The Positives

+ Stronger cash flows. On a full-year basis, free cash flows surged 113% YoY to US$15.1mn, largely due to lower trade receivables.

The Negatives

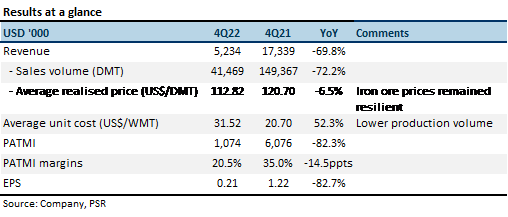

- Lower sales volume. Revenue and PATMI dropped 70% and 83% YoY respectively, due to lower sales volume which dropped 73% YoY. This could be attributed to lower capacity due to the spread of the Omicron variant and unfavourable weather conditions. Revenue and PATMI for FY22 dropped 9% and 21% YoY respectively.

- Net cash to net debt. Fortress Minerals recorded net debt of US$15.2mn in FY22, as compared to net cash of US$5.8mn in FY21. This is due to new bank borrowings of US$23.3mn, mainly used to finance the acquisition of Fortress Mengapur and lower profit after tax recorded in FY22.

Outlook

Demand for iron ore. According to the World Steel Association, YTDMar22, global crude steel production decreased 5% to 458.7mn tons. In 1Q22, China’s crude steel production was down 8.4% YoY to 245.0mn tons (Figure 1).

The National Development and Reform Commission has pledged to continue cutting steel output for 2022. According to the China Iron and Steel Association, the country met the target of controlling steel output last year at 1.035bn tons, down 3% YoY. In 2022, steel demand from the real estate sector is expected to slow down but infrastructure investment is expected to pick up.

Another factor which would be hampering low-grade iron ore demand growth would be the road to decarbonisation of China’s steel industry. This includes producing more steel from electric arc furnaces (EAF), which could use half as much energy as blast furnaces and only emits 25% of carbon dioxide. In the 14th five-year plan, China has set a goal of EAF-produced steel accounting for 15-20% of national steel output. In 2020, EAF-produced steel only accounted for 9.2% of total steel output. This would support the demand for high-grade iron ore which has less impurities.

Supply of iron ore. To reduce reliance on iron ore imports, China would be increasing their iron ore production levels. YTDMar22, iron ore production was up 19% YoY to 250.5mn tons.

Supplies from the world’s two largest iron ore exporting countries have not been keeping pace. YTDApr22, Brazil iron ore exports was down 8% to 76mn tons. YTDFeb22, Australia iron ore exports was up 2.7% to 135mn tons.

The Russia-Ukraine conflict would have minimal impact on China’s iron ore supply. Imports from these two countries accounted for 2.3% of China’s total iron ore imports, while Australia and Brazil accounted for 62% and 21% respectively.

Upgrade to BUY with higher TP of S$0.66, from S$0.50

We have a higher TP of S$0.66, up from S$0.50. We increase FY23e PATMI by 20.7%, as we increase our production forecast by 9.5% to 498,032 DMT. Iron ore prices are expected to remain resilient with higher infrastructure spending by the Chinese government, and slower than expected supply growth from Australia and Brazil. We expect prices to trend around US$150/DMT (Figure 2).

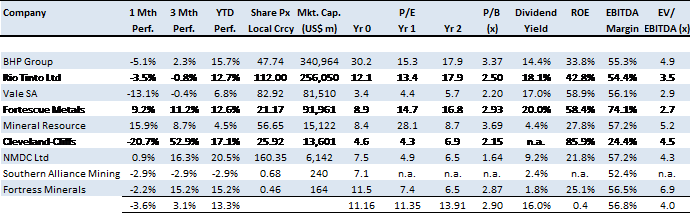

Our TP remains pegged to the industry average, which is 11x FY23e P/E, up from 10x (Figure 3).

Figure 3: Industry peers trading at 11x FY23e P/E

Source: Bloomberg, PSR (Closing prices as at 29 April 2022)

The Positives

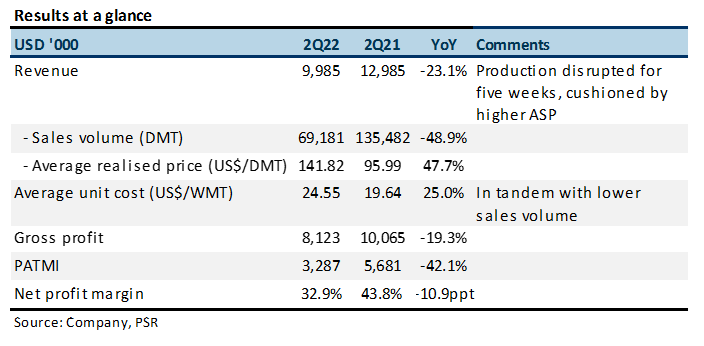

+ Higher iron ore prices. 2Q22 revenue was down 23% YoY due to a 49% collapse in production. The 48% YoY improvement in selling prices offset some of the revenue weakness.

+ Operating cash flow increased. Operating cash flow catapulted from US$54k in 2Q21 to US$6.3mn in 2Q22, with the help of lower working capital. FCF turned positive to US$2.2mn, from US$495k, even with capex increasing to US$4.2mn, from US$549k.

The Negatives

- Lower sales volume. Sales volume was negatively impacted by the production disruptions at Bukit Besi Mine. Mining and processing activities have since resumed on 5 July 2021 at 80% capacity. Average unit cost rose due to the fall in production.

- Higher net debt. Bank borrowings increased from US$166k to US$22.9mn for the acquisition of Fortress Mengapur which was completed in April 2021 and purchase of equipment. Net debt increased further to US$14.7mn since 1Q22.

Updates

FML announced on 12 October 2021 that its subsidiary, Fortress Resources Pte Ltd, has entered into a new offtake agreement with a third-party domestic steel mill in Malaysia. Fortress Resources will deliver 375,000 WMT of iron ore to this customer over a 15-month period from 11 October 2021 to 31 December 2022 (3QFY22 to 4QFY23). The total volume of iron ore concentrate delivered in FY21 was 497,369 WMT.

The Positives

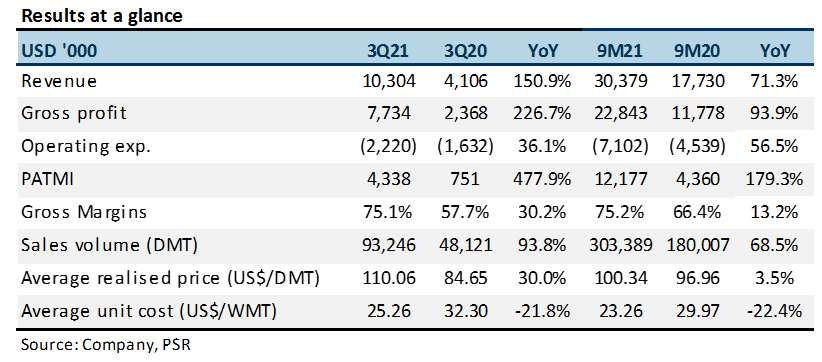

+ Continued volume growth. Iron ore concentrate volumes sold increased 93.7% YoY in 3Q21. This translated to revenue growth of 150.9% YoY. Volume and revenue were both lower QoQ due to monsoon disruptions to production that typically occur at year-end.

+ Spike in margins. Gross margins increased from 57.7% to 75.1% in 3Q21. Revenue for the quarter more than doubled, driven by higher prices for high-grade iron ore concentrates. Their ASP was a record US$110.06/DMT as iron ore prices reached a 7-year high. Average unit cost was also lower YoY through increased iron ore production.

+ Operating cash flow increased 7x. 3Q21 operating cash flow of US$11.7mn was 7x the US$1.6mn achieved a year ago. Net cash slightly dipped from US$9.9mn to US$9mn while FCF turned around from -US$328k in 3Q20 to US$10.4mn in 3Q21.

The Negative

- Nil.

Proposed acquisition of Malaysian subsidiary of Monument Mining Ltd

Monument Mining Ltd (MMY CN, Not Rated) is an established Canadian gold producer that operates gold mines. It also acquires, explores and develops other base metals. FML has entered into a conditional sale and purchase (SPA) agreement with the company for the acquisition of the entire Monument Mengapur (MMSB). MMSB owns a 100% stake in the Mengapur copper and iron project in Pahang, Malaysia. Cash consideration is US$30mn. FML will pay a royalty fee of 1.25% of gross revenue from all products produced at Mengapur to Monument Mining.

Other than magnetite, Mengapur contains a significant amount of copper, gold and silver resources. FML will mine only magnetite for the production of its iron ores. Ores containing other materials encountered during mining will be stockpiled for future use.

With this acquisition, FML’s magnetite resources will surge from 7.18mn tonnes from its Bukit Besi mine as of February 2020 to 17.93mn tonnes. Geochemical analysis and metallurgical tests have proven that the Mengapur magnetite is extremely similar to that from the Bukit Besi mine, which has demonstrated to be economical. FML’s Buki Besi mine has been able to yield consistently-high-grade magnetite iron ore concentrates.

Mengapur is strategically located 65km away from the Kuantan port, the main bulk iron ore export port on Malaysia’s East Coast. It is also within close proximity of the two largest steel mills in Malaysia, both of which are FML’s customers.

Mining leases and environmental approvals for open-pit mining have been obtained. With its existing processing plants and other facilities, the Mengapur site is ready for development. It is immediately available for magnetite production after refurbishment.

This is the company’s first proposed acquisition. If executed according to plan, it should help transform FML into a regional player in iron ores, coupled with its efforts to explore and develop iron ore assets across Malaysia. Mengapur should also complement FML’s existing portfolio of advanced iron ore projects.

Outlook

Iron ore prices are expected to taper down in 2021 as supply balances out demand. We expect them to drop from the current US$190/DMT (Platts IODEX 65% Fe CFR North China) to the region of US$110/DMT. This would translate to lower ASPs of US$95/DMT for FML, from US$110.06/DMT in 3Q21. However, FML’s revenue should still increase with higher iron ore volumes sold following its announcement of an offtake agreement in September 2020. Operating expenses are also expected to be stable with the help of improved economies of scale.

Maintain BUY with higher TP of S$0.47 from S$0.28

We maintain BUY with a higher TP of S$0.47, up from S$0.28, after we increase FY21e PATMI by 69.2% to factor in its 3Q21 outperformance. We continue to peg the stock at 11x FY21e PE, the industry average. We expect production to jump 50% in FY21e and iron ore prices (Platts Iron Ore Index, IODEX 65% Fe CFR North China) to remain above US$110/DMT, providing stock catalysts.