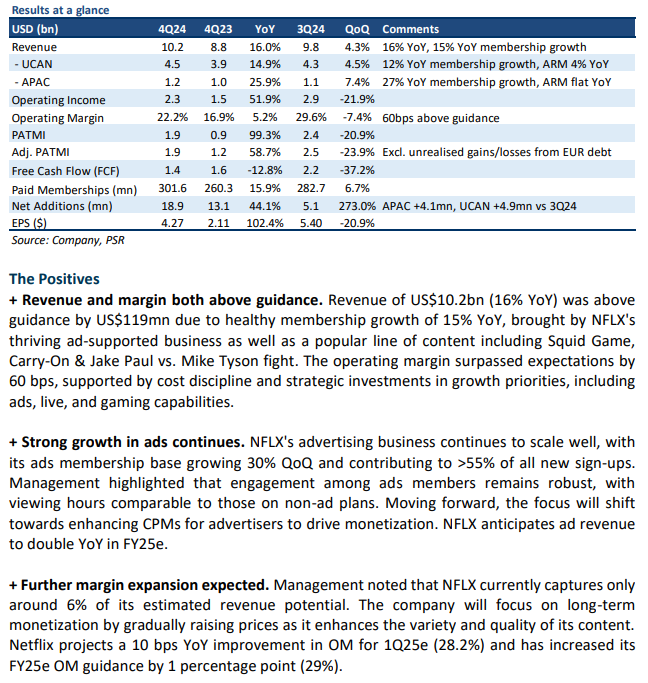

The Positives

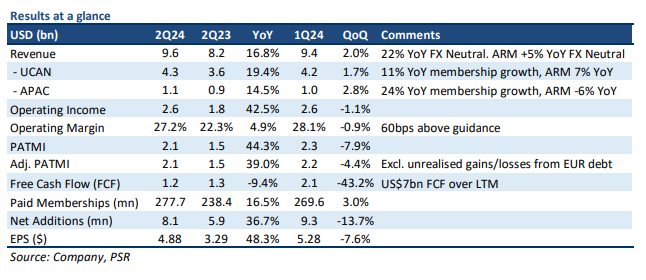

+ Better-than-expected net additions are driving an acceleration in revenue growth. NFLX added 8.1mn net membership additions, driven by beats in all markets (particularly in India). The net additions outperformance was attributed to 1) a strong content slate, 2) some positive impact from paid sharing, and 3) a lower price point appealing to more cost-conscious consumers. Revenue growth in 2Q24 accelerated to 17% YoY (22% FX neutral) vs 15% YoY (18% FX neutral) in 1Q24, modestly above NFLX’s guidance of 16% YoY.

+ Ads business continues to scale meaningfully. NFLX continues to scale its ads business rapidly, increasing its ad tier membership base 34% QoQ to ~52mn (~19% of NFLX’s total membership) in 2Q24. Ad tiers now account for >45% of all new signups in markets where NFLX has rolled out its Ad tiers. NFLX continues to also grow its Ad inventory to support the business. It still does not expect advertising to be a primary driver of revenue for FY24e or FY25e due to 1) near-term challenges in monetisation – NFLX lacks adequate features for advertisers, and 2) an outsized proportion of existing subscription revenue. We view advertising as the next big margin driver for NFLX (behind price increases).

+ Positive forward guidance for FY24e. Given the better-than-expected membership additions so far this year, NFLX again revised upwards its FY24e targets for revenue growth (13%-15% to 14%-15%) and operating margin (from 25% to 26%). Its 26% OM target would be a YoY improvement of 540bps, indicating significant operating leverage due to its larger scale and cost discipline. NFLX expects consistent YoY margin expansion moving forward. We increase our FY24e operating income and PATMI estimates by 6% each as a result.

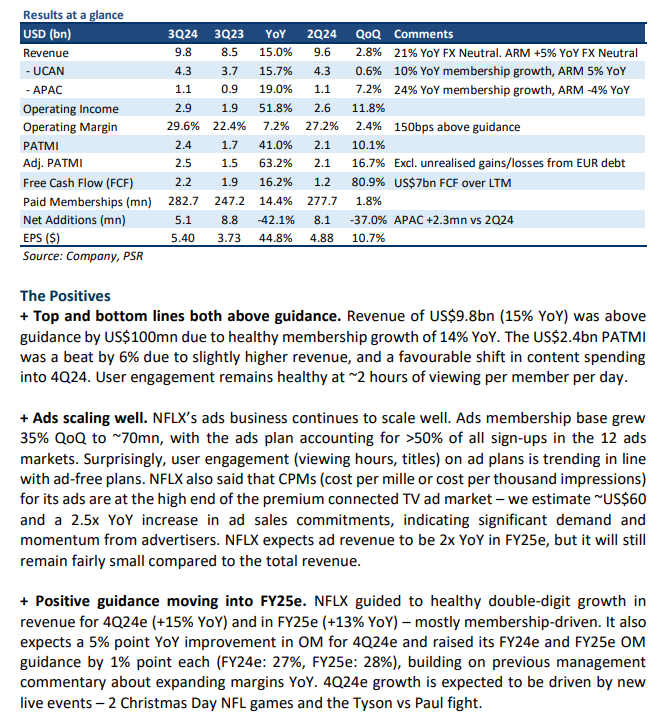

The Negative

- Nil

The Positives

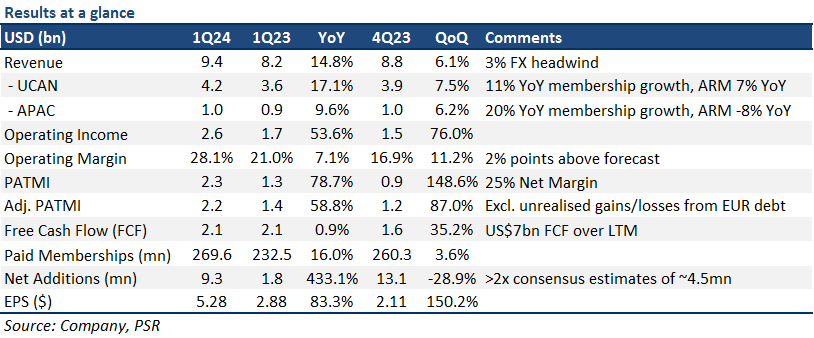

+ Better-than-expected membership additions despite price hikes. NFLX outperformed consensus expectations with 9.3mn net additions in 1Q24, driven by an 11%/19% YoY growth in its US/EU membership base – reaffirming our investment thesis of its undoubted ability to grow both volume and prices (NFLX increased prices in its US/EU markets mid-4Q23). As a result, revenue growth accelerated to 15% YoY (18% YoY FX neutral). We expect net additions for FY24e to remain fairly resilient (~24mn) due to: 1) continued momentum in Paid Sharing (converting password borrowers) and 2) higher take-up of its lower-priced ads plan. NFLX also translated its subscriber outperformance into a 79% YoY increase in PATMI, showcasing an increase in operating leverage – it beat consensus estimates on its bottom line by ~25%.

+ Rapid scaling of its ads business. NFLX continues to scale its ads business rapidly, growing its ad tier membership base 65% QoQ to ~40mn members (~14% of NFLX’s total membership) in 1Q24. Ad inventory has increased, while engagement and CPMs still remain strong. Its ads business is currently under-monetised due to existing supply-demand dynamics, although we expect this to ease as more advertisers come on board – NFLX’s ads business started in 4Q22.

+ Positive FY24e guidance indicating further margin expansion. NFLX revised its FY24e operating margin target to 25% (prev. 24%), which would be a 4% point increase vs FY23. NFLX’s commentary surrounding margins also suggests that the capital-intensive portion of building out its business is behind them, with a clear focus on margin expansion ahead. We expect the company to manage this by pulling on its three main levers: 1) organic membership growth through more engaging content, 2) increasing pricing, and 3) driving higher margin advertising revenue while maintaining current cash content spend levels.

The Negative

- Nil.

The Positives

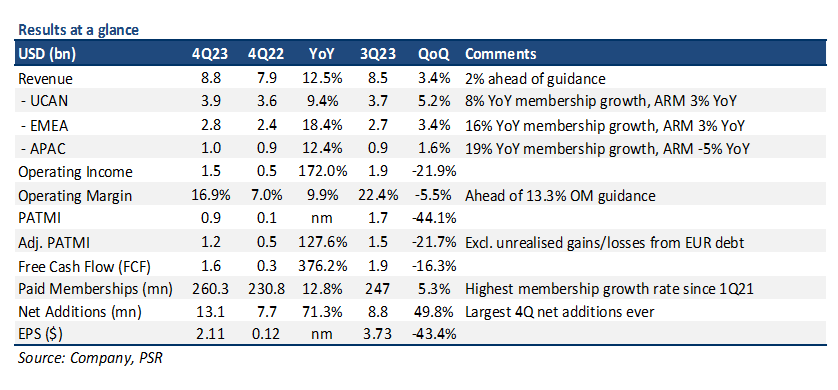

+ Increasing subscriber momentum driving revenue growth. 4Q23 ended on a high, with 260mn paid memberships (13% YoY). Subscriber growth momentum increased for a 4th straight quarter. NFLX also added 13.1mn paid memberships (vs. 8.9mn est.) in the quarter, the most in 4Q. We believe the outperformance was driven by NFLX capturing price-sensitive consumers with its lower-priced ad-tier. Moving into FY24e, we expect revenue growth to be supported by: 1) membership growth of 8% YoY; and 2) 3% YoY ARM growth due to a combination of price increases and scaling of its advertising business.

+ Ads business scaling well; laying the ground work for future margin expansion. NFLX continues to scale its ads business well, with 70+% QoQ growth in the last 3 quarters. It has 23mn users on its ads tier, with 40% of new paid memberships opting for the cheaper subscription. Scaling its ads business is important because advertising revenue remains a long-term margin expansion opportunity for the company. However, we only expect advertising to contribute more meaningfully to revenue as it reaches scale in FY25e.

+ Raising margin expectations for FY24e and beyond. NFLX raised its FY24e operating margin guidance by ~150bps from a range of 22-23% to 24%, indicating a sharp ~340bps increase vs 20.6% in FY23. This expectation reflects: 1) FX tailwinds vs FY23; and 2) better-than-expected 4Q23 subscriber additions combined with price increases flowing into FY24e. Moving beyond FY24e, NFLX also expects to steadily improve margins YoY through a combination of price increases and advertising revenue growth.

ARM (Average Revenue Per Membership): Streaming revenue divided by average number of streaming paid memberships during a given period.

The Negative

- Nil.

The Positives

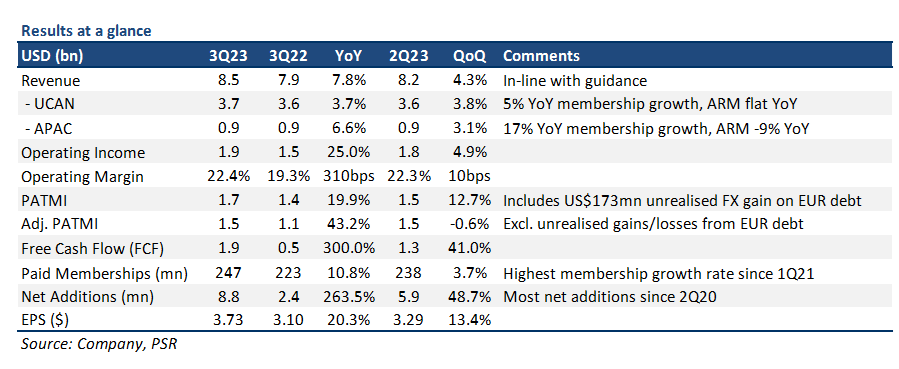

+ Most membership additions in a quarter since 2Q20. NFLX added 8.8mn new members to its platform, the most in a quarter since 2Q20, and the most for a 3Q in 6 years. A bulk of this was attributed to the success of NFLX’s Paid Sharing program as it converts password borrowers into paying members. There is also an expectation for incremental membership additions from Paid Sharing to continue into the next few quarters, alleviating concerns on near-term growth. NFLX ended the quarter with 247mn paid memberships (11% YoY growth).

+ Guiding acceleration in revenue growth for 4Q23e; margins to also expand moving into FY24e. NFLX issued very encouraging guidance for 4Q23e, with revenue growth accelerating to 11% YoY on the back of growing paid memberships and increasing monetisation. Additionally, the company expects FY23e operating margin to be at the top end of their 18%-20% range, with further margin expansion into FY24e by another 200bps. FY23e Free Cash Flow (FCF) was also increased by US$1.5bn to US$6.5bn – supported by healthier cash flow generation and ~US$1bn in lower content spend due to writer/actor strikes.

+ Price hikes in developed markets continue to show pricing power. NFLX announced that it would be raising prices for some of its subscription plans in the US/UK/FR. In the US, its basic plan will see a price increase of US$2 to US$11.99, while its premium plan will be costlier by US$3 at US$22.99. With the price adjustments, churn rates are still expected to be relatively low – in-line with similar adjustments in the past, and should immediately benefit the company’s bottom-line. This is the first price hike for NFLX in >18 months.

The Negative

- Nil.

The Positives

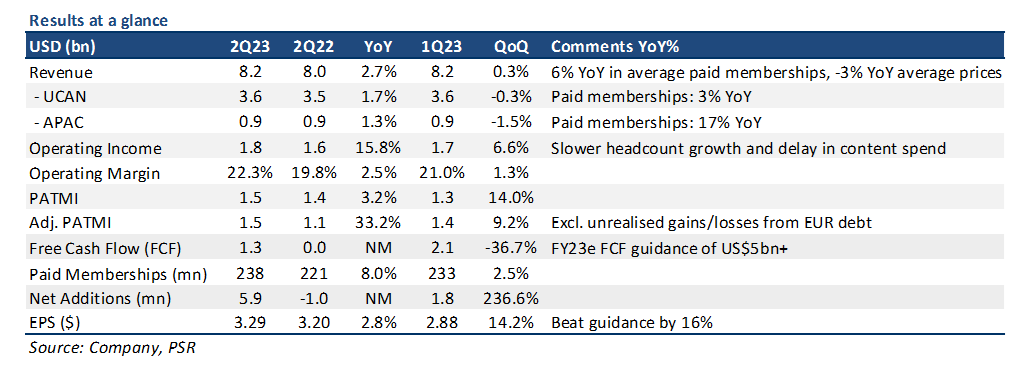

+ Key initiatives showing positive results. NFLX’s new Paid Sharing initiative has almost fully taken off and is now implemented in >100 countries (>80% of total revenue contributions). Initial results have been positive, revenue and membership numbers are better now vs prelaunch. Paid membership growth was broad-based, with all regions gaining at least 1mn new members. Most of NFLX’s revenue growth was attributed to Paid Sharing, with the expectation of a gradual positive business impact in the near term as borrowers continue to convert over the next few quarters. Paid memberships for NFLX’s ad-supported plan is also ramping up, with memberships doubling from 1Q23 to 2Q23. Revenue from this plan is still marginal, but each ad-supported member is margin accretive.

+ Positive guidance for 3Q23e with revenue growth expected to accelerate to 8%. After 3 consecutive quarters of relatively flat growth, NFLX guided to slightly more positive revenue growth of 8% YoY for 3Q23e, citing increasing monetization from its Paid Sharing initiative and advertising growth. Growth is expected to further accelerate into 4Q23e as more account borrowers convert into paid memberships.

The Negative

- Writer/Actor strikes a temporary positive for margins. Hollywood actors and writers continued to go on strike after failing to reach an agreement with major studios and streaming companies over better compensation and job security. Although this cast some negative publicity for streaming companies like NFLX, the strikes actually benefitted the company’s financials for the quarter. Operating margins beat guidance by 17%, coming in at 22.3% for 2Q23, as the strikes delayed planned content spend into future quarters.

The Positives

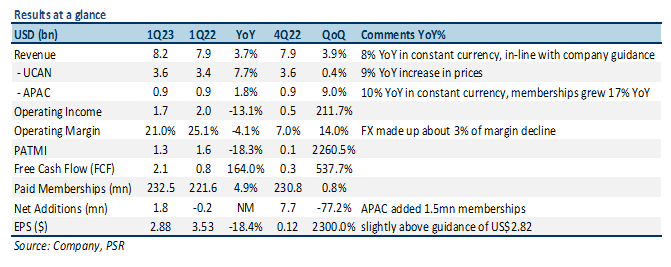

+ Revenue growth remained resilient at 4% YoY, in-line with guidance. Netflix generated US$8.16bn in revenue for 1Q23 (4% YoY, 8% YoY constant currency), in line with its guidance, and our estimates. Growth was supported by a 5% increase in membership base (232.5mn) as the company added 1.8mn new members onto its platform. Asia was the main growth driver, with memberships increasing 17% YoY to 39.5mn, offset by a 13% decline in prices due to a combination of price cuts and FX headwinds. Earnings were also roughly in line, with EPS of US$2.88 vs guidance of US$2.82.

+ Operating metrics improving, within expectations. Netflix continued to operate within expectations. Operating Income of US$1.7bn beat its own guidance by 5% as a result of better expense management. Operating margin of 21% was also slightly above guidance – led by incremental margin expansion from advertising, with profit from its ad-supported plan better than that of Netflix’s standard plan in the US. The company reiterated FY23e operating margin to be in the 18-20% range (FX neutral basis), and also increased FY23e FCF guidance by US$500mn to US$3.5bn due to increasing operating leverage.

The Negative

- 2Q23e revenue guidance disappoints, indicating decelerating topline growth. Netflix issued a muted 2Q23e revenue guidance of US$8.2bn (3.4% YoY), representing a decline in topline growth. There are several reasons for this: 1) delay in launching its paid sharing initiative from late 1Q to 2Q, shifting revenue benefits into 3Q23e; 2) higher mix of membership growth in lower monetization regions, reducing overall prices; 3) expected FX headwinds to continue in APAC. The company also expects 2Q23e net additions similar to 1Q23 levels.

The Positives

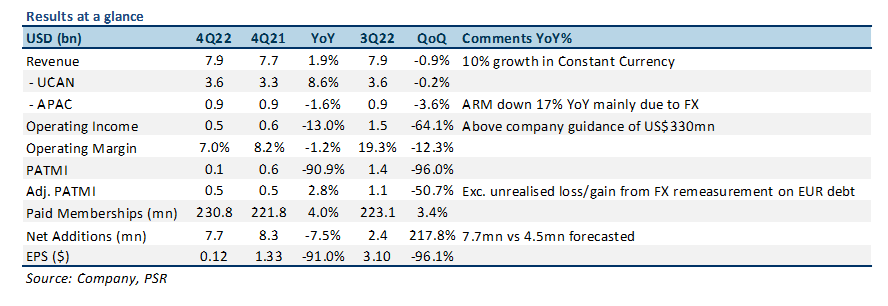

+ Netflix continues to grow its subscriber base. Netflix looks to have worked through most of its subscriber challenges from 1H22 as the company reported 7.7mn membership additions for 4Q22, 3.2mn more than it guided, increasing for a 2nd straight quarter. Most of the growth came from EMEA, with 3.2mn additions, followed by LATAM and APAC which both contributed 1.8mn additions. Membership additions were supported by a strong schedule of content released in 4Q22, and positive incremental benefits from the new ad-supported plan.

+ “Basic with ads” plan showing early signs of promise. Netflix’s new ad-supported plan, dubbed “Basic with ads”, continues to show strong user engagement trends similar to the company’s non-ads plans, with solid growth trends, and lower-than-expected switches from higher premium plans. Additionally, early signs indicate that the unit economics of Basics with ads remains very strong and should generate incremental revenue and profits moving forward, although this impact would remain relatively modest in FY23e as Netflix continues to gradually roll out this plan to more regions.

+ US$1.6bn positive FCF showing improvements in operating efficiency. Netflix generated US$1.6bn in FCF for FY22, compared with -US$159mn in FY21. Content spend also moderated in FY22, down about US$900mn YoY, with the company building operating leverage from more disciplined content spend. Netflix also guided at least US$3bn in FCF for FY23e as it focuses on growing higher-margin ad revenue, and launching its paid sharing program which aims to reduce the leakage of revenue from users who share accounts outside a specific household. Operating income was US$220mn above company guidance as a result of higher-than-expected revenue, and slower-than-expected hiring.