Keppel Ltd – Asset gathering and earnings growth intact

- Key financial highlights disclosed were 1) New Keppel - slightly lower net profit YoY (due to lower real estate); 2) Overall net profit - lower YoY due to absence of fair value gains and lower asset monetisation gains.

- Asset management fees grew 13% YoY in 1Q26 (FY25 +14.5%) to S$108mn, with S$2bn commitments being finalised, especially in digital infrastructure. There was no notable impact in fundraising activities from the Middle East conflict. Asian dedicated infrastructure funds continue to gather interest from investors.

- Our SOTP-derived TP of S$13.80 and BUY recommendation are maintained. The Middle East conflict has lifted electricity margins, particularly for longer-dated contracts. We expect customers to place a premium and will look to secure longer-term electricity contracts. 2H26 earnings will be anchored by the commencement of 600MW Keppel Sakra, an increase in funds under management, the sale of Bifrost cables, and the completion of DSS projects. The assets monetisation target in FY26 is S$2-3bn (FY25 S$2.8bn), which will support special dividends. Middle East conflict has essentially lifted electricity spreads and improved the attractiveness of AssetCo rigs.

The Positive

+ Recovery in electricity spreads. Electricity (spark) spreads have climbed significantly since

the Middle East conflict. The company mentioned that blended spark spreads were declining

around S$10 YoY, but post the Middle East conflict, they have been up more than S$20.

+ Better outlook for the S$4.3bn Assetco rigs. The long-dated oil curve has trended up. It

has resulted in very strong inquiries for Assetco’s jackups and rigs. Day rates are also 10-15%

higher upon renewal. There are 13 vessels in Assetco, of which six jackups are completed,

and another seven are at various stages of completion.

The Negative

- Small disruption to gas supply so far. The force majeure on LNG supply due to the Middle

East conflict has impacted a very small percentage of Keppel’s gas supply. The replacement

gas will then be sourced from GasCo at spot JKM rather than the typical Brent-indexed price.

The company did add that blended cost with replacement gas has normalised. We believe

GasCo has a Brent-based LNG long-term contract that can increase its offtake.

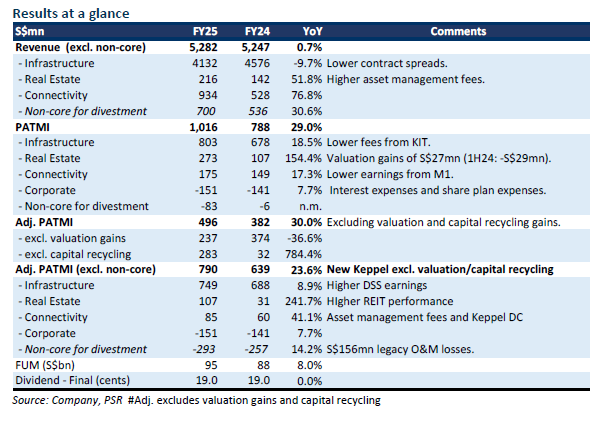

Keppel Ltd – Giving more, Growing more

- FY25 adjusted revenue and PATMI were within our expectations at 97%/96%, respectively, of our forecast. FY25 results exclude M1, which is classified as an asset for sale. Ordinary dividend was maintained at 34 cents. A 12.7-cent special dividend was announced (2-cent cash + 1 Keppel REIT for every 9 Keppel shares).

- FY25 underlying or (New Keppel) earnings 24% YoY to S$790mn. All three divisions enjoyed growth led by real estate asset management and operating performance at Keppel REIT. Infrastructure growth was driven by higher demand for decarbonisation & sustainability solutions (DSS), despite a weaker electricity spread.

- We lower our headline earnings due to the incorporation of non-core operations. Our SOTP-derived TP is raised to S$13.80 (prev. S$12.20) and the BUY recommendation is maintained. We raised our earnings and PE multiples for infrastructure and asset management to align closer with global peers. New Keppel earnings growth will be supported by asset management fees, lower interest rates, cost cuts, the Keppel Sakra Cogen power plant, and maintenance income from subsea cables and DSS. Special dividends will be pegged to 10-15% of assets monetised p.a. Assets earmarked for monetisation total S$13.5bn by 2030 (avg. S$2.7bn p.a.).

The Positive

+ Growth in core operations. Core PATMI of New Keppel rose 23.6% YoY in FY25 to S$790mn.

Infrastructure earnings manage to grow despite a softer spread and lower asset

management fees. DSS EBITDA jumped 32% to S$130mn despite a softer spread and higher

contribution from KIT. Real estate earnings surged due to asset management fees, Keppel

REIT's operating performance, and lower interest expenses. Connectivity improvement was

from acquisition fees and earnings from Keppel DC REIT.

Keppel Ltd – Asset management franchise building momentum

- Limited financials were provided, except that the 9M25 core net profit rose over 25% YoY. The growth rate is in line with 1H25 core net profit that climbed 29% YoY to S$444mn (excluding connectivity). More importantly, 9M25 recurring net profit (asset management and operating income excl. corporate) rose 15% YoY, faster than the 7% in 1H25.

- Asset management fees rose an estimated 8% YoY to S$104mn in 3Q25. The asset management franchise continues to build momentum. Equity raised 9M25 was S$2.7bn, a massive jump from 9M24 S$0.7bn. 3Q25 equity raised was S$0.8bn. Assets monetised jumped by S$1.47bn (M1 S$1.28bn/800 Super S$0.18bn) in 3Q25 (1H25 S$915mn).

- Our FY25e forecast is unchanged. We raised our SOTP-derived TP from S$10.70 to S$12.20 as we roll over our valuations to FY26e earnings. We maintain our BUY recommendation. FY26e will register stronger recurring earnings growth driven by the operations and maintenance income from Bifrost subsea fibre and waste to energy projects, Keppel Sakra Cogen Plant becomes operational 1H26, and rising funds under management. Other drivers of the share price include higher dividends from the planned S$14bn asset monetisation and the outstanding S$407mn share buyback programme. A loss from the M1 disposal will not affect dividends.

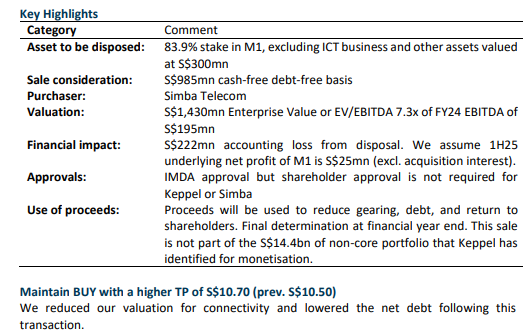

Keppel Ltd – Ring ring, come collect your cash

- Keppel will dispose of its 83.9% effective stake in M1’s consumer business for S$985mn cash to mobile operator Simba Telecom. Keppel will retain M1’s information and communication technology (ICT) business that can support the growth in data centre and subsea operations.

- Keppel will recognise a loss of S$222mn from the disposal. The transaction requires approval from the IMDA, but shareholder approval is not required. Detailed use of the proceeds will be decided at the financial year end.

- We view the transaction positively. Mobile competition has turned extremely competitive, capex heavy and a drag on group earnings. We assume M1's underlying earnings in 1H25 is S$25mn (excluding acquisition interest). Our SOTP-derived TP is raised to S$10.70 (prev. S$10.50) and BUY recommendation maintained. We lowered our valuations for the remaining connectivity assets but included the proceeds from sale. Keppel’s asset light model designed to deliver the entire value chain for data centres from power, connectivity, operations, capital and asset management, is reinforced from this transaction.

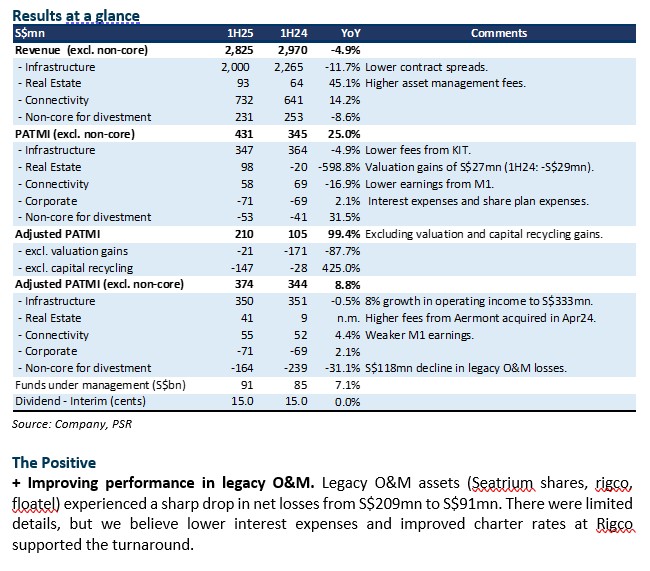

Keppel Ltd – Clarity in “hong bao” draws

- 1H25 revenue and adjusted PATMI were within our expectations at 44%/43% respectively of our FY25e forecast. Adjusted PATMI (excl. non-core / valuation/divestments) grew 9% YoY to S$374mn primarily due to asset management fees contributed by Aermont.

- Keppel has separated a pool of assets worth S$14.4bn in the balance sheet (with S$4.7bn NAV) deemed non-core that will be monetised. Management is reiterating its target of S$10-12bn asset monetisation by end 2026, of which S$7.8bn has been completed. The management has provided greater clarity on the assets that will be monetised and capital returned to shareholders. A S$500mn share buyback programme was announced whilst the interim dividend was maintained at 15 cents.

- We maintain our FY25e adjusted earnings. Our SOTP-derived TP is raised to S$10.50 (prev. S$8.00) and BUY recommendation is maintained. We raised our valuations for infrastructure and asset management, driven by the expected earnings spurt over the next 2-3 years. We also removed the holding co discount due to the virtuous synergies as asset owner and operator across the key divisions of infrastructure, real estate, asset management, and connectivity. FY26e will be a year of growth from Keppel South Central, Keppel Sakra Cogen power plant, and Bifrost cables completions.

Keppel Ltd – Earnings growth is more visible

- Limited financials were provided except 1Q25 net profit was up 25% YoY. Growth was driven by infrastructure and real estate. Not disclosed was the contribution of valuation gains in net profit.

- Asset management fees grew 9% to S$96mn, supported by S$1.6bn of equity raised. Asset monetised has been S$347mn YTD. No change to the S$10-12bn monetisation target (cumulative: S$7.2bn). Part of the monetisation will include 63.36mn Seatrium shares available for sale from end Mar25.

- We maintain our FY25e forecast. Our SOTP-derived TP of S$8.00 and BUY recommendation is unchanged. There is improved visibility of (operating) earnings growth from 2H25 onwards from several projects namely leasing of Keppel South Central, commissioning of Bifrost cables and Keppel Sakra Cogen Plant.

Keppel Ltd – Rewarded as the company transitions

- FY24 adjusted PATMI was above expectations at 110% of our FY24e forecast. Adjusted PATMI declined 4.9% YoY to S$357mn. Losses in the real estate division stabilised but infrastructure was weaker than expected due to lower contributions from KIT and MET. Management is reiterating their target of S$10-12bn asset monetization by end 2026. Currently, S$7bn has been completed. The pool to monetize is at least S$17.5bn.

- We nudge our FY25e earnings by 2% from higher asset management income. Our SOTP-derived TP is raised to S$8.00 (prev. S$7.60). Our BUY recommendation is maintained.

- We expect lacklustre earnings in FY25e from muted real estate sales, competitive mobile markets, and softer renewable earnings. Vessel sales in assetco can materialise as charter income as cash flow builds up. Operating earnings will be strong in FY26e as the new Keppel Sakra Cogen power plant and Bifrost cables are operational. Keppel pays an attractive yield of 5% as the company transitions into an asset manager leveraged on data centre infrastructure and operations rollout through its fund management, renewable energy, cooling and subsea cable operations.

Keppel Ltd – Surfing the huge data centre wave

- Limited financials provided except 9M24 net profit comparable YoY. We believe 3Q24 net profit declined due to lower real estate earnings. Monetisation more than doubled by S$453mn to S$733mn.

- The huge wave in data centre demand has catalysed multiple growth drivers for Keppel: 1) Around S$10bn of funds under management are available for greenfield data centres; 2) Prices for Bifrost transmission cable has more than doubled; 3) Imported green power into Singapore will more than double; 4) Huge demand from commercialisation of two data centres in Genting Lane. There are both divestment gains and long-term recurrent asset management, operations and maintenance fees from these opportunities.

- No change to our FY24e forecast and SOTP-derived TP of S$7.60. Our BUY recommendation is unchanged. Asset monetisation target of S$10-12bn from 2020 to end-2026 has not changed (or another S$4-6bn). Leading the asset sale is Rigco where operation conditions continue to improve. In the medium term, we believe the surge in data centre demand in driving demand for power in Singapore, more funds under management and raised the valuations of its greenfield submarine and data centre assets.

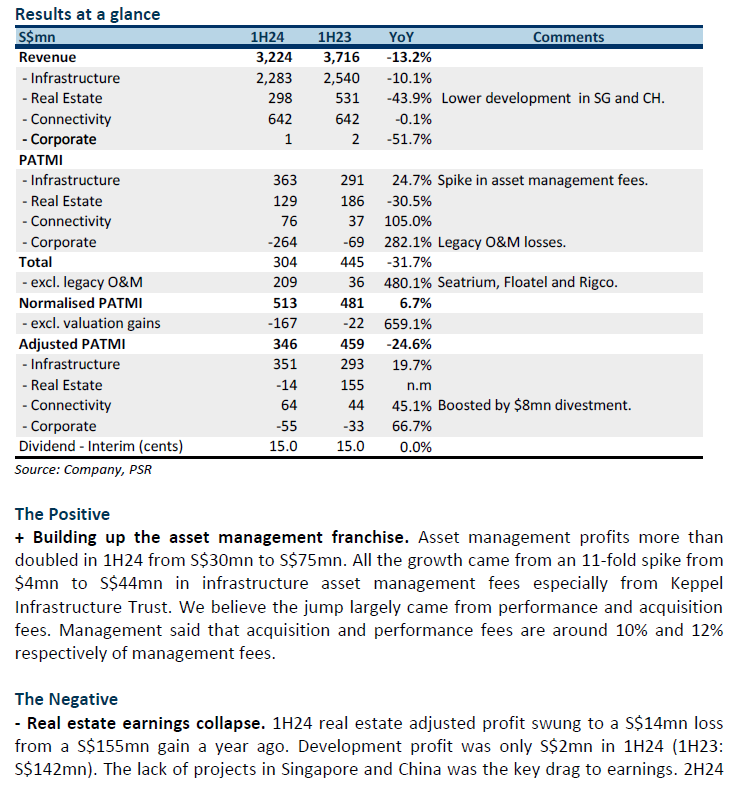

Keppel Ltd – Real estate and legacies depressed earnings

- 1H24 revenue and adjusted PATMI was below expectations at 42%/37% of our FY24e forecast. Adjusted PATMI declined 25% YoY to S$346mn due to losses in the real estate division. Headline earnings was dragged down by legacy assets including fair value losses at Seatrium, Rigco notes receivables and Floatel associate losses.

- Asset management profits more than doubled in 1H24 from S$30mn to S$75mn. All the growth came from an 11-fold jump in fee income from the infrastructure division largely due to Keppel Infrastructure Trust's performance and management fees.

- We cut our FY24e revenue forecast by 12% and earnings by 20% to account for the weakness in real estate and associate earnings. Our SOTP-derived TP is lowered to S$7.60 (prev. S$7.98) as we raise the RNAV discount on the property division. We upgrade from ACCUMULATE to BUY due to recent share price weakness. Keppel is building an operator-run infrastructure and real estate management global franchise. Funds under management have grown 13% YoY to S$60bn, excluding the additional S$25bn from Aermont. Operationally, we expect earnings to be under pressure from the decline in property development sales. The key share price driver will be the monetisation of Rigco and Floatel.

Keppel Ltd – A slow quarter

- Little financial details were revealed in this update. Revenue was S$1.5bn in 1Q24, down from S$1.6bn in 1Q23. Net profit was higher YoY if the impact of the disposed offshore and marine assets were excluded. The real estate segment underperformed.

- The pace of asset monetisation slowed in this quarter. Only S$169.9mn (FY23: S$947.4mn) was achieved, which includes the divestment of the Wuxi landbank for S$161mn.

- Net gearing hovered at 0.9x (Dec 23: 0.9x), suggesting muted operating cash inflow while capex is kept low. With its asset-light strategy, investments are made through funds under management and not through its balance sheet.

- Maintain ACCUMULATE and SOTP-derived TP at S$7.98. A near-term share price catalyst could be a potential redemption of the notes receivables.

Highlights

The Negatives

The pace of asset monetization was slow. S$169.9mn was unlocked (FY23: S$947.4mn), which included the proposed divestment of a residential landbank in Wuxi for S$161.6mn. The total value unlocked from the monetisation programme since 2020 is S$5.5bn. It maintains the monetisation target of 10-12bn by 2026.

- Net gearing hovered at 0.9x at end-Mar 24 (Dec 23: 0.9x), suggesting slow cash inflow. The average cost of debt was 3.81% (FY23: 3.75%). About S$2.4bn (22% of total debt) is due this year and S$400mn 2.9% perpetual securities are due for reset/refinance in Sep 24. Management expects cost of debt to be maintained at 3.81% when these are refinanced.

The Positives

+ It received S$71.3mn from Asset Co, which holds the legacy rig assets. The rigs are fully deployed on bareboat charters, buoyed by stronger offshore and marine activities. We believe these rigs could be monetized in the near term, which could return S$3.1bn cash to Keppel when the notes receivables from Asset Co are redeemed.

+ Fees from asset management grew 52% to S$88mn (FY23: S$283mn). About 90% of this is recurring. About S$436mn in equity was raised YTD (FY23: S$5bn). It has 19 active private funds currently and plans to launch three new funds for data centres, education assets and private credit in 2024.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report