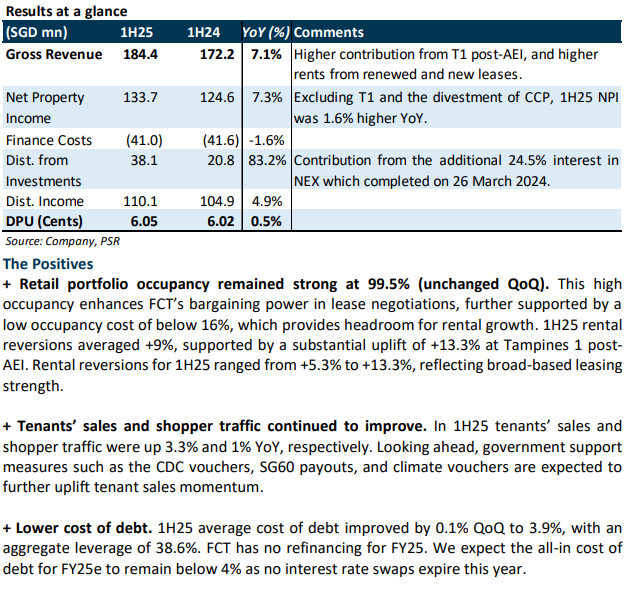

The Positives

+ 2Q24 retail portfolio occupancy remained almost full at 99.9% (unchanged QoQ). Occupancy was at least 99% across all the malls. 1H24 rental reversion of +7.5% exceeded our expectations, and it was above 1H23 rental reversion of +4.3%. We expect this healthy positive rental reversion trend to continue for the remaining 14% of leases (by GRI) that expire in FY24.

+ Improvements in tenants’ sales and shopper traffic. 2Q24 tenants’ sales and shopper traffic were 4.3% and 8.1% higher YoY, respectively. Portfolio shopper traffic is now only 2% below pre-COVID levels, while tenant sales are c.20% higher than pre-COVID levels. We expect tenants’ sales to remain robust, supported by the various government handouts to Singapore residents in 2024.

+ All-in cost of debt improved 10bps QoQ to 4.2%, as FCT used the proceeds from the divestments of Changi City Point and interest in Hektar REIT to pay off some of the higher-cost debt. Aggregate leverage rose 1.3%pts QoQ to 38.5% as loans were drawn down to finance the increased stake in NEX and the Tampines 1 AEI. 68.5% of debt is hedged to a fixed rate. FCT has no debt expiring in FY24, and its ICR is 3.26 times. FY24e all-in cost of debt is expected to be low 4%.

The Negative

- nil

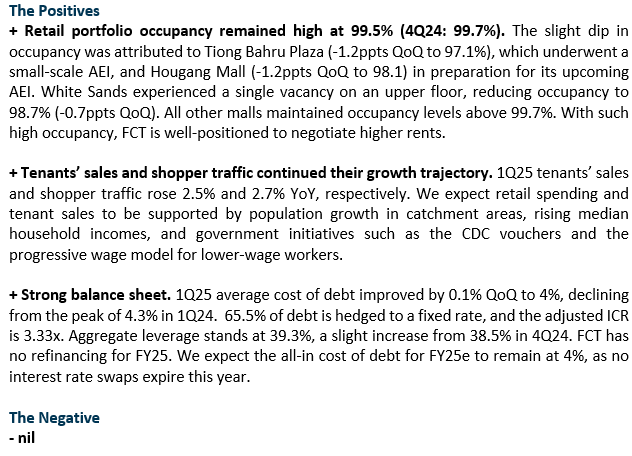

The Positives

+ Retail portfolio occupancy is almost full at 99.9% (+1.5ppts YoY; +0.2ppts QoQ). Management guided that rental reversions for the quarter were above FY23’s +4.7%, and we expect this positive rental reversion trend to continue for the 20.3% of leases (by GRI) that expire in FY24.

+ Gearing improved from 39.3% to 37.2%, after using the proceeds from the divestments of Changi City Point and interest in Hektar REIT to pay off some debt. The all-in cost of debt increased 20bps QoQ to 4.3%, and the proportion of fixed-interest rate borrowings stands at 63.4%. Green loans now account for 72.5% of total borrowings. FCT has no debt expiring in FY24.

The Negative

- Tenant sales were down 0.7% YoY in 1Q24 due to several key anchor tenants undergoing renovations, and from a higher base in 2023. Excluding this, it was up 1.1% and was 18% above pre-COVID levels. Portfolio shopper traffic was 3.1% higher YoY, and F&B continues to be the key demand driver. Occupancy cost remains healthy at 15.5%.

The Positives

+ Retail portfolio occupancy nearly full at 99.7% (+2.2ppts YoY; +1.0ppts QoQ). Excluding Tampines 1 which is undergoing AEI, occupancy at all nine malls came in at 99% or higher. Rental reversions for the retail portfolio were +4.7% for FY23; and we expect similar rental reversions for FY24e, when 29.3% of leases by GRI will be expiring.

+ Tenants’ sales and shopper traffic continued to grow 7.3% and 24.7% YoY respectively for FY23 indicating robust demand. FY23 tenants’ sales averaged c.17% above pre-COVID levels. Improving tenants’ sales should lower occupancy costs further (currently at 15.6% and 6-year lows), and this should support FCT’s ability to raise rents.

+ Retail portfolio valuation increased by S$52.7 million, or 0.6%, to S$8.74bn with unchanged cap rates. This suggests that suburban retail malls in Singapore continue to exhibit resilience despite rising interest rates. The below-historical-average and low retail supply of 1.21mn sq ft through to 2025 makes up only 2.4% of the current private retail stock, and this is expected to support valuations and rental rates going forward.

+ No refinancing risks in FY24. After S$353.5mn, or 16%, of total debt that was originally due in FY24 has been refinanced to FY29, there are no more refinancing requirements in FY24.

63% of total debt has been hedged to fixed rate, and the YTD all-in cost of debt increased 10bps QoQ to 3.8%. We expect the all-in cost of debt to increase to above 4% in FY24e. ICR remains healthy at 3.47x. Gearing, currently at 39.3%, is expected to drop to 36.1% on a pro forma basis assuming the net proceeds from the divestment of Changi City Point and interest in Hektar REIT are used to repay certain debts.

The Negative

- Higher operating costs from higher energy and water prices, as well as higher manpower costs, will likely eat into NPI margins in FY24e. We expect NPI margins to drop from 71.8% in FY23 to 70.6% in FY24e.

The Positives

+ Retail portfolio occupancy remained high at 98.7% (+1.6ppts YoY; -0.5ppts QoQ). The lower occupancy QoQ was largely due to a 6.4ppt drop in occupancy at Changi City Point from 99% to 92.6%. This was mainly transitionary vacancies as FCT looks to reposition the mall by bringing in popular brands such as Coach. Excluding Tampines 1 which is undergoing AEI, occupancy at the eight malls came in at 92.6% or higher, with six malls having an occupancy of 98.6% or higher. The recently acquired NEX, in which FCT holds a 25.5% stake, has a committed occupancy of 100%. Only 4.2% of leases by GRI are up for renewal for the rest of this financial year.

+ Tenant sales and shopper traffic continued to grow 5% and 16% YoY respectively in 3Q23 indicating robust demand. YTD tenants’ sales averaged c.16% above pre-COVID levels. Trade sectors that performed well were F&B, fashion and accessories, electronics, and beauty. Essential trades like supermarkets and healthcare are still performing well above pre-COVID levels but are growing at a slower pace from the higher base in 2022.

The Negative

- Gearing increased from 39.6% to 40.2%, and the proportion of fixed interest rate borrowings decreased from 76.4% as at 1H23 to 63.0%. The YTD all-in cost of debt increased 10bps QoQ to 3.7% after refinancing all loans due in FY23. FCT has collaborated with OCBC on its green loan offering with carbon credits and the proceeds from this loan will be used to refinance debt that is expiring in FY24. Green loans account for c.49.8% of total borrowings (Mar23: 37.9%).

Outlook

Improving tenant sales should lower occupancy costs further (currently below 16% and 5-year lows), and this should support FCT’s ability to raise rents. Inorganic growth opportunities include the acquisition of the sponsor’s pipeline of assets such as the 24.5% effective interest in NEX and Northpoint City South Wing.

AEI works have commenced at Tampines 1 in 2Q23 and is on schedule for completion in 3Q24. The mall continues to operate as works are staged and more than 90% of AEI spaces have been pre-committed to date.

Maintain ACCUMULATE, DDM TP unchanged at S$2.35

Catalysts include stronger than forecast reversions and accretive acquisitions. Risks include a slowdown in retail sales. The current share price implies a FY23e DPU yield of 5.6%.

The Positives

+ Retail portfolio occupancy improved 0.8%-point QoQ to 99.2%, mainly due to the backfilling of the anchor cinema space at Century Square, taking its occupancy from 88.7% to 96.8%. Occupancy at all nine malls came in at above 96.8%, with five malls having an occupancy of 99% or higher. 1H23 rental reversions for the retail portfolio were +1.9%, up from +1.5% in FY22. After starting FY23 with 27.6% of leases (by GRI) expiring in the year, 11.4% remain for the rest of this financial year. As a reflection of the strong underlying demand, about 16.2% of leases (by GRI) have been renewed in 1HFY23, with 11.4% yet to be renewed by this FY.

+ Tenant sales and shopper traffic grew 9.2% and 35.3% YoY, indicating resilient retail sales. However, we expect tenant sales growth to moderate going forward due to the increase in Goods and Services Tax rate and a slowdown in consumer spending.

The Negative

- Gearing increased from 33.9% to 39.6%, due to the increase in bank borrowings to finance the acquisitions of the effective 25.5% stake in NEX and the additional 10% stake in Waterway Point which were completed in February 2023. However, the proportion of fixed interest rate borrowings increased from 73.2% as at 1Q23 to 76.4%, and the all-in cost of debt increased only 10bps QoQ to 3.6%. FCT indicated that it has secured financing to refinance all borrowings due in FY23 (17.7% of total), which we think is likely at above 4%.

The Positives

+ Retail portfolio occupancy improved 0.9% QoQ to 98.4%, aided by Century Square (+1.9%), Changi City Point (+4.1%), White Sands (+1.9%) and Hougang Mall (+1.6%). Leases signed in the quarter were at positive rental reversions. Occupancy at eight of their nine malls came in at above 97.8%. Leasing negotiations are ongoing to backfill the anchor space (~8% NLA) at Century Square left by Filmgarde.

+ Tenant sales and shopper traffic grew 13.4% and 38.3% YoY, averaging 116% and 82% of pre-pandemic levels for the quarter, respectively. However, we expect tenant sales growth to moderate to single digits going forward due to the increase in Goods and Services Tax and a slowdown in consumer spending.

The Negative

- High cost of debt. All in cost of debt for 1Q23 increased 50bps QoQ to 3.5%. FCT’s 73% of debt hedged to fixed rate (Sep 22: 71%) is on the lower end compared to most peers. About 46% of debt matures in FY23-FY24 and is likely to be refinanced at above 4%.

The Acquisition

Outlook

FCT announced a S$38mn asset enhancement initiative (AEI) for Tampines 1 where NLA from lower yielding floors will be transferred to B1, L1 and L2 as well as an additional c.8000 sq ft of NLA from various bonus GFA schemes. Management estimated a ROI of 8% on the back of higher rents and asset valuation gains. FCT’s operating metrics continues to improve, but its short debt maturity and low interest hedge ratio will offset these gains going forward.

Maintain ACCUMULATE, TP lowered from S$2.38 to S$2.31

FY23e-FY25e DPU estimates are trimmed by 6-8% after factoring the NEX acquisition and higher borrowing costs. The current share price implies a FY23e DPU yield of 5.5%.