The Positives

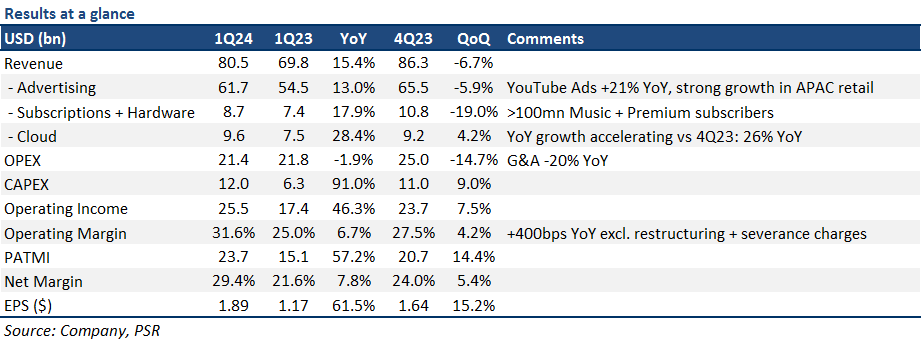

+ Search is still strong, and YouTube is seeing a quick acceleration in growth. Search advertising growth remained resilient at 14% YoY, driven by strength from Chinese retailers, which began in 2Q23. YouTube ad revenue saw a significant reacceleration to 21% YoY (4Q23: 16% YoY) as a result of higher user engagement on the platform, particularly in Shorts. YouTube ad revenue was driven by both strengths in direct response and brand advertising, with Shorts monetisation continuing to improve (monetisation rate >2x YoY).

+ Cloud remains the fastest growing segment, benefitting from AI offerings. Cloud growth accelerated to 28% YoY (4Q23: 26% YoY) as it remained GOOGL’s fastest-growing segment. Growth was supported by an increase in average revenue per seat, reflecting stronger demand for GOOGL’s cloud infrastructure and Generative AI solutions. Cloud’s 2nd quarter of accelerating growth indicates a resumption in customer spending likely due to continued migration to the Cloud and AI-related offerings – which was also seen from GOOGL’s key competitors Amazon’s AWS and Microsoft’s Azure.

+ Margins continue to expand due to ongoing efficiency efforts. GOOGL’s ongoing cost optimisation efforts continue to pay off – leaner organisational structure and improved product prioritization, with its 1Q24 operating margin of 31.6%, a 670bps increase YoY (+400bps YoY excl. restructuring and severance related charges), and is almost back to pandemic highs of 32.3%. GOOGL also reiterated its focus on moderating expense growth and its commitment to expanding margins, even in the face of higher AI-related investments. Headcount was down -5%/-1% YoY/QoQ. We raise our FY24e PATMI by 8% on higher operating leverage and cost efficiencies.

The Negative

- Higher CAPEX is a headwind to valuations. GOOGL’s 1Q24 CAPEX almost doubled to US$12bn as the company increased its investments in AI-related infrastructure like servers and data centres to support future AI development. GOOGL also mentioned that it would sustain this level of spending through the rest of FY24e. As a result, we increase our FY24e/FY25e CAPEX by ~25% YoY each to account for the higher levels of investments.

The Positives

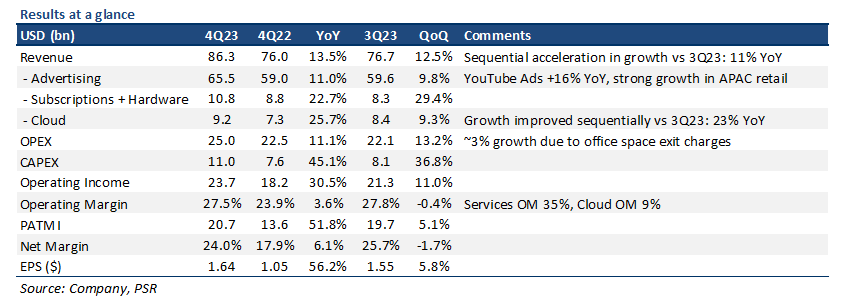

+ Advertising continued to rebound; growth improved sequentially. Ad revenue in 4Q23 improved sequentially vs 3Q23 (9% YoY) to US$65.5bn (11% YoY), driven largely by Search (+13% YoY) and YouTube Ads (16% YoY). Retail strength in APAC was the standout, with small and medium businesses GOOGL’s fastest-growing channel. AI technology in products like Performance Max and Search Generative Experience continues to also drive higher conversions per dollar for advertisers, and incremental query growth from consumers. We expect AI to continue driving most of the gains in advertising by creating: 1) increasing ROI and value for advertisers; and 2) wider accessibility for customers like SMBs.

+ Monetisation on YouTube improving, with subscription momentum gaining traction. Continuing on from previous quarters, Shorts monetisation has been progressing well as viewership expands. Shorts currently has ~2bn MAUs and ~70bn average daily views. YouTube Music and Premium subscriptions are also scaling well, with an annualised run rate of US$15bn. The first season of NFL Sunday Ticket was the key driver for subscription growth. Although still a very small portion of its business, we anticipate ~20-25% YoY subscription growth in FY24e given the growing user base of YouTube on connected TV.

The Negative

- Significantly increasing FY24e CAPEX for servers and data centres to support AI work. GOOGL ended 4Q23 with US$11bn in CAPEX, a 45% YoY increase. It also expects “notably larger” levels of CAPEX in FY24e as it remains focused on developing its technical infrastructure (servers and data centres) to support AI development. We are modeling for a ~20% YoY increase in CAPEX for FY24e vs our previous estimates of ~6% YoY.

The Positives

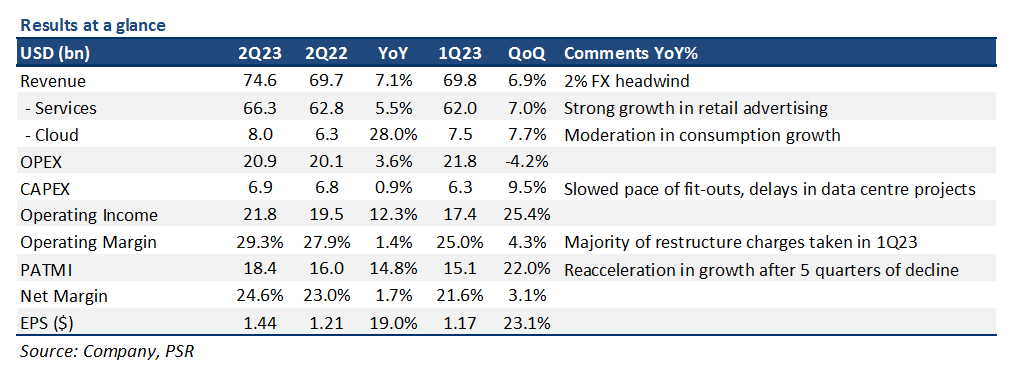

+ Advertising looks to have bottomed. GOOGL showed some signs of recovery in its advertising business, with US$58bn in ad revenue expanding 3% YoY after 2 consecutive quarters of contractions. Within advertising, Search revenue re-accelerated slightly to 5% YoY (1Q23: 2% YoY) on the back of better retail advertising trends, with revenue from YouTube also accelerating to 4% YoY (1Q23: -3% YoY) after 3 quarters of negative growth – indicating that at the very least we are starting to see some stabilisation in advertising spend. Ad growth is expected to continue accelerating into 2H23e given an increase in advertising activity, and easier comps vs 2H22.

+ Cloud showing healthy growth in the face of moderating consumption. Google Cloud showed resilient growth in the face of slowing cloud consumption trends. Cloud revenue increased 28% YoY to US$8bn with growth in both seats and average revenue per seat. Additionally, Cloud saw extensive customer interest in its AI-related products like Bard and Duet AI. Operating income for the segment was US$395mn (5% operating margin), its 2nd consecutive quarter of profitability.

+ Earnings grew for the first time in 5 quarters. With re-accelerating topline growth, a sharp reduction in total expenses, and restructuring charges behind them, GOOGL finally posted earnings growth after 5 consecutive quarters of declines. PATMI of US$18.4bn grew 15% YoY, with net margin of 24.6% expanding by 2%/3% YoY/QoQ as a result. As AI drives improvements in efficiency and productivity, we continue to expect margins to improve moving forward – FY23e PATMI is increased by 4%, with net margin of 24.4% (1H23: 23.1%).

The Negative

- Nil.

The Positives

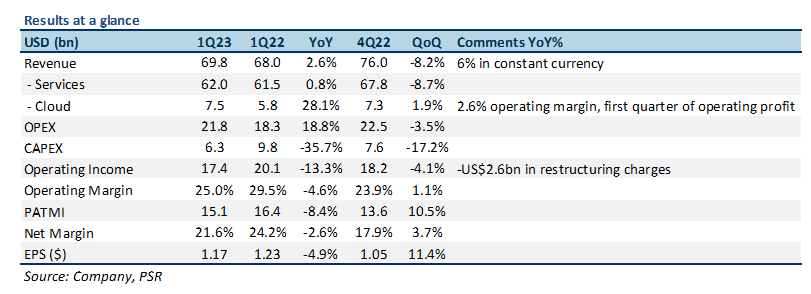

+ Revenue growth re-accelerated slightly due to advertising revenue. GOOGL saw a re-acceleration in revenue growth, posting total revenue of US$69.8bn, 3% YoY (4Q22: 1%). Growth was driven by a 2% YoY increase in advertising revenue from Search (4Q22: -2% YoY) as spending from its travel and retail verticals improved. Additionally, ad revenue from YouTube showed some signs of stabilisation, declining only 3% YoY (4Q22: -8% YoY) as YouTube Shorts monetization increased, offset by some incremental pullback in advertiser spend.

+ Google Cloud momentum slowing, but turned the corner on profitability. Cloud saw some slowdown in its growth momentum, with revenues up 28% YoY (4Q22: 32% YoY). This was led by a continued weaker macro environment, with customers choosing to optimise their current Cloud consumption instead of expanding. Even with topline growth slowing, Cloud posted its first profitable segment, with operating income of US$191mn (1Q22: US$706mn) – operating margin of 2.6%, as management remained focused on driving longer-term profitability in this segment.

+ Earnings in-line with our forecasts. GOOGL announced 1Q23 PATMI of US$15.1bn, in line with our expectations as the company continued to be more prudent with expenses. Earnings were hurt by a US$2.6bn one-off restructuring related charge, offset positively by a US$1bn reduction in depreciation expenses due to an increase in estimated useful life of servers and other equipment, and a delay in timing of its stock-based compensation. 1Q23 PATMI was at 21% of our FY23e forecasts, with Adj. PATMI (excl. restructuring charges) at 24% of our forecasts.

The Negative

- Cautious FY23e outlook. Given the ongoing uncertainty in the macro environment, management remained cautious for the remainder of FY23e, expecting advertising revenue growth to remain muted, with continued decline in Cloud momentum.

The Positives

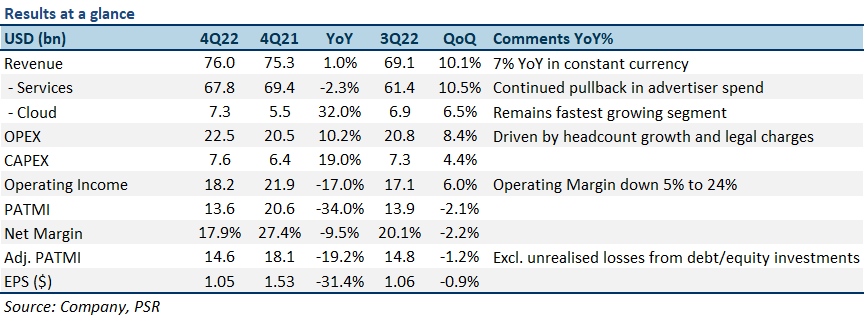

+ Google Cloud momentum still strong, with profitability in focus. Cloud remained GOOGL’s fastest growing segment, increasing 32% YoY to US$7.3bn as customers continue to leverage on Cloud’s AI/Infrastructure/Cybersecurity offerings. Cloud continues to operate in the red, with a 4Q22 operating loss at -US$480mn, although management spoke about its focus on making Cloud profitable sooner rather than later.

+ Slowing expense growth guided moving forward; FY23e CAPEX in line with FY22. Management remains committed to slowing expense growth moving forward; guiding FY23e CAPEX to be at similar levels with FY22 as it consolidates office facilities, offset by continued investments in tech infrastructure. GOOGL also announced the reduction of around 12,000 jobs (~6% of workforce) in 1Q23e as it looks to reduce some of its fixed costs, and will remain prudent and more selective when making investment decisions. FY23e operating margins are still expected to remain relatively similar compared with FY22 at around 27% due to consolidation and severance-related charges, but to expand more meaningfully in FY24e.

The Negative

- Headline earnings missed on weakness in advertising demand, inventory charges, and FX drag. 4Q22 revenue of US$76bn missed estimates marginally by US$440mn, dragged down by a 2% YoY decline in services (advertising) revenue; and a 6% FX headwind. Headline earnings also missed due to higher-than-expected inventory charges of US$1.2bn; and a US$1.5bn unrealised loss on debt/equity investments.

The Positives

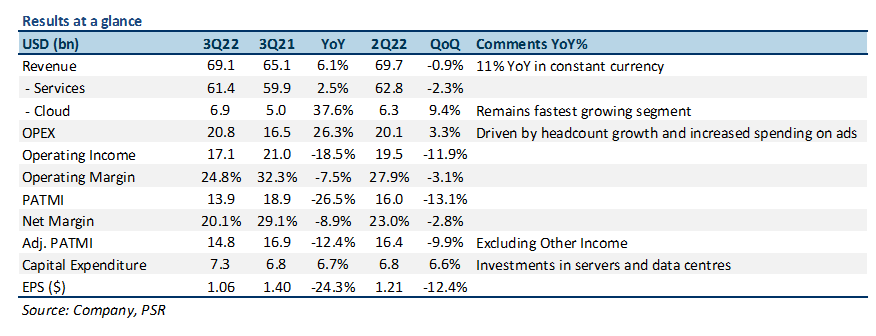

+ Continued momentum in Google Cloud. Cloud remained GOOGL’s fastest growing segment with 38% YoY growth in the quarter, and US$6.9bn in revenue. Growth continues to be driven by increasing cloud adoption and cybersecurity needs, as businesses look to reduce IT costs and digitalize.

The Negatives

- Revenue/earnings both miss on pullback in ad spend and FX drag. GOOGL posted revenue of US$39.1bn for the quarter, equating to a 6% YoY increase, its slowest revenue growth since 2013. Revenue was hurt by a 5% FX headwind, and a pullback in advertising spend due to an uncertain macroeconomic environment – particularly in the financial services vertical, with advertising revenue up only 3% YoY. Net margin was 20% for 3Q22, down almost 9% compared with 3Q21, hurt by increasing OPEX associated with headcount growth (26% YoY), and a US$3.5bn fluctuation in unrealized losses of equity/debt investments.

- FX drag to increase for 4Q22. The strengthening of the US dollar is expected to be an even larger headwind moving into 4Q22, with a greater impact on bottom line growth compared to revenue (% of expenses incurred in US Dollar is higher than % of revenue). Revenue and earnings growth is also expected to be weak compared to a very strong 4Q21, adding to growth headwinds for the upcoming quarter.

Outlook

We expect 4Q22 revenue growth to be around 6% YoY, mainly due to tough comparisons vs a very strong 4Q21 (Figure 1). An uncertain macroeconomic environment and continued strengthening of the US dollar is also expected to continue in the short term, which should present growth headwinds as well. GOOGL also said that 4Q22 headcount additions will be significantly less than 3Q22, as it continues to work on driving efficiencies by shifting resources away from lower priority opportunities, and focusing on bigger growth opportunities like AI technology.

YouTube Shorts continues to show great user momentum, with 1.5bn monthly active users, and 30bn daily views. Shorts viewership as a percentage of total YouTube watch time also continued to increase. GOOGL also lowered the barriers of entry to YouTube Partner Program and began a revenue sharing model for Shorts creators, increasing monetization and support for the creator ecosystem.

GOOGL continues to generate strong Free Cash Flow (FCF) – US$16.1bn for 3Q22, and about US$63bn for the trailing 12 months. The company also bought back slightly more than US$15.4bn worth of shares in the quarter

The Positives

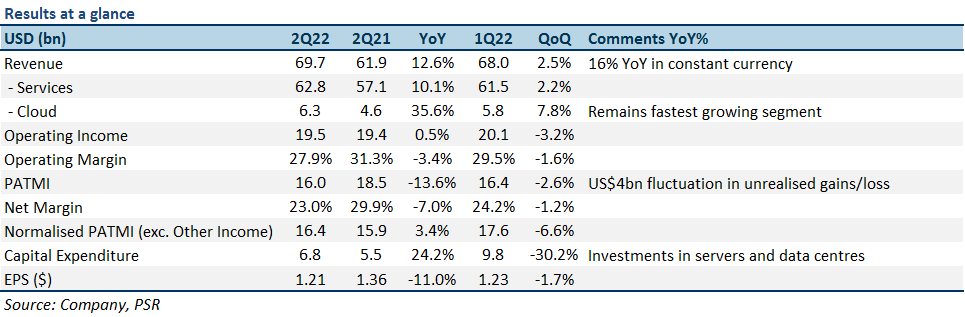

+ 2Q22 revenue in line with forecasts. GOOGL met consensus estimates for its top line, posting US$69.7bn in revenue, representing a 13% YoY increase (16% YoY in constant currency). Revenue growth continued to be supported by growth in GOOGL’s Services (10% YoY) and Cloud (36% YoY) segments. The company also remains on track to hit our FY22e revenue estimates of US$303.4bn, even amidst near-term FX headwinds that are expected to continue.

+ Cloud continues to push ahead. Cloud remained GOOGL’s fastest growing segment, with 36% YoY growth in the quarter, crossing US$6bn in revenue for the first time. Growth was driven by continued corporate demand across Google Cloud Platform and Google Workspace, as companies leverage on Google Cloud’s Artificial Intelligence, Machine Learning, and Cybersecurity capabilities to optimize and safeguard operations. GOOGL also remains focused on working towards profitability in its Cloud segment, reducing losses QoQ.

The Negatives

- Higher-than-expected unrealized losses in debt/equity investments hurting bottom line. GOOGL’s net margin contracted from 30% a year ago, to 23% this quarter, hurt by an almost US$4bn fluctuation in unrealized gain/loss on debt/equity investments. Taking out these fluctuations, net margin for 2Q22 would be 24%, compared to 26% in 2Q21. If we normalize PATMI (exclude Other Income), 1H22 would be 43% of our normalized FY22e PATMI forecasts.

- Weak macroeconomic outlook and strengthening FX headwinds to continue. Pullback in spending by some advertisers across all verticals and industries in 2Q22 continue to reflect uncertainty regarding a weakening macroeconomic environment, with these challenges expected to continue in 3Q22. Also, a strengthening US dollar led to a 3.7% growth headwind for 2Q22, and is expected to worsen in 3Q22 given the strong quarter-to-date performance of the US dollar so far.

Outlook

We expect overall growth to be moderated compared to a particularly high growth period in FY21. Capital expenditure is expected to remain elevated as the company continues to invest in more servers and data centers. A weak macroeconomic environment and a strengthening US dollar is also expected to continue in the short-term, led by uncertainty over the severity of continued interest rate hikes and a possible recession.

Google Cloud continues to grow well, and we expect this to continue moving forward with increasing commitment from management to expand its scale and capabilities – increasing its focus on building up Artificial Intelligence, Machine Learning, and Cybersecurity technologies to support Cloud products. Corporate demand for Google Cloud’s products and services is also expected to remain resilient.

YouTube continues to see strong user engagement, with YouTube Shorts recording more than 30bn daily views, by over 1.5bn users each month. YouTube advertising continues to be an important tool for advertisers, with advertisers excited about YouTube’s reach and ability to drive results. YouTube is currently in its infancy stage as far as monetization, which we believe would be a huge additional driver of revenue growth moving forward.

GOOGL continues to generate strong Free Cash Flows (FCF) – US$12.6bn for 2Q22, and about US$65bn for the trailing 12 months. The company also bought back slightly more than US$15bn worth of shares – the most it has ever done in a single quarter, and also increased its share repurchase authorization for the year to US$70bn.

We reduce our FY22e PATMI forecasts by 10% on the back of higher-than-expected unrealized losses from debt/equity investments, and adjust total expenses forecast upwards slightly to account for increasing investments in IT.

Maintain BUY with a lowered target price of US$139.00 (prev. US$144.00)

We maintain a BUY rating with a lowered target price of US$139.00 (prev. US$144.00), with a WACC of 7.3%, and a terminal growth rate of 3.5%.