The Positives

+ Time Zone saw faster sales in 3Q22 vs. 1H22. Residential sales of its 17.3%-owned Humen development saw sales accelerate in 3Q22 to 306 units vs. 329 units sold in 1H22. The better sales reflect the recent ease in housing policy restrictions in Dongguan as the Group released another 255 units during the quarter. Housing policy restrictions in Dongguan have been mostly lifted except for the five core districts, where some degree of restrictions are still in place.

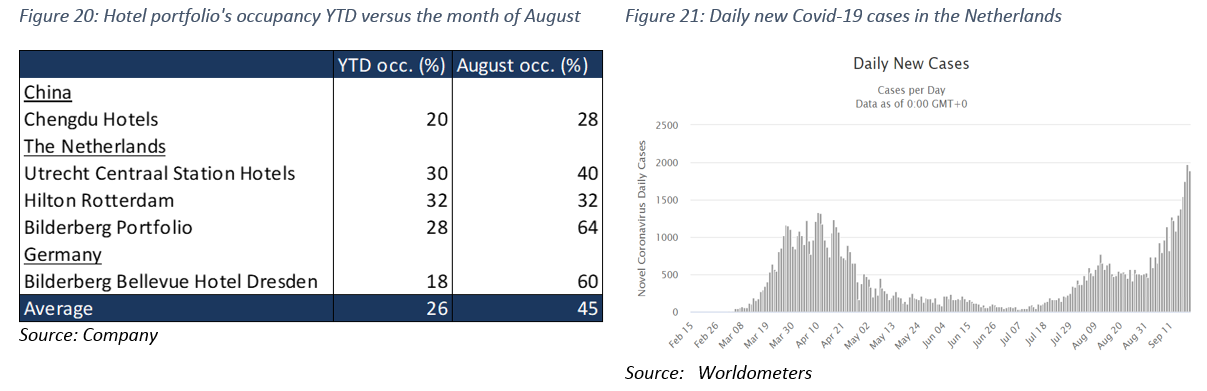

+ European PH saw stronger performances for both its office and hotel portfolio. The Group’s operating results in this segment came in at 77% of FY22e. Its Bilderberg hotel portfolio saw a strong recovery with occupancy increasing to 73.2% vs. 64% in the same period last year. The recovery in its hotel properties was driven by a combination of fewer Covid-19 restrictions and strong leisure and meeting business.

+ Group’s PRC PF loanbook decline less than expected. During the quarter, the Group’s PRC PF loan book stood at RMB1.2bn (-9% YoY) as at 30 Sept 2022, above our estimate of RMB1.09bn. The repayment came from the repayment from the S$97mn and S$89mn junior and senior convertible bonds which it hold for the purpose of financing the acquisition and conversion of the land parcel, and the development of Oasis Mansion.

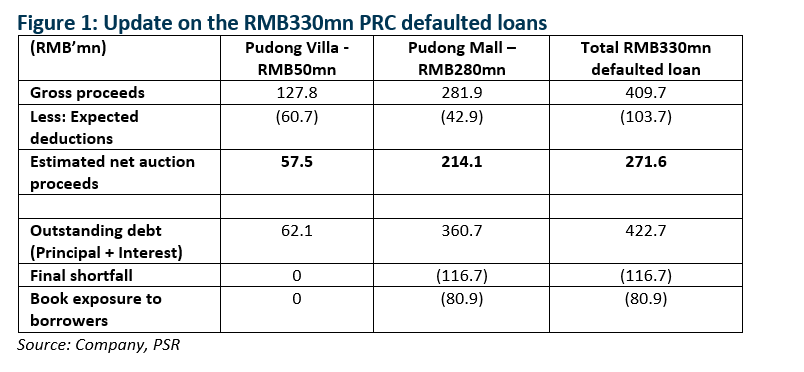

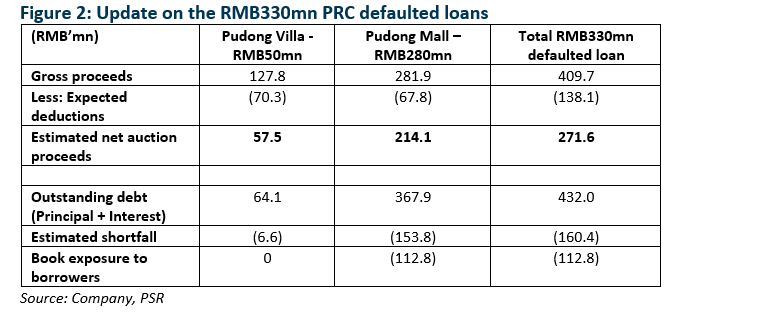

+ Lower tax liabilities see higher recovery of Group’s RMB330mn PRC defaulted loans. The Group’s total tax liabilities for its Pudong Villa and Pudong Mall were settled at about RMB35mn lower than was initially projected. The net effect of this is an overall improvement in its overall net auction proceeds to RMB306mn from RMB271.6mn previously and an improvement to the overall book exposure to RMB80.9mn from RMB112.8mn

|

Potential recovery from the disposal of Pudong Mall. The legal title of the Pudong Mall as well as net auction proceeds of the Pudong Villa are expected to be transferred to the Group in 3Q22. As the Group managed to win the title of the mall through an auction process, we believe there is upside to the valuation of the mall at the end of the year when a valuation is done. We believe the Group will attempt to divest the mall to recover the shortfall, which we estimate to be in FY23e.

The Negatives - Primus Bay residential apartment blocks continue to see slower sales. The pre-sales for the three residential blocks in Panyu, Guangzhou, with 177 units was launched on 26 May this year, with only 13% of the units sold as the weak macro backdrop weighed on sales. ASP of RMB26,200sqm is on the lower end of the spectrum, but we expect pricing to remain stable as the Group will launch the smaller units in 2H22, which should support pricing. |

The Positives

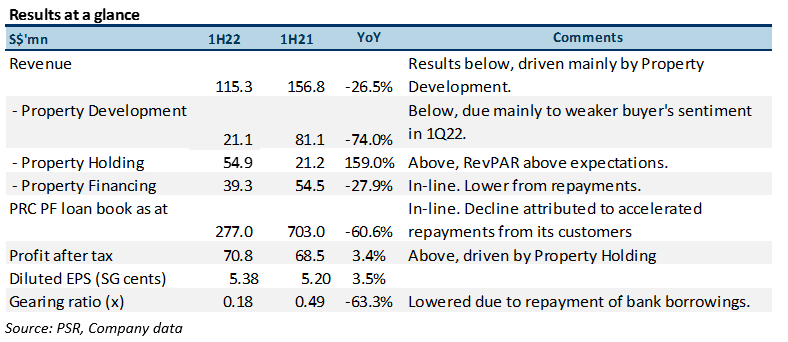

+ 1H22 profit of $71.3mn above our estimates, at 60.5%. The beat came from PH. PH’s profit was driven by the acquisition of the Dutch Bilderberg hotel portfolio it acquired on 2 May 2022 and the overall improvement in RevPAR of its hotel portfolio due to fewer Covid-19 restrictions. All of its hotel properties reported positive profits for 1H22. Interim dividend of 1.1 Singapore cents was in-line with our forecasts.

+ Housing policy relaxation measures in Dongguan drove sales higher. Buyer sentiment in the Dongguan residential market improved after two rounds of housing policy relaxation by the local municipal authorities in May 2022. 190 residential units of its project in Time Zone were sold in 1.5 months after relaxation measures were announced. This was significantly higher than the 139 residential units sold in the first 4.5 months of 2022. We believe this bodes well for the two residential projects it has targeted to launch in 2H22, the Hefu project and Phase 1.2 of its Time Zone development, both in Dongguan.

+ RMB271.6mn in net auction proceeds recovered from RMB330mn in defaulted loans. The Group recovered a portion of the proceeds in April 2022 from the mortgaged properties (Figure 2). The estimated net proceeds of RMB271.6mn however, is insufficient to cover the outstanding loan principal, default and penalty interest and other fees, resulting in an estimated shortfall of RMB160.4mn, with a book exposure of RMB112.8mn left to be collected. The Group will continue to pursue the shortfall via the court process. In other words, if the Group fails to recover such an amount, the negative P&L impact on the Group would be RMB112.8mn.

|

Potential recovery from the disposal of Pudong Mall. The legal title of the Pudong Mall as well as net auction proceeds of the Pudong Villa are expected to be transferred to the Group in 3Q22. As the Group managed to win the title of the mall through an auction process, we believe there is upside to the valuation of the mall at the end of the year when a valuation is done. We believe the Group will attempt to divest the mall to recover the shortfall, which we estimate to be in FY23e.

The Negatives - Primus Bay residential apartment blocks receive muted response at launch. The pre-sales for the three residential blocks in Panyu, Guangzhou, with 177 units was launched on 26 May this year, with only 11% of the units sold as the weak macro backdrop weighed on sales. ASP of RMB26,200sqm is on the lower end of the spectrum, but we expect pricing to remain stable as the Group will launch the smaller units in 2H22, which should support pricing.

|

- Potential impairment of hotels in 2H22 as rates soar. With inflation rates in Netherlands (+8.6% YoY) and Germany (+7.5% YoY) soaring in June and July respectively, management has guided for potential impairments arising from higher rates. The ECB recently raised rates for the first time in 11 years, with a larger than expected rise of 50bps. That said, we expect the impairments, if any, to be offset partially by the continued recovery of RevPAR and occupancy in Europe.

The Positives

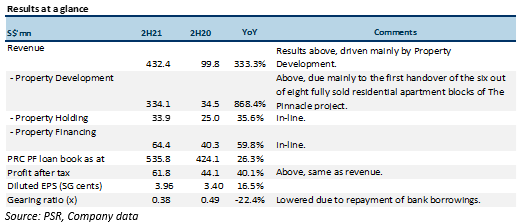

+ 2H21 profit of $61.8mn above our estimates, at 53.6%. The beat came from property development and property financing. The Group made good progress with its various PRC property development projects with the handover of six out of eight fully sold residential apartment blocks of The Pinnacle project in Dongguan in December 2021. The average PRC PF loan book also hit a high of RMB2.7bn in 2021.

+ Revenue from hotel operations showed nascent recovery. Strong leisure demand led to better performance of its European hotel portfolio with revenue from hotel operations increasing 33% YoY in 2H21. Its European hotel portfolio also saw improvements in occupancy, average daily rate (ADR) and revenue per available room (RevPAR) following the easing of COVID-19 measures. According to management, January 2022 continues to be positive and is trending better than 2021.

The resurgence of COVID-19 cases in PRC, however, pared back gains. The implementation of restriction measures in Chengdu led to a weaker performance of its PRC hotels in 2H21 after it had to close the Holiday Inn Express Chengdu Wenjiang Hotspring Hotel for almost a month each in early August 2021 and early November 2021.

+ Revenue from property financing ahead of our expectations as PRC loan book exceeds. The PRC property financing business achieved a record full-year average loan book of RMB2.7bn for FY21.

|

The Negatives - Outlook for property financing disappoints. We believe the recent policy change in China will see clients repaying the loans in favour of bank loans. This, after the People’s Bank of China (PBOC) reduced the reserve requirement ratio for banks by 0.5% in December last year, in a bid to boost economic growth. This resulted in the release of an additional RMB1.2 tn (~$255bn) into the economy. To further ease the lack of liquidity in the property sector, PRC authorities are in the midst of drafting rules to allow developers to access funds from sales that are held in escrow accounts to meet obligations as well as payments.

- Dongguan’s property market slows, inventory rose to 12.5 months from 3.2 months. Curbs on debt and strict COVID-19 measures has negatively impacted property demand in China. According to Reuters’ calculations, property investment declined 13.9% in December 2021 from a year ago, dropping at the fastest rate since early 2020. Unsold housing stock in the PRC’s 100 biggest cities reached a five-year high in November last year. With the slowdown in the property sector, residential inventory in Dongguan rose to 12.5 months from 3.2 months as home buyers remain on the sidelines. |

|

Outlook Weak economic outlook in China clouds Group’s outlook. Falling property prices in China have resulted in a slowdown in demand. Unsold housing stock in the PRC’s 100 biggest cities reached a 5-year high in November last year. Some developers have also resorted to lowering prices to clear inventory, adding to the downward pressure in the property sector.

In January 2022, the PBOC cut the interest rate for the one-year medium-term lending facility from 2.95% to 2.85%. In the same month, the central bank reduced the one-year loan prime rate by another 10 basis points from 3.8% to 3.7% and the five-year loan prime rate by five basis points from 4.65% to 4.6%. To boost liquidity, the PBOC is also offering RMB700bn (S$148.7bn) of one-year medium-term lending facility loans in addition to RMB100bn (S$21.2bn) with seven-day reverse repurchase agreements. All these have culminated in a reduction in the Group’s PRC loan book, and is expected to add further pressure to its PRC loan book in the next two years.

In view of this, we have tweaked our model to account for the lower PRC loan book in the next two years. We lowered our expectations for the Group’s PRC loan book for FY22e-23e by 50% and 16% respectively as we expect customers to start repaying off its loans to refinance with the banks. Consequently, our earnings estimates for its PF business is reduced by 47% and 13% respectively for FY22e and 23e.

Strong balance sheet to capitalise on new opportunities. FSG is backed by a strong balance sheet, substantial unutilised committed credit facilities and potential equity infusion from the exercise of outstanding warrants. The Group is also expected to realise a substantial infusion of cash from the repayment of loans from its customers in the next two years. All of this will further strengthen the cash resources of the Group and to enable it to capitalise on any new business opportunities when they arise.

Downgrade to NEUTRAL from ACCUMULATE with reduced SOTP-TP of S$1.39. As the economic and property outlook in China turns more uncertain, we lowered our earnings expectations for its PD and PF business by 21% and 47% respectively for FY22e. Catalysts for an upgrade are a recovery in the Chinese property market and its China hotel portfolio. |

The Positives

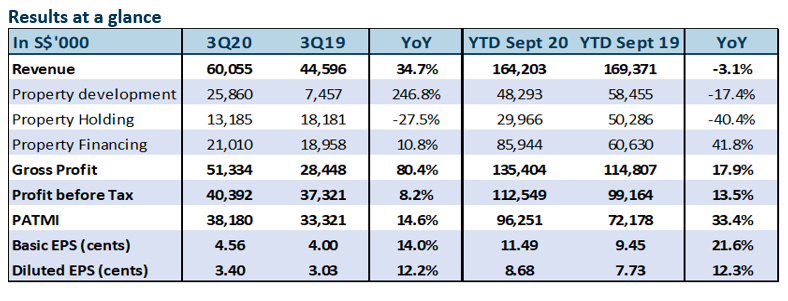

+ Robust 3Q20, notwithstanding Covid-19. 3Q20 revenue rose 34.7% YoY, led by more carpark lots sold at its Millennium Waterfront project (Plot A: 1091; Plot C: 882) which have zero carrying book costs. 9M20 topline held up, largely due to a 41.8% YoY increase in property financing revenue. The increase was aided by one-off loan restructuring income of S$15.5mn and establishment fees from its new development venture in Australia.

+ Better-than-expected property holdings. Its two Wenjiang hotels made a combined gross operating profit of RMB6.7m during the quarter, up 39% YoY. European hotels were mixed. While most of its non-core-city Bilderberg hotels and Bilderberg Bellevue Hotel Dresden in Germany benefited from local leisure demand during summer, its two core-city Bilderberg hotels in Amsterdam and Rotterdam were hit by low corporate demand. Nevertheless, the European hotels made a gross operating profit of €3.9 mn for 3Q20 vis-à-vis -€3.6mn in 1H20.

+ 14.8% YoY DPS growth registered in FY20e. In lieu of a final dividend, FSG has announced a second interim cash DPS of 2.0c for FY20, bringing total DPS declared YTD to 3.1c. This is 14.8% higher than the FY19 full year DPS of 2.7 cents. FSG will work towards a stable dividend payout with a steady growth when appropriate, subject to prevailing market conditions.

The Negatives

- Financial subsidies from governments which cushioned hotel losses to taper off. FSG’s European hotels are being supported by subsidies from the German and Dutch governments, which provided a €4.9mn cushion to the hotels’ gross operating profits. The Dutch government recently announced Temporary Emergency Measure for the Preservation of Jobs (NOW) 3, which is less generous than NOW 1 and 2. NOW 1 and 2 allowed claims of up to 90% of a company's wage bill, depending on loss of turnover. Under NOW 3, the wage claim is capped at 80% and will be decreased every three months: from 80% to 70% and to 60%.

Mixed outlook due to European hotels

Dongguan still vibrant. The Dongguan property market continues to see overwhelming demand for the residential properties and unwavering strength in the selling prices. Most inventories at FSG’s existing projects that were eligible for presales - Star of East River, Emerald of the Orient and the Pinnacle - were sold as of 3Q20. Some properties that are ineligible for presales have also been pre-booked 2-5 years in advance with upfront cash deposits. According to FSG, over 7,000 interested applicants have registered for the presales of 830 units at its upcoming Skyline Garden project. Presales are expected to commence next month. FSG is confident that the units at Skyline Garden will see good buying interest.

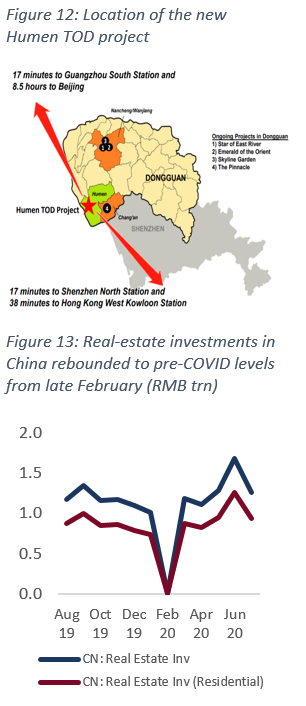

Humen TOD project to be the key project from FY21 onwards. Construction work has begun for the first sector of its newly-acquired Humen transit-oriented development project. Sector 1 has a land area of c.46,300 sqm and constitutes c.231,500 sqm of the 1mn sqm GFA project. We are expecting completion of this sector to bring in c.S$220-230mn of gross development value upon handover in 2022/2023 as the progressive launch of this project is expected to commence in the second half of 2021.

Possible Plot E Sale. The company announced it has been approached by an independent third party with regard to Plot E of the Chengdu Millennium Waterfront project. Plot E is expected to

comprise three blocks of approximately 2,900 SOHO units and an elder care centre of total 304,300 sq m (includes a hospital building of 69,500 sqm), 91,800 sqm of commercial / retail space

and 3,200 underground carpark lots. Upon completion, we are expecting the handover to bring in c.S$630-640mn of gross development value.

Property financing is stable. With regards to FSG’s property financing business, its PRC loan book remained steady at RMB2295.3mn. While FSG continues to receive requests for loans, it remains selective as it is looking to pace its loan growth with its property development business.

Hotel woes. As the number of Covid-19 cases in Europe continues to spike, we are less optimistic on its European hotels, even for the ones located away from cities. 3Q20 occupancy at its Bilderberg Bellevue Hotel Dresden was in the mid-70s to high 90s everyday, as it benefitted from being in the countryside. These numbers have since tumbled to the low 60s-70s. At its key Amsterdam and Rotterdam hotels, occupancy was low teens on good days and low single digits on other days. These hotels would be affected when subsidies from the government dwindle in the coming months. We expect some mark-downs in the fair value of the hotels at year end. A 3% decline in hotel investment properties implies a c.S$1.8mn impact on revenue (FY19 hotel revenue: S$60.8m).

Covid-19 has driven more hotels into liquidation. Some lessees are also looking to return their operating leases. With cash of S$474.9mn and low net gearing of 0.12x, FSG has the balance-sheet strength to pursue opportunities. In October, it successfully refinanced S$50.5mn worth of debt and upsized its revolving credit facilities by S$124.5mn. Coupled with undrawn facilities and potential equity infusions from the exercise of outstanding warrants, FSG is exploring new business opportunities.

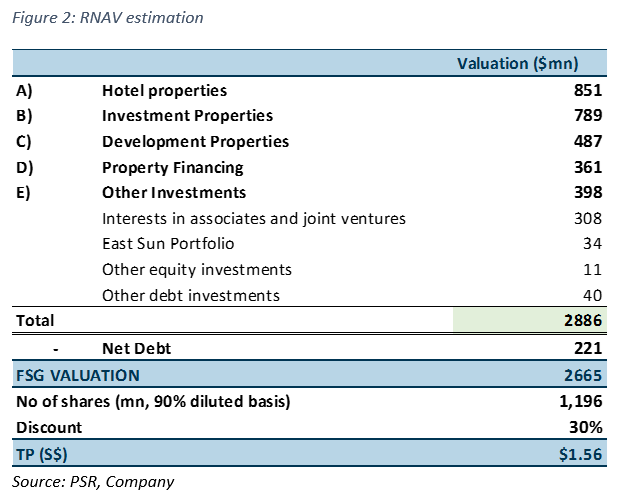

Maintain BUY with revised TP of S$1.56. Our target price implies a total potential return of 24.3% and dividend yield of 2.4%. It remains based on a 30% discount to FSG’s diluted RNAV per share. Our new TP is based on its enlarged share base after its 1:4 bonus warrant issue announced on 23 July, factored on a 90% diluted basis (1196mn) from 100% previously. Unexercised warrants total 416mn, which increase issued ordinary shares to 1,329mn on a fully diluted basis (1H20: 1,102mn). Based on its current 912mn shares, our TP is S$2.04.

The report is produced by Phillip Securities Research under the ‘Research Talent Development Grant Scheme’ (administered by SGX).

Company Background

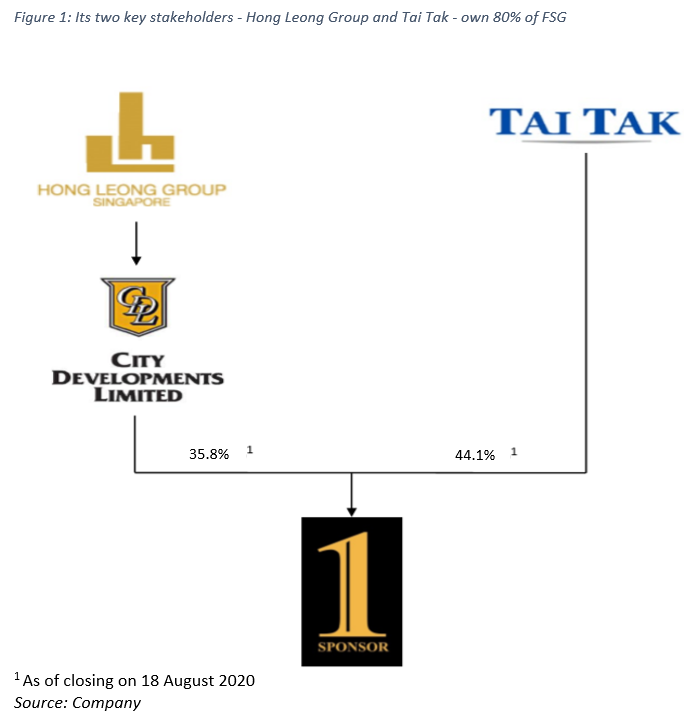

Listed on the mainboard of the SGX on 22 July 2014, First Sponsor Group (FSG) is a property developer (FY19 revenue: 50%), owner (22.5%) and financier (27.5%). It operates in China (FY19 assets: 58%), Europe (40%) and Australia (2%). Hong Leong Group Singapore (35.8%) and Tai Tak Estates (44.1%) are its two controlling shareholders.

Investment Merits

Key risks

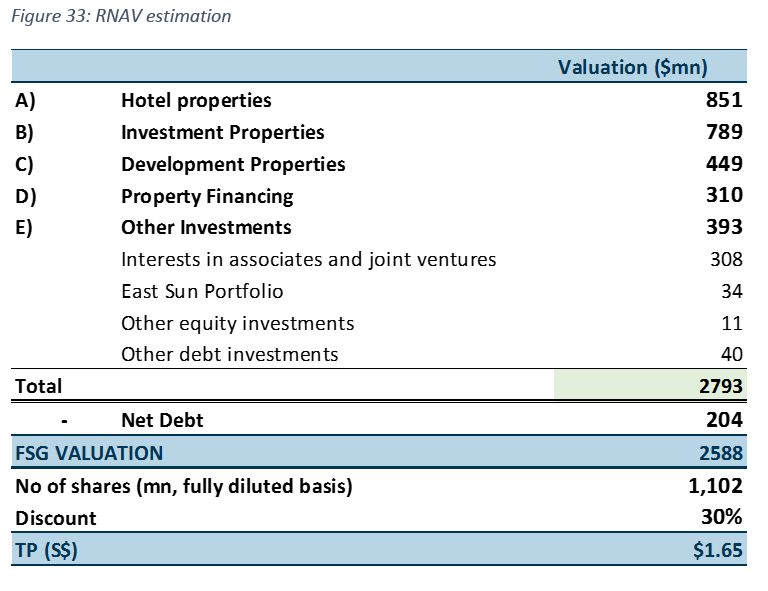

We initiate coverage with a BUY rating. Our target price is S$1.65, based on its historical 30% average discount to RNAV. This implies a potential total return of 33.6% and dividend yield of 1.75%.

About First Sponsor Group Limited

FSG has been listed on the mainboard of the SGX since 22 July 2014. The group is supported by controlling shareholders, the Hong Leong group of companies, through its shareholding interest in City Developments Limited (CIT SP, Current: S$8.09,TP: S$11.68), and Tai Tak Estates Sendirian Berhad, both recognised property-holding companies in Asia.

Hong Leong Group is a globally diversified company with gross assets of over S$40bn, owned by the Kwek family. It employs some 30,000 people around the world. The Group’s four core businesses are property development, hotels, financial services, and trade & industry.

Tai Tak is a family-owned (Ho family) private company incorporated in Singapore in 1954. It invests in a wide range of businesses, including plantations, listed and private equities, property holding and development. The Tai Tak family is one of the largest shareholders of United Overseas Bank (UOB SP, ACCUMULATE, TP: S$20.40). The family was a co-founder of the bank with the Wee family and was the second largest shareholder until the merger of UOB and Overseas Union Bank.

Revenue

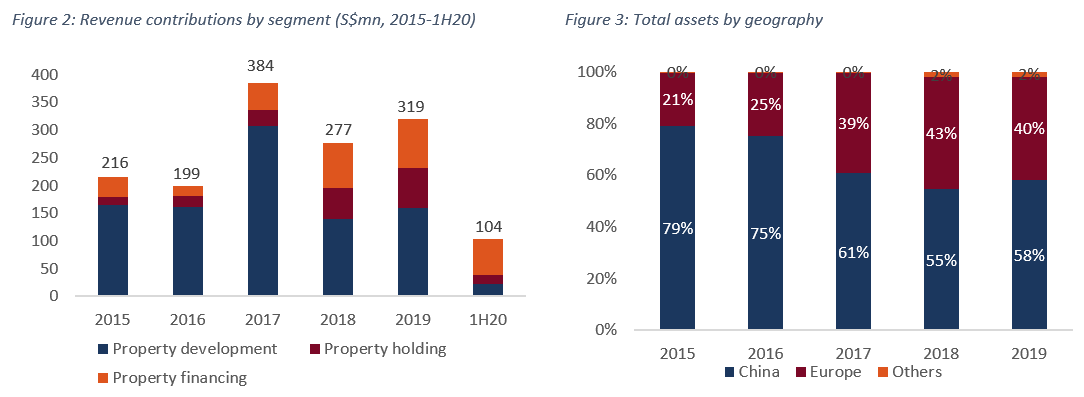

FSG has three operating segments: Property Development, Property Holding and Property Financing.

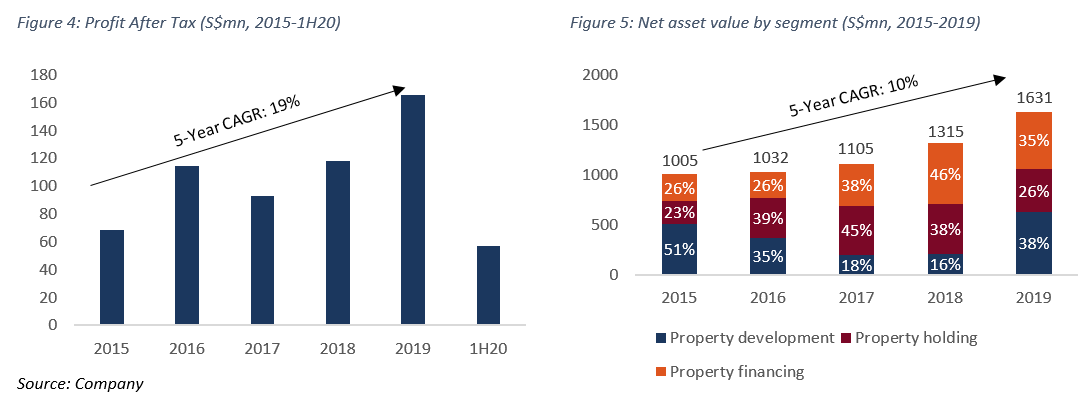

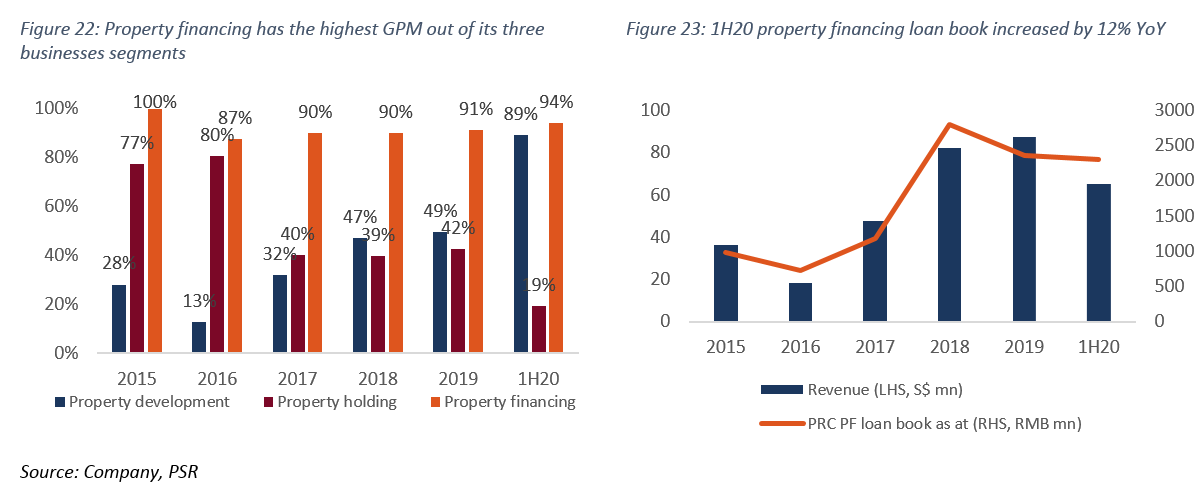

Property Development is historically its largest revenue contributor. In FY19, it contributed 50%, followed by Property Financing’s 27% and Property Holding’s 22%. The bulk of FSG’s income is derived from its operations and assets in the PRC (FY19: 58%) and Europe (40%). In 2015-2019, profit after tax and net asset value grew at CAGRs of 19% and 10% respectively. Property Financing has the highest gross profit margin (Fig. 20).

I. Property Development

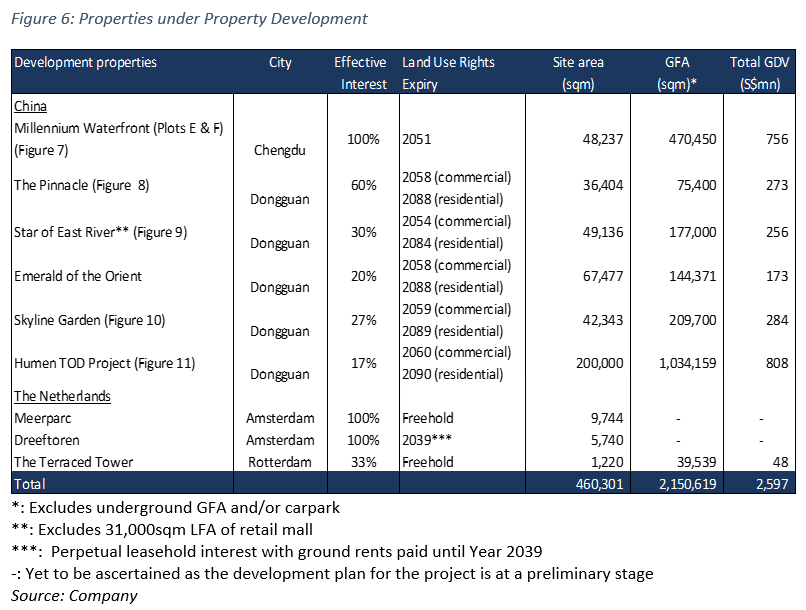

Presently, FSG is working on the Millennium Waterfront, Dongguan portfolio and The Terraced Tower in The Netherlands. Its Dongguan portfolio consists of Star of East River (SoER), Emerald of the Orient (EoO), The Pinnacle, Skyline Garden and the Humen Transit Oriented Development (TOD) Project.

Investment Merits

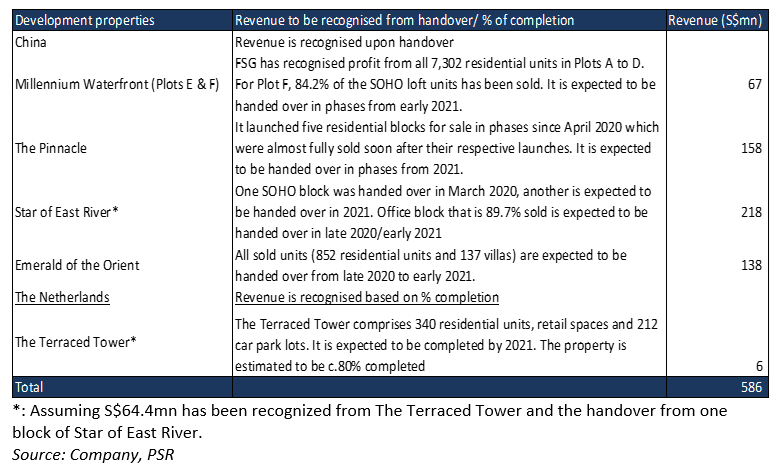

1. Unrecognised revenue from development properties amounts to S$586mn, or 1-2 years of sales. Revenue is only recognised upon handover for its Chinese properties and by percentage of completion for The Terraced Tower. As most of its projects are due for handover either in late 2020 or 2021, we expect the bulk of the revenue to be reflected this and next year.

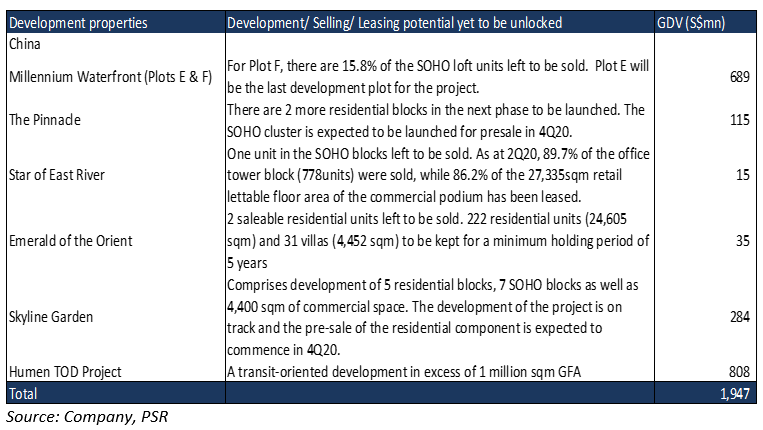

2. GDV of S$1.95bn for unlocking, equivalent to 5-6 years of sales. The largest projects in its pipeline are Plot E Millennium Waterfront and its recently secured Humen TOD project.

3. Humen TOD to become one of FSG’s largest development projects to date (Figs. 11-12). FSG successfully won the bid for a mixed-use development on 29 June at RMB6.6bn (c.S$1.3bn) in a JV with China Poly Group and China State Railway Group. The land will be developed into a transit-oriented development with more than 1mn sqm in GFA, encompassing the different interchanges along Guangzhou, Hongkong, Shenzhen, Humen and Dongguan. FSG has a c.17% effective equity interest in the JV.

4. Unrelenting demand in Dongguan residential market. Dongguan, a city in China's Greater Bay Area, is located between Shenzhen and Guangzhou. It is a manufacturing hub that is receiving an influx of talent, as more companies move to the city. As Shenzhen remains a highly-sought-after market due to its proximity to Hong Kong, Dongguan is benefitting from spillover demand for properties in the Greater Bay Area.

Buying sentiment in the Dongguan property market has exceeded FSG’s expectations after normal business activities resumed in late February. As of 30 June, almost all the SOHO units in its SoER project and saleable residential units in its EoO project had been sold. The Pinnacle project launched five residential blocks for sale in phases from April. These were also almost fully sold soon after their launches. Another residential block in The Pinnacle was launched for pre-sales on 14 July and has since sold more than 85%. The current resurgence of demand has triggered price-control measures from the Dongguan municipal, though the measures appear to have failed to slow down sales. The Group will pace the launch of its remaining two residential blocks in The Pinnacle and five residential blocks in its Skyline Garden project appropriately.

Key Risks

1. Rental abatements provided to retail tenants during Covid-19. Due to the impact of Covid-19, several retail tenants in the Star of East River retail mall requested for concessions to their rental obligations. The amount of rental abatements provided as of 1H20 was about three months of rent. We are expecting an additional waiver of three months to help the tenants tide over the crisis. Total amount of arrears is estimated to be S$2mn.

2. Reassessment of development pipeline to slow down growth plans. FSG obtained an irrevocable building permit to redevelop and increase the net lettable floor area of its Dreeftoren Amsterdam office property (acquired for €11.7mn) by 74% in 2019. In light of prevailing market conditions, it is re-assessing the feasibility of this new residential and office project. If it does not materialise and assuming a net yield of 3%, we are expecting S$0.98mn worth of delay in recurring profits.

II. Property Holding

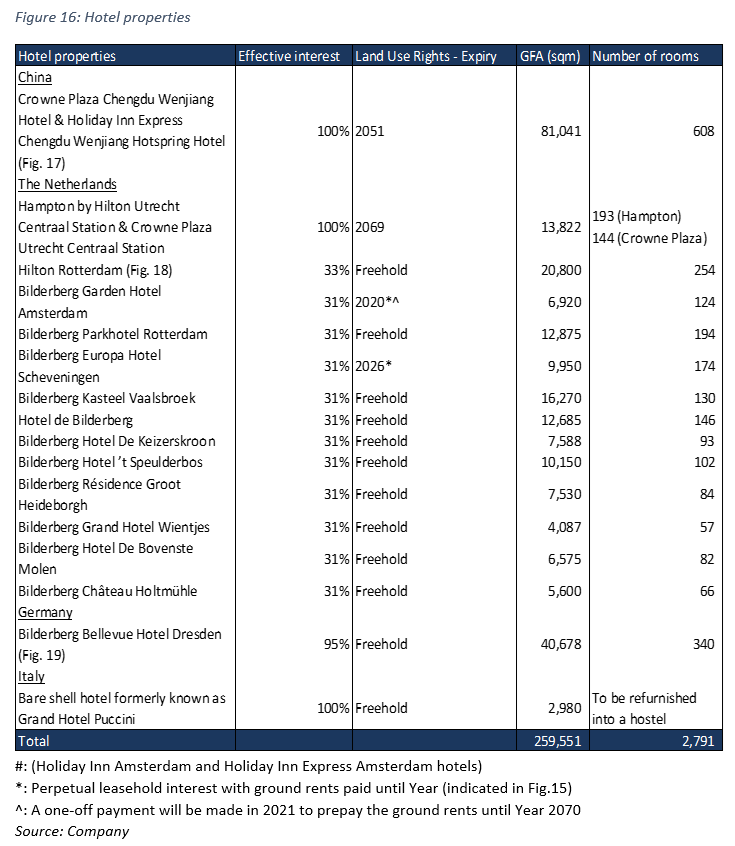

FSG owns a portfolio of hotels and investment properties in Europe (FY19: 13.6% of total assets) and China (7.8%).

Investment Merits

1. Arena Towers provide recurring income at yields of more than 6%. Arena Tower comprise two hotels in Amsterdam and their adjoining car parks that have been leased to external tenants. Each lease contains annual rents indexed to consumer prices and an initial non-cancellable period of 25 years. Despite Covid-19, tenant is still paying rent. In case of default, FSG holds three months of bankers’ guarantees. With regards to the other investment properties, most are paying rent except for a few small tenants.

2. Strong financial standing opens FSG to new opportunities. With cash of S$474.9mn and a low net debt-equity ratio of 0.16x, balance sheet remained robust as at end-1H20. Additionally, undrawn committed long-term debt facilities of S$520.1mn and potential equity infusions from the exercise of outstanding warrants of S$460mn should equip FSG financially to take advantage of acquisition opportunities.

Key Risks

1. Worst may not be over; stunted recovery is expected. FSG’s hotels are located in the parts of Europe where hotels saw a greater recovery in August (Netherlands portfolio ex-Amsterdam/ Rotterdam and Germany), boosted by demand for staycations. However, The Netherlands has seen a resurgence of Covid-19 cases lately, with new cases in September exceeding their peak in April. We are thus expecting a stunted recovery for its hotel portfolio till the end of 2020.

2. Rental arrears at Le Méridien Frankfurt. Le Méridien Frankfurt’s lessee, MHP, closed the hotel in March 2020 without the permission of the landlord and did not pay rent for April 2020. The Group has sought legal advice from its German lawyers on the non-payment of rents for May and June and half the rent for July. As at 21 July 2020, rental arrears amounted to €1.0mn, excluding VAT. The tenant re-opened the hotel on 15 May 2020. FSG holds a one-year banker’s guarantee for this lease. Results of the court hearing will be announced in 3Q20.

3. Reassessment of development pipeline to slow down growth plans. FSG is reconsidering its plan to convert its bare-shell hotel in Milan acquired for €10.7mn in January 2019 into a high-density youth hostel in light of current market conditions. If this development does not materialise and assuming a 5% net yield, we are expecting S$0.86mn worth of delay in recurring profits

III. Property Financing

According to the World Economic Forum, China has one of the largest shadow-banking industries, with about 40% of its outstanding loans tied up in shadow banking. Shadow banking is mainly driven by the need for funding by small and medium-sized private companies (SMEs). These companies are unable to obtain loans from banks, which often prefer to lend to state firms and the larger listed private companies. FSG operates its property-financing business primarily in China via entrusted loans, The Netherlands, Germany, and Australia. In China, FSG only lends in first-tier and second-tier cities where it has a presence in. (Refer to Appendix I – Entrusted Loans).

Investment Merits

1. High recurring income coupled with double-digit growth in loan book. Of all its business lines, property financing has the highest gross profit margin (Fig. 22). This is because funding for this business in China is derived from its Chinese operations, which allows the business to grow at minimal to no costs. The business gives FSG high recurring income underpinned by interest rates of low to mid-teens p.a. Its China loan book grew at a CAGR of 19% from 2015 to 2019, largely attributable to high demand for credit among the SMEs. We are estimating loan book growth of around 8% for FY20e and FY21e. Average tenure for its China loan book is 3 years.

As of 1H20, two defaulted loans had been fully repaid. The YoY increase in revenue in 1H20 (Fig. 21) was mainly due to one-off loan restructuring income of S$15.5mn and establishment fees from its new development venture in Australia.

2. Zero bad-debt losses in eight years of operations; conservative LTV range of 40-60%. FSG started its property-financing business in 2012. To date, it has not incurred any bad-debt losses. Although there were two cases of default in 2015 and 2016, FSG has managed to recover both its principal and interest. A 30.4% annual return was registered for one of these defaulted loans. Average loan to value (LTV) ratio for its portfolio ranges from low 40% to 60%.

3. Maiden venture in Australia to redevelop City Tattersalls Club. FSG holds an equity stake of 39.9% in ICD SB Pitt Street Trust, which is renovating Sydney’s City Tattersalls Club’s premises and developing the airspace above into a hotel and residential apartments. Apart from development fees payable to the trust, FSG will also charge a single-digit interest rate p.a. on a A$370mn (S$368mn) construction loan financing facility to fund the project. The project has received approval for its Stage 1 concept development and construction is expected to start in 2022.

Key Risks

1. Subject to interest-rate cuts for penalty interest. China’s Supreme Court announced a plan in July to cut interest rates that shadow banks can charge for default penalties. The default penalty rate is now limited to 4x the Loan Prime Rate (4.35%) + a court-judged default rate (6%). This means FSG’s return on default loans is now capped at 23.4%, versus no limits previously. The Group had ever recovered defaulted loans at 30.4% p.a. penalty rates in the past.

2. Short-term deferral for interest payments provided for 40% of its China loan book. Amid Covid-19, FSG has given consent to two borrowers of a RMB580mn loan and RMB330mn loan respectively for the short-term deferral of their interest payments.

Others

East Sun and Wanli portfolios. Through a 90% stake in Dongguan East Sun Limited, which has a 49% stake in Dongguan Wan Li Group Limited (Wanli), FSG owns a portfolio of commercial and industrial properties in Dongguan. The East Sun and Wanli portfolios are tenanted with positive running yields.

Update on sale of certain parts of Chengdu Cityspring. In February 2020, the buyer of certain parts of FSG’s Chengdu Cityspring project wrote to the Group to terminate their sale and purchase agreement. In June 2020, the buyer entered into a supplemental agreement with the Group to obtain a discount of RMB3.5m on the purchase consideration for 292 car-park spaces and to acquire another 268 car-park spaces. The total purchase consideration was increased by RMB5.9m to RMB470.9m. The buyer has also withdrawn its termination letter. To date, 89% of the total purchase consideration has been collected, or RMB421.3mn. The outstanding RMB49.6mn will be repaid via monthly instalments of at least RMB10mn.

Disposal of Villa Nuova Office, Zeist, The Netherlands. FSMC completed the sale of Villa Nuova, a 1,428 sqm office property in Zeist, The Netherlands, on 31 Jan 2020. The property was 100% leased with lease expiry on 1 Jun 2022. The sale was completed before the Covid-19 pandemic hit The Netherlands, at a premium of about 8% over its allocated cost. FSMC had enjoyed an annual net rental yield of more than 10% since its purchase in November 2015.

Market Outlook

Property development in China. Hong Kong and mainland China are closely connected. With well-developed cross-boundary transportation networks and cross-boundary facilities, cross-boundary passenger traffic has been on the rise in recent years. In 2018, over 235mn passenger trips were made across the border via land crossings, bringing the daily average to over 640,000 passenger trips.

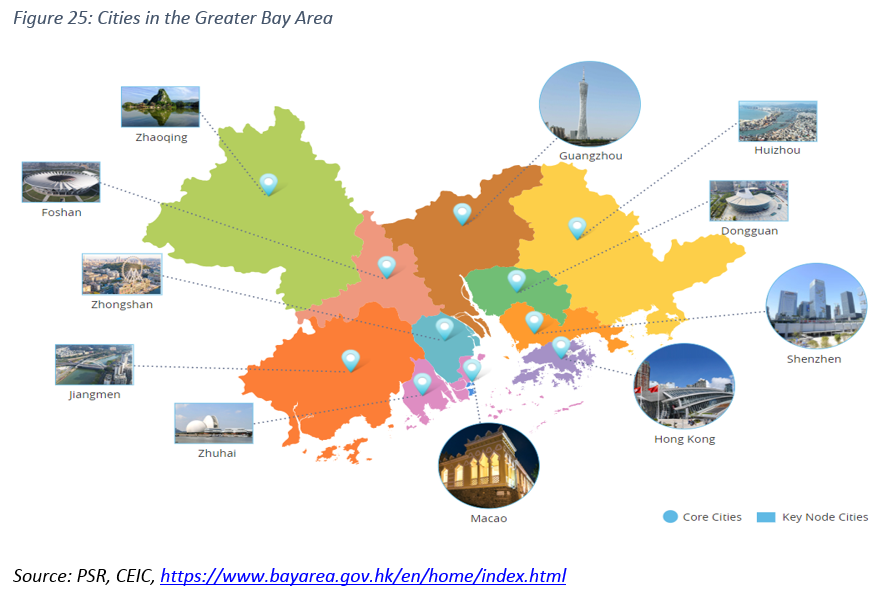

Initiated in July 2017, the Greater Bay Area (Fig. 25) covers the four core cities of Hong Kong, Macao, Guangzhou and Shenzhen as engines for regional development, while supporting Zhuhai, Foshan, Huizhou, Dongguan, Zhongshan, Jiangmen and Zhaoqing to become key node cities with distinct characteristics. The ultimate aim is to raise the development quality of this cluster of cities. The Dongguan property market is expected to continue to benefit from the development of the Greater Bay Area. Additionally, Shenzhen’s continuing dominance as a tech hub could drive demand from mainland and Hong Kong tenants. In March 2020, 288 apartments in a new Shenzhen property development were sold out online in less than eight minutes. Dongguan’s proximity to Shenzhen is expected to position FSG well for capturing spillover demand for residential properties.

Property financing in China. After 2.5 years of regulatory clampdown, shadow banking has returned as China pledges faster credit growth to rescue its coronavirus-hit economy. According to Moody’s, shadow-banking assets in the world’s second-largest economy grew RMB100bn (US$14bn) to RMB59.1trn (US$8.4trn) in the first quarter of 2020, compared with a RMB1.2trn decline to RMB60.2trn during the same period in 2019. A survey in February 2020 of 2,069 small businesses by Zhenghe Island Research Institute found that more than a fifth of the respondents took private loans after Covid-19 broke out. The borrowing binge came with high interest rates. Private lenders in four provinces said they charged annual interest of 18-40%, compared with the benchmark one-year bank lending rate of 3.85%, to offset credit risks among subprime borrowers.

China’s Supreme Court announced a plan in July 2020 to cut the penalty interest rate that shadow banks can charge. The figure could fall as low as 15% a year from 24%, affecting nearly RMB7trn (US$1trn) of outstanding loans. As a result, multiple shadow-banking lenders may stop servicing medium to high-risk borrowers. FSG is selective about the loans it makes, with several criteria to be met by its borrowers (Appendix I – Entrusted Loans). It is also not in the ‘high risk’ business, as evident from the interest rates it charges on its loans relative to the other lenders. Given current economic conditions, it has received overwhelming requests for loans. However, FSG intends to remain discerning and selective.

Property holding in The Netherlands. Amsterdam remains the most attractive city for hotel investments in 2020 for the fourth year in a row due to its positive demand fundamentals and yield profile. Overall arrivals at Amsterdam grew at a CAGR of almost 7% annually over the past 10 years with continuous national y-o-y arrival growth since 2008. In 2019, international inbound tourists (19.5mn) largely comprised EU residents (79%), according to NBTC Holland Marketing. Residents from the US and Asia constituted 11% and 7% respectively. This highlights that inbound tourism is highly reliant on EU travellers.

Member states of the EU were provided with guidelines and recommendations to lift travel restrictions gradually on 13 May. In July, ticket numbers for cross-border air travel within Europe stood at 28% of 2019 levels, as Europeans began to travel again after months of lockdown, according to the travel analysis group, ForwardKeys. However, in recent months, countries across Europe are seeing a resurgence of Covid-19 cases, after successfully slowing down outbreaks earlier. France, Poland, The Netherlands and Spain could be dealing with a much-feared second wave.

The Dutch government has announced specific measures to control the spread of coronavirus. The measures apply to the six safety regions that are currently seeing the sharpest spikes in coronavirus infections. These are Amsterdam-Amstelland, Rotterdam-Rijnmond, Haaglanden, Utrecht, Kennemerland and Hollands Midden. Restrictions include a ban on gatherings of more than 50 people and closing of catering establishments by midnight. The six regions are also adopting specific local measures. We are expecting these restrictions to undo the August recovery for FSG’s hotels in July and August and for hotel occupancy to fall back to YTD levels till the end of the year, before a potential recovery in 2021 should the situation improve.

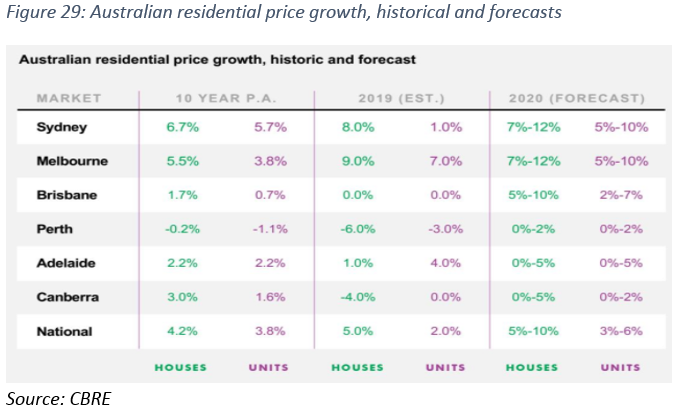

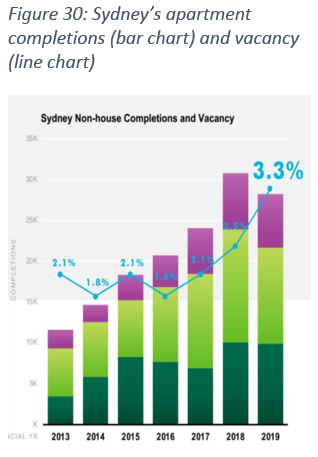

Property Development in Australia. According to CBRE, residential prices in Sydney grew 8% in 2019, though vacancies climbed higher to 3.3% (2018: 2.5%), amid lower apartment completions. We are expecting residential price growth to moderate in 2020 due to existing inventories before the decline in new supply comes through in 2020 and 2021.

For hotels, softer trading conditions in 2020 will be driven by a combination of supply additions and subdued demand growth. New CBD retail luxury brands are expected to attract international visitors after the relaxation of travel restrictions (Fig. 31).

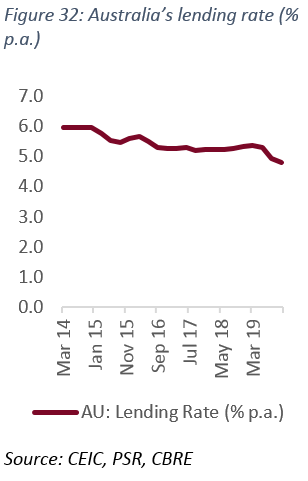

Property financing in Australia. Non-bank lending in the Australian property market is forecast to expand further in 2020, driven by increased interest from both developers and investors. The Australian non-bank loan market has been an essential source of funding for Australian property developers and investors for decades. Domestic banks currently hold around 70% of the corporate lending market, according to Metrics.

Due to the large balance-sheet capacity and capital required to operate in the market, barriers to entry are high. In recent times, banks have come under regulatory pressure to reign in their loan portfolios to meet stricter capital requirements. This has opened up opportunities for non-bank lenders to claim a greater share of the >US$900bn market. For this reason, we expect non-bank lenders to register modest growth in the coming year.

Valuation

We initiate coverage of FSG with a BUY rating and RNAV-derived target price of S$1.65. Our target price implies a total potential return of 33.6% and dividend yield of 1.75%. It is based on a 30% discount to FSG’s fully-diluted RNAVPS (@1,102mn shares after adding outstanding warrants). Based on its current number of shares (912mn), we derive a target price of S$1.99. FSG trades at 0.6x FY20e P/B versus its historical 5-year average of 0.7x.