The Positives

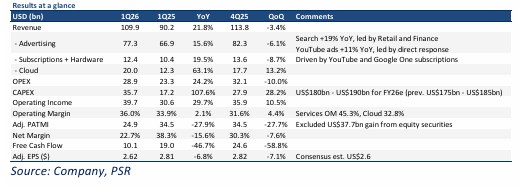

+ Strong AI integration to Search. Search advertising revenue grew 19% YoY to US$60.4bn

(1Q25: +10%), led by the retail and finance verticals. YouTube ad revenue also up 11% YoY to

US$9.9bn (1Q25: +10%), driven by strong momentum in Living Room and Shorts. The queries

are now at an all-time high due to AI experiences in AI Overviews and AI mode, which are

boosting usage and commercial queries. GOOGL has also expanded the deployment of Gemini

models across its ad infrastructure to improve ad targeting and campaign efficiency by better

understanding user intent. We keep FY26e forecast unchanged and expect ad revenue growth

of ~16% YoY, supported by stronger user engagement and improving monetisation

opportunities from deeper Gemini integration across Search, particularly within AI Mode,

alongside longer-term potential for ad placements in the Gemini app.

+ Continued strong momentum in Cloud. GOOGL’s cloud segment accelerated 63% YoY in

1Q26 to US$20bn (1Q25: +28%), and operating income grew 3x to US$6.6bn, led primarily by

robust demand for Enterprise AI solutions. The resilient performance was also driven by 1)

accelerating customer acquisition, with the client base doubled compared to 1Q25; 2) strong

deal momentum, with the number of US$100mn – US$1bn deals doubled in 1Q26; and 3)

expanding client spend, with initial contractual commitment outpaced by 45% (4Q25: 30%).

Revenue from products built on GenAI models grew nearly 800% YoY in 1Q26 (4Q25: +400%).

The cloud backlog doubled sequentially to US$462bn (4Q25: +55%), and GOOGL expects 50%

revenue realisation over the next 24 months, indicating that Cloud revenue will surpass

US$230bn in 1Q28e. We increased our revenue forecast by 21% and now expect the FY26e

cloud segment to grow 75% YoY (prev. 45%) due to robust cloud demand and gradual

conversion of backlog into revenue recognition.

+ Strong operating leverage. In 1Q26, GOOGL’s operating margin increased 220bps to 36.1%,

led by a 300bps expansion in Google Services margin to 45.3% (1Q25: 42.3%), and Cloud’s

margin rose significantly to 32.8% (1Q25: 17.8%). The efficiency gains were supported by strong

revenue growth and process innovation. META mentioned that the cost of AI responses has

reduced by more than 30% since the company upgraded AI Overview and AI Mode to Gemini 3.

We expect operating margins to improve over time as GOOGL leverages its integrated AI stack

and expanding technology infrastructure to drive greater cost efficiency in model deployment,

supporting more stable long-term profitability.

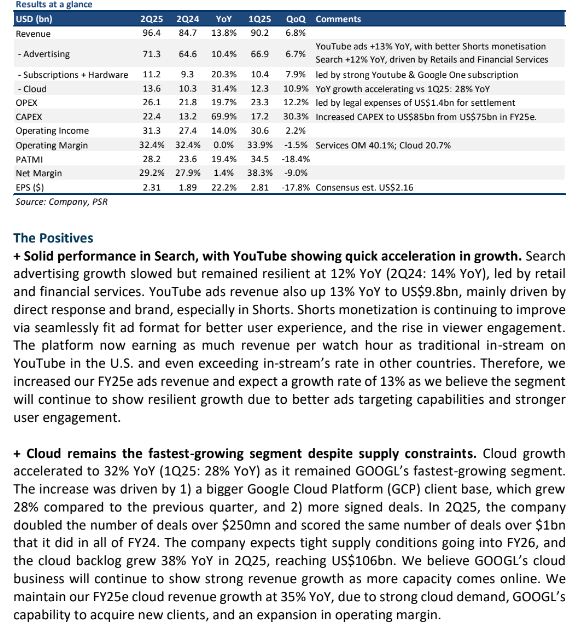

· 2Q25 revenue and PATMI were within our expectations, with revenue up 14% YoY to US$96.4bn and PATMI increased 19% YoY to US$28.2bn. 1H25 revenue/PATMI were at 47%/44% of our FY25e forecasts.

· Strong revenue growth across all core business segments as a result of 1) resilient search ads growth (12% YoY) and increasing YouTube monetisation, 2) Cloud acceleration (32% YoY), and 3) ongoing efforts on cost efficiency.

· We maintain a BUY rating with a reduced DCF target price of US$235 (previously US$250) due to short-term valuation pressure on higher CAPEX, but increase FY25e revenue by 3.5%, reflecting strength in the ad and subscription business with improved cloud service delivery. We expect GOOGL to continue benefitting from AI-driven product enhancement and operational efficiencies, boosting Cloud capacity and strengthening ad targeting capabilities. In addition, we view the current share price as attractive, trading at a discount with a P/E ratio of 20.5x, which is below its 5-year historical average of ~25x.

The Positives

+ Search is still strong, and YouTube is seeing a quick acceleration in growth. Search advertising growth remained resilient at 14% YoY, driven by strength from Chinese retailers, which began in 2Q23. YouTube ad revenue saw a significant reacceleration to 21% YoY (4Q23: 16% YoY) as a result of higher user engagement on the platform, particularly in Shorts. YouTube ad revenue was driven by both strengths in direct response and brand advertising, with Shorts monetisation continuing to improve (monetisation rate >2x YoY).

+ Cloud remains the fastest growing segment, benefitting from AI offerings. Cloud growth accelerated to 28% YoY (4Q23: 26% YoY) as it remained GOOGL’s fastest-growing segment. Growth was supported by an increase in average revenue per seat, reflecting stronger demand for GOOGL’s cloud infrastructure and Generative AI solutions. Cloud’s 2nd quarter of accelerating growth indicates a resumption in customer spending likely due to continued migration to the Cloud and AI-related offerings – which was also seen from GOOGL’s key competitors Amazon’s AWS and Microsoft’s Azure.

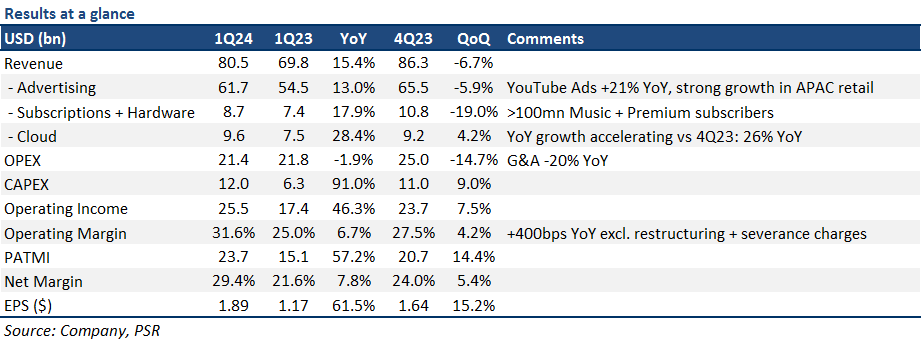

+ Margins continue to expand due to ongoing efficiency efforts. GOOGL’s ongoing cost optimisation efforts continue to pay off – leaner organisational structure and improved product prioritization, with its 1Q24 operating margin of 31.6%, a 670bps increase YoY (+400bps YoY excl. restructuring and severance related charges), and is almost back to pandemic highs of 32.3%. GOOGL also reiterated its focus on moderating expense growth and its commitment to expanding margins, even in the face of higher AI-related investments. Headcount was down -5%/-1% YoY/QoQ. We raise our FY24e PATMI by 8% on higher operating leverage and cost efficiencies.

The Negative

- Higher CAPEX is a headwind to valuations. GOOGL’s 1Q24 CAPEX almost doubled to US$12bn as the company increased its investments in AI-related infrastructure like servers and data centres to support future AI development. GOOGL also mentioned that it would sustain this level of spending through the rest of FY24e. As a result, we increase our FY24e/FY25e CAPEX by ~25% YoY each to account for the higher levels of investments.

The Positives

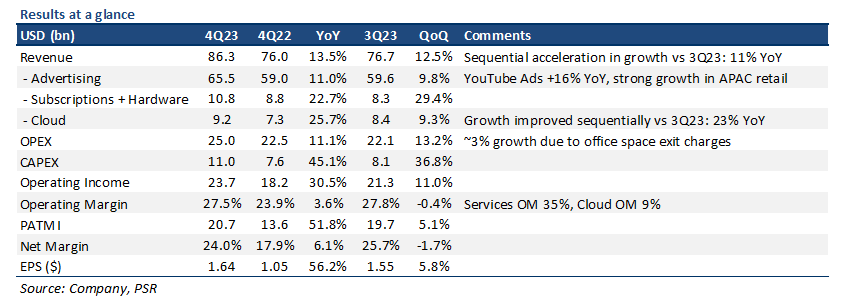

+ Advertising continued to rebound; growth improved sequentially. Ad revenue in 4Q23 improved sequentially vs 3Q23 (9% YoY) to US$65.5bn (11% YoY), driven largely by Search (+13% YoY) and YouTube Ads (16% YoY). Retail strength in APAC was the standout, with small and medium businesses GOOGL’s fastest-growing channel. AI technology in products like Performance Max and Search Generative Experience continues to also drive higher conversions per dollar for advertisers, and incremental query growth from consumers. We expect AI to continue driving most of the gains in advertising by creating: 1) increasing ROI and value for advertisers; and 2) wider accessibility for customers like SMBs.

+ Monetisation on YouTube improving, with subscription momentum gaining traction. Continuing on from previous quarters, Shorts monetisation has been progressing well as viewership expands. Shorts currently has ~2bn MAUs and ~70bn average daily views. YouTube Music and Premium subscriptions are also scaling well, with an annualised run rate of US$15bn. The first season of NFL Sunday Ticket was the key driver for subscription growth. Although still a very small portion of its business, we anticipate ~20-25% YoY subscription growth in FY24e given the growing user base of YouTube on connected TV.

The Negative

- Significantly increasing FY24e CAPEX for servers and data centres to support AI work. GOOGL ended 4Q23 with US$11bn in CAPEX, a 45% YoY increase. It also expects “notably larger” levels of CAPEX in FY24e as it remains focused on developing its technical infrastructure (servers and data centres) to support AI development. We are modeling for a ~20% YoY increase in CAPEX for FY24e vs our previous estimates of ~6% YoY.

The Positives

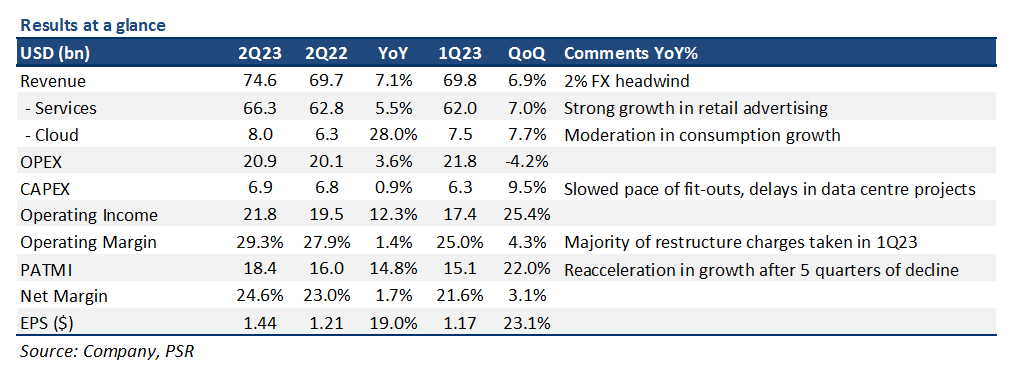

+ Advertising looks to have bottomed. GOOGL showed some signs of recovery in its advertising business, with US$58bn in ad revenue expanding 3% YoY after 2 consecutive quarters of contractions. Within advertising, Search revenue re-accelerated slightly to 5% YoY (1Q23: 2% YoY) on the back of better retail advertising trends, with revenue from YouTube also accelerating to 4% YoY (1Q23: -3% YoY) after 3 quarters of negative growth – indicating that at the very least we are starting to see some stabilisation in advertising spend. Ad growth is expected to continue accelerating into 2H23e given an increase in advertising activity, and easier comps vs 2H22.

+ Cloud showing healthy growth in the face of moderating consumption. Google Cloud showed resilient growth in the face of slowing cloud consumption trends. Cloud revenue increased 28% YoY to US$8bn with growth in both seats and average revenue per seat. Additionally, Cloud saw extensive customer interest in its AI-related products like Bard and Duet AI. Operating income for the segment was US$395mn (5% operating margin), its 2nd consecutive quarter of profitability.

+ Earnings grew for the first time in 5 quarters. With re-accelerating topline growth, a sharp reduction in total expenses, and restructuring charges behind them, GOOGL finally posted earnings growth after 5 consecutive quarters of declines. PATMI of US$18.4bn grew 15% YoY, with net margin of 24.6% expanding by 2%/3% YoY/QoQ as a result. As AI drives improvements in efficiency and productivity, we continue to expect margins to improve moving forward – FY23e PATMI is increased by 4%, with net margin of 24.4% (1H23: 23.1%).

The Negative

- Nil.

The Positives

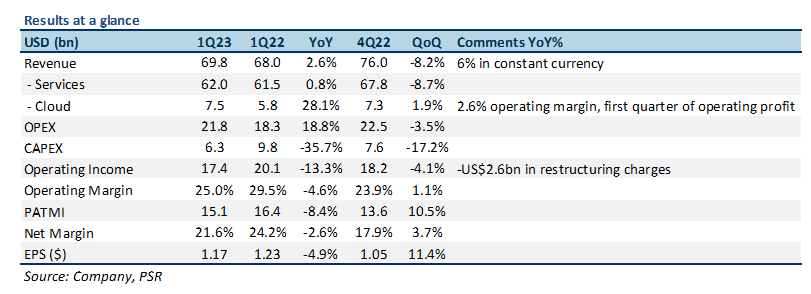

+ Revenue growth re-accelerated slightly due to advertising revenue. GOOGL saw a re-acceleration in revenue growth, posting total revenue of US$69.8bn, 3% YoY (4Q22: 1%). Growth was driven by a 2% YoY increase in advertising revenue from Search (4Q22: -2% YoY) as spending from its travel and retail verticals improved. Additionally, ad revenue from YouTube showed some signs of stabilisation, declining only 3% YoY (4Q22: -8% YoY) as YouTube Shorts monetization increased, offset by some incremental pullback in advertiser spend.

+ Google Cloud momentum slowing, but turned the corner on profitability. Cloud saw some slowdown in its growth momentum, with revenues up 28% YoY (4Q22: 32% YoY). This was led by a continued weaker macro environment, with customers choosing to optimise their current Cloud consumption instead of expanding. Even with topline growth slowing, Cloud posted its first profitable segment, with operating income of US$191mn (1Q22: US$706mn) – operating margin of 2.6%, as management remained focused on driving longer-term profitability in this segment.

+ Earnings in-line with our forecasts. GOOGL announced 1Q23 PATMI of US$15.1bn, in line with our expectations as the company continued to be more prudent with expenses. Earnings were hurt by a US$2.6bn one-off restructuring related charge, offset positively by a US$1bn reduction in depreciation expenses due to an increase in estimated useful life of servers and other equipment, and a delay in timing of its stock-based compensation. 1Q23 PATMI was at 21% of our FY23e forecasts, with Adj. PATMI (excl. restructuring charges) at 24% of our forecasts.

The Negative

- Cautious FY23e outlook. Given the ongoing uncertainty in the macro environment, management remained cautious for the remainder of FY23e, expecting advertising revenue growth to remain muted, with continued decline in Cloud momentum.