a raised target price of US$970 (prev. US$685) as we roll over an additional year of valuations. Our WACC/g is unchanged (6.8%/4.5%).

The Positives

+ Demand for Data Centre GPUs still outpacing supply. DC growth continues to be driven by: 1) Increased investments from consumer internet companies into inferencing LLMs and generative AI applications; 2) Hyperscale CSPs expanding into new market opportunities; 3) 5x YoY increase in demand for InfiniBand (Networking >US$10bn annual run-rate). To meet the demand, NVDA has been increasing supply QoQ this year, and expects to continue this into FY25e. DC revenue spiked 280%/41% YoY/QoQ as a result. We expect near-term demand to remain strong given overflowing customer commitments.

+ 4Q24e revenue guidance implies 231% YoY growth. NVDA guided US$20bn (+/- 2%) in revenue for 4Q24e, implying further acceleration in revenue growth – above consensus estimates of US$18bn. Most of the growth is expected to be driven by DC demand, and takes into account a significant drop in revenue contribution from China due to US export controls. Taking this guidance, our FY24e revenue is raised 13% to US$59bn, implying a 118% YoY growth. 4Q24e gross margins are also expected to increase sequentially to 74.5% due to a favourable product mix as demand for higher margin DC products continue to expand, with NVDA ending FY24e with a 72% gross margin, 1500bps higher than FY23.

The Negative

- Export controls expected to impact China revenue in 4Q24e. US government export control regulations to China are expected to impact revenue from China moving forward, with limited visibility on its long term impact. NVDA is working on regulation-compliant products for the affected markets, although the contribution from these products is not expected to be meaningful in the near term. China revenue represents 20-25% of NVDA’s total revenue.

Outlook

Guidance: NVDA guided to 4Q24e revenue of US$20bn (+/- 2%), implying a further acceleration in YoY growth as demand for its DC products is extremely robust. NVDA also guided a gross margin of 74.5%, a sequential 50bps expansion due to a more favourable shift in mix to higher-margin DC products.

The Positives

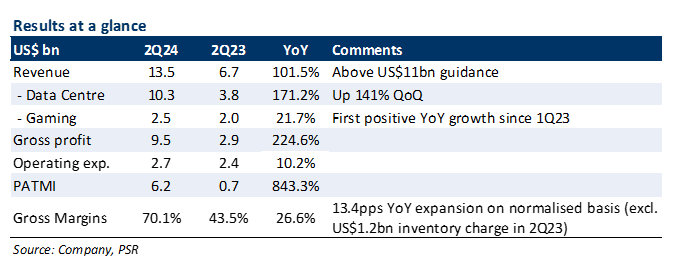

+ Data Centre driving strong revenue beat. Revenue doubled YoY to US$13.5bn, beating company guidance of US$11bn. The strong performance was attributed to Data Centre business surging by 171% YoY to make up 76% of total revenue, driven by accelerating demand from cloud service providers and consumer internet companies for NVDA’s HGX server platform. Data Centre growth mainly came from US customers, while China makes up 20-25% of the segment’s revenue, in line with historical trends. Gross margins also expanded by 550bps QoQ and 26.6pps YoY as a result of larger revenue contribution from the server business.

+ An even stronger 3Q24 guidance. NVDA guided for a revenue of US$16bn (+/- 2%), a potential 170% YoY jump, largely driven by Data Centre strength as customers continue to focus their investments on generative AI and accelerated computing. NVDA said this allows it to have demand visibility that extends into CY2024. As such, the company is working with suppliers to expand production capacity, and will be increasing supply over the next several quarters to fulfill the demand. Gross margins are expected to be at 71.5% (+/- 50bps), another strong 17.9pps YoY expansion.

+ Gaming returns to positive growth. Sales was up by 22% YoY, the first positive growth following 4 consecutive quarters of YoY decline. The increase was fueled by the solid end-customer demand for the GeForce RTX 40 Series GPUs, partly driven by the back-to-school season. NVDA believes the global end demand has returned to growth following the slowdown in CY2022. Furthermore, it also believes the segment has a large upgrade opportunity as only 47% of its installed base are on GPUs equipped with its RTX technology.

The Negatives

- Professional Visualisation down YoY, Automotive down QoQ. Professional Visualisation (3% of revenue) declined by 24% YoY, but contraction has moderated significantly from the -53% in 1Q24. In Automotive, revenue was up by 15% YoY to US$253mn, but was down 15% QoQ due to the lower overall demand from Chinese OEMs.

The Positives

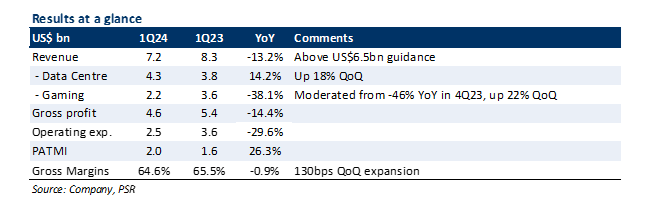

+ Revenue beat company guidance. Revenue was down 13% YoY to US$7.2bn, but this was above company guidance of US$6.5bn. The better-than-expected performance was driven by 14% YoY growth in Data Centre sales, which set a new record of US$4.3bn. NVDA attributed the growth to the surge in demand across its customer base (cloud service providers, consumer internet, and enterprises) who are looking to harness the technology of generative AI and large language models (LLMs) that use the company’s Hopper and Ampere GPUs.

+ Strong 2Q24 guidance. NVDA guided for a revenue of US$11bn (+/- 2%), which is ~53% above consensus estimates of US$7.2bn, and represents a 64% YoY growth, following YoY sales contraction since 3Q23. The company said the growth will largely be driven by its Data Centre business benefiting from the steep increase in demand related to Generative AI and LLMs. NVDA said this allowed it to extend its visibility of the segment’s business out a few quarters. Although no guidance was provided beyond 2Q24, NVDA noted that it will be procuring a significantly higher level of supply for 2H24, where it indicated that sales will be higher than that of 1H24. Gross margin is expected to be 68.6%, indicating a potential 25% YoY expansion (6.6% on a normalised basis as NVDA incurred a US$1.2bn inventory charge in 2Q23) as it sells more of its new H100 data centre GPUs, where we believe the price difference is as much as 200% compared to its previous A100.

The Negatives

- Gaming, Professional Visualisation contraction continues. Gaming/Professional Visualisation revenue declined 38%/53% YoY as both businesses continue to face macroeconomic headwinds and lower sell-in to normalise channel inventory. However, the contraction has moderated compared to 4Q23 where they declined 46%/65% YoY, and sales were up QoQ by 22%/31% as NVDA ramps its new GPUs based on Ada Lovelace architecture.