The Positives

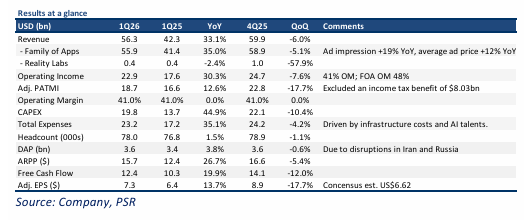

+ Resilient ad performance. META delivered robust advertising performance in 1Q26, with

ad revenue reaching US$55bn, up 33% YoY (1Q25: +16%), driven by higher engagement and

improved monetisation across its Family of Apps ecosystem. The performance was supported

by the integration of Muse Spark, META’s newly launched natively multimodal reasoning

model by Meta Superintelligent Lab (MSL), which enhanced content personalisation and

recommendation capabilities across platforms. Following deployment, Instagram Reels time

spent increased 10% YoY while Facebook video time spent rose over 8% YoY, marking the

strongest QoQ engagement improvement in four years. The company also reported 19% YoY

increase in ad impressions (1Q25: +5%) and a 12% YoY rise in average price per ad (1Q25:

+10%), highlighting continued monetisation strength. Given the strong early traction and

scalability potential of Muse Spark across platforms, including WhatsApp, Instagram, and

Messenger, we maintain our FY26e advertising forecasts and continue to expect 30% YoY

revenue growth.

The Negative

- Loss-making continued in Reality Lab. META’s non-core Reality Labs segment remains

unprofitable, but operating losses narrowed ~4% YoY to US$4.2bn. (1Q25: losses +9.5%).

Segment revenue declined 2% YoY to US$885mn (1Q25: -6%), primarily due to lower Quest

headset sales. However, the company saw AI glasses continue to perform well, with daily

users growing 3x YoY.

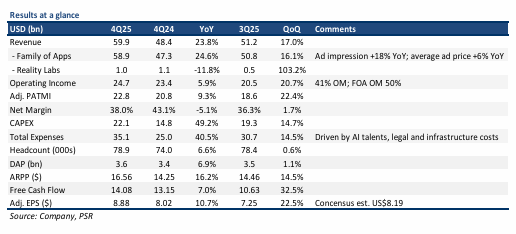

The Positives

Continued strong AI-led ad performance. META delivered robust advertising performance in

4Q25, with ad revenue reaching US$58.1bn, up 24% YoY (4Q24: +21% YoY) driven by higher

user engagement and strong advertiser demand supported by improved ad efficiency.

Looking ahead, we expect FY26e revenue growth to remain underpinned by broad-based AI

improvements, with particularly attractive monetisation and engagement opportunities in

video and Threads. In the US, Instagram Reels watch time increased 30% YoY following

improvements in recommendation quality, and Facebook video watch time grew double

digits YoY supported by ranking and product enhancements across feed and video surfaces.

Continued model optimisation lifted organic Feed and video views by 7%, delivering the

largest quarterly revenue impact from Facebook product launches in the past two years, while

time spent on Threads rose 20% following recommendation upgrades. Based on this

momentum, we increased our FY26e ad revenue forecast by 7%, expecting 30% YoY revenue

growth.

Resilient WhatsApp performance. In 4Q25, META’s Family of Apps “other” revenue grew 54%

YoY to US$8.1bn, supported by WhatsApp paid messaging and Meta verified subscription

(4Q24: +55% YoY). Business messaging maintained strong momentum, with click-to-message

ads in the US rising more than 50% YoY, driven by robust adoption of website-to-message

ads, which guide users to the business’s website for more information before initiating a chat.

Additionally, paid messaging continues to scale, reaching an annual run-rate of over US$2bn

in 4Q25.

The Negative

Unprofitable in Reality Lab. META’s non-core Reality Labs segment remains unprofitable, with

operating losses widening 21% YoY to US$6bn. (4Q24: losses +7% YoY). Segment revenue

declined 12% YoY, primarily due to a high base following the launch of Quest 3S in 4Q24 and

earlier revenue realisation from retail partners’ headset purchases ahead of the holiday season

in 3Q25. Looking ahead, META expects Reality Labs' operating losses to have peaked, with FY26e

losses broadly in line with FY25 levels (FY25: US$19.2bn) before gradually narrowing thereafter.

Strategically, the company plans to focus investment on glasses, where sales more than tripled

in FY25, while working toward building a profitable virtual reality (VR) ecosystem over the longer

term.

Higher CAPEX going into FY26e. In 4Q25, META’s CAPEX nearly doubled to US$22.1bn (4Q24:

+88% YoY) with the majority of spending directed toward data centres, servers, and network

infrastructure. For FY26e, the company has guided CAPEX to US$115bn–US$135bn to support

its core advertising business and the expansion of Meta Superintelligent Lab (MSL). If spending

reaches the top end of guidance, it would imply ~87% YoY CAPEX growth. Despite aggressive AI

spending, META’s free cash flow grew 7% YoY in 4Q25. The surge in CAPEX is expected to weigh

on valuations in the short term due to higher depreciation and AI-related expenses, which rose

40% YoY in 4Q25 (4Q24: +5%). However, we believe the impact should be offset by robust

revenue growth in core advertising segment. We think the company demonstrated a strong

ability to monetise existing products while effectively expanding its potential pipelines to grow

its advertising ecosystem

The Positives

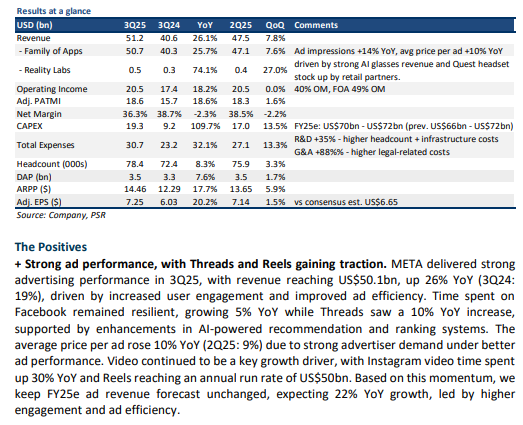

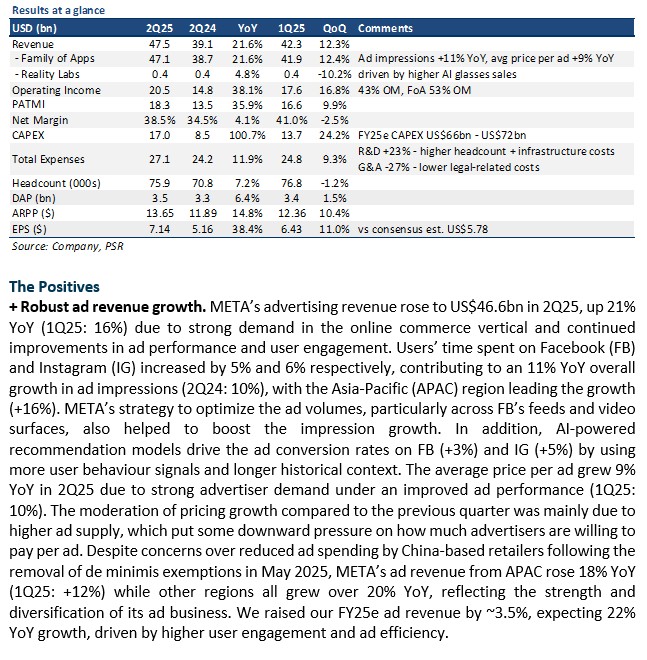

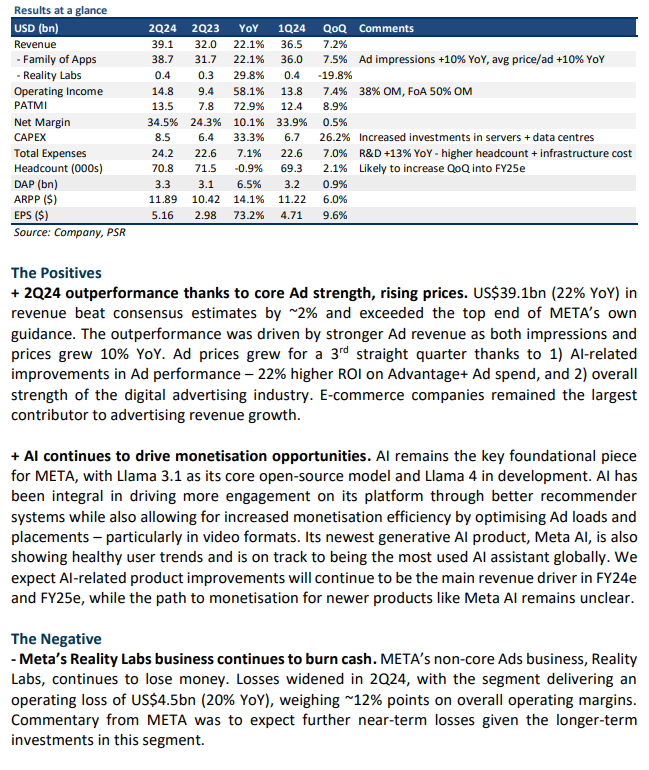

+ AI content driving greater engagement, leading to higher ad revenue. META continues to leverage its AI capabilities to improve engagement on its apps, indirectly leading to higher ad revenue (+27% YoY). META’s AI recommendation system now contributes roughly half of all content users see on Instagram, driving more value for advertisers. The demand-supply dynamics of digital ads are also improving, with META seeing healthy 20+% YoY growth in impressions and a 2nd consecutive quarter of YoY advertising price increases. E-commerce companies remained the largest contributor to advertising revenue growth.

+ Positive momentum for Video/Reels. Video engagement continues to be a bright spot for META, contributing to >60% of viewing time on both FB and IG. Reels remain the key driver for this growth, with its strong ramp throughout FY23. Reels monetisation is also improving with META leveraging AI for more optimised ad loads and placements.

The Negatives

- Higher CAPEX spending moving forward. META is doubling down on scaling its AI capabilities to develop more advanced and compute-intensive models while also scaling its training and inferencing needs (custom silicon). As a result, FY24e CAPEX guidance was raised by ~US$4bn to a range of US$35bn-US$40bn. It expects this investment cycle to take at least 2 years to complete.

- Decelerating revenue growth for 2Q24e. META guided to 2Q24e revenue growth of ~18% YoY, implying a deceleration in growth as it: 1) laps a period of tougher comparisons due to China recovery from early-FY23, 2) slower increase in Reels’ advertising load after an initial aggressive ramp, 3) ~1% YoY impact from a strengthening USD.

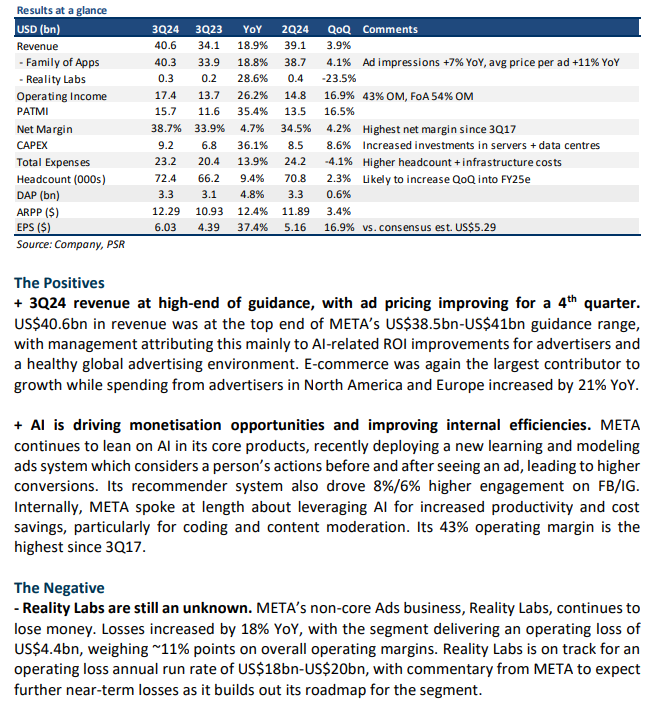

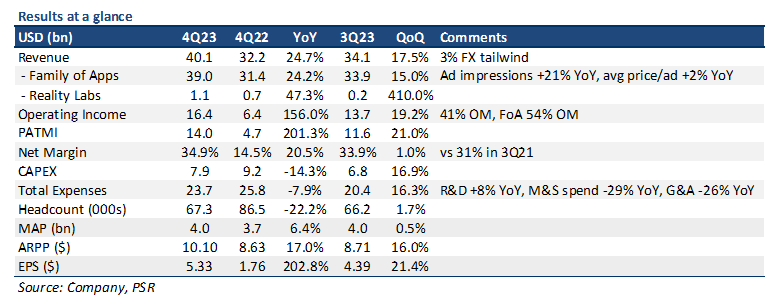

The Positives

+ Beat on both top and bottom line showing year of efficiency has played out well. Revenue of US$40.1bn beat our estimates by 7%, driven by a 3% FX tailwind, a 21% YoY growth in ad impressions, and a 2% YoY increase in average price per ad (CPM). CPMs grew for the first time in 2 years, driven largely by APAC+China demand. 4Q24 PATMI increased 3x YoY to US$14.0bn, as META benefitted from strong revenue growth and a much leaner workforce – headcount/total expenses were both down 22%/8% YoY, respectively.

+ Well-positioned to build the most advanced AI products with a stockpile of GPUs. META remains focused on building out its tech infrastructure, stating that it intends to have the equivalent of ~600K H100 GPUs (350K H100s + remaining 250K of other GPUs) worth of computing power by the end of FY24e. This is enough compute to support Reels, and another Reels-sized AI service. In addition, its open-source software infrastructure should help attract top AI talent to develop Llama models and other AI products.

+ Reels commentary positive, contributing net revenue to META. In 4Q23, Reels drove >25% YoY growth in daily watch time across all video types, with Reels re-shared 3.5bn times a day. Historically, Reels growth has been a headwind to overall revenue growth due to its lower monetisation levels. However, it is starting to contribute net revenue to META, with the company further expecting Reels to leverage a unified recommendation system across all META patforms to drive further views and engagement.

The Negative

- Raised top end of FY24e CAPEX guidance. META raised the top end of its CAPEX guidance for FY24e by US$2bn, to US$30bn-US$37bn, indicating it expects the need for higher levels of server capacity to support more intense AI product development. We raise our FY24e CAPEX by 3% as a result.

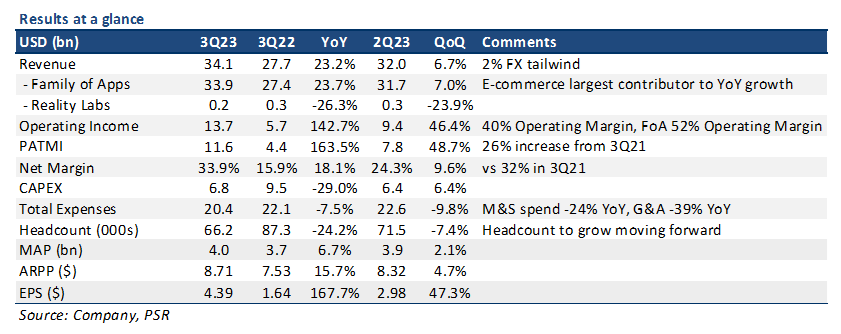

The Positives

+ Advertising trends continued to accelerate. META saw a huge acceleration in digital advertising revenue (3Q23: 24% YoY vs 2Q23: 12% YoY). Much of this acceleration was contributed by e-commerce companies, particularly from outbound Chinese advertisers trying to reach other markets like the US and Brazil. We expect these trends to continue improving given a typically strong 4Q holiday season, and a general recovery in the digital advertising industry.

+ Reels monetisation no longer a headwind. Reels – which has been a near-term headwind given its lower levels of monetisation, reached an inflection point. Monetisation levels for Reels finally reached net neutral to overall revenue as a result of ranking improvements and increasing ad supply. We think that this is significant given the incremental time spent on short-form video formats like Reels vs Feed/Stories. Moving forward, we expect Reels to be a modest tailwind to revenue growth as it continues to improve its monetisation levels.

+ Earnings grew ~2.5x YoY; highest margins in >2 years. PATMI increased 164% YoY, with net margins of 34%, its highest since 2Q21. Earnings also beat consensus estimates by 21% on higher revenue growth, and a leaner cost structure after significant cost-cutting measures over the last 12 months. Headcount was down -24% YoY.

The Negative

- Uncertain growth outlook for 4Q23e, increasing expenses into FY24e. META issued a fairly wide revenue guidance for 4Q23e, with a range of US$36.5bn-40bn (implying a 13%-24% YoY growth) due to concerns over increasing volatility led by geopolitical events in the middle east. It also guided to a reacceleration in total expenses growth for FY24e (10% YoY), citing increasing AI-related investments and payroll expenses.

ddle