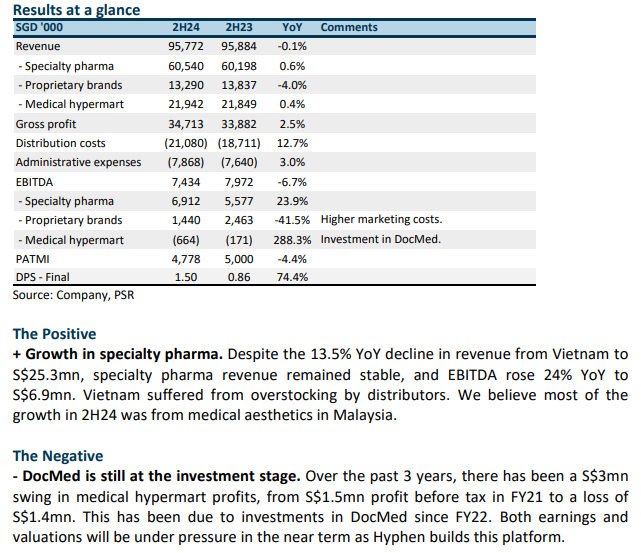

The Positive

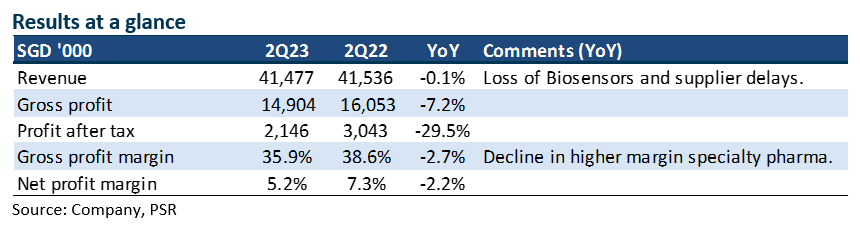

+ Rebound in specialty pharma revenue. Despite the loss of Biosensor's S$5mn revenue contribution in 2023, revenue in 2H23 rose 27% YoY to a record S$61mn. The addition of new specialty products, namely Laboratoires Gilbert S.A.S, drove growth in the export sector. Revenue from other countries (Indonesia, Phillippines) tripled in 2H23 to S$13.7mn.

The Negative

- Weaker gross margins and higher opex. EBITDA margins declined 1.5% points YoY to 8.3% in 2H23. We believe a combination of higher export sales, an increase in headcount costs and additional expenses from DocMed drove down margins.

Outlook

Investments in a larger management team has resulted in more aggressive expansion in principals, products and distribution. We believe Hyphens is on a faster growth trajectory:

Maintain BUY with unchanged TP of S$0.35

Hyphen enjoys a dividend yield of 4% and trades at a PE ratio of 7x FY24e.

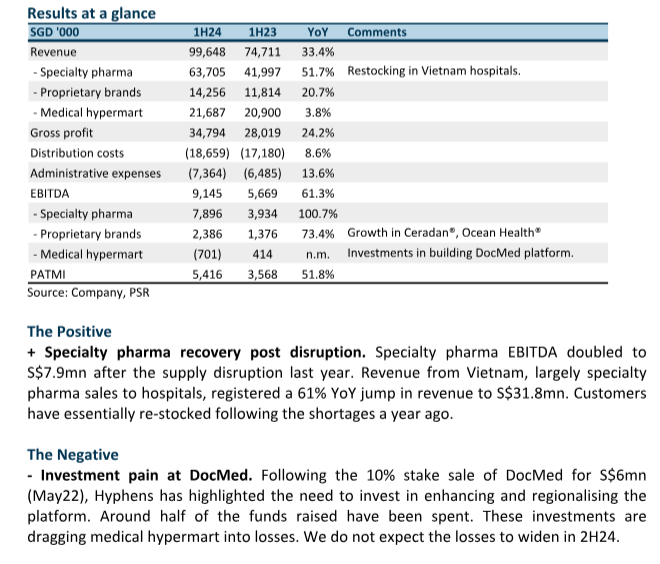

The Positive

+ Healthy balance sheet and special dividend. The company announced a 3.6 cents special interim dividend for the 5th anniversary of its IPO. The payout of S$11mn is well supported by its net cash of S$33mn as of Jun23.

The Negative

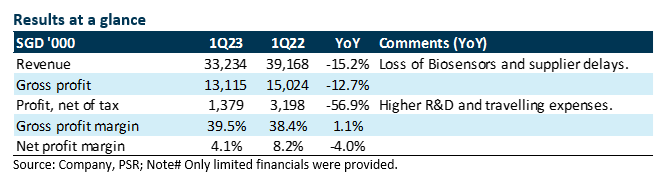

- Weakness in specialty pharma. Specialty revenue was down 13% YoY in 1H23 to S$41mn. The drop was from the discontinuation of distributing Biosensors products (Dec22), the absence of one-off hospital tenders and supply disruptions of several specialty pharma products. Vietnam bore the brunt of the supply disruption with revenue contracting 27% in 1H23.

The Positive

+ Healthy growth in proprietary brands. Proprietary brands revenue increased by 16% in 1Q23 supported by higher demand for Ceradan® dermatological products. Ceradan® and Ocean Health® have a pipeline of new products to be launched this year. The Group launched Ceradan® Advanced Emollient Wash in Singapore and Malaysia during 1Q2023.

The Negatives

- Supply disruption in specialty products. Specialty revenue fell 27% due to the cessation of the distributorship of Biosensors products in Dec 22 and the delay in the shipment of key products in Vietnam. Of the three suppliers facing production disruption, two resumed production in 2Q23.

- Weaker operating margins. Net profit margin suffered from higher R&D and travelling expenses. Margins will be weighed down further from DocMed investments into the platform.

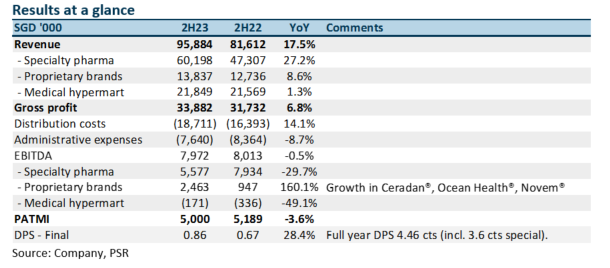

The Positive

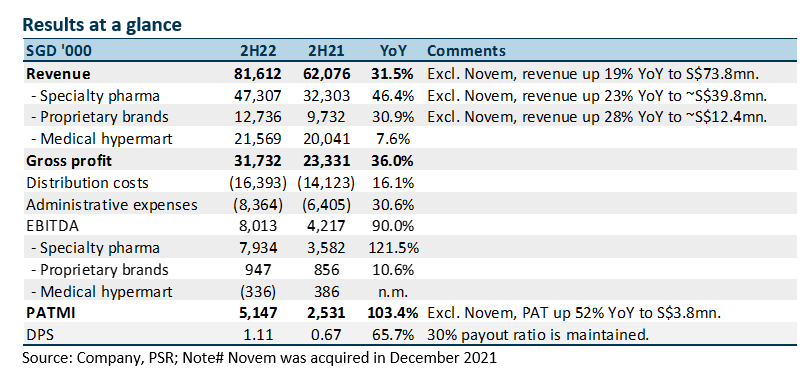

+ Strong growth in specialty pharma. The largest earning driver was specialty pharma. EBITDA more than doubled to S$7.9mn with the inclusion of recently acquired Novem. We believe the re-opening has increased surgeries and visits to hospitals and specialists, thereby driving up revenue.

The Negative

- Softer proprietary margins. EBITDA margins for proprietary brands declined by 1.4% points YoY to 7.4% in 2H22. We believe higher production and product development costs contributed to the weakness in margins.

Outlook

We expect slower growth post the pent-up demand after the re-opening. New products launched will support sales, such as Nabota® (botox), Meradan® (steroid eczema cream) and Winlevi® (acne cream). Hyphens continue to build medium-term franchises: (i) DocMed - a platform for doctors, drug companies and other healthcare providers; (ii) Proprietary brands in skin health products; (iii) Novem - expand specialty products distribution into the public sector.

Event

Metro Holdings Limited will invest S$6mn through new preference shares for a 10% stake in Hyphens wholly owned subsidiary DocMed Technology (DocMed). DocMed owns Hyphens medical B2B hypermart (POM Medical Hypermart) and a licensed e-pharmacy (WellAway).

Comment

With the proceeds, DocMed will build up its manpower (technology, operations, marketing) and enhance its B2B platform to serve doctors. The platform can be enhanced with more pharmaceutical offerings, mobile features and a regional footprint across ASEAN. The expected timeline to enhance and expand the B2B platform is two years.

Key operational milestones of the platform will include a larger number of doctors joining and purchasing through the platform. Pharmaceutical companies are constantly looking to reach out and engage doctors. DocMed platforms will be an important platform to showcase their drugs to doctors. In turn, DocMed can generate new sources of revenue such as advertising and promotion from pharmaceutical companies.

We upgrade our recommendation to BUY with a higher TP of S$0.43 (prev. S$0.345)

Hyphen's multiple-year growth strategy is to expand its proprietary brands of skincare products (e.g. Ceradan and tDf) across the region. The creation and development of the digital healthcare platform DocMed is an additional growth and share price catalyst. Near-term earnings drivers are the acquisition of Novem and growth in specialty pharma sales due to the return of elective surgeries after the pandemic.

The Positive

+ Proprietary brands growth. Hyphens mentioned that proprietary brands have enjoyed robust growth. Skin healthcare products namely Ceradan and TDF likely performed better in Singapore due to border closure and branding efforts. Ocean Health supplements faring well in corporate sales but retail remains competitive due to the presence of multiple brands.

The Negative

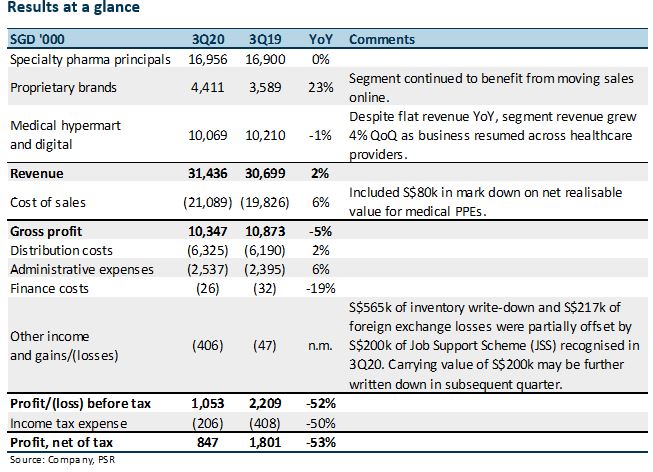

+ Hurt by severe lockdown in Vietnam. Hyphen’s main products in Vietnam are specialty pharma products. Due to the tight movement controls and lockdown, non-essential medical tests and procedures such as X-rays, CT scans and cardiac stents were delayed. For instance, contrast media, a dye used in X-rays and CT scans, will face lower demand due to the reduced amount of medical tests conducted.

Outlook

We view specialty pharma* as a stable cash-flow generator for Hyphens. Lockdowns in Vietnam will stifle sales momentum into 4Q21. The longer-term journey for Hyphens is to grow, invest and expand their portfolio of proprietary products namely Ceradan, TDF and Ocean Health. Hyphens has expanded Ceradan skincare creams from selling exclusively to doctors into retail pharmacies. Doctors prescribe Ceradan Advance whilst consumers can purchase the other range of Ceradan products. There is a sizeable pool of brand recognition from existing users of Ceradan when dispensed by doctors. TDF is another skin health product focused on ageing, pigmentation and age defence. The range of products was extended with a new range of sunscreen products. In August 2020, Hyphens introduced scalp care products under the CG 210 brand. Ocean Health supplements growth will primarily come from new export markets and continuous roll-out of innovative formulations.

*Specialty pharma – Selling more than 30 products to doctors and specialist. Doctors will in turn prescribe the products to their patients for consumption or use in procedures and tests. Hyphens typically have exclusive distribution agreements with their principals. The business is rather sticky because doctors seldom change such products.

Maintain BUY with an unchanged target price of S$0.345.

Our FY21e PATMI is raised by 6% due to higher margins as the mix of proprietary brands increase.

New Acquisition – Novem

Hyphens has proposed to acquire Novem for S$16.28mn (S$13.83mn cash and 8.3458mn new Hyphens shares worth S$2.44mn). The new shares issued is 2.7% of the enlarged share capital. Around 2/3 or 5.56mn of the consideration shares are under a 3-year moratorium. Novem is a distributor of pharmaceutical products for over 20 years. The majority of its customer base are government hospitals and polyclinics. This compares with only 10% for Hyphen. We view the acquisition as a positive for Hyphens. There is a potential 25% to 30% uplift in EPS, expansion of Hyphens product range, widening of customer especially into the public sector and raising of margins due to the higher margin profile of Novem (FY20 PAT margin of 18% vs Hyphens 5-6%).

The Positive

+ Proprietary brands sustained growth

Proprietary-brand revenue grew 23% YoY as the company continued to move sales online. Revenue was down 2% QoQ due to S$1mn of exceptional corporate sales of Ocean Health® supplements in the previous quarter. Stripping that out, QoQ growth would have been 26%, underscoring the strong organic growth of proprietary-brand products.

Specialty pharma and medical hypermart revenue was flat YoY though up 6%/4% QoQ. This reflected their recovery as Singapore gradually reopened.

The Negatives

- Inventory obsolescence hurt earnings

Inventory in excess of S$600k was marked down as a result of disruptions from COVID-19 across products:

FX exposure

About S$217k in FX losses was recognised from SGD weakness against the USD/EUR as well as depreciation of the rupiah and peso.

Outlook

Repositioning business to capture long-term growth

The company continued to expand its proprietary-brand business with the signing of two distribution agreements: one for the distribution of Ocean Health® in Sri Lanka with Healthguard Pharmacy Limited (non-listed) and another for Ceradan® in China with Shanghai Good Luck International Trading Co. Ltd. (non-listed). We expect the company to continue investing in this business on account of better margins.

Normalisation expected in FY22

Inventories, receivables and payables may only normalise in FY22 after the company’s reorganisation of its operations.

Investment Action

Maintain ACCUMULATE with reduced DCF TP of S$0.365 from S$0.435

FY20e and FY21e earnings have been shaved by 20% to reflect a total write-off of COVID-19 test kits in the fourth quarter and a pushout in recovery to FY22e. We have also reduced margin expectations from their high base in FY19 and incorporated higher expenses from possible reinvestments in its own-brand business.

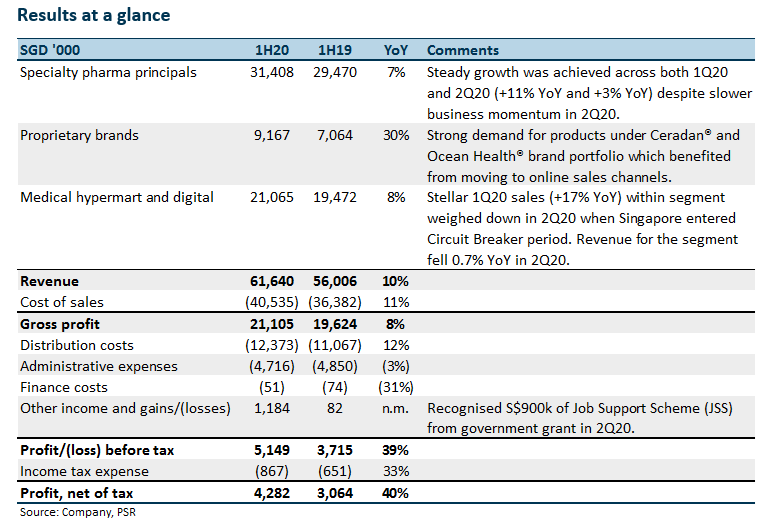

The Positives

+ Proprietary brands revenue benefited (+24% YoY) from online sales channel during Circuit Breaker period in the second quarter.

Strong revenue growth within the proprietary brands segment was sustained throughout 1H20 with 1Q20 growth of 36% YoY and 2Q20 growth of 24% YoY. Demand across Ceradan® and Ocean Health® brand portfolio in 1H20 benefited from the Group’s move towards online sales channels in late FY19.

+ Underlying revenue growth intact despite slower second quarter.

Specialty pharma principals as well as medical hypermart and digital saw modest growth of 7% and 8% YoY in 1H20 respectively despite business slowdown during the second quarter as a result of disruption from COVID-19 across various geographies.

The medical hypermart and digital segment fell 0.7% YoY in the second quarter due to the nationwide Circuit Breaker implemented which saw dampened demand for medical supplies and prohibition of face-to-face interactions.

The Negatives

- Inventory stock-up in anticipation of product license renewals weigh on cash flows.

Due to expected delays in product license renewals typically observed in Vietnam operations, the company has started building up inventory to ensure supply in Vietnam is not disrupted. Inventory levels increased by S$4.7mn in the quarter as a result. This was partially offset by a strong set of operating performance to see the group record a net cash outflow of S$1.7mn for 2Q20.

Nevertheless, inventory levels should normalize in FY21 and the Group continues to maintain a healthy cash balance of S$26mn despite the tougher operating environment in 1H20.

Outlook

Active expansion of product portfolio continues to provide growth catalysts.

During the quarter, the Group acquired hair growth product brand CG 210® to strengthen its proprietary brands portfolio. CG 210® will be sold through medical channels in Singapore and retail channels in Malaysia at the onset with plans to shift sales to retail channels for the Singapore market. New product launches across existing brand portfolios Ceradan® and Ocean Health® also provides the Group with new revenue streams.

Expanded product portfolio will contribute positively to the Group’s top line from FY20 but the impact of contribution will be contingent on the uptake of new products.

Ocean Health® enters Hong Kong market with the inking of partnership deal with SUTL.

Hyphens Pharma enters the US$722mn vitamins and dietary supplements market in Hong Kong with the inking of a Distribution Agreement of Ocean Health® products with lifestyle group SUTL.

SUTL is known for its extensive distribution network of Fast-Moving Consumer Goods (FMCG) brands across 14 markets in Asia and Ocean Health® is the first health supplement product to be distributed under the Company.

The deal will provide the Group with an established retail sales channel for its Ocean Health® products to enter a competitive market.

Investment Actions

We maintain our ACCUMULATE recommendation with a revised TP of S$0.495 (prev S$0.435). FY20e earnings was adjusted upwards by 25% to reflect strong top-line growth and income recognised from the Job Support Scheme in Singapore. We also adjusted terminal growth rate from 1.5% to 2.0% to represent the plentiful organic and inorganic growth opportunities in the long term within the fragmented industry.