First REIT – Portfolio restructuring in progress

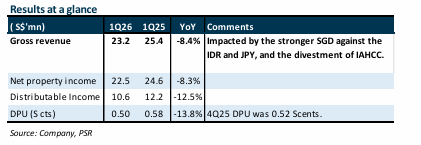

- 1Q26 DPU fell 13.8% YoY to 0.50 Singapore cents, coming in below expectations at just 22% of our FY26e forecast. The decline was mainly driven by weaker IDR and JPY against SGD, as well as the divestment of Imperial Aryaduta Hotel & Country Club. Excluding the divestment, revenue would still have declined 6.8% on a like-for-like basis.

- First REIT has proposed to divest eight hospitals to PT Siloam International Hospitals Tbk (Siloam) and three non-hospital assets in Indonesia for S$471.5mn, alongside a separate put option for the remaining six hospitals at S$294.8mn. The two-tranche divestment of its entire Indonesian portfolio is aimed at prioritising DPU stability and is subject to unitholders’ approval at an upcoming Extraordinary General Meeting (EGM).

- We maintain ACCUMULATE with an unchanged target price of S$0.25, pending completion of the divestments. Our valuation remains based on 1x FY25 P/NAV, reflecting uncertainty over the future portfolio composition, as no assets have been earmarked for acquisition and the REIT is expected to be cash-rich post-divestments. We estimate DPU could decline to c.1.6 cents (excluding special dividends) if the first tranche of divestments completes in Aug 2026. No updates were provided on potential acquisitions, as the ongoing strategic review continues to identify, evaluate and execute opportunities in the APAC region, with the aim of increasing exposure to developed markets.

The Positives

+ Stable operating performance in local currency terms. 1Q26 income from Indonesia and

Singapore properties increased 4.7% and 2.0%, respectively, in local currency terms, while

Japan remained stable. The lease at Siloam Hospitals Lippo Cikarang (SHLC) has been

extended to 31 December 2026, with an option to extend to 30 June 2027. SHLC is part of

the potential divestments under the put option.

+ Stable capital management. The cost of debt declined 60bps QoQ to 3.9%, while ICR was

healthy at 4.4x. Gearing rose from 42.1% to 44.6% QoQ, following the drawdown of debt to

redeem the perpetual bond in January 2026. FIRT also extended its S$300mn term loan and

revolving credit facilities by one year to May 2027. Pending the divestment of its Indonesian

portfolio, we expect FY26 all-in cost of debt to remain stable below 4%, with 44.2% of

borrowings on fixed rates.

The Negative

- Rentals still owed by MPU. Full recovery remains pending in connection with the

transaction, with S$6.6mn outstanding as at 31 March 2026.

First REIT – Proposed divestment of Indonesian assets

- First REIT proposed to divest eight hospitals and three non-hospital assets in Indonesia for S$471.5mn, with a separate put option for the remaining six hospitals at S$294.8mn. The purchaser of the eight hospitals is PT Siloam International Hospitals Tbk (Siloam).

- The two-tranche divestment of all Indonesian assets is designed to prioritise DPU stability while recycling capital from non-core assets and properties with rental arrears. The proposed divestments are subject to unitholders’ approval at an Extraordinary General Meeting (EGM) scheduled for Jun 2026, with targeted completion in Aug 2026.

- We maintain ACCUMULATE with a lower target price of S$0.25 (prev. S$0.29), pending completion of the divestments. We have changed our valuation methodology to 1x FY25 P/NAV from DDM, reflecting uncertainty over the future portfolio composition, as no assets have been earmarked for acquisition and the REIT is expected to be cash-rich post-divestments. We maintain our FY26e DPU forecast at 2.27 cents, pending divestments, but estimate that DPU could decline to c.1.7 cents (excluding special dividends) if the first tranche of divestments completes in Aug 2026. No updates were provided on potential acquisitions, as the strategic review remains ongoing to identify, evaluate, and execute opportunities in the APAC region, with the aim of increasing exposure to developed markets.

Key Highlights

First tranche divestment. The proposed divestment comprises eight hospital assets for

IDR5.1tn (S$389.2mn) and three non-hospital assets for IDR1.1tn (S$82.4mn), bringing the

total consideration to S$471.5mn. This represents a 2.1% premium over the average of the

two latest independent valuations. In connection with the divestments, S$6.9mn in rental

arrears from MPU will be fully repaid.

Second tranche put option. FIRT has the right to divest the remaining six Indonesian

hospitals to Siloam for IDR3.9tn (S$294.8mn) by 31 Oct 2026. Completion of the put option

divestments is subject to certain conditions, including the completion of the first tranche

divestments and unitholders’ approval.

Financial impact. The manager will waive its S$2.4mn divestment fee to align with

unitholders’ interests. The c.S$9.7mn premium over appraised value will be distributed as

special dividends over the two quarters following completion. On a pro forma basis, FY25

DPU would have been 1.39 cents (1.85 cents including special dividends) vs 2.17 cents

reported, assuming completion on 1 Jan 2025. Aggregate leverage would have declined to

16.7% (FY25: 42.1%) assuming completion on 31 Dec 2025.

Use of proceeds. After accounting for associated divestment costs, aggregate net proceeds

of S$464.2mn will be primarily used to pare down debt (S$362.7mn or 78%), with S$9.7mn

(2.1%) committed to unitholders as special distributions. The remaining proceeds will be

allocated to capital expenditure and working capital. FIRT’s remaining debt will then largely

comprise JPY-denominated borrowings, which carry significantly lower interest costs.

What’s next? FIRT will continue to manage its Singapore and Japan assets while transitioning

toward developed markets, benefiting from lower equity risk premiums, lower debt costs,

and more stable currencies. Short-term challenges include finding assets that match

Indonesian yields, but longer-term expansion into developed markets could improve

portfolio quality and reduce exposure to emerging-market currencies.

Maintain ACCUMULATE with a lower TP of S$0.25 (prev. S$0.29).

First REIT – FX remains a drag

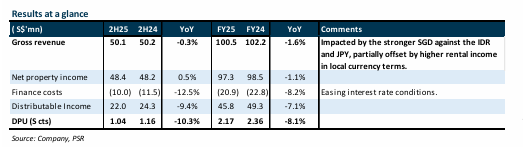

- 2H25/FY25 DPU of 1.04/2.17 Singapore cents (-10.3%/-8.1% YoY) was in line with expectations, forming 48%/100% of our FY25e forecast. The YoY decline was due to the depreciation of the IDR and JPY against the SGD, partially offset by higher local-currency rental income and lower finance costs.

- The divestment of the non-core Imperial Aryaduta Hotel & Country Club (IAHCC) was completed on 4 Dec 2025. Following the redemption of S$33.3mn of 4.9817% subordinated securities in Jan 2026, FIRT no longer has any perpetual securities outstanding. Excluding the IAHCC divestment, portfolio valuations declined 6.2% YoY, mainly due to depreciation in IDR and JPY.

- We maintain ACCUMULATE with a lower DDM-derived target price of S$0.29 (prev. S$0.31) as we roll forward our forecasts. FY26e/27e DPU estimates are reduced by 5%/8% to reflect weaker IDR, JPY, and the divestment of IAHCC. The strategic review of Siloam's intent to acquire FIRT’s Indonesian hospital assets is still ongoing, with no material updates to date. In the meantime, FIRT continues to benefit from the base 4.5% rental escalation across its Indonesia portfolio, as more Indonesian hospitals transition to performance-based rent (currently three). FIRT trades at an FY26e DPU yield of 8.4%.

The Positives

+ Stable operating performance in local currency terms. FY25 income from Indonesia and

Singapore properties rose by 5.1% and 2.0%, respectively, in local currency terms, while

Japan remained stable.

+ Stable capital management. The cost of debt declined by 50bps YoY to 4.5%, while gearing

and ICR remained healthy at 42.1% and 3.7x, respectively. FIRT is in discussions to extend

and refinance S$260mn of loans due in 2026. We expect FY26e all-in cost of debt to remain

around 4.5%, with 46.1% of debt on fixed rates.

The Negative

- Rentals continue to be owed by MPU, with S$6.9mn outstanding as at 31 Dec 2025.

S$1.5mn was received in Jan 2026, reducing the amount owed to S$5.4mn.

- Decline in portfolio valuations. On a same-store basis, valuations fell 6.2%, primarily due

to FX headwinds. In local currency terms, the Indonesia portfolio rose 1.4% on higher rents,

while the Japan portfolio declined 0.7%. The Singapore portfolio declined by 5.8% due to

decreasing land tenure.

First REIT – Earnings stability tempered by FX

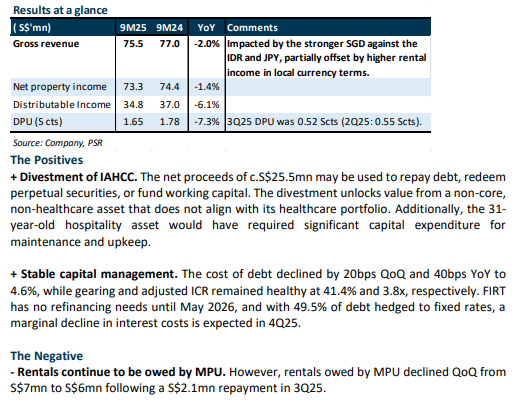

- 3Q25/9M25 DPU of 0.52/1.65 Singapore cents (-10.3%/-7.3 YoY) was slightly below our estimates, forming 23%/73% of our FY25e forecast. The YoY decline in DPU was due to depreciation of the IDR and JPY against the SGD, partially offset by higher rental income in local currency terms.

- Rental income for 9M25 from Indonesia and Singapore grew 5.5% and 2% respectively in local currency terms, while Japan remained stable. On 17 October, FIRT announced the proposed divestment of Imperial Aryaduta Hotel & Country Club (IAHCC) for Rp.322.2bn (S$25.9mn), representing a 22% premium over its original purchase price and 0.65% above the latest valuation.

- We downgrade from BUY to ACCUMULATE with an unchanged DDM-derived target price of S$0.31 due to the recent share price performance. FY25e/26e DPU estimates are trimmed by 4%/2% to reflect the weaker Indonesian Rupiah and Japanese Yen. The strategic review of Siloam's letter of intent (LOI) to acquire FIRT’s Indonesian hospital assets remains ongoing, with no material updates as of 3Q25. In the meantime, organic growth will be driven by more Indonesian hospitals transitioning to performance-based rent (currently three). FIRT trades at an FY25e DPU yield of 7.8%.

First REIT – Facing ongoing FX headwinds

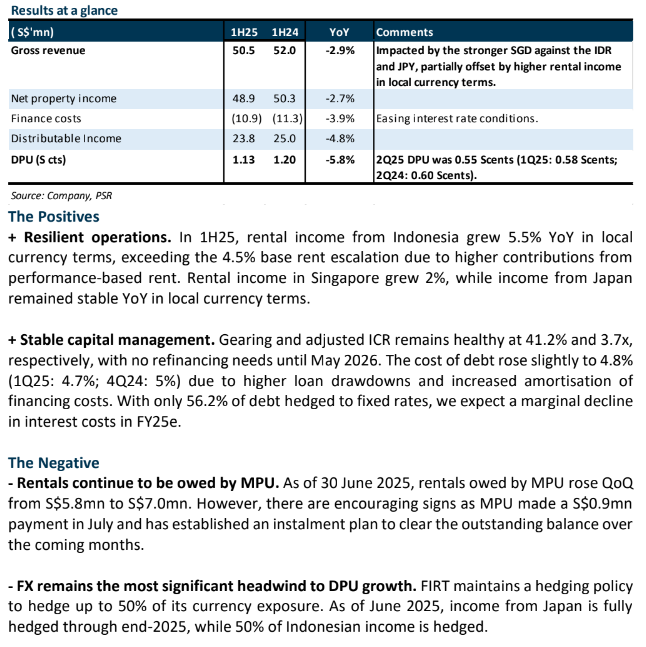

- 2Q25/1H25 DPU of 0.55/1.13 Singapore cents (-8.3%/-5.8 YoY) was slightly below our estimates, forming 23%/48% of our FY25e forecast. The YoY decline in DPU was due to the depreciation of the IDR and JPY against the SGD, partially offset by higher rental income in local currency terms.

- Rental income from Indonesia and Singapore rose 5.5% and 2% respectively in local currency terms, while income from Japan remained stable. As of 30 June 2025, overdue rent from PT MPU stood at S$7.0mn (1Q25: S$5.8mn), with S$0.9mn received in July 2025.

- Maintain BUY with a lower DDM-derived target price of S$0.31 (prev. S$0.32). We trim our FY25e/26e DPU estimates by 3%/1% due to ongoing FX headwinds, particularly the weaker Rupiah. Despite this, FIRT offers an attractive FY25e DPU yield of 8.4%. It is undergoing a strategic review in response to Siloam's letter of intent (LOI) to acquire its Indonesian hospital assets, with no material updates as of 2Q25. In the meantime, organic growth will be driven by more Indonesian hospitals transitioning to performance-based rent from the current three.

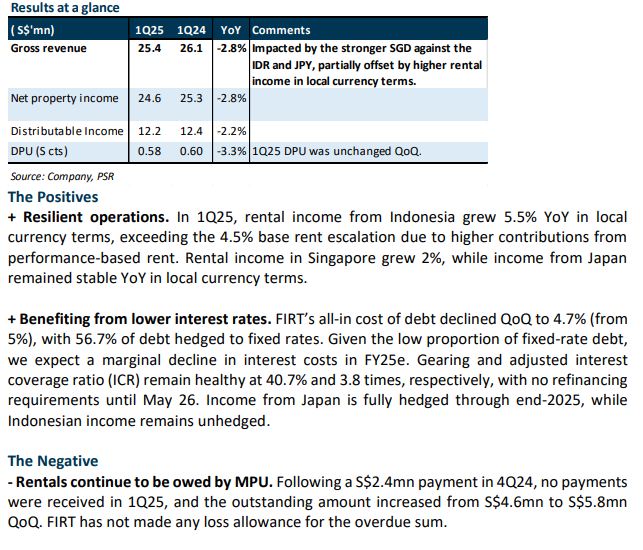

First REIT – Stable operations undermined by FX

- 1Q25 DPU of 0.58 Singapore cents (-3.3% YoY) was slightly below our estimates, forming 23% of our FY25e forecast. The YoY decline in DPU was due to the depreciation of the IDR and JPY against the SGD, partially offset by higher rental income in local currency terms. 1Q25 DPU of 0.58 cents was unchanged QoQ.

- With 56.7% of its debt hedged to fixed rates, FIRT benefited from lower interest rates, bringing its all-in cost of debt down to 4.7% (Dec 24: 5.0%). After receiving S$2.4mn from MPU in 4Q24, no payments were made in 1Q25, bringing the total overdue rent to S$5.8mn as of 31 March 2025.

- Maintain BUY with an unchanged DDM-derived target price of S$0.32. We trim our FY25e/26e DPU estimates by 6%/4% to reflect ongoing FX headwinds. Despite this, FIRT is still trading at an attractive FY25e DPU yield of 9.2%. FIRT is undergoing a strategic review to assess Siloam's letter of intent (LOI) to acquire its hospital assets in Indonesia, with no material developments as of 1Q25. Organic growth will come from more Indonesian hospitals achieving performance-based rent.

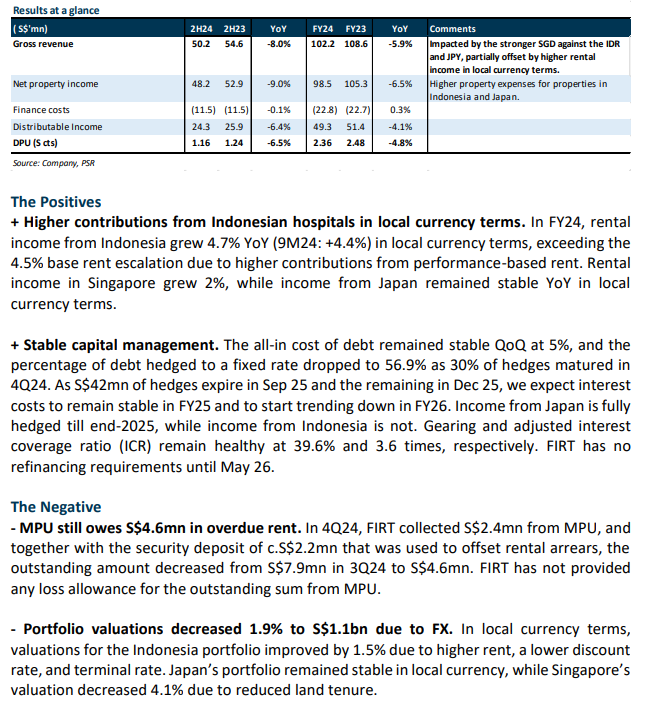

First REIT – Impacted by FX headwinds

- 4Q24/FY24 DPU of 0.58/2.36 Singapore cents (-6.5%/-4.8% YoY) was in line with our estimates, forming 25%/100% of our FY24e forecast. The YoY decline in DPU was due to the depreciation of the IDR and JPY against the SGD, partially offset by higher rental income in local currency terms. 4Q24 DPU of 0.58 cents was unchanged QoQ.

- Revenue growth for Indonesian properties in local currency terms improved in 4Q24 to 5.5% YoY (9M24: +4.4%), driven by higher performance-based rents. MPU made some payments in 4Q24 but still owes S$4.6mn as of 31 December 2024.

- Maintain BUY with a higher DDM-derived target price of S$0.32 (prev. S$0.30) as we roll forward our forecasts. Our estimates remain unchanged. First REIT is trading at an attractive forward FY25e distribution yield of 9.2%. Organic growth will come from more Indonesian hospitals achieving performance-based rent. FIRT is conducting a strategic review to assess Siloam's letter of intent (LOI) to acquire its hospital assets in Indonesia and to evaluate all options, aiming to deliver long-term value for unitholders.

First REIT – A buyer for Indonesian hospitals

- FIRT received a preliminary non-binding letter of intent (LOI) from PT Siloam International Hospitals Tbk (Siloam) to acquire FIRT’s portfolio of 14 Indonesian hospitals (72% of AUM). We view this positively as (i) Siloam’s interest in the assets supports the inherent value of the Indonesian hospitals, (ii) the proceeds from the sale could provide FIRT with more financial capacity for future acquisitions in developed markets such as Australia and Japan, and (iii) the sale could unlock considerable value for unitholders. Siloam is the current tenant and operator of the hospitals and is 65% owned and controlled by CVC Capital Partners.

- FIRT’s NAV per share of 29.16 cents is reinforced by Siloam’s interest as a buyer. Also, we expect any sale of the Indonesian hospitals to be above valuations in order to gain shareholder approval.

- Maintain BUY with an unchanged DDM-derived target price of S$0.30. FIRT is undergoing a strategic review to evaluate all options and deliver sustainable long-term value for its unitholders. There is also no certainty that any transaction will materialise from the strategic review or LOI. As this LOI is in its preliminary stage, there is no change to our estimates. FIRT is trading at an attractive forward FY24e/25e distribution yield of 8.9%/9.5%.

First REIT – Hurt by the weak IDR and JPY

- 3Q24/9M24 DPU of 0.58/1.78 Singapore cents (-6.5%/-4.3% YoY) was in line with our estimates, forming 25%/75% of our FY24e forecast. The drop in DPU was due to the depreciation of the IDR and JPY against the SGD. 3Q24 DPU was 3.3% lower than the two preceding quarters of 0.60 cents per quarter.

- Revenue growth in local currency terms remained stable in 3Q24, with a YoY increase of 4.4% for properties in Indonesia, 2% for nursing homes in Singapore, and flat performance in Japan. Rentals outstanding from MPU amounted to S$7.9mn as of 3Q24.

- Maintain BUY with an unchanged DDM-derived target price of S$0.30. Our estimates remain unchanged. First REIT is trading at an attractive forward FY24e distribution yield of 8.9%. Organic growth will come from more Indonesian hospitals achieving performance-based rent. Potential catalysts include the divestment of non-core assets, such as Imperial Aryaduta Hotel and Country Club (IAHCC), and the reinvestment of proceeds to fund acquisitions in developed markets as part of the First REIT 2.0 growth strategy aimed at achieving over 50% of AUM in developed markets by FY27.

First REIT – A stable quarter with stable DPU

• 1H24 DPU of 1.20 Singapore cents (-3.2% YoY) was in line with our expectations, forming 51% of our FY24e forecast. 1H24 DPU was lower YoY mainly due to the stronger SGD against the IDR and JPY. 2Q24 DPU was stable QoQ at 0.60 Singapore cents.

• 1H24 revenue in local currency terms grew 4.4% YoY for properties in Indonesia, 2% YoY for nursing homes in Singapore, and remained stable in Japan. Finance costs grew marginally by 0.8% (S$0.1mn) YoY due to good interest rate risk and currency risk management.

• Maintain BUY with an unchanged DDM-derived target price of S$0.30. First REIT is trading at an attractive 16% discount to NAV and a forward FY24e distribution yield of 9.3%. Organic growth will stem from more Indonesian hospitals achieving performance-based rent. Potential catalysts include the successful divestment of non-core assets such as Imperial Aryaduta Hotel and Country Club (IAHCC) and recycling the proceeds to fund acquisitions in developed markets as part of its First REIT 2.0 growth strategy. Our estimates remained unchanged.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report