The Positives

+ Market shares maintained. Del Monte maintained market share in most product categories. In the US, market share in fruit cup snacks and canned fruits and vegetables was retained at 22-30%. Dominance in the Philippines was unchanged – packaged pineapple (95.7%), tomato sauce (84.6%), canned mixed fruit (74.9%) and RTD juice ex-foil pouches (45.5%).

The Negatives

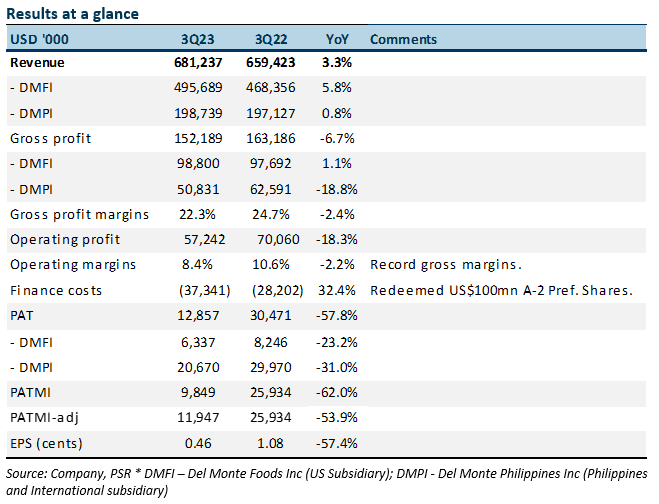

- Double whammy in Asia. 3Q23 revenue at DMPI was flat YoY. The two factors driving the weakness were; 1) 12% decline in the Philippine peso: In constant currency, revenue rose 13% YoY to PHP11.3bn, but a 12% decline in peso drove down revenue growth; 2) Weak festive sales: Demand for canned tropical fruit in the Philippines and fresh pineapple sales to China were below expectations. The volume bump during the holiday season did not occur. Phillipines suffered from weak consumer demand for discretionary items. The lockdown affected sales.

- Weak gross margins in the US. 3Q23 gross margins for US operations collapsed by 8 percentage points to 20.4%. The decline was a surprise despite price increases. The reason for the weakness was the higher cost inventory of raw materials being sold. For instance, in 1H23 sales, 70-80% of the inventory was procured in FY22. Other costs remain elevated such as energy and fuel.

- Elevated inventory. Del Monte exited the festive period with a record US$1.14bn of inventory as of Jan23. The rise in value was in part due to inflationary pressure but inventory days have jumped to 204 days, compared to 149 days a year ago. We worry there is a risk of provisions with the huge jump in inventory.

The Positives

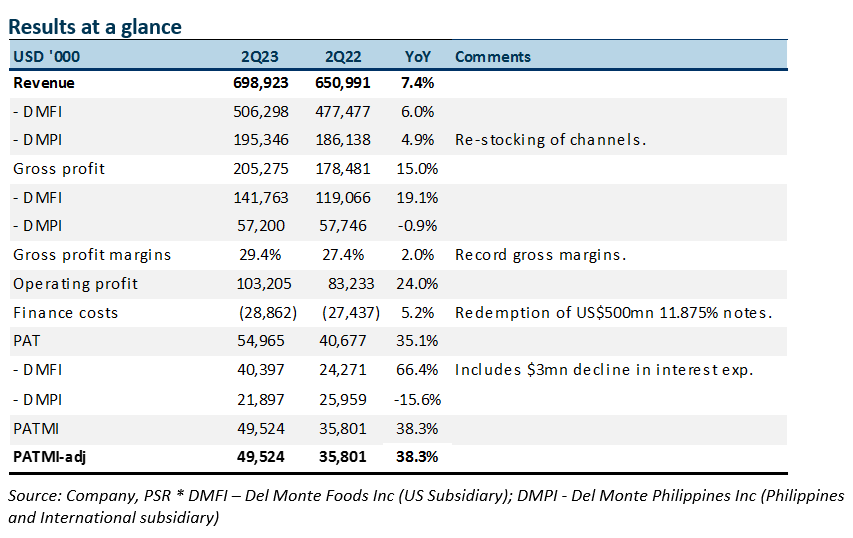

+ Record gross margins. Gross margin climbed to record high 29.4%, a 2% point rise YoY. Margin gains were from US operations from multiple price increases over the past 18 months. These have supported margins despite raw material and logistics cost pressure. There was also operating leverage from a slower 6% rise in general and administration expenses.

+ Sharp rebound in Philippines. Sales in the Philippines and International (DMPI) recovered strongly in 2Q23, surging 22% YoY in peso terms to PHP11.3bn. However, revenue in USD terms only improved by 5% due to the weakness in the Philippine peso. Growth stemmed from the transition to new distributors in the last quarter and a rebound in food service (+21% YoY) and convenience stores (+48% YoY) as the lockdowns ease.

The Negative

- Rise in net debt by US$505mn to US$2bn. Net debt to EBITDA climbed from 4.3x to 5.6x over the past six months. Whilst total net debt has risen by US505mn YoY to US$2bn in May 2022. Driving up debt levels was: (i) US$366mn increase to US$1250mn; (ii) US$70mn for the purchase of Kitchen Basics. The 40% YoY jump in inventory was due to higher cost of materials, which we believe was in preparation for a strong holiday season. We expect debt to remain elevated due to the redemption of a 6.5% US$100mn Preference Shares in Dec2022. Around 15-20% of total debt is on fixed rates.

The Positives

+ Healthy gross margins. Gross margin was maintained at 28.9%, higher than our modelled 25.8% and 4Q22’s 25.9%. A combination of higher prices in June 2022 and packaging changes helped support margins. In early September, the US operations underwent their third round of phased price increases since May 2021.

+ Joint venture returning to profitability. The joint venture in India turned around from a US$0.6mn loss to a US$0.7mn profit. Earnings benefited from 19% YoY growth in revenue together with margin improvement. India has discontinued fresh business and a greater focus on B2B sales. There have also been management changes.

The Negatives

- One-off refinancing cost. In May 2022, Del Monte refinanced the US$500mn 11.875% p.a. 2025 high yield senior secured note with a US$600mn 7-year Term Loan facility. The interest on the loan is SOFR plus 4.25% or 6.45% currently. The early redemption incurred a US$71.9mn one-off cost (or US$50.2mn post-tax and minority interest). Current savings on the refinancing are around US$27mn p.a.

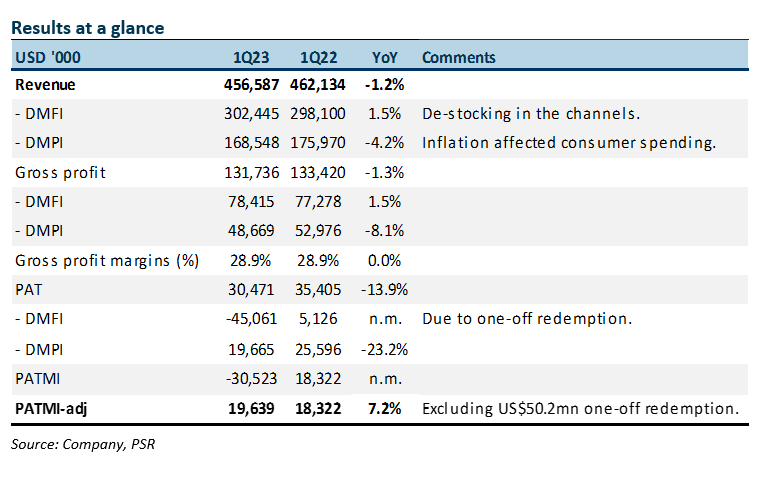

- Sluggish revenue. Revenue growth decelerated to a negative 1.2% YoY in 1Q23e to US$456mn. It is a major deceleration from the 14% YoY growth in 4Q22. The US growth rate slowed to 1.5% (4Q22: +25% YoY). We believe there was a general de-stocking exercise by US retailers in the quarter (Figure 3). The Philippines faced several hiccups during the quarter. There was a change in the distributor; de-loading of inventory in May and June; consumers shifting away from discretionary; and some market share loss in ready-to-drink juice to cheaper PET bottled juices. Another headwind was the 8% decline in the Philippine peso.

Outlook

We expect a healthy recovery in the coming quarters.

Results at a glance

Source: Company, PSR

The Positives

+ Del Monte Foods Inc (DMFI) rebounds in margins and profitability. DMFI revenue jumped 25% YoY to US$411mn. Revenue was supported by a surge in packaged vegetable sales as DMFI expands into new channels, including convenience stores, natural food, club stores and food service. Households are looking for value and quality home meals, replacing their spending on restaurants as inflation picks up nationwide.

+ Refinancing expensive preferential shares and high yield debt. In April 22, US$200mn 6.625% preference shares were refinanced by Del Monte with senior fixed-rate debt (3.75%) and floating-rate loan (3.8%). The estimated savings in dividends is around US$6mn.

In May 22, DMFI raised a US$600mn 7-year term loan at a floating 4.75%. The funds were to refinance US$500mn 11.875% Senior Secured Notes. The early redemption of the high yield notes cost a one-off US$70mn*, to be incurred in FY23. Annual cash savings is US$20mn-30mn.

*US$45mn cash commitment fee, US$24mn non-cash write-off of deferred financing cost and US$1mn commitment fee

The Negatives

- Weakness in the Philippines. Revenue in the Philippines declined 6% YoY with earnings dropping a larger 31%. Packaged or mixed fruit suffered the largest drop, a 31% YoY fall to US$22mn in the Asia Pacific. Consumers are faced with surging inflation in the Philippines. There is a shift in consumer priorities to essential items, away from special occasion or less-essential food such as canned mixed fruit or packaged fruit.

- Elevated capex. Free cash flow generated in FY22 was US$66mn, a decline from prior years' US$163mn. A large drain in operating cash flow was the additional US$135mn in inventory to stock up on raw materials as a hedge from rising prices. Capex also rose by US$39mn to US$202mn. The higher capex is to expand the planted area for pineapples, increase manufacturing capacity and new packaging capabilities (eg Joyba Bubble Tea multipacks).

Outlook

We see multiple drivers for earnings growth in DMFI, namely new products, more distribution channels, higher prices, cost optimization and food inflation driving more home dining. DMFI has built a broad pipeline of products to suit consumer preferences for value and wellness (Figure 1). The recovery in the Philippines will be slower as inflation shifts consumption patterns to more staples. Recovery will come from convenience and food services channels as foot traffic returns with lockdowns being eased

The Positives

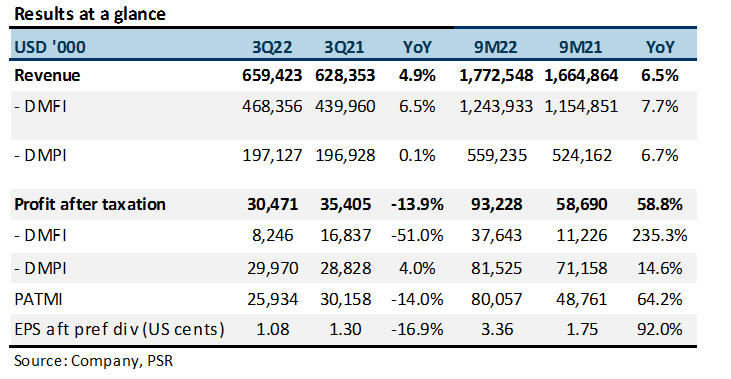

+ US subsidiary Del Monte Foods Inc (DMFI) sales in 3Q22 increased 6.5% YoY. In the Americas, sales increased by 6.3% YoY to US$471.3mn due to higher sales from branded retail (+2.5% YoY) primarily core canned vegetable and fruit which more than offset planned reduction in private label sales. With the re-opening of schools and restaurants, sales from the food service channel grew significantly by 48% YoY.

+ Del Monte Philippines Inc (DMPI) in 3Q22 supported by both local and international sales. Asia Pacific sales increased 4.1% YoY to US$181.5mn. S&W branded business increased 11.2% YoY, driven by higher sales of fresh pineapples due to increase in volume in North Asia and Singapore, expanded distribution in China as well as price increases to counter inflation. In peso terms, sales in the Philippines rose 4.2%. Some growth was seen across almost all categories despite continued lockdown and lower foot traffic due to the pandemic, proving the strength of Del Monte’s market leader position in the Philippines.

The Negative

- Inflationary pressures. US subsidiary DMFI saw profit after tax falling 51% YoY despite higher sales, due to higher manufacturing cost driven by commodity headwinds, weather-related events and freight headwinds, particularly ocean freight on co-pack products, which more than offset higher sales. Gross margins declined 3.5 ppts to 20.9%. On 9M basis, gross margin was up 1.4 ppts to 23.6%.

Other updates

Improving cost of debt in the long term. DMFI issued US$500mn of 11.875% Senior Secured Notes on 15 May 2020. They will mature on 15 May 2025 and are redeemable at the option of DMFI beginning in May 2022. Interest paid under this loan in FY21 was US$29.7mn, accounting for 27% of total interest expense. Due to the one-time estimated US$45m cost of early redemption, we will only see the effect of net savings on this loan in FY24 (Figure 1).

DMPL announced that they will be redeeming all the outstanding US$200mn Series A-1 Preference Shares, which we expect the company to refinance through loans. This would increase interest expense, but net savings are expected as the new loans would be taken at lower rates. DMPL recently issued US$90mn 3-year unrated Senior Notes with fixed coupon rate of 3.75% payable semi-annually. This compares to fixed rates of 6.625% and 6.5% per annum for Series A-1 and A-2 preference shares respectively.

In October 2021, S&P Global Ratings raised the credit rating on DMFI to ‘B’ from ‘B-‘, and issue-level rating on its debt to ‘B’ from ‘B-‘. In January 2022, Moody’s upgraded DMFI’s Corporate Family Rating to B2 from B3. We expect DMFI to issue debt at a lower cost.

The Positives

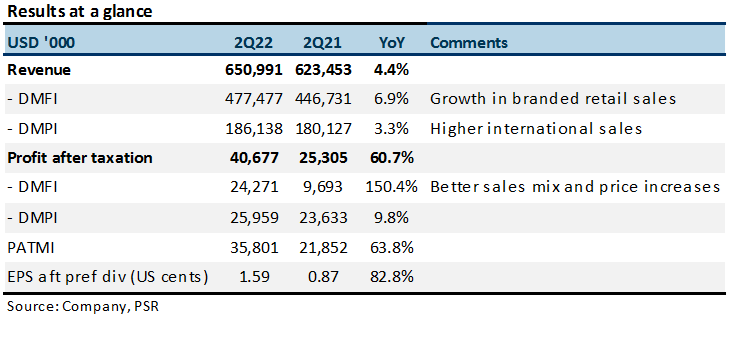

+ US subsidiary Del Monte Foods Inc (DMFI) sales in 2Q22 increased 7% YoY. Branded retail sales grew 11% YoY, with strong momentum from core vegetable business and shipments in preparation for Thanksgiving holiday promotional activity. DMFI’s highest margin canned vegetable continues to hold the largest market share of 20.2% in its segment. DMFI continued to expand distribution of new products launched, which contributed to 5.3% of DMFI’s total sales in 2Q22. Profitability increased with a better sales mix and price increases. Compared to April 2021, prices have increased about 10%. More consumers are turning to trusted brands like Del Monte for meal preparation options of better quality.

+ Del Monte Philippines Inc (DMPI) in 2Q22 supported by international sales. DMPI’s sales in the international market increased 18% YoY to US$69.7mn in 2Q22. This was driven by strong sales of packaged fruit and beverages in the USA and Europe, and S&W packaged pineapple and mixed fruit in North Asia. Sales of S&W packaged pineapple products in 2Q22 rose 58.4% YoY, but that of fresh pineapples declined by 17.2% YoY, due to lower supply attributed to timing of the harvest. This is expected for 2Q22 only.

The Negatives

- Lower sales from Philippines. In US dollar terms, 2Q22 sales in the Philippines decreased 5.8% YoY to US$100.2mn due to a high base in 2Q21. The packaged fruit and new products saw growth, which was offset by a reduction in culinary and beverage categories.

- FieldFresh joint venture in India still suffering. DMPL’s share in the JV in India suffered a loss of US$0.5mn in 2Q22, compared with a US$0.2mn loss in 2Q21. B2B business and e-commerce sales grew, but were offset by the decline in fresh sales.

Other updates

Improving cost of debt. DMPL has successfully priced an aggregate principal amount of US$90mn 3-year unrated Senior Notes with a fixed coupon rate of 3.75%, payable semi-annually. The Notes were priced with a yield of 4% at a reoffer price of 99.3%. Approval in-principle has been received for the listing of the Notes on the SGX-ST. This would be for the partial refinancing of the preference shares. A total of US$300mn of preference shares were listed in 2017 at fixed rate of 6.625% and 6.5% per annum for Series A-1 and A-2 respectively.

DMFI issued US$500mn of 11.875% Senior Secured Notes on 15 May 2020. They will mature on 15 May 2025 and are redeemable at option of DMFI beginning in May 2022. Interest paid under this loan in FY21 was US$29.7mn, accounting for 27% of total interest expense.

In October 2021, S&P Global Ratings raised the credit rating on DMFI to ‘B’ from ‘B-‘, and issue-level rating on its debt to ‘B’ from ‘B-‘. We expect DMFI to issue debt at a lower cost.

Maintain BUY with a higher TP of S$0.62, from S$0.60.

We have a higher TP of S$0.62, up from S$0.60. We raise FY22e PATMI slightly by 2%, to US$88.2mn. We raise sales forecasts for the Americas by 5% to US$1.62bn, but lower sales forecasts for Asia Pacific by 4% to US$690mn, in line with lower revenue in 2Q22 from the Philippines, due to a high base from impact of the pandemic in 2Q21.

Our TP remains pegged to 13x FY22e P/E, as we apply a 20% discount to the industry valuation which remained unchanged, due to comparatively higher leverage.

Company Background

Dual-listed on the Singapore Exchange and Philippine Stock Exchange, Del Monte Pacific Limited (DMPL) produces and markets packaged vegetable and fruit, beverage and culinary products (refer to Appendix 1).

In the US, DMFI is ranked first in canned vegetables and second in canned fruits, as consumers continue to turn to trusted brand names for meal preparation and healthy snacks. DMPI’s dominant market shares in the Philippines of as high as 90% in key categories have continued to rise. Retailers are carrying fewer brands and focused on the largest.

Investment Merits

Significant undervaluation of DMPL. DMPL is trading at FY22e P/E of 8.2x, far below the industry average of 16x. The company had been underperforming since the acquisition of US subsidiary DMFI in 2014. Over the years, the new management has turned DMFI around successfully, steering towards innovation to address shifting consumer habits and expanding distribution into key growth areas. We believe another reason for the undervaluation is the debt level of US$1.3bn, resulting in high interest expenses of US$111mn, which we expect to wind down gradually. We apply a 20% discount to the industry average, due to its gearing level which is higher than peers and smaller market capitalization.

REVENUE

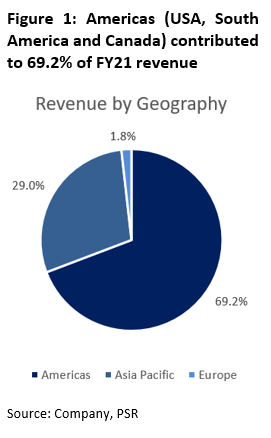

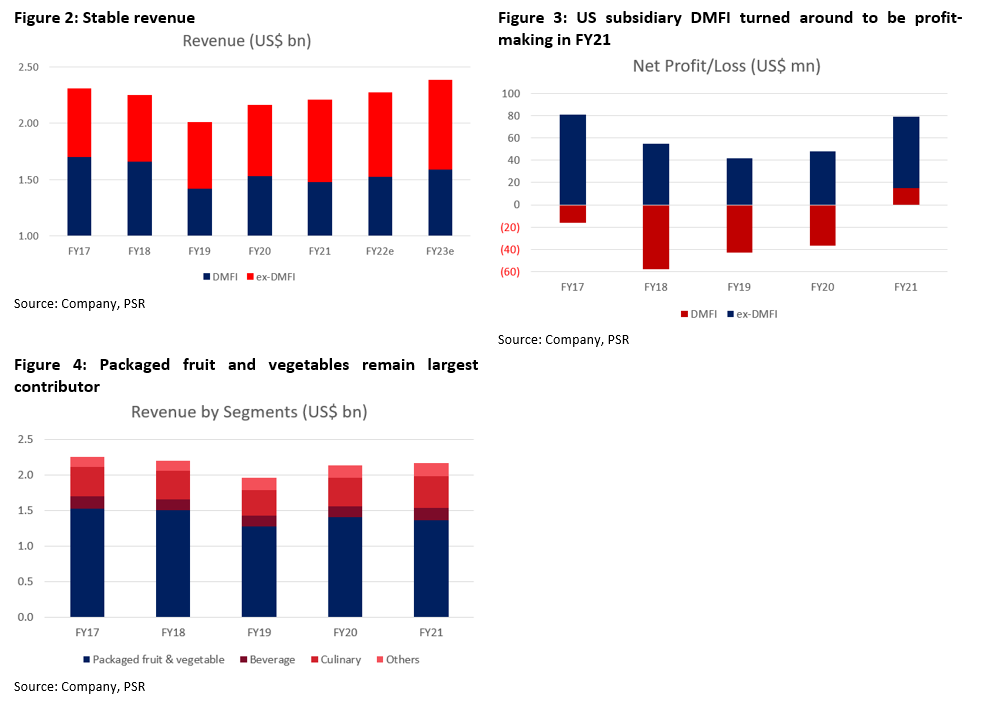

Del Monte Foods Inc (DMFI). DMFI is Del Monte’s US subsidiary, under which they have both branded and private retail sales. This segment was acquired in 2014 and is mainly present in the US. It has been accounting for the bulk of DMPL’s revenue, and made up 70% of FY21 revenue, driven by branded retail sales (Figure 2). The majority of sales under the Americas segment are sold under the Del Monte brand but also include products under the Contadina, S&W, College Inn and other brands. This segment also includes sales of private label food products. Sales are distributed in all channels serving retail markets, and to certain export markets, the food services industry and other food processors.

Del Monte Philippines Inc (DMPI). This is DMPL’s second-largest and most profitable subsidiary. In the Philippines, sales are derived from general trade, modern trade and food services. General trade (GT) includes retailing to a network of retailers, wholesalers, and dealers. Modern Trade (MT) includes the distribution of goods to supermarket chains. Food services include selling through restaurants. The GT and MT combined grew by 13.4% in FY21, delivering record sales of US$705.8mn.

DMPI products are also exported to Europe and S&W markets. This includes exports of fresh and packaged pineapples. Sales increased from higher sales of fresh pineapples in China, Japan and South Korea, and packaged pineapple, mixed fruit and juice drinks.

EXPENSES

Costs primarily include metal packaging, packaging and raw material costs. DMPL has introduced various cost cutting measures over the years.

DMPL has high levels of borrowing, with net debt of US$1.3bn in FY21. This also comes with interest burden of US$111mn. The company has progressively reduced net debt over the past five financial years. It may take another three years before reduction of interest expenses to below US$100mn, as we expect repayment of some short-term borrowings.

In 2017, DMPL completed the offering and listing of 20mn Series A-1 and 10mn Series A-2 preference shares, both at an offer price of US$10 per share in the Philippines, at a fixed rate of 6.625% and 6.5% per annum. We have factored in assumptions that Series A-1 and A-2 preference shares would be redeemed by FY22 and FY23 respectively.

MARGINS

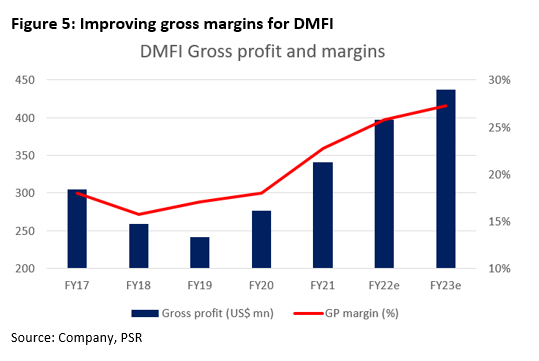

DMFI generated a gross profit margin of 22.6% in FY21, up from 17.6% in FY20. This was driven by higher sales from branded retail, combined with lower promotional trade spend and cost improvement including lower cash discounts. There were also lower packing costs from the asset light strategy, with production outsourced. Plant closures in FY20 generated savings, in line with DMPL’s asset-light strategy.

We expect DMFI gross margins to climb further in FY22e and FY23e. Levers to raise margins to include reducing overhead and trade spending, and capacity expansion in packaging. To alleviate recent cost pressures, DMFI raised product prices in May and September this year. We believe the strength of the brand will keep volumes resilient despite the higher prices.

DMPL generated an average gross profit margin of 21.8% over the past five financial years, and EBITDA margin of 13.3%, which we expect to remain stable.

BALANCE SHEET

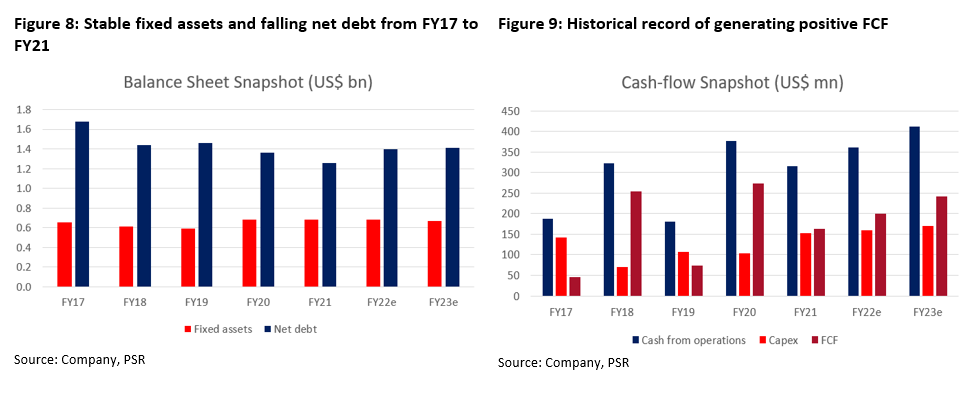

Assets. Fixed assets have remained largely stable over the past five financial years from FY17 to FY21, at US$680mn. DMPL has adopted IFRS 16 since 1 May 2019.

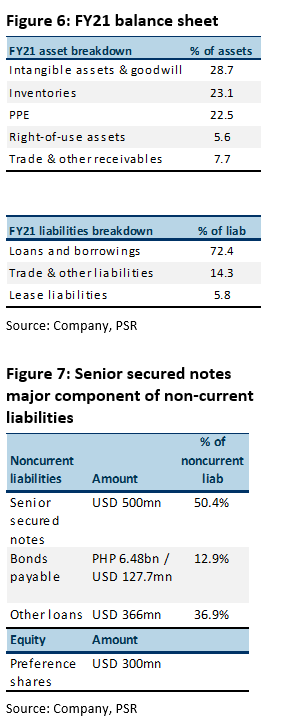

Intangible assets and goodwill is the biggest component of DMPL’s assets, consisting of trademarks, including the right to use the “Del Monte” trademarks in connection with the production, manufacturing, sales and distribution of food products, in various markets (Figure 6).

As of 30 April 2021, DMPL carries goodwill of US$203.4mn and indefinite life trademarks of US$408mn, with US$394mn relating to DMFI.

Liabilities. DMPL has been gradually reducing its net debt, to US$1.3bn in FY21 (Figure 8), and gearing was lowered from 2.4x to 2.0x equity.

DMFI issued US$500mn of 11.875% Senior Secured Notes on 15 May 2020. They will mature on 15 May 2025 and are redeemable at the option of DMFI beginning in May 2022. The Notes make up 50.4% of total non-current liabilities (Figure 7). Interest paid under this loan in FY21 was US$29.7mn, accounting for 27% of total interest expense.

Recently, S&P Global Ratings raised credit rating on DMFI to ‘B’ from ‘B-‘, and issue-level rating on its debt to ‘B’ from ‘B-‘. This is on the back of continued deleveraging, with 11% revenue growth and high profitability in 1QFY22, with EBIT margin of 9.3%. This resulted in improvement in leverage from 10x to about 3.5x for 12 months ending 1 August 2021.

Cash flow. DMPL has been generating positive operating and free cash flows from FY17 to FY21. Operating cash flow was lower in FY21 due to higher working capital. Capex has remained relatively stable at an average of US$115mn over the past five financial years (Figure 9).

DMPL’s dividend policy is to distribute a minimum of 33% of net profit. In FY21, DMPL paid 37% of PATMI in FY21, and 50% of PATMI in FY19. In FY20, although it was a loss-incurring financial year due to plant closures resulting in one-off expenses, DMPL declared a special dividend due to the one-off gain generated from the sale of a 13% stake in DMPI. Preferred dividends were also paid.

INVESTMENT MERITS

KEY RISKS

INDUSTRY

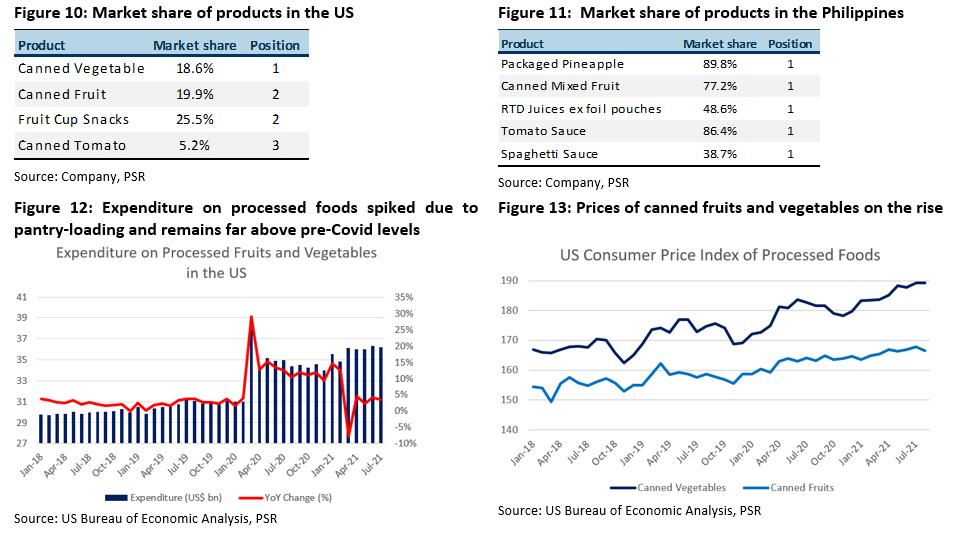

Del Monte Pacific ranks among the top players in the US (Figure 10) and has a dominant share in the Philippines (Figure 11).

Increasing interest in culinary home meal preparation has accelerated due to Covid-19. As a result, more consumers are looking for quick, convenient and healthy food options, and they are turning to strong brands, including Del Monte.

The personal consumption expenditure on processed fruits and vegetables in the US was recording steady growth until the Covid-19 pandemic hit in early 2020, and spiked in March 2020 (Figure 12). Consumers had to prepare their meals at home during the lockdowns, which led to pantry loading and higher demand for meal preparation products. This has also led to steady growth in the prices of processed foods (Figure 13). DMFI has also raised prices over the year.