The Positives

+ High income visibility due to portfolio occupancy of 99.1% (-0.8ppts QoQ), and WALE by GRI of 3.8 years. 74% of FY20e revenue is secured through 4 master leases to the Sponsor, with built-in rental escalations ranging 1% to 3% (commentary on master lease below). Hengde Logistics, the specialised logistics asset customised for and leased to a state-owned tobacco company, contributes c.13% to NPI. This brings the percentage of “stable” leases to 87%.

+ Running cost of interest fell QoQ from 4.4% to 4.3%. This is likely attributed to ECW increasing the interest rate hedge in 1Q20 from 72.2% to 100%, and the lower interest rates in FY20 versus FY19.

The Negatives

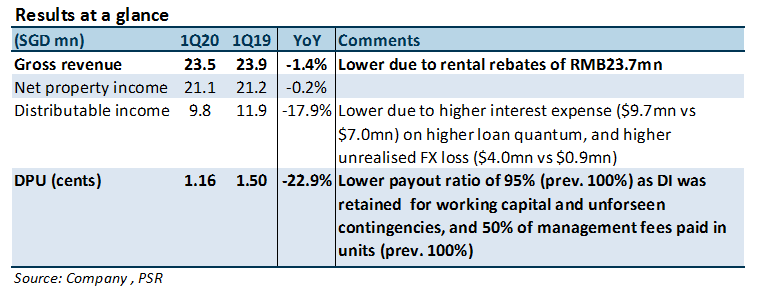

- Accretion from the acquisition of Fuzhou E-commerce wiped out. DPU fell 22.9% YoY in 1Q20 due to granting rental rebates of RMB23.7mn, unfavourable FX, higher finance expense and a 5% retention of distributable income (DI). Higher finance expense was due to the higher loan quantum from acquiring Fuzhou E-commerce (completed on 8 August 2019). Excluding rental rebates, DPU would have been 5.129 cents, 1.9% higher YoY.

Outlook

Commentary on Master Leases

Master leases to the Sponsor make up c.74% of ECW’s NPI. We note that c.S$3.2mn out of the S$4.6mn (70%) of the rental rebates offered to tenants went to the Sponsor for namely 2 assets, Chongxian Port Investments and Beigang. The rebates to the Sponsor are deemed equitable and in line with the Sponsor’s contribution to revenue. Trade receivables ballooned by S$18.8mn (roughly 51%) QoQ, indicating that 80% of 1Q20’s revenue of S$23.5mn has not been collected. While the spike in arrears understandable given that business disruption to tenants, we note that some of the arrears could be attributed to the leases to the Sponsor, given that he Sponsor was responsible for 73.6% of 1Q20’s revenues. As of 31 March 2020, no outstanding trade receivables are past 180 days due. There are security deposits of 9.9 months for Chongxian Port Logistics and 11.4 months for Beigang in place, while there is a corporate guarantee in place for the Fuzhou E-commerce asset.

Since the lifting of the lockdown in China, all tenants have resumed operations as at 31 March 2020. Tenants are in the process of ramping up operations and are back to 90% of pre-lockdown levels.

The 5% retention of distributable income in 4Q19 and 1Q20 amounts to c.S$1.1mn, retained for working capital purposes and buffer against unforeseen contingencies.

After the RMB23.7mn (c.S$4.6mn, approximately 0.5months) in tenant rebates were offered in 1Q20, the management has not received any material request for rental assistance or restructuring of leases.

In the previous quarter, the management received notifications of non-renewal of 24,929sqm of space up on a lease expiring in 2Q20 at Wuhan Meiluote. This represents 50% of Wuhan Meiluote’s NLA of 48,695sqm. Occupancy is expected to fall from 97.7% to 46.7%. This asset contributes 1.6% to gross rental income (GRI) and will not affect DPU materially. Muted leasing demand is expected in the near term.

15.7% of leases by GRI is up for renewal in FY20, half of which is for space at Hengde Logistics which is leased out to a state-owned tobacco company at below-market rentals. However, negotiations for a higher rental may be viewed as insensitive, as the country is in a state of flux, brought on by the Covid-19 outbreak. As such, the management is guiding for flattish rental reversions on all leases expiring in FY20. The rest of the expiring leases are attributed to the Wuhan Meiluote and Chongxian Port Logistics assets.

Key management personnel and the Directors of the Manager will be taking a 10% reduction in remuneration and fees for the 3-month period from April 2020 to June 2020. The manager has elected to receive 50% of base fees in the form of units (previously 100%) from the quarter ended 31 March 2020 onwards.

Maintain BUY with lower TP of S$0.77 (prev. S$0.83).

We trim our FY20e/FY21e DPU by 5.6% and 3.9% respectively to incorporate the rental rebate for FY20, lower rental reversion on expiring leases and the lower management fees that will be paid in units (from 100% to 50%). Additionally, we increase our cost of equity from 9.23% to 9.45% to reflect the higher market risk. Our TP is cut by 7.2% to $0.77, which translates to a FY20e and FY21e DPU yield of 9.0% and 9.6% respectively.

The Positives

+ Solid portfolio to weather turbulence. High income visibility due to portfolio occupancy of 99.9%, and WALE by GRI of 4.1 years. Post-acquisition of Fuzhou E-Commerce, 84.4% of FY20e revenue is secured through 4 master leases to the Sponsor, with build-in rental escalations ranging 1% to 3%. Hengde Logistics, the specialised logistic asset customized for and leased to a state-owned tobacco company, contributes c.8% to NPI. This brings the percentage of “stable” leases to 91%.

The Negatives

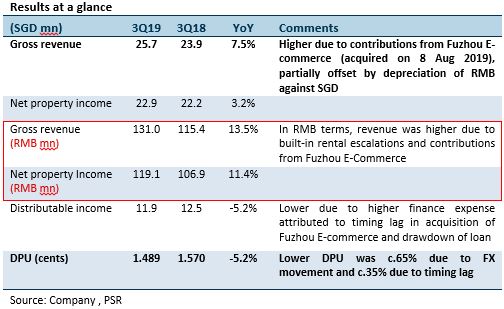

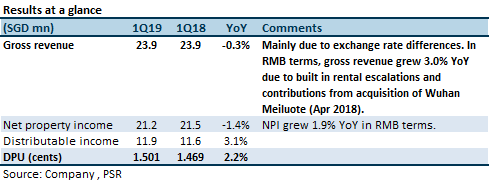

- Accretion from the acquisition of Fuzhou E-commerce wiped out. DPU -3.8%/-2.1% in 4Q19/FY19 due to FX and higher finance expense and 5% retention of distributable income (DI) in 4Q19. Higher finance expense was due to the timing mismatch of drawdown of loans and the acquisition of Fuzhou E-Commerce and the higher loan quantum. Acquisition financing for Fuzhou E-commerce (completed on 8 August 2019) was done in conjunction with the refinancing of the IPO loans (28 June and 8 August). DPU would have been 6.13 cents if 100% of 4Q19 DI was paid out, but this would still have been 0.8% lower than FY18 DPU of 6.18cents. 5% of DI was retained for working capital purposed and unforeseen circumstances.

Outlook

The management received notification of non-renewal of 24,929sqm of space on a lease expiring in 2Q20 at Wuhan Meiluote. This represents 50% of Wuhan Meiluote’s NLA of 48,695sqm. Occupancy is expected to fall from 97.7% to 46.7%. This asset contributes 1.6% to gross rental income (GRI) and will not affect DPU materially. Muted leasing demand is expected in the near term.

15.7% of leases by GRI is up for renewal in FY20. One of the leases expiring is for space at Hengde Logistics which is leased out to a state-owned tobacco company at below-market rentals. With the country in a state of flux, brought on by the Covid-19 outbreak, management is guiding for flattish rental reversions on leases expiring in FY20.

Key risk to our valuation remains the weakening of the RMB. The manager has revised its hedging strategy from a put spread to a plain vanilla call option. The previous hedging strategy employed would only protect ECW if FX fluctuated within a collar - exchange movements outside of the collar would mean that ECW would have to take the prevailing market rate. The amended strategy effectively locks in a worst-case exchange rate.

Maintain BUY with lower TP of S$0.83 (prev. S$0.84).

We maintain our BUY call with a marginally lower TP of S$0.83. This translates to a FY20e/FY21e DPU yield of 8.9%/9.3%.

The Positive

+ High income visibility due to portfolio occupancy of 99% (69%/72% of FY19e/FY20e revenue underpinned by master leases) and WALE by GRI of 4.6 years. 69% of revenue is secured by master leases to the Sponsor, Hengde Logistics, the specialised logistic asset customised and leased to a state-owned tobacco company, contributes c.15% to NPI. All assets are at 100% occupancy, except Wuhan Meiluote (85.1%), bringing portfolio occupancy to 99%.

The Negatives

- Accretion from the acquisition of Fuzhou E-commerce was wiped out by the FX movement and timing lag between drawdown of loan and acquisition. The acquisition financing for Fuzhou E-commerce (completed on 8 August 2019) was done in conjunction with the refinancing of the IPO loans (28 June and 8 August). The lower DPU was 60-70% due to the unfavourable FX movement and 30-40% due to the timing lag on the acquisition.

- Occupancy at Wuhan Meiluote slipped 0.7ppts QoQ. This comes after a -13.8pps fall in occupancy in 2Q19 due to non-renewals. This asset contributes c.S$0.7mn (1.7%) towards NPI and consists of a warehouse, auxiliary office building and a dormitory. c.6,000 sqm of warehouse space was vacated in 2Q19. Throughout the quarter, the asset was rented out on a short-term lease.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.

Outlook

Two leases with below-market rents will be up in 2020 and 2021 – one lease at the Hengde facility and the second lease to one of the anchor tenants at Wuhan Meiluote which is c.25% below market rent. Under market rents represent positive reversionary potential for the REIT.

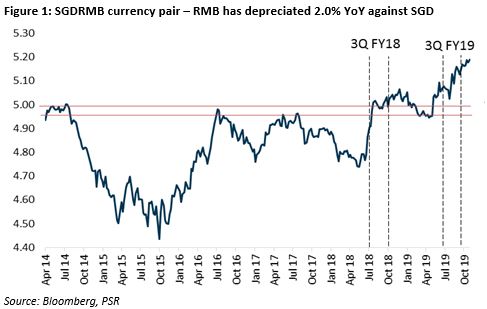

A key risk to our valuation remains the weakening of the RMB. Figure 1 shows the prices that the SGDRMB pair has been trading at, with emphasis on the 3Q18 and 2Q19. The area between the red lines indicates the put spread hedge for the quarter ended September 2019.

ECW hedges 75% of distributable income on a 6-month rolling hedge using put spreads. The hedging strategy employed means that the REIT will accept the FX fluctuations within a collar, and remain protected when the SGDRMB pair moves strongly against (as well as in favour of) them. The cost of implementing the put spread strategy is 50% the cost of the forward hedge strategy, however, it also takes away the upside potential when the currency moves in favour of them. The management is re-evaluating their FX hedging strategy.

Maintain Buy with lower TP of S$0.84 (prev. S$0.87).

We maintain our BUY call with a lower TP of S$0.84. We lowered our revenue forecasts to reflect the weaker RMB which has fallen 2% against SGD YoY. FY19e/FY20e DPU has been lowered from 6.38/6.83 cents to 5.98/6.76 cents. This translates to a FY19e/FY20e DPU yield of 8.1%/9.0% (prev. 8.7%/9.3%).

The Positives

+ WALE by GRI extended from 1.8 to 4.7 years due to extension of master leases. 99.3% of shareholders voted in favour of accepting the master leases on Chongxian Port, Beigang Stage 1 and Fuheng warehouse at the EGM held on 22 April 2019.

+ Proposed yield-accretive acquisition of ROFR asset with 5+5 year master leases. On a pro-forma basis, the 6.4% acquisition yield on Fuzhou e-commerce will lift NPI and DPU by 16.4% and 1.6% respectively. However, the acquisition will push gearing from 31.3% to 41.1%, which is slightly above the 40% gearing targeted by management. The asset is located beside ECW’s e-commerce asset, Fu Heng warehouse, and will be leased out to 2 master lessees on a 5+5 year term, with built-in rental escalation of 2.25% p.a. Acquisition is expected to be completed in 3Q19. Assuming full funding by debt, we expect FY19e/FY20e DPU to increase by 0.6%./6.17%.

The Negatives

- 100% of debt maturing in July 2019; refinanced debt maturity profile will be lumpy. The Management shared that they are in the final stages of concluding the refinancing of all loans. It is likely a maturity of 3 years. Refinancing this batch of loans will once again lead to a lumpy debt maturity profile.

Outlook

Extended WALE of 4.7 years and committed portfolio occupancy of 99.97% provides much income visibility. This is important in the context of the current global geopolitical tensions and economic uncertainty. Key risk is the depreciation of the RMB, which is partially mitigated by the rolling 6-month hedging strategy implemented on 75% of the distributable income.

Maintain Buy with higher TP of S$0.87 (prev. S$0.85)

We raise our target price to S$0.87 to incorporate the proposed yield-accretive acquisition of the Fuzhou E-Commerce asset. EC World trades at an attractive yield of 8% and a P/NAV of 0.93x.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.

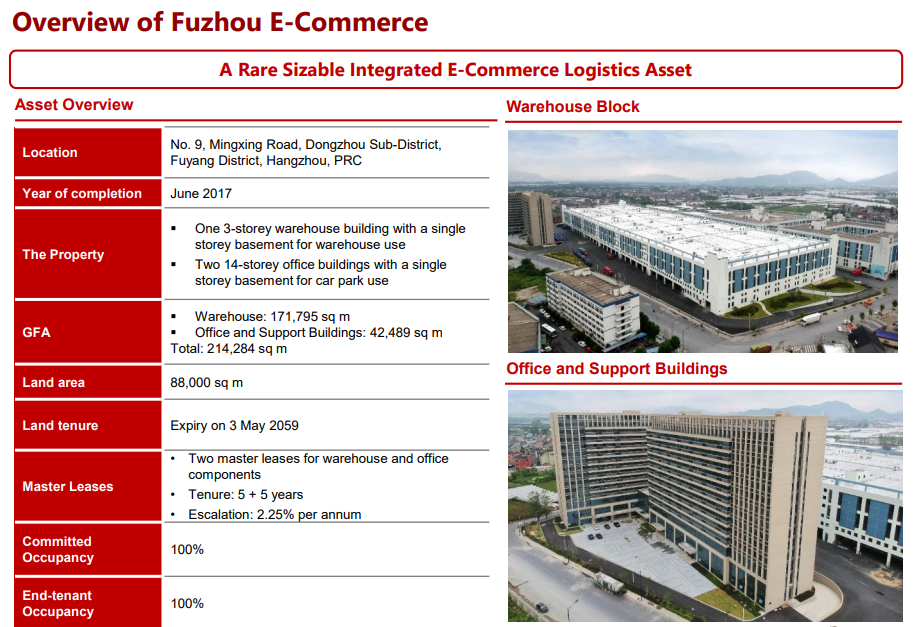

Details of proposed acquisition of Fuzhou E-Commerce

Figure 1: Details of asset

Source: Company

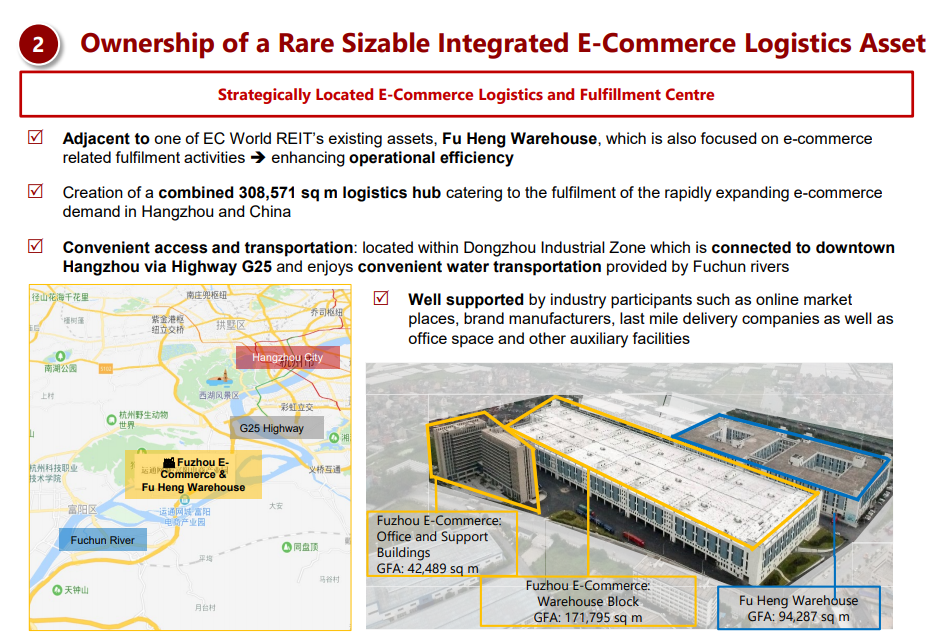

Figure 2: Together with Fu Heng warehouse, the adjacent sites form the largest e-commerce fulfilment warehouse in Hangzhou.

Source: Company

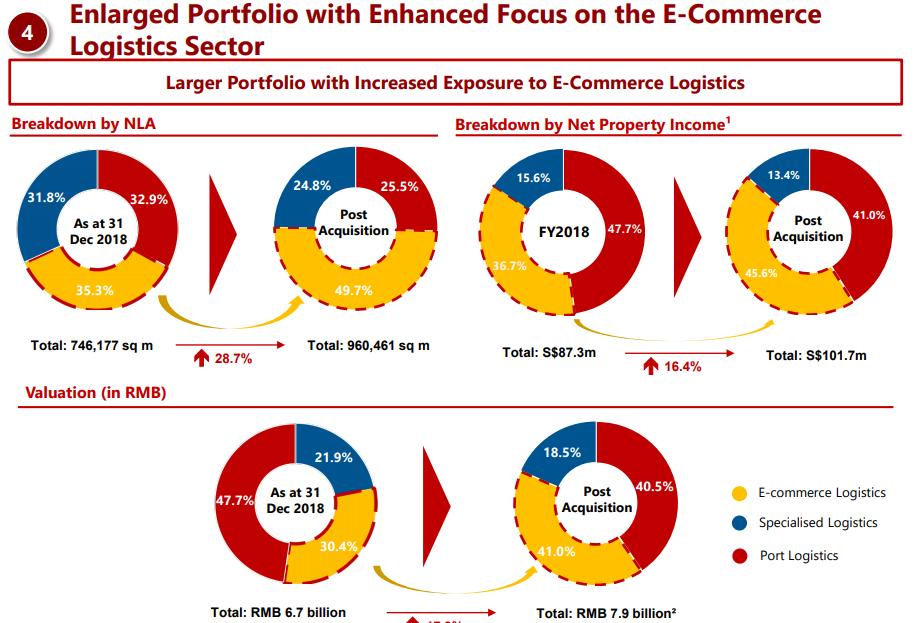

Figure 3: Acquisition increases proportion of revenue sourced from e-commerce sector

Source: Company

The Positives

+ Wuhan asset performing well after acquisition. Occupancy has ramped up from c.60% to c.86% since acquisition in April 2018, owing to the efforts of the Manager.

The Negatives

- Slow ramp-up of occupancy at Beigang. Occupancy for this asset has increased from 55.3% to 84% over the last 3.6 years. As this asset is currently under master lease with the sponsor, there is income support provided by the master lease gives the Manager a finite runway to work on boosting vibrancy of the property.

Outlook

All ECW’s master-leased assets - Chongxian Port, Beigang Stage 2 and Fuheng warehouse - are up for renewal in 4Q20. The rents from these three properties represent 70% of EC World’s revenue. If the terms are accepted by shareholders, portfolio WALE will increase from 2.0 to 4.8 years, providing stable earnings visibility. The master leases will now have built-in annual rental escalation of 1-2% (vs 1-3% rental growth rates for warehouses in Hangzhou), and will be renewed at existing prices. We also note that that Fuheng’s rents are currently already c.50% above market (c.RMB3.91psf vs c.RMB2.60psf).

100% of debt will be expiring in July 2019 comprising 50:50 onshore and offshore debt, and 89% of revolving credit facilities have been drawn down.

Maintain Buy with higher TP of S$0.85 (prev. S$0.82)

We raise our rental assumptions due to early lease renewals this quarter with positive reversions. We raise our target price to S$0.85, which translates to a FY19e yield of 20.2% and a P/NAV of 0.84x.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.

Company Background

EC World REIT (ECW) was listed on the SGX Mainboard on 28 July 2016 at S$0.81. Its initial portfolio was six assets in Hangzhou relating to e-commerce, specialized logistics and port logistics. Their seventh asset, an e-commerce logistics warehouse located in Wuhan, was acquired in February 2018. Portfolio net lettable area is 747,173sqm, valued at S$1.38bn, as at end-June 2018. EC World’s pipeline of assets includes one e-commerce asset from the sponsor and 13 logistics real estate assets worth S$400mn from supply chain management company YCH Group. ECW’s sponsor Forchn Group is a Shanghai-based conglomerate based out of Shanghai. We believe some of the assets in ECW portfolio require income support as the underlying rental income is lower than master lease rent.

Investment Thesis

Attractive dividend yield from captive assets. ECW is currently paying a dividend yield of 9%. The weighted average lease expiry (WALE) is 2.5 years with annual step-up of an estimated 3% p.a. There will be a major re-leasing in 2020 where 86% of the portfolio lease by revenue will expire. We expect a 3% rental reversion for these expiring leases. Whilst WALE is short we believe these are captive assets that will be renewed. Port facilities have an 80% market share of steel imports into Hangzhou. Port volumes are growing at 14% in 2018. The specialized tobacco warehouse holds RMB10bn worth of inventory that needs to be aged over two years. The e-commerce warehouses are supported by China’s burgeoning online commerce.

Large inorganic growth opportunity. Current gearing of 28.6% affords a debt headroom of S$200mn (assuming 40% gearing), we expect ECW to have the immediate capacity make a 6% DPU accretive acquisition. ECW has a right of first refusal (ROFR) pipeline of 14 assets not confined to China but including SE Asia. This should enlarge the size of ECW portfolio by almost 70%.

Landlord to e-commerce proxies. E-Commerce is growing at a torrid pace of 30% in China. Supporting such growth will require large investments in logistics, warehouses and transportation. Despite the growth of warehouses in China, the penetration on a per sqm basis is only 0.9, compared to U.S. and Japan of 5.4 and 4.4 respectively. ECW’s sponsor owns Ruyicang, a fulfilment platform which provides the warehouse and logistics support services for customers such as Alibaba and JD.com. Key and major tenants include prominent names in e-commerce such as Ruyicang and JD.com, who occupy the Fu Heng and Wuhan warehouses respectively.

We initiate coverage on ECW with a BUY and TP of S$0.82. Our valuation is based on dividend discount model (DDM) using an 8.5% cost of equity. The stock is also trading at 25% discount to book and a 9% yield. We expect DPU growth for ECW will come from acquisitions that will widen their footprint not only in China but also SE Asia, another fast-growing e-commerce market.