The Positive

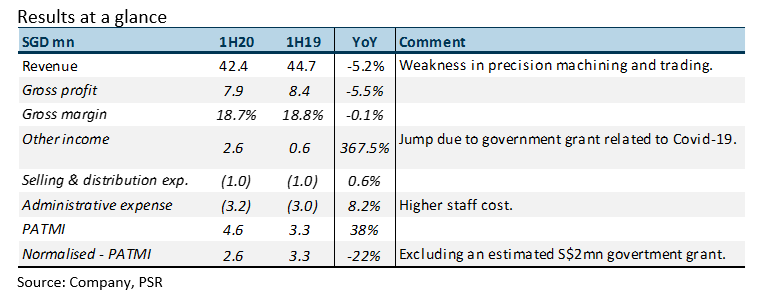

+ Revenue was relatively resilient. Weakness in revenue came from precision manufacturing and trading whilst equipment manufacturing expanded. The sales breakdown of these divisions were not disclosed. Total revenue only declined by 5% despite the disruption in operations from the lockdown in Malaysia and Singapore.

The Negative

- Rise in administrative expenses. We were surprised that administrative expenses rose 8% YoY to S$3.2mn despite the decline in revenue. The increase was due to higher provision of staff cost related to performance.

Outlook

It will be a rough 18 months for JEP as aviation equipment orders have frozen. The Boeing Company reported aircraft deliveries of only 19 in 2Q20, a 80% YoY drop from 90 in 2Q19. We expect JEP to now pivot more to semiconductor orders especially with the support from UMS. Some of the initiatives we believe JEP will undergo during this period of consolidation in aviation are: (i) UMS can tap on JEP to utilise their excess capacity for semiconductor orders; (ii) Further realign cost and production into the Malaysian factories; (iii) Pursue more semiconductor equipment and printing projects, in particular customers looking to shift out of China.

Downgrade to REDUCE from BUY with reduced TP of S$0.158 (prev. S$0.26)

With the lack of visibility, we are benchmarking our target price to book value. We still expect to be profitable but depressed in the medium term. Any valuation based on earnings would understate the earnings potential of the aircraft machining operations.

The Positive

+ Gross margins rebounded. FY19 Gross margins are the highest in a decade. We believe it is a combination of the lower cost of production after shifting more work to Malaysia and better pricing from customers.

+ Removed significant fixed cost. Total operating cost in FY19 fell 12.5% to S$7.9mn. A large part of the decline was from administrative and other operating expenses. We believe the number of headcount in the company was rightsized.

The Negatives

- Revenues were below our expectations. We were modelling 7% YoY growth in revenue for FY19. Precision machining grew 20% due to more aerospace orders. There was disappointment in the non-aerospace business, namely semiconductor, oil and gas and trading business. Trading was affected by less manufacturing activity in China, which is their largest market.

Outlook

The outlook for FY20e will be driven by the stable growth from aerospace customers – Safran and Collins Aerospace. Another source of earnings growth will be margin expansion from more parts being made in Malaysia. The labour cost savings in Malaysia could be more than 50%.

The next phase of growth for JEP will be new customer programmes. There is a demand to outsource more aerospace parts from Asia due to price, diversification and the large backlog of aircraft orders. However, new initiatives will face a delay if the recent Covid-19 outbreak is prolonged. JEP is also looking for higher-end niche products, such as aerospace gears.

Maintain BUY with higher TP of S$0.26 (prev. S$0.20)

The aerospace components industry is trading around 23x PE (Figure 1). JEP should trade at a discount due to the size and lack of profitable track record until recently. Our initial 10x PE valuations were conservative. We are pegging a 14x PE, similar to Taiwanese and European peers.

Company Background

JEP was listed on the SGX as Alantac Technology in 2004. It initially specialised in semiconductor and hard disk drive parts. In 2007, Alantac made a major acquisition of JEP Precision Engineering (JEPS) to venture into precision parts for the aerospace and oil and gas industries. The combined entity was renamed JEP in 2010. In January 2018, SGX-listed UMS Holdings acquired a 29.5% stake in JEP. New management was installed after Mr Andy Luong was appointed as the Executive Chairman in February 2018. Eighteen months later, UMS Holdings launched a mandatory conditional cash offer at S$0.15 per share. Its offer lapsed as the level of acceptances did not cross 50% of the voting shares.

Investment Merits

Outlook

JEP’s growth is expected to stem from, firstly, resilient demand for commercial aircraft. Global passenger air travel is rising the fastest in decades. According to Airbus, aircraft demand is expected to sustain at a growth rate of 4.4% CAGR from 2018 to 2037. Low penetration of air travel in emerging economies and a booming middle-class are some of the triggers of growth. Commercial aircraft deliveries currently have a 10-year backlog of orders; Secondly, we expect further cost optimisation efforts from JEP’s transfer of more projects to lower-cost Malaysia. Thirdly, we are expecting JEP to gain more traction with existing and new customers. JEP in improving its execution and track record which will elevate their supplier status. The current trade spat between the U.S. and China is another likely opportunity to move more aircraft components manufacturing into Southeast Asia.

Initiating coverage with a BUY rating and target price of S$0.20.

We initiate coverage of JEP with a BUY rating and target price of S$0.20. Our target price is based on 10x PE FY19e, a 50% discount to the industry’s 20x in view of JEPs smaller size. We expect its discount to narrow with future scale and consistent profitability.

History

History of JEP dates back to 1994, under the name Atlantac Engineering Works. The focus of the company was precision machining parts for hard disk and semiconductor industry. Atlantac was listed in September 2004 on the SGX. In 2007, Alantac made a major acquisition of JEP Precision Engineering (JEPS) to venture into the manufacturing of precision parts in the aerospace and oil and gas industries. Management of JEPS effectively took control of Alantac and the company renamed in 2010. In January 2018, UMS Holdings acquired a 29.5% stake in JEP. New management was installed after Mr Andy Luong was appointed as the Executive Chairman in February 2018. Almost 18 months later, UMS Holdings launched a mandatory conditional cash offer at S$0.15 per share. The offer lapsed as the acceptances did not cross 50% of the voting shares.

Milestones

|

Date |

Event |

|

Jun-07 |

Acquire 85% stake in JEP Precision Engineering for S$23.8mn.

|

|

Apr-10 |

Rights issue to raise S$11.7mn.

|

|

May-10 |

Alantac Technology Ltd changed name to JEP Holdings Ltd.

|

|

Jan-12 |

Acquired 100% of Dolphin Engineering Pte Ltd for S$8mn cash and 62.5mn shares at $0.04 per share. Provides large format precision engineering and equipment fabrication services.

|

|

Aug-15 |

Acquired 100% of JEP Industrades Pte Ltd, involved in the trading of cutting tools used in manufacturing activities for various industries such as aerospace, mould and die, and oil and gas.

|

|

Nov-16 |

New S$25mn Seletar manufacturing facility completed.

|

|

Dec-16 |

Rights cum warrants issue – one rights share for every 2 existing shares @S$0.02 per share plus one free detachable warrant for every 2 rights subscribed. Each warrant exercisable at S$0.02 during the 3-year period.

|

|

Sep-17 |

Moved into a new facility located in Seletar Aerospace Park.

|

|

Jan-18 |

UMS Group acquired a 29.5% shareholding interest in the Company. Mr Andy Luong, who is the Chairman and CEO of UMS, became the Executive Chairman.

|

|

Dec-18 |

Acquired the remaining 15% stake in JEPS and made it a wholly-owned subsidiary.

|

|

May-19 |

UMS acquired 43.84mn shares (10.9% stake) of JEP at S$0.15 from Ellipsiz or total value of S$6.57mn. This raised UMS shareholding to 38.8%, triggering a mandatory conditional cash offer of S$0.15 of the remaining shares. Outstanding warrants were offered at a price of S$0.074.

|

|

Jun-19 |

Close of conditional cash offer @ S$0.15 per share. Acceptance of only 8.8% and did not cross the 50% mark. The offer is considered lapsed, except for the warrants offer. |

Source: Company, PSR

Revenue

Revenue for JEP has doubled over the last five years. The major driver to earnings has been aerospace, from 60% to 70% of sales (excluding trading). Trading as a contributor to revenues surged post-acquisition of JEP Industrade. The weakest division has been oil and gas with revenue collapsing almost 90%.

In terms of products for aerospace, the main components are engine casing (CFM), landing gear, air and management system. We are forecasting mid-single-digit revenue growth as we expect management focus to be on growing margins.

Some of JEP customers include:

Margins

JEP was hardly profitable in the past 4 years (2014 -2017). Gross margins of 11% or S$8mn to $10mn per annum could not cover the huge annual operating cost of S$10 to S$11mn.

We saw the turnaround in 2H18 when gross margins surged to around 19%. The highest on record. Operating expenses also registered a S$2mn decline. There were S$1.5mn exceptional administrative expenses in FY17 from the relocation cost plus rental expenses on the old unoccupied factory premise.

There are several reasons for the higher margins:

Cash-flow

Operating cash-flow has been positive the past five years totalling around S$13mn. The bulk of the improvement in cash-flows was 2018 positive operating cash-flows of S$10mn.

The bulk of the cash-flow has been spent on capital expenditure in particular in 2016/17. Past five years, capex was a cumulative outflow of S$37mn. The capex has been funded 2/3 by loans and 1/3 from new issuance of shares

Balance Sheet

Assets: Total assets grew over the past five years by around S$40mn. The jump was from a rise in fixed assets (S$24mn) and trade debtors ($11mn). Fixed assets expanded significantly in 2016 following the acquisition of the new plant. A rise in trade debtors is in-line with the improvement of revenue, especially with the acquisition of the trading business

Liabilities: Bulk of the liabilities are in loans (60%) and trade payables (20%). Loans more than doubled in 2016 to S$36mn in order to fund the expansion into the new factory.

Industry

The basic supply chain of aerospace industry can be divided into:

Aircraft manufacturers:

Boeing, Airbus, Bombardier, Embraer, Textron

Engine makers:

Engines are the typical razor and razorblade business model where higher margins are in the engine spares and services. Manufacturers can sell engines even at a loss. Some leakages occur when non-OEM parts are used.

As per Figure 7, the highest volume engine for narrowbody aircraft will be CFM Leap. CFM is a joint venture between GE Aviation and Safran.

Component makers

United States:

Europe:

Taiwan:

Japan 3 Heavies:

Korea:

Hanwha Aerospace: Aircraft and military engine; land-based weapon vehicles, security cameras and surveillance equipment and air/gas compressors.

There has been a spate of consolidation in the aerospace industry such as Safran acquiring Zodiac and United Tech purchasing Rockwell Collins.

Outlook

We are positive on the outlook for JEP. From the macro perspective, global air travel is expanding the fastest in decades. Some of the factors contributing to air travel are the growth of low-cost airlines and rising middle class and low penetration of air travel, especially in emerging markets. As per Figure 8, 2008-18 has been the fastest growth for air travel in decades.

Specific to JEP, earnings growth will come from improvement in vendor tier, shifting of production to Malaysia and securing new customers.

Investment Merits

*Based 12 mth rolling profit, Jun 18 against Jun 19.

Valuation

We initiate coverage with a BUY recommendation and target price of S$0.20. Our target price is based on 10x PE, a 50% discount to the industry’s 20x in view of JEPs smaller operations. We expect its discount to narrow with future scale and consistent profitability.

*Our target price exclude 12.8mn (3.1% of total shares) outstanding warrant dilution, warrants will expire 22 Dec 19.