NVIDIA Corporation – New growth drivers signalled

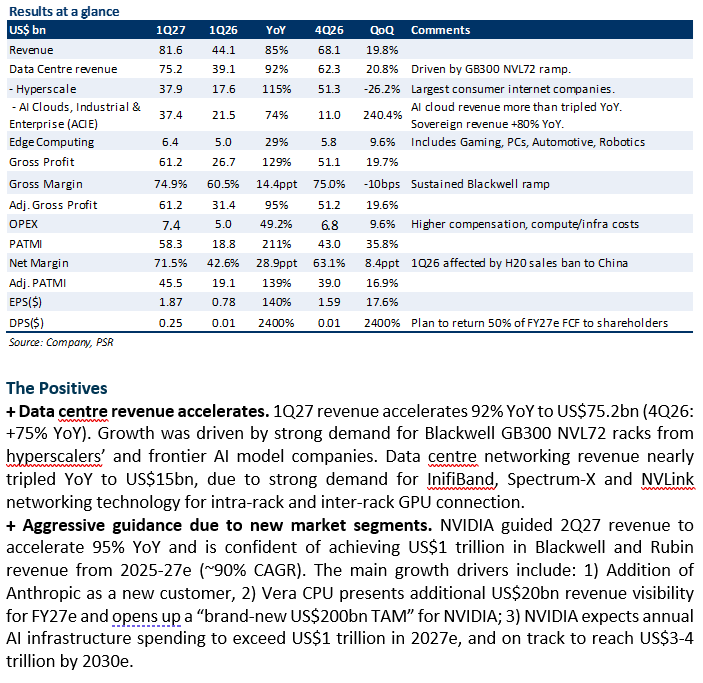

- 1Q27 revenue/PATMI were within our expectations, at 24%/26% of our FY27e forecasts. Data centre revenue accelerated 92% YoY to US$75bn, the fastest growth in 4 quarters. This was driven by strong demand for Blackwell GB300 NVL 72 racks from hyperscalers and frontier AI model companies.

- NVIDIA broke down data centre revenue into two segments: 1) Hyperscale – includes the world’s largest consumer internet companies (AMZN, GOOG, META, MSFT, ORCL), and 2) AI Cloud, Industrial and Enterprise (ACIE) – including AI native clouds (eg. CRWV, NBIS), sovereign nations, and 250,000 Enterprise companies worldwide. We believe there would be acceleration in ACIE growth over the next 1-2 years, driven by Coreweave and Nebius’ aggressive capex expansion to support sovereign and smaller enterprises’ demand for cloud and AI workloads. NVIDIA guided 2Q27 revenue to accelerate 95% YoY.

- We maintain BUY with a higher target price of US$285 (prev. US$220). We raised our FY27e revenue/PATMI by 11%/17%, due to stronger growth expected from Anthropic as a new customer, and an additional US$20bn revenue visibility from Vera CPU. We increased our WACC assumptions to 7.9% (prev. 7.5%) to reflect lower visibility from the consolidation of gaming, automotive and professional visualisation segments.

Nvidia Corporation – De-risked valuations, rapid AI momentum

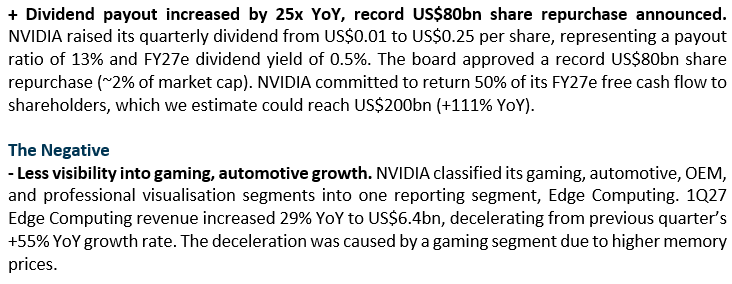

- 4Q26 revenue was within our expectations, while PATMI exceeded our expectations. FY26 revenue/adj. PATMI were at 101%/107% of our FY26e forecasts. 4Q26 data centre revenue spiked 75% YoY, the highest since 4Q25, driven by Blackwell GPU ramp.

- 4Q26 networking revenue surged 263% YoY to US$11bn, highest increase since 1Q25. Growth was driven by strong demand for NVL72 scale-up switches designed into the Blackwell GB200/GB300 systems. We estimate the amount of AI tokens generated in 2025 has increased 14x YoY, driven by the use of reasoning AI models.

- We upgrade to BUY (prev. ACCUMULATE). We raise our DCF-derived TP to US$220 (prev. US$200) as we roll forward our model, increasing our FY27e revenue/PATMI by 12%/4% respectively. WACC is unchanged at 7.5%. We reduced our growth rate assumption to 4.2% (prev. 4.5%) due to reduced growth visibility beyond 2027e. Nvidia is trading at a one-year forward PE of 24x, a 13% discount to peers’ average of 28x.

Nvidia Corporation – Robust earnings visibility on AI demand

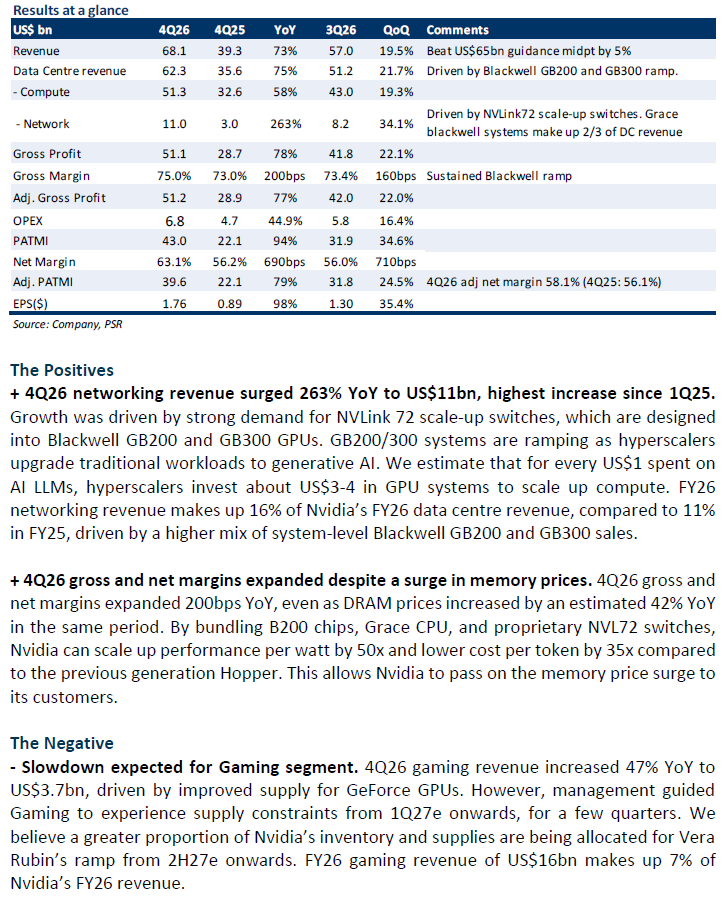

- 3Q26 revenue/PATMI were within our expectations. 9M26 revenue/PATMI were at 72%/77% of our FY26e forecasts. Data centre 3Q26 revenue surged 66% YoY, driven by major cloud service provider (CSP)’s transition to Blackwell GB300 racks, which shipped twice as much compared to GB200 in the quarter.

- Nvidia mentioned it has visibility to US$500bn in Blackwell and Vera Rubin revenue in 2025-26e, which we estimate to be ~US$380bn remaining revenue from 4Q26e to 4Q27e (+67% YoY). Nvidia’s 4Q26e revenue guidance of US$65bn (+65% YoY) excludes data centre sales to China - any GPU sales to China in 4Q26e presents upside to Nvidia’s revenue.

- We maintain ACCUMULATE with a higher TP of US$200 (prev. US$185). We raised our FY26e revenue/PATMI forecasts by 4%/10% due to the ongoing Blackwell GB300 ramp, which increased our FY26e gross margin assumptions by 50bps. We believe risks of circular financing from Nvidia’s deals with OpenAI (US$100bn) and Anthropic (US$10bn) are warranted but immaterial at this juncture. The value of the mentioned deals is estimated to make up less than 10% of Nvidia’s ~US$380bn revenue visibility till end-2026. Organic demand for Nvidia’s GPU infrastructure is still evident from hyperscalers’ increased CAPEX budget, and sovereign nations’ deals with Nvidia such as those from South Korea, Europe, and the UAE. Nvidia is trading at a forward PE of 44.8x, within its historical 1 standard deviation forward PE of 52.2x.

NVIDIA Corporation – Data centre segment still growing

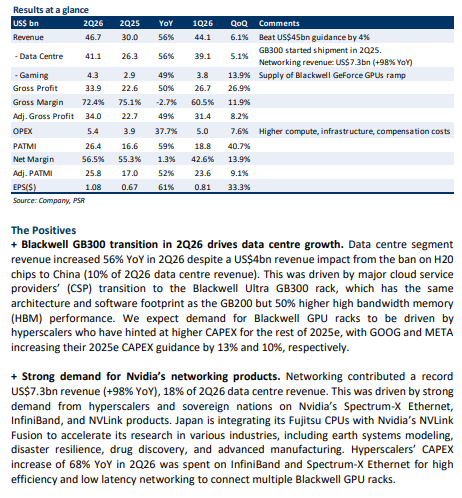

- 2Q26 revenue/PATMI were within our expectations, at 44%/45% of our FY26e forecasts. Revenue increased 56% YoY, driven by the data centre segment where there is still strong demand for Nvidia’s Blackwell GPU from hyperscalers. We expect 2H26e growth to be driven higher CAPEX on AI infrastructure by hyperscalers. GOOG and META announced higher 2025 CAPEX guidance in their June 2025 quarter results, while AMZN and MSFT hinted at higher CAPEX for AI infrastructure for the rest of 2025e.

- Nvidia’s 3Q26e revenue guidance (+54% YoY) excludes potential H20 chip sales to China which impacted 2Q26 revenue by ~9%. The US government granted some licenses for Nvidia’s China-based customers in August 2025. We expect approximately US$3.5bn H20 sales in 3Q26e as Nvidia has ready H20 inventory on hand to ship to China. Including this, we could see 3Q26e revenue increase by ~64% YoY.

- We maintain ACCUMULATE with a higher target price of US$185 (prev. US$145). We maintain our FY26e forecasts. We raise our FY27e revenue/PATMI by 24%/31% due to an expected increase in hyperscalers’ CAPEX in AI infrastructure, robust demand for Nvidia’s GeForce GPUs, and the US government’s reversal of the ban on H20 chips to China. Nvidia is trading at a forward PE of ~41.8x, close to its historical average of 41.7x.

NVIDIA Corporation – Blackwell’s growth offset impact from China

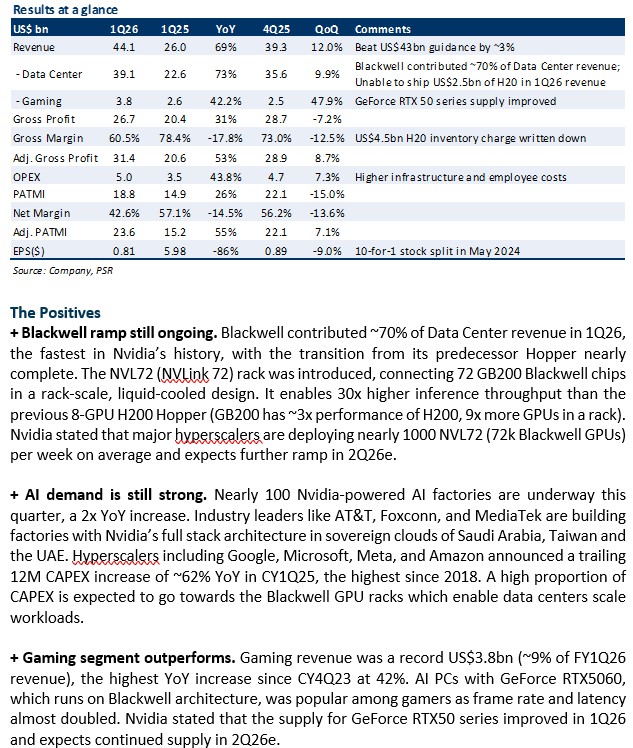

- 1Q26 revenue was within our expectations, while PATMI underperformed. 1Q26 revenue/PATMI was 21%/18% of our FY26e forecast. PATMI was impacted by a one-off US$4.5bn inventory charge from H20 chips which could not be sold to China due to US export restrictions.

- Revenue beat Nvidia’s own guidance by ~3%, driven by Blackwell GPU sales which contributed ~70% of data center revenue in 1Q26. Growth is expected to continue in the data center segment as major hyperscalers still guide higher CAPEX, and Nvidia sees further demand from hyperscalers in 2Q26e.

- We maintain ACCUMULATE with a higher target price of US$145 (prev. US$130). We lower our FY26e PATMI by ~3% to reflect the impact of the US$4.5bn inventory write down. FY26e revenue is unchanged. Given better clarity of US export impact on Nvidia’s China segment, we lower our WACC to 7.5% (prev. 7.9%).

Nvidia Corporation – Short term headwinds, but Blackwell starts to ramp

- FY25 revenue was within expectations, while PATMI beat our expectations. Revenue/PATMI was 100%/106% of our FY25e forecast. Blackwell shipments started in 4Q25, driving revenue growth by +78% YoY and not dragging down gross margins as much as we expected.

- Nvidia’s gaming segment (9% of FY25 revenue) dropped 11% YoY due to supply constraints. However, demand for RTX 50 series desktop and laptop GPUs remains strong, and we expect gaming revenue to recover by 1Q26e.

- We maintain ACCUMULATE with a lower target price of US$130 (prev. US$160). We adjusted our FY26e revenue/PATMI by 5%/-3% to reflect expected Blackwell ramp until 3Q26e, which is expected to drive revenue growth but lower margins. We believe record CAPEX figures from hyperscalers will continue to drive growth in the data center segment. Given short-term uncertainties from tariff/retaliation announcements, we raised our WACC to 7.9% (prev. 6.8%).

Nvidia Corporation – Moving more AI into autos, consumer and robotics

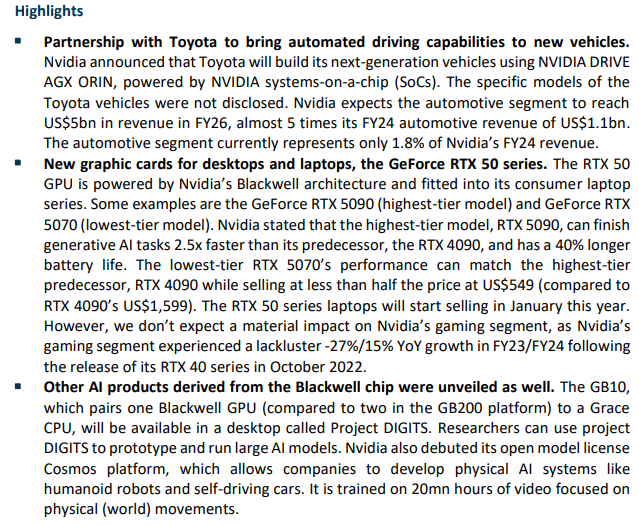

- Nvidia’s CEO Jensen Huang presented at the Consumer Electronics Show, CES2025 to unveil several new AI products at the event. The most significant was the NVIDIA DRIVE Thor, which is an AI chip to be used in autonomous vehicles. Thor is built based on the Nvidia Blackwell architecture and delivers 20x the performance of NVIDIA DRIVE Orin, its predecessor.

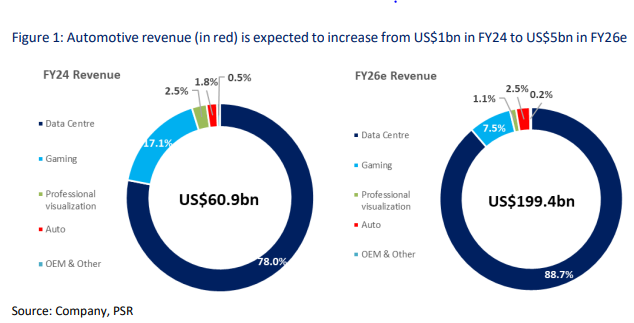

- Toyota's partnership was announced at the event. Revenue growth in the automotive segment (1.8% of FY24 revenue) is expected to grow by almost 5x from FY24 to FY26e.

- Maintain ACCUMULATE with unchanged TP of US$160. Revenue and PATMI growth due to the new AI products are not expected to be material in FY25e and FY26e.

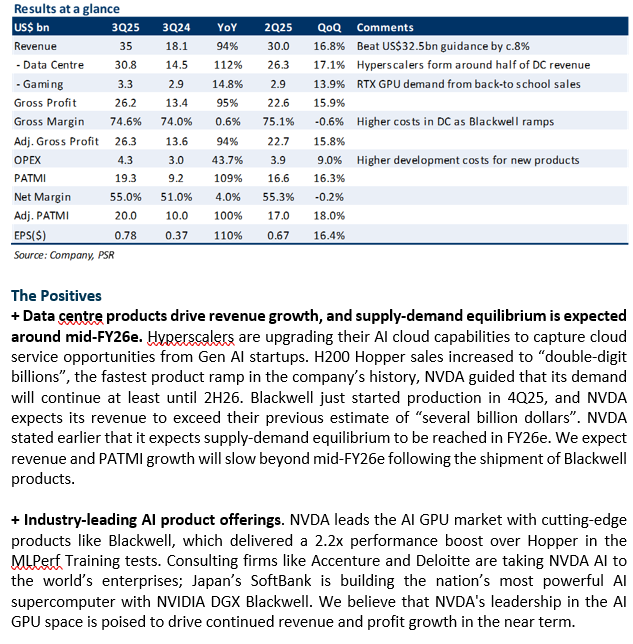

NVIDIA Corporation – Waiting for Blackwell ramp

- 3Q25 results met our expectations. Revenue beat NVDA’s guidance by 8%, and PATMI was up by 109% YoY. 3Q25 revenue/PATMI was at 70%/74% of our FY25e forecasts.

- Hyperscalers make up around half of data centre sales, with the remaining sales coming from enterprises and sovereign nations. Blackwell will be in production for 4Q25, and NVDA expects Blackwell revenue to exceed their previous estimate of “several billion dollars”. NVDA guided the initial ramp of Blackwell to lower gross margins to “moderate to low-70s”, Blackwell margins to be in the mid-70s when fully ramped.

- We downgrade BUY to ACCUMULATE due to recent price movements, with a higher target price of US$160 (prev. US$155). We kept our FY25 revenue/PATMI unchanged and raised our FY26e revenue/PATMI by 5%/7% to reflect the stronger ramp-up of its data accelerator platforms (Hopper + Blackwell) and lower anticipated corporate tax rates. We lowered our margins assumptions for FY26e to reflect management guidance of lower margins due to Blackwell products. Our WACC/g is unchanged (6.8%/4.5%).

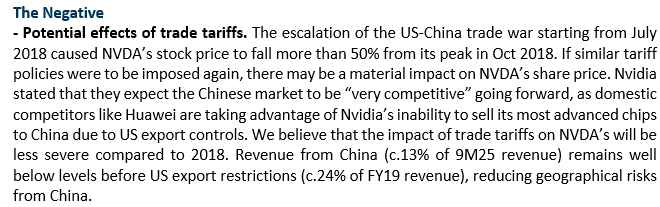

Nvidia Corp. – No change in the growth story

- 2Q25 results exceeded expectations on still strong AI demand and continued supply ramp. Revenue beat NVDA’s own guidance by 7%, and PATMI jumped >2.5x YoY. 1H25 revenue/PATMI was at 46%/49% of our FY25e forecasts.

- 2.5x YoY growth supported by demand from Hypserscalers (45% of revenue), Enterprises, and Sovereign nations. Forward guidance still implies 80% YoY growth in 3Q25e, while supply-demand equilibrium is expected to be reached in mid-FY26e.

- We raise our FY25e/FY26e revenue by 9% to reflect higher demand for Data Centre GPUs (Hopper + Blackwell). Our margin assumptions remain unchanged. We maintain BUY with a raised target price of US$155 (prev. US$140). Our WACC/g is unchanged (6.8%/4.5%). NVDA still dominates (~90% share) AI GPUs, which are benefitting from secular tailwinds from a shift to accelerated computing and increasingly complex Gen AI models.

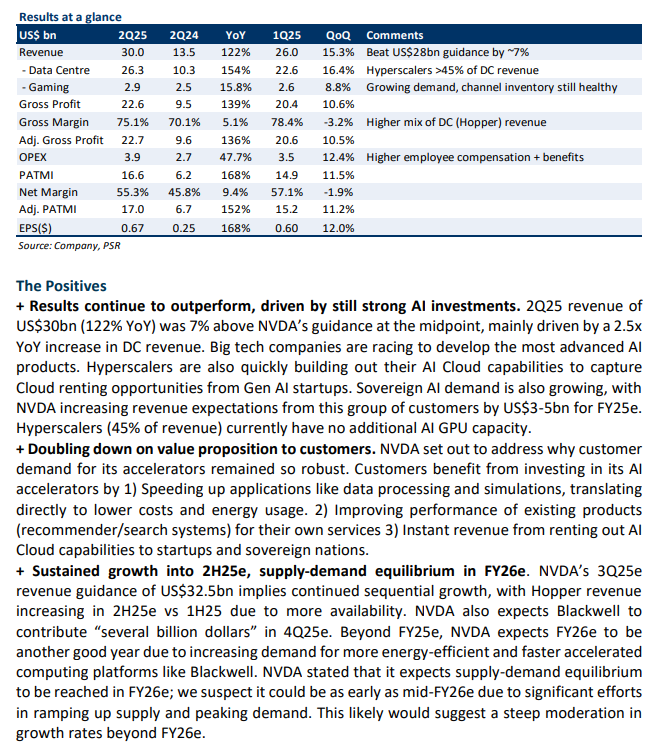

NVIDIA Corporation – Extending market dominance

- 1Q25 results exceeded expectations on more robust AI demand. Revenue beat NVDA’s own guidance by 9%, and PATMI jumped >7x YoY. 1Q25 revenue/PATMI was at 25%/28% of our FY25e forecasts.

- US$4bn sequential ramp-up in AI GPU supply is expected to continue QoQ until the end of FY25e, implying 30% higher DC revenue vs. our previous forecasts. Demand still far outstrips supply, with NVDA also announcing a 1-year cadence for new product launches post Blackwell.

- We raise our FY25e/FY26e revenue by 14%/38% to reflect stronger demand for Data Centre GPUs (Hopper + Blackwell). NVDA dominates (~90% share) AI GPUs that are growing 5x YoY, with superior product performance and an accelerating product pipeline. We maintain BUY with a raised target price of US$1400 (prev. US$970). Our WACC/g is unchanged (6.8%/4.5%).

The Positives

+ Revenue outperformed again, led by 5x YoY growth in Data Centre (Hopper) demand. NVDA’s US$26bn in revenue for 1Q25 outperformed again, beating its own guidance by 9% (US$2bn). Growth more than tripled YoY for a 3rd straight quarter, led mostly by a 5x/3x YoY increase in demand for its DC compute/networking products like Hopper/InfiniBand – from Cloud hyperscalers and consumer internet companies. Inferencing made up ~40% of DC revenue, with sequential DC growth driven by Tesla’s 35K H100 GPUs expansion. NVDA’s gaming segment also grew 18% YoY due to strong end-customer demand for AI PCs equipped with its GeForce RTX GPUs and normalized channel inventory levels.

+ NVDA working hard on increasing supply, 1Q25 results imply ~US$4bn sequential ramp. NVDA’s DC revenue of US$22.6bn implies a sequential increase of ~US$4bn. Given NVDA’s comments on trying to acquire more supply, coupled with current demand-supply dynamics, we assume that most of this came from an increase in chip supply from TSMC. Since 1Q24, DC revenue has also increased sequentially at this US$4bn-US$5bn rate. We expect this rate of increase to continue at least until the end of the year given the 1) current strength in demand and 2) Blackwell shipments beginning in 2Q25e (higher ASPs vs Hopper), which would imply ~US$113bn-US$115bn DC revenue for FY25e – 30% higher than our previous estimates.

+ Aggressive yearly product launch beyond FY25e, low risk of product transition. CEO Jensen Huang reiterated its focus on launching new products at a faster cadence (annually) as it looks to continue outpacing its competitors, announcing a new AI GPU chip after Blackwell that is slated to launch next year officially. Concerns over the risk of customers waiting for newer chips were also alleviated as Hyperscalers average into newer technologies given the early stages of their accelerated compute build-out. In addition, newer platforms like Blackwell are backward compatible, meaning no transitional issues from Hopper.

The Negative

- Nil.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report