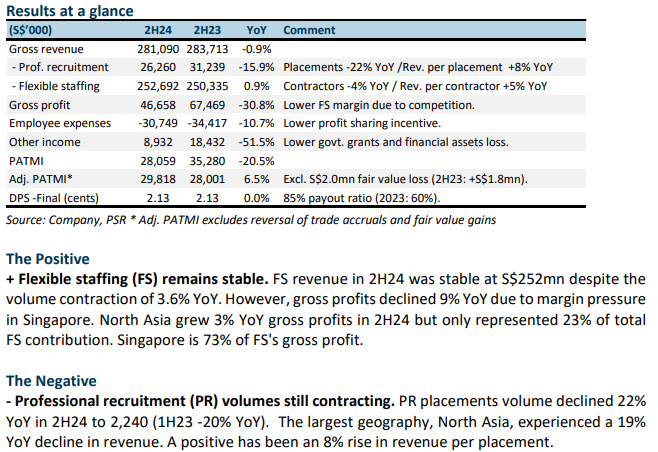

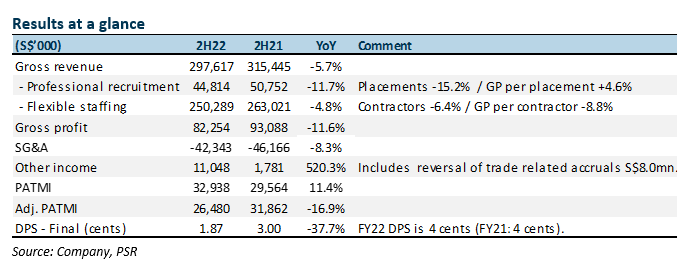

The Positive

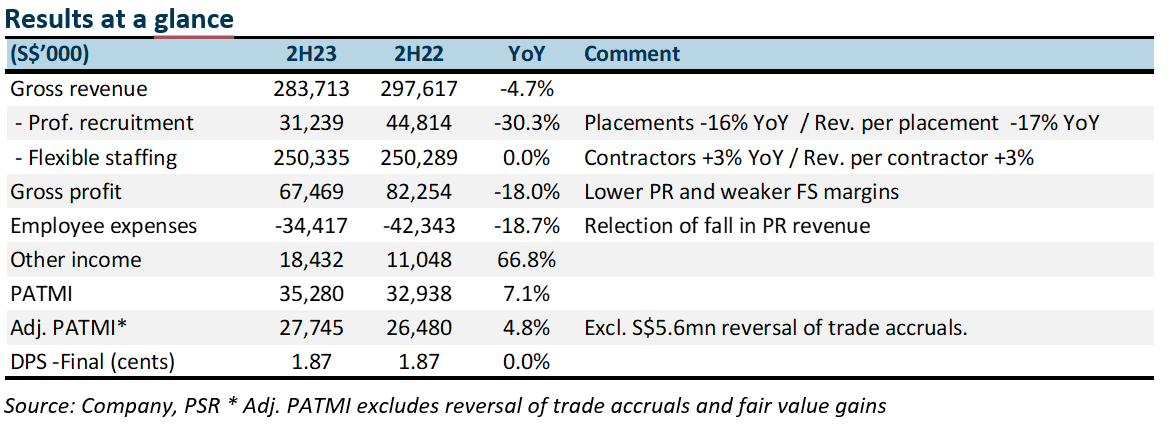

+ Flexible staffing (FS) is the key performer. Around 94% of FS revenue is from Singapore. 2H23 FS revenue in Singapore rose 1.8% YoY. Despite the decline in number of contractors, the rise in wages supported revenue. Government policy to drive up wages of the lower income also pushed income from government subsidies to S$6.6mn in 2H23 (2H22: S$1.2mn).

The Negative

- Professional recruitment (PR) is still the weak spot. The number of PR hirings in 2H23 fell 17% YoY to 2,856, due to hiring freezes and cautious sentiment. Revenue per placement declined 17% YoY as more placements were completed for junior roles.

Outlook

We are forecasting a 5% contraction in volumes for PR. There are limited indications corporates are ramping up their hiring of managerial roles in this region. FS revenue is expected to grow stronger from higher wages and improvement in volumes especially in Taiwan. The FS operations in Taiwan is beginning to hit scale and gain more traction with corporates.

Maintain BUY and lower TP of S$0.85 (prev. S$0.88).

HRnetGroup enjoys net cash of S$303mn with barriers of scale with more than 500 full-time recruitment consultants across 17 cities. There is another S14mn outstanding in their committed share buyback programme.

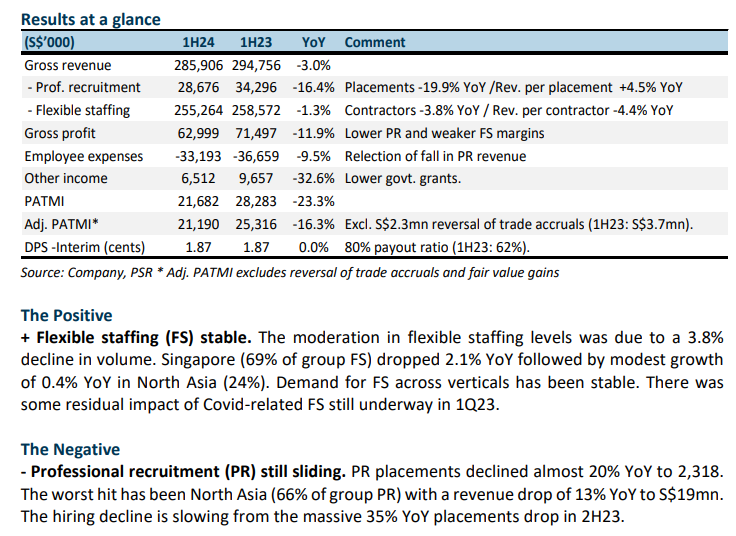

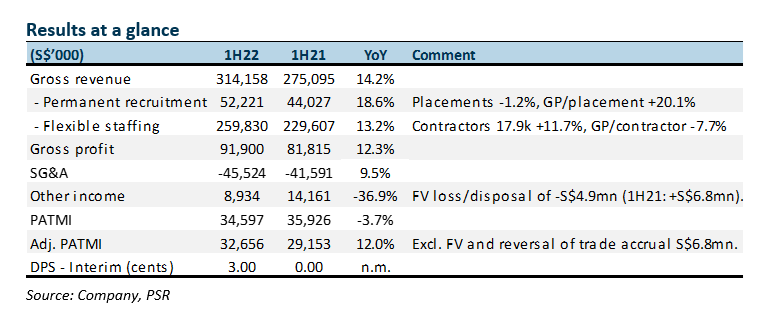

The Positive

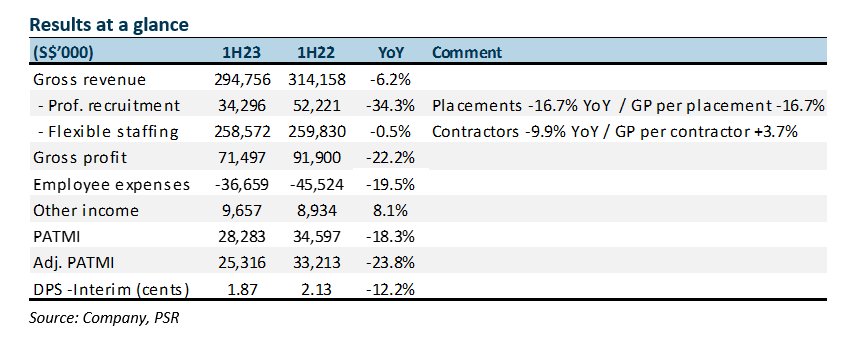

+ Flexible staffing (FS) resilient and flexible staff cost. Despite the absence of pandemic-related hiring, FS revenue was resilient. Sectors supporting FS in 1H23 were banking, luxury retail, consumer and logistics. FS is also expanding outside Singapore, namely Taipei, Hong Kong and Jakarta. In line with the weaker revenues, employee cost was down 19% YoY, from lower bonus payout and headcount reduction of 83.

The Negative

- Steep drop in North Asia and Singapore professional recruitment (PR). The drag on 1H23 earnings was the 37% and 31% YoY decline in North Asia and Singapore PR respectively. There was a severe drop in semiconductor and technology type placements. PR hiring will now be driven by industrial, engineering, lifescience and consumer sector roles.

Outlook

We expect FS to remain the near-term growth driver as corporates pivot towards contingent workers in an uncertain macro backdrop. Another FS growth pillar is expansion overseas, where its advantages are the track record, technology and capital. The strength of the ownership model was reflected by the flexibility to reduce employee expenses. From the $30mn share buyback plan announced in June 2022, there is a balance of S$16.6mn to be completed. In PR both business and candidate confidence is weak, negatively impacting demand and supply.

Maintain BUY and lower TP of S$0.88 (prev. S$0.98).

Our FY23e forecast is cut by 11% to adj. PATMI of S$56mn. The target price is a huge discount to global peers trading at 17x PE. HRnetGroup enjoys net cash of S$303mn with barriers of scale from its nearly 700 recruitment consultants across 16 cities.

The Positive

+ Transitioning well from COVID staffing needs. Revenue from Covid-related staffing was a drag on growth. For instance, in FY21, the average monthly number of contractors jumped 36% to 16.92k. It managed to still grow by 2% in FY22, and remains 45% above pre-pandemic levels. Margins from such staffing needs were higher due to the urgency in demand.

The Negative

- Professional recruitment softer in Singapore and China. 2H22 experienced a major 15% fall in placement volume. The weakest countries were Singapore and China. Demand has moderated in Singapore as confidence in the macro environment has waned. China’s lockdown created much uncertainty in hiring decisions. Strength was from Taiwan and Hong Kong.

The Positives

+ Strong growth outside Singapore. Revenue from Rest of Asia grew 30% to S$107.8mn. These regions now account for 40% of total revenue, a jump from the 26% in FY18. Revenue has grown in region from increasing the number co-owners to build the franchise and expanding into flexible staffing services.

+ Returning S$100mn cash, as it piles up. FCF generated in 1H22 was S$33.1m (1H21: S$3.5mn). Net cash on the balance sheet is S$312.7mn (1H21: S$297.1mn). HRnet announced a maiden interim dividend of 3 cents per share (S$30mn). Together, with planned share buyback of S$30mn, FY21 final dividend of 3 cent (S$30mn) and special dividend of 1 cent (S$10mn), HRnet is returning around S$100mn to shareholders this year.

The Negative

- Weak equity market hurt book value. In 1H22 there was a decline of S$12.6mn in financial assets, namely equity shares in listed recruitment companies. There was S$5.7mn loss recognised in the income statement and another S$6.9mn in the balance sheet.

Outlook

Weaker economic conditions in the region may have a dampening effect on volume. In Singapore, we expect the high job vacancy rates and re-opening of borders to drive revenue growth. For instance, there has been a decline in COVID-19 related vaccination roles but replaced but other non-COVID medical needs as foreign tourist and elective procedures return. The sustainability of growth in North Asia can improve if lockdowns ease. Another strength of HRnet is the ability to veer into faster growing segments of the economy. Despite the slower economic growth and lockdown in North Asia in 1H22, revenues expanded 28% YoY in 1H22. HRnet capitalized on the strong demand from semiconductor headcount by local and multinational companies

Investment Thesis

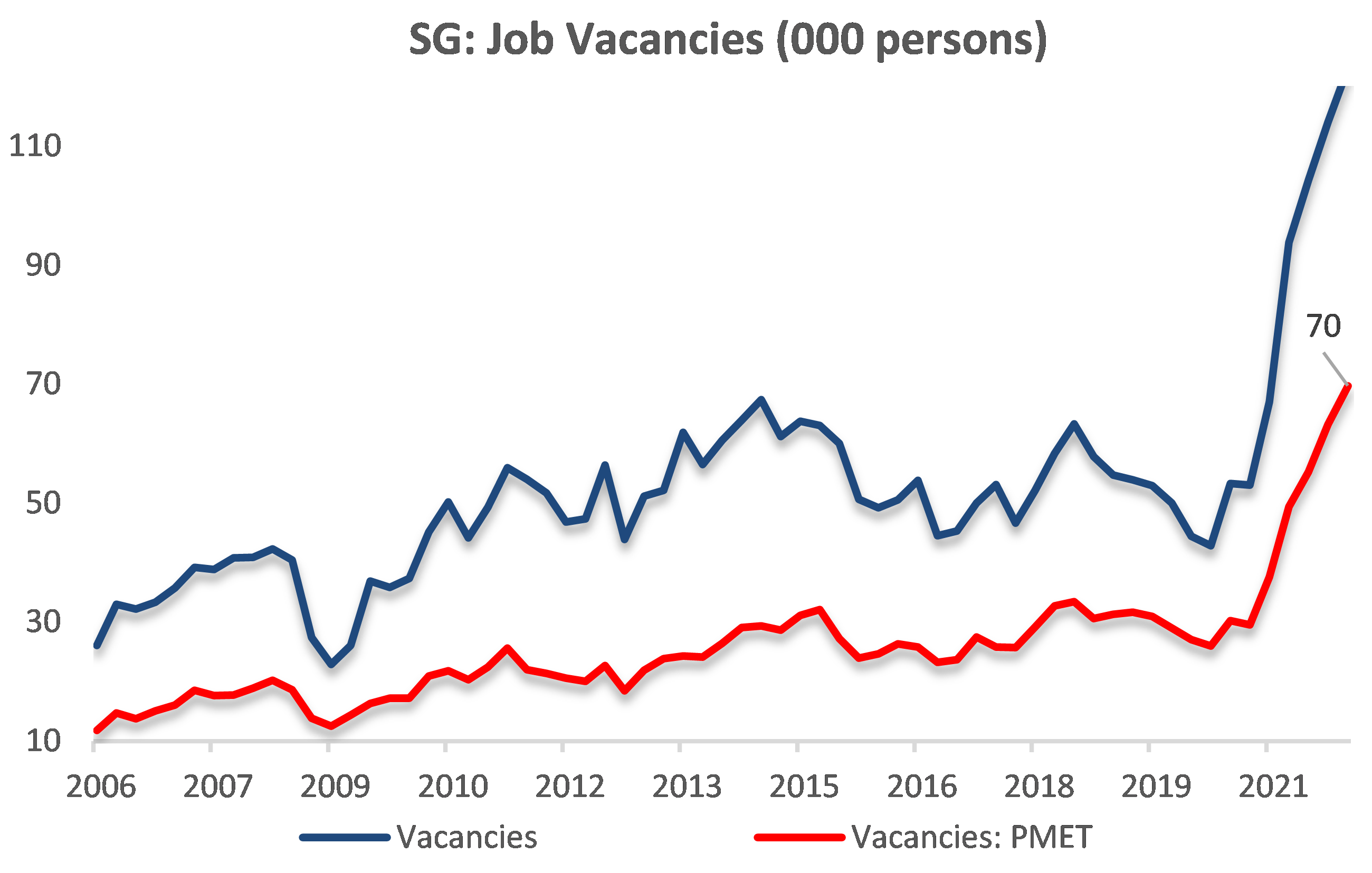

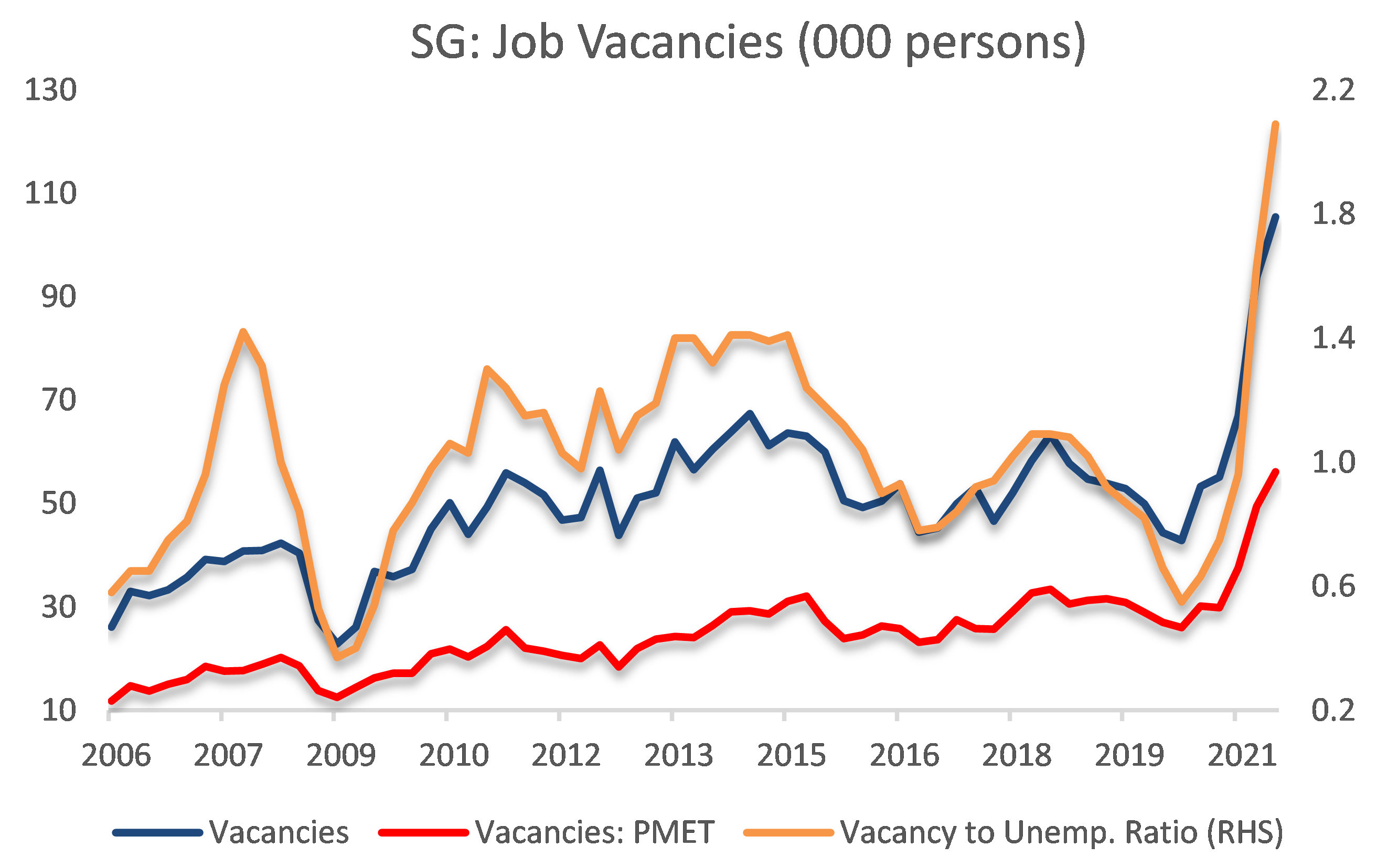

Robust demand for jobs in Singapore. Singapore is experiencing a robust recovery in jobs. In 1Q22, employment rose by 42,000. Employment growth was across all sectors including 17,500 from services. Financial and professional services enjoyed the largest growth in employment in more than a decade. PMET vacancies were the highest on record, at around 70,000. A tight labour market and difficulty in sourcing candidates invariably led to higher reliance on recruitment agencies. Hiring managers have no desire to spend hours interviewing and assessing candidates. It is a waste of a hiring manager’s precious time. Clients want recruiters to identify the best one or two options for them. The ratio of job vacancies to unemployed persons in 1Q22 was 2.4, the highest since 3Q97.

Figure 1: Surge in vacancies in Singapore

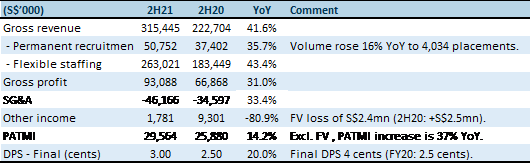

The Positives

+ Growth in both segments. Both permanent and flexible staffing enjoyed growth in 2H21. Permanent staffing recorded 16% volume growth at 4,034 placements and 16% improvement in margins per placement. Flexible staffing volumes grew an estimated 36% YoY. Sectors that performed the best in 2H21 were healthcare (+182% YoY), manufacturing (+65%) and IT and Tech (+49%). Consumer (-1%) and financials (+7%) were the weak spots. Healthcare was driven by COVID-19 vaccinations and testing work in Singapore, while IT and tech hires came from North Asia.

+ Jump in dividends. Full-year dividend was raised 60% to 4 cents (includes 1 cent special). This represents a payout of S$40mn. Cash flow from operations of S$53mn and a net cash hoard of S$327mn will support the dividends. CAPEX for the year was a modest S$1.3mn.

The Negative

- Volatility from investments. There is S$30mn of listed equities and debt on the balance sheet which will be marked to market. Changes in value will be reflected through the income statement. In 2H21 there was a S$2.4mn net fair value loss. In contrast, 2H20 saw a S$2.5mn gain. This swing in fair value will create some volatility in reported net earnings.

Outlook

We expect another healthy year of growth in FY22e. Economies are recovering and vacancies are at record levels, especially in Singapore (Figure 1). Labour challenges have led to companies working closer with recruiters. The pivot towards local hires is another demand driver for recruiters. North Asia demand is driven by semiconductors roles such as IC design and wafer fabs in Taiwan and China. We expect growth in flexible hiring to soften as healthcare hires slow down. The pick up will come from sectors most affected by border closures such as retail and consumer.

Figure 1: Record vacancies in Singapore including PMET

Source: PSR, Company; PMET = professionals, managers, executives and technicians

Maintain BUY with a higher TP of $1.18 from S$1.05. We raised our FY22e revenue and PATMI by 13% and 20% respectively. The employment market is stronger than expected. Our margins are also raised from higher margin per placement due to improvement in salaries and pricing. Our valuation metric is lowered from 14x to 12x PE FY22e ex-cash. We tag to the mid-range of the historical 5-year range as the labour recovery has moved past the peak cycle.

The Positives

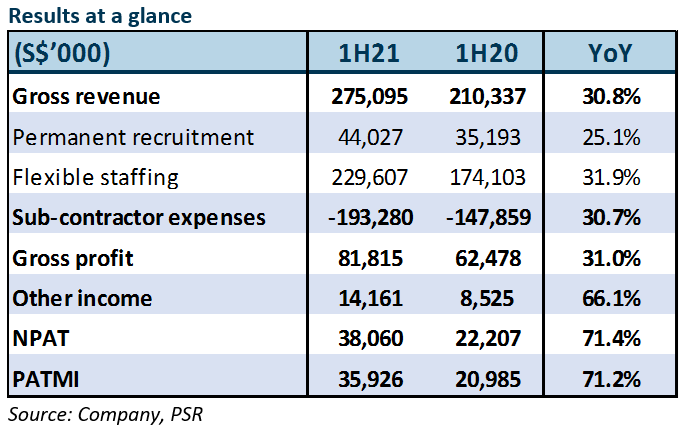

+ Record gross profit and NPAT. 1H21 revenue and gross profit were in line at 54%/51%, but NPAT and PATMI exceeded at 75% of our estimates. We attribute this to S$6.8mn of net fair value gains from its disposal of financial assets and lower-than-expected SG&A expenses. Permanent-staffing revenue grew 25.1%, underpinned by a 17.5% increase in revenue per placement YoY as HRnet filled more senior and niche positions that command higher remuneration packages. Flexible-staffing revenue rose by 31.9% on the back of a 47.1% YoY spike in the number of contractors hired to an all-time-high of 17,123 in June 2021. This was thanks to its Recruit First business expansion in 2019 and 2020 and clients’ preference for manpower flexibility amid business uncertainties.

+ Recovery in key markets. Singapore is HRnet’s largest revenue and gross-profit contributor. 1H21 gross profit in this market grew 31.1% YoY: flexible staffing +33.5% and permanent recruitment +25.0%. Gross profit in North Asia, comprising China, Hong Kong and Taiwan, was up 29.9% YoY: flexible staffing +57.6% and permanent recruitment +23.9%. Volume growth was notably strong for flexible staffing in Rest of Asia, particularly Malaysia and Indonesia, where gross profit surged 40.8%.

+ Strong hiring in healthcare sector. The healthcare and life-science sector which serves pharmaceutical firms, hospitals and vaccination centres contributed 26% to revenue in 1H21, up from 15% in 1H20. The hiring of vaccination nurses constituted about 2% of revenue. Although more than 70% of the Singapore population is now fully vaccinated, demand for medical staff is still expected to come through in various forms, such as more nurses in hospitals, social-distancing ambassadors and temperature scanners at the airport. As Singapore gradually reopens borders for vaccinated travellers and a third booster shot for better immunity is within sights, hiring in the healthcare sector is not expected to pull back in the near term.

The Negative

- Pandemic-related relief tapered off. Pandemic-related assistance dropped in 1H21, as government grants and subsidies declined S$1.7mn from S$7.9mn in 1H20. We expect pandemic-related assistance to diminish by end-FY21, leaving S$4-5mn of government grants from the Wage Credit Scheme. We believe that this scheme will continue to support HRnet’s bottom line, given that the scheme has been introduced and extended since 2013.

Outlook

As various Asian economies commence their recovery with the aid of vaccination programmes, pent-up demand from 2020’s hiring standstill is expected to unleash job openings and employment churns. Strong local employment is predicated on restricted border movements. Still a market leader in Singapore in revenue and profits, we remain optimistic that HRnet will be able to ride the rush for employment. While a continued recovery in the permanent recruitment of mid-level positions is contingent on a re-opening of the economies that HRnet operates in, flexible-staffing volume is expected to grow further as various sectors and organisations choose this option to avoid committing to permanent headcounts.

Maintain BUY with a higher TP of $1.05 from S$1.00.

We lift our FY21e revenue and gross profits by 1.8% and 1.1% on the back of higher-than-expected flexible-staffing contributions. FY21e NPAT and PATMI have been raised by 27.7%, after accounting for higher other income of S$10.4mn and lower SG&A expenses. The increase in other income comprises S$6.8mn of net fair value gains from its disposal of financial assets as well as an additional S$3.6mn of pandemic-related government grants.

After adjusting for the one-offs, our FY21e core PATMI increases by 8.8%. Accordingly, our TP climbs to S$1.05 from S$1.00. This is still set at 14x FY21e ex-cash P/E, HRnet’s historical 5-year high as we anticipate labour market recovery and potential M&As.