The Positives

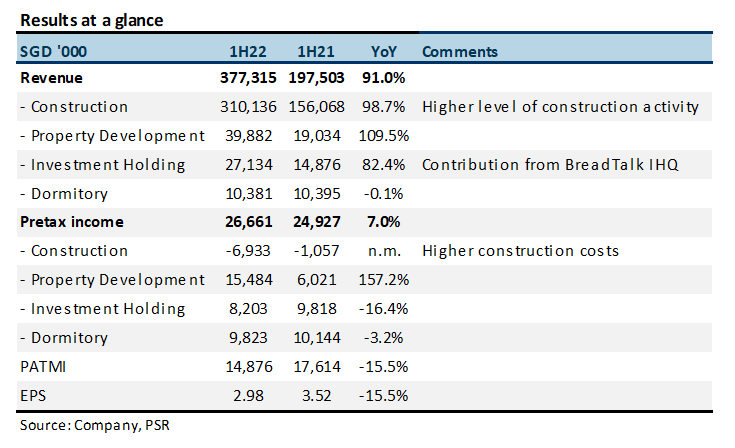

+ Higher revenue from construction and property development. Construction revenue almost doubled from a low base in 1H21. The level of construction activity has recovered and there is also more progress made in various construction projects. Revenue from Investment Holding increased mainly due to contribution from BreadTalk IHQ. The acquisition was completed in April 2021.

+ Operating and free cash flows turned positive. Operating cash flow was S$31mn, from negative S$3.3mn in 1H21. FCF was S$21.9mn, from S$6.5mn in 1H21. This was mainly due to the decrease in development properties from S$180.9mn in May 2021 to S$134.6mn in November 2021, as a result of increase in sale of development units of INSPACE.

The Negatives

- Lower PATMI and EPS due to higher construction costs. Only 77.6% of the Property Development segment’s profit, representing the effective interest held by Lian Beng in SLB was recognised. As such, the increase in contribution was offset by the higher loss incurred by the Construction segment.

Outlook

The construction industry continues to be plagued by rising cost and manpower issues. Lian Beng expects operating conditions to remain challenging, but will closely monitor the delivery of projects.

As of 14 January 2022, Lian Beng’s order book stands at S$1.3bn, which should support construction activities through FY26.

Key Highlights

REVENUE

Revenue comes from four main business segments: construction, property development, investment holding and dormitory.

Construction. Lian Beng’s construction segment is in the business of building a diversified portfolio of residential, industrial and commercial properties and civil engineering projects as the main contractor. It also engages in other construction-related activities such as the provision of scaffolding and engineering services, sale of ready-mix concrete, reinforcement bar fabrication and leasing of construction machinery.

The construction sector in Singapore has experienced a slowdown since April 2020 due to various measures implemented by the Singapore government to contain the outbreak of Covid-19. Construction activities are resuming at a slow pace amid a manpower shortage arising from tighter border restrictions, disruptions in manpower deployment and additional safe management measures implemented at the worksites.

As of 18 October 2021, Lian Beng’s construction order book stands at S$1.4bn, which it will progressively deliver till FY26.

Property development. Revenue from SLB Development (SLB SP, Not rated), which is Lian Beng’s property development arm, is fully recognised in the income statement. It is 77.56% owned by LBG. SLB is involved in the development and sale of properties, including residential, commercial and industrial, and fund management services and investment in funds managed by fund managers through SLB.

Revenue has remained largely stable from FY18 to FY21, and this segment has been a pillar of profitability during the pandemic.

Dormitory. Revenue is recognised through the rental of dormitory units and provision of dormitory accommodation services. Lower revenue in FY21 was mainly due to the rental relief granted to tenants and the lower occupancy in Lian Beng’s dormitory business.

Investment holding. This segment holds a portfolio of commercial, industrial and residential properties in Singapore, which provides LBG with stable recurring rental income and also long-term capital appreciation and dividend yields.

In FY21, LBG reported lower revenue of S$514.5mn, down 7.5%, mainly due to lower revenue from the construction segment (Figure 3). Revenue from construction in FY21 declined 7.2% to S$427.5mn, due to the reasons mentioned.

OTHER INCOME

Other operating income increased mainly due to government grants consisting of the Jobs Support Scheme, property tax rebate, foreign worker levy waiver and rebate.