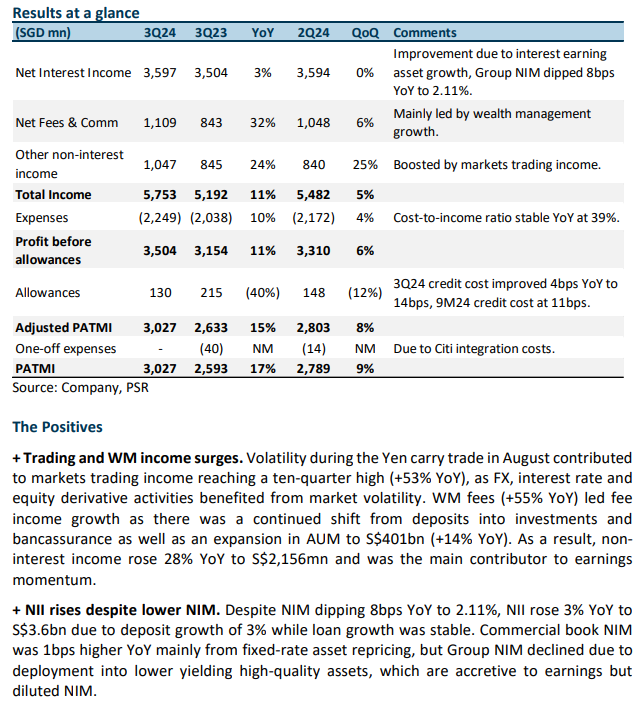

The Positives

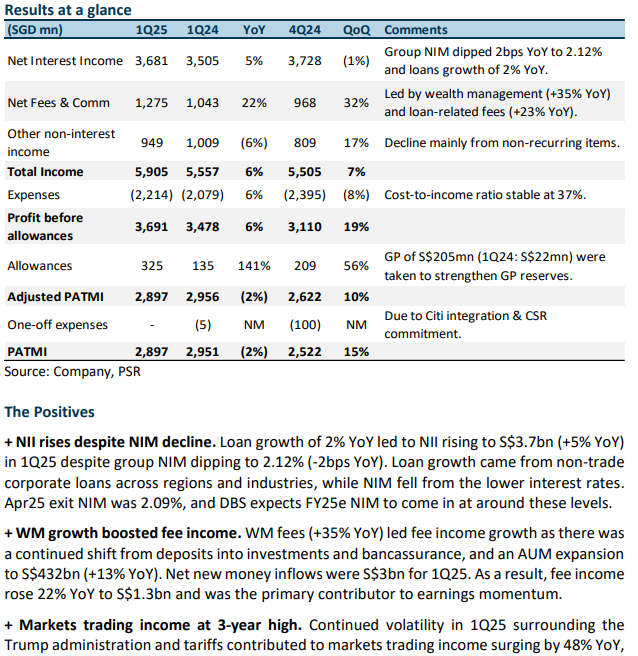

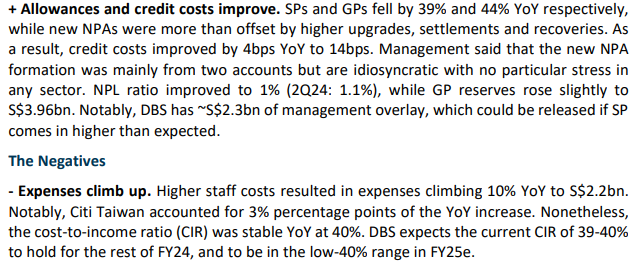

+ NII rises from loan and deposit growth. Despite NIM dipping 2bps YoY to 2.14%, NII rose 5% YoY to S$3.6bn due to loan and deposit growth of 3% and 6% respectively. Commercial book NIM was 2bps higher YoY mainly from fixed-rate asset repricing, but Group NIM dipped slightly due to deployment into lower yielding high-quality assets which are accretive to earnings but diluted NIM slightly. Management said that loan growth was broad-based but was seen more in Singapore and India, offset by Hong Kong loans shifting to mainland China.

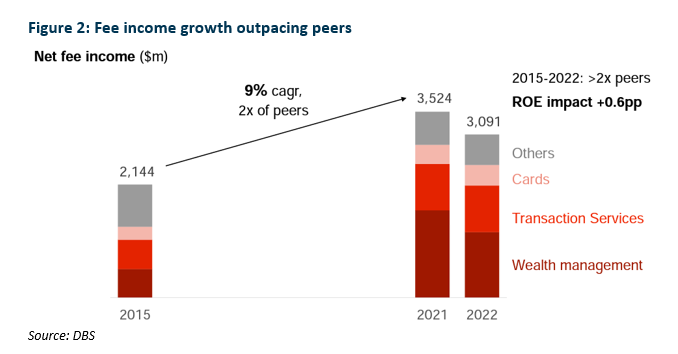

+ WM leads fee income growth. Wealth management fees (+37% YoY) led fee income growth as there was a continued shift from deposits into investments and bancassurance as well as an expansion in assets under management (AUM). As a result, fee income rose 27% YoY to S$1,048mn. Card fees rose 32% YoY from higher spending, while loan-related fees grew 40% YoY. The consolidation of Citi Taiwan benefitted both WM and card fees. 2Q24 AUM grew 24% YoY to S$396bn while interest earning assets rose 20% YoY to S$447bn.

+ Credit cost and SPs improve YoY. SPs dipped 15% YoY to S$97mn, while new NPAs formation was more than offset by higher upgrades, settlements and recoveries. As a result, credit costs improved by 2bps YoY to 8bps. DBS said that the NPA formation was

idiosyncratic, and it did not see particular stress in any sector. However, 2Q24 total allowances rose to S$148mn (2Q23: S$114mn) as the lower SP was more than offset by higher GP of S$51mn (2Q23: write-back of S$42mn). The NPL ratio was flat at 1.1% (1Q24:

1.1%), while GP reserves grew 5% YoY to S$3.98bn. DBS has ~S$2bn of management overlay, which could be released if SP comes in higher than expected

The Negatives

- Expenses climb up. Higher staff costs due to salary increments and higher bonus accruals, as well as headcount growth including the addition of staff from Citi Taiwan resulted in expenses climbing 12% YoY to S$2,172mn. Notably, Citi Taiwan accounted for 5% points of the YoY increase. Non-staff costs were also higher from higher revenue-related expenses. As a result, the cost-to-income ratio (CIR) rose 2% points YoY to 40%. Nonetheless, this is still within DBS’ guidance of around 40%.

- CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 6% points YoY to 50%, mainly due to the high-interest rate environment and a continued move towards fixed deposits (FDs). The declining CASA ratio could further increase funding cost and there could be an increased dependence on FDs, which usually comes at a higher interest rate. Nonetheless, total customer deposits grew 6% YoY to S$551bn as the growth in FDs more than offset the decline in CASA deposits.

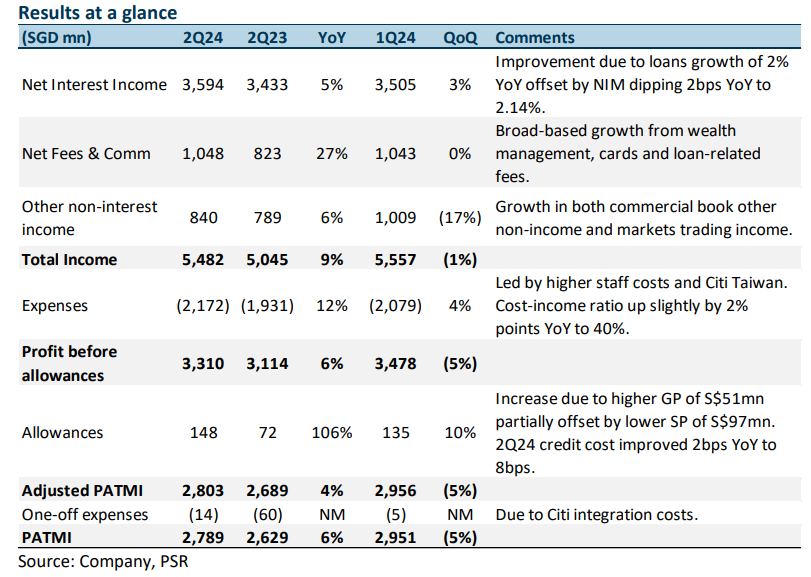

The Positives

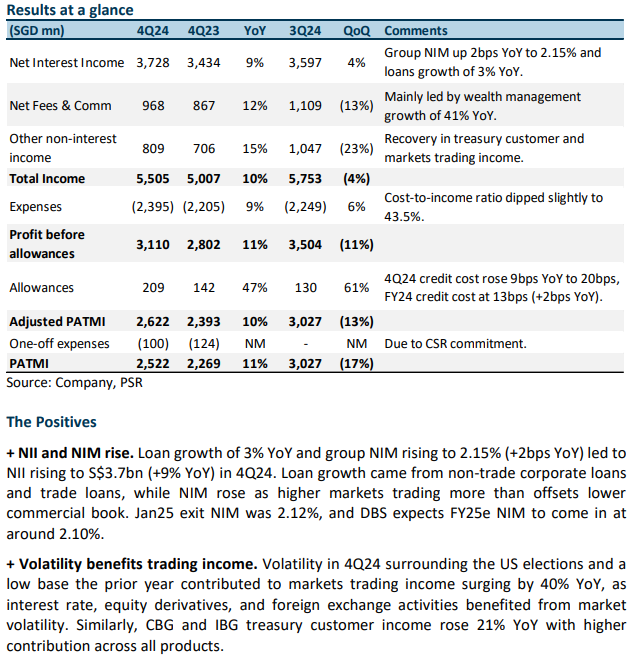

+ NII rises 7% YoY. NII rose 7% YoY to S$3.5bn due to a 2bps NIM increase to 2.14% (4Q23: 2.13%) as interest rates continue to remain high and loan growth grew modestly by 2% YoY. Loan growth came from higher non-trade corporate loans and the consolidation of Citi Taiwan. Management noted that loan growth was broad-based but was seen more in Singapore and India, which was offset by Hong Kong loans shifting to mainland China.

+ Fee income continues to recover. Fee income rose 23% YoY to a record level of S$1,043mn. The growth was led by wealth management (WM) fees surging 47% YoY from stronger market sentiment and an increase in assets under management (AUM). Card fees rose 33% YoY from higher spending, while loan-related fees grew 30% YoY. The consolidation of Citi Taiwan benefitted both WM and card fees. This was offset slightly by a decline in investment banking fees (-59% YoY) due to slower capital market activities while transaction services were flat YoY.

+ Other non-interest income rose 24% YoY. This growth was mainly due to higher treasury customer sales, partially offset by a decline in market trading income from higher funding costs. Notably, commercial book continues to account for the majority of other non-interest income at 62% (1Q23: 53%), while treasury markets account for 38% (1Q23: 47%).

The Negatives

- SPs and NPAs rise YoY. SPs rose 82% YoY to S$113mn, while new NPAs rose 45% YoY to S$317mn from broad-based increases across all sectors. As a result, credit costs rose from 4bps YoY to 10bps. DBS has mentioned that the NPA formation was idiosyncratic, and they do not see particular stress in any sector. Nonetheless, 1Q24 total allowances were lower by 16% YoY as the higher SP was more than offset by a lower GP of S$22mn (1Q23: S$99mn). The NPL ratio was flat at 1.1% (4Q22: 1.1%), while GP reserves grew 4% YoY to S$3.93bn. Notably, management mentioned ~S$2bn of management overlay, which could be released if SP comes in higher than expected.

- The decline in the CASA ratio continues. The Current Account Savings Accounts (CASA) ratio fell 6% points YoY to 51%, mainly due to the high-interest rate environment and a continued move towards fixed deposits (FDs). The declining CASA ratio could further increase funding cost and there could be an increased dependence on FDs, which usually comes at a higher interest rate. Nonetheless, total customer deposits grew 3% YoY to S$547bn as the decline in CASA deposits was offset by growth in FDs and a contribution of S$12bn from the Citi Taiwan consolidation.

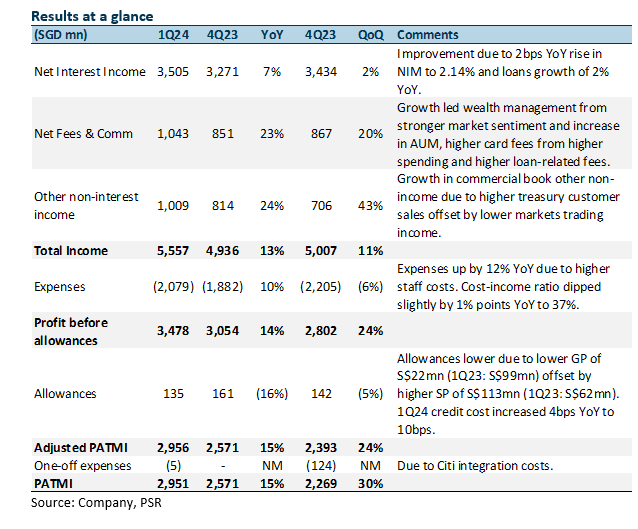

The Positives

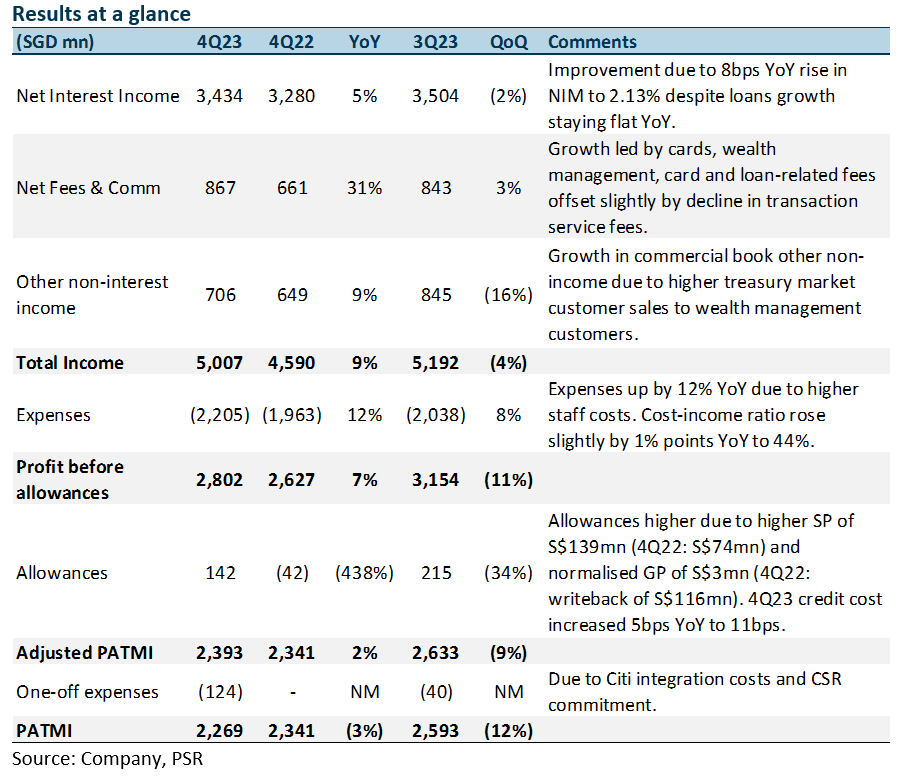

+ NIM and NII continue to increase YoY. NII rose 5% YoY to S$3.4bn due to an 8bps NIM increase to 2.13% (3Q23: 2.19%) as interest rates continue to remain high, despite loan growth remaining flat YoY. Loan growth was stable as higher trade and consumer loans were offset by lower non-trade corporate loans. Nonetheless, the Citi Taiwan consolidation contributed S$10bn to loans.

+ Fee income recovers strongly. Fee income rose 31% YoY to S$867mn. WM fees increased 41% YoY driven by strong net new money inflows as customers shifted deposits into bancassurance and investments, while card fees grew 27% YoY from higher spending and the integration of Citi Taiwan. Loan-related fees rose 80% YoY, while investment banking fees were up 26% YoY. These increases were moderated by a 4% YoY decline in transaction fees as trade finance slowed.

+ Other non-interest income rose 9% YoY. Other non-interest income growth was mainly due to higher treasury customer sales and gains from investment securities. Notably, commercial book accounts for a majority of other non-interest income was at 55%, while treasury markets accounts for 45%.

The Negatives

- Allowances rose 438% YoY. 4Q23 total allowances were higher 438% YoY due to normalised GP of S$3mn (4Q22: writeback of S$116mn) and higher SP of S$139mn (4Q22: S$74mn). As a result, 4Q23 credit costs rose to 11bps, with FY23 credit costs at 11bps. The NPL ratio was flat at 1.1% (4Q22: 1.1%), while GP reserves grew 4% YoY to S$3.90bn. Notably, management mentioned S$2.2bn of management overlay, which could be released if SP comes in higher than expected.

- CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 8% points YoY to 52.3%, mainly due to the high-interest rate environment and a continued move towards fixed deposits (FDs). Nonetheless, total customer deposits grew 2% YoY to S$535bn as the decline in CASA deposits was offset by growth in FDs and a contribution of S$12bn from the Citi Taiwan consolidation.

The Positives

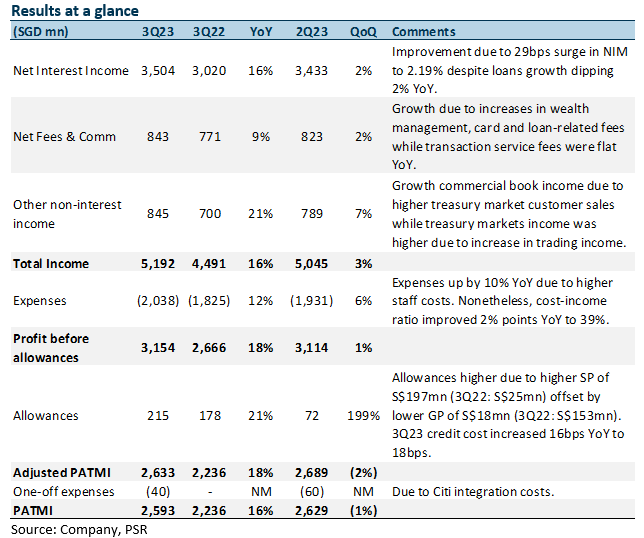

+ NIM and NII continue to increase YoY. NII rose 16% YoY to S$3.5bn due to a 29bps NIM increase to 2.19% (2Q23: 2.16%) as interest rates continue to remain high, despite loan growth dipping 2% YoY. Loan growth dipped due to a decline in customer and trade loans due to unattractive pricing while non-trade corporate loans were lower due to higher repayments. Nonetheless, the Citi Taiwan consolidation contributed S$10bn to loans.

+ Fee income continues to grow. Fee income rose 9% YoY to S$843mn. WM fees increased 22% YoY from higher bancassurance and investment product sales, while card fees grew 21% YoY from higher spending and the integration of Citi Taiwan. Loan-related fees rose 12% YoY, while transaction fees were flat YoY. These increases were moderated by a 16% YoY decline in investment banking fees due to slower capital market activities.

+ Other non-interest income rose 21% YoY. Other non-interest income rose 21% YoY mainly due to an increase in net trading income from higher trading gains and an increase in treasury customer sales to both wealth management and corporate customers. Notably, commercial book accounts for majority of other non-interest income was at 59%, while treasury markets accounts for 41%.

The Negatives

- Allowances rose 21% YoY. 3Q23 total allowances were higher 21% YoY due to higher SP of S$197mn (3Q22: S$25mn). Resultantly, 3Q23 credit costs rose to 18bps, with 9M23 credit costs at 11bps. The rise in SP was due to allowances being prudently taken for exposures linked to the recent money laundering case in Singapore. The NPL ratio rose slightly to 1.2% (3Q22: 1.1%), while GP reserves were stable YoY at S$3.91bn.

- CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 12.5% points YoY to 47.8%, mainly due to the high interest rate environment and a continued move towards fixed deposits (FDs). Resultantly, total customer deposits were flat YoY at S$531bn as the decline in CASA deposits were partially offset by growth in FDs.

The Positives

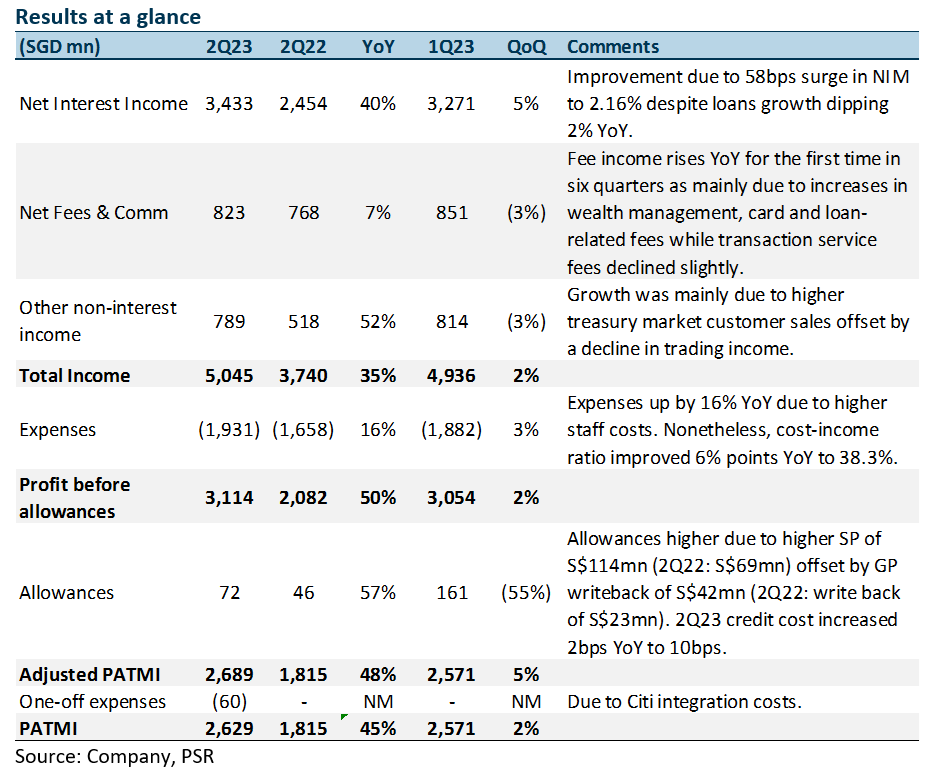

+ NIM and NII continue to increase. NII spiked 40% YoY to S$3.43bn due to a NIM surge of 58bps YoY to 2.16% (3Q22: +32bps, 4Q22: +15bps, 1Q23: +7bps, 2Q23: +4bps) despite loan growth dipping 2% YoY. Increases in non-trade corporate loans were offset by lower trade loans. Housing loans were stable, while wealth management loans declined modestly. Management spoke of an upside bias to NIM from its current levels and indicated that NIM will likely peak in 2H23.

+ Fee income rose 7% YoY, first in 6 quarters. Fee income increased 7% YoY, the first YoY increase in six quarters. WM fees increased 12% YoY to S$377mn from higher bancassurance and investment product sales. Card fees grew 17% YoY to S$237mn from higher spending including for travel while loan-related fees rose 17% YoY to S$133mn. These increases were moderated by a 5% YoY decline in transaction service fees led by trade finance.

+ Other non-interest income rose 52% YoY. Other non-interest income rose 52% YoY mainly due to an increase in net trading income from higher trading gains and an increase in treasury customer sales to both wealth management and corporate customers. Additionally, gains from investment securities more than doubled due to improved market opportunities.

The Negatives

- Allowances rose 57% YoY. 2Q23 total allowances were higher 57% YoY due to an increase in SP to S$114mn (2Q22: S$69mn) offset by higher GP write-back of S$42mn for the quarter (2Q22: write-back of S$23mn). Resultantly, 2Q23 credit costs rose by 2bps YoY to 10bps. Nonetheless, the NPL ratio declined to 1.1% (2Q22: 1.3%) as new NPA formation fell by 39% YoY. GP reserves rose slightly to S$3.80bn, with NPA reserves at 127% and unsecured NPA reserves at 224%.

- CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 14.9% points YoY to 51.5%, mainly due to the high interest rate environment and a continued move towards fixed deposits (FDs). Resultantly, total customer deposits fell 2% YoY to S$520bn as the decline in CASA deposits were partially offset by growth in FDs.

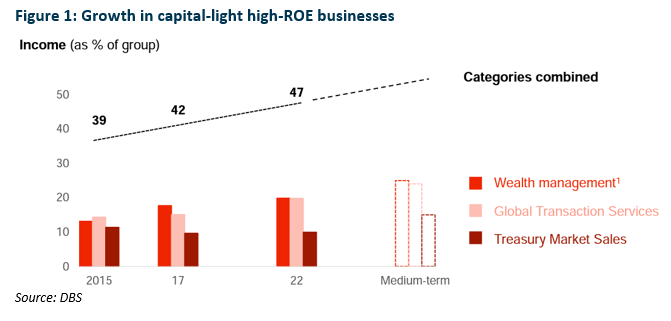

We attended DBS’ Investor Day on 22 May 2023 where management shared their digital-led strategy in growth markets, how new businesses with potential have evolved from the previous Investor Day in 2017 and addressed some of the questions from investors and analysts. The key takeaways from DBS Investor Day 2023 are:

Group Financials

The Positives

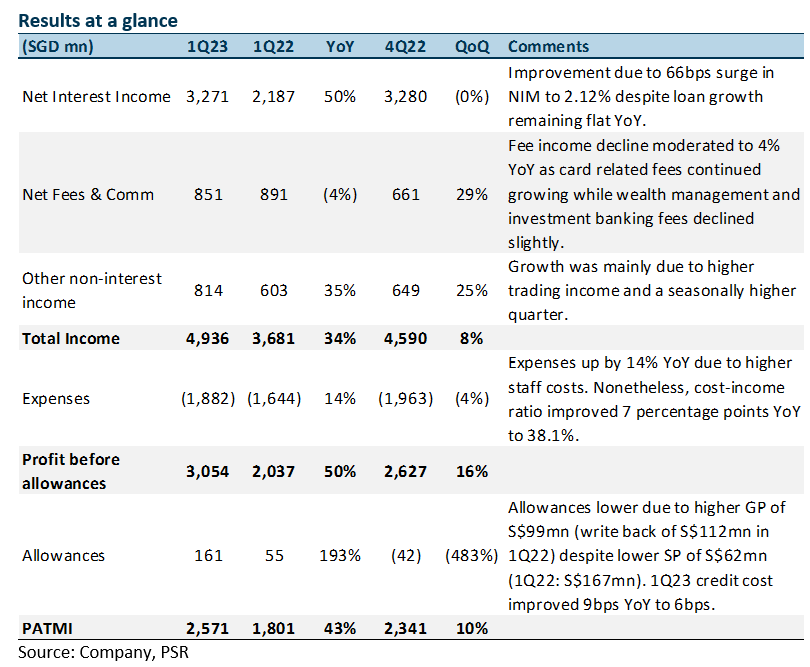

+ NIM and NII continue to increase. NII spiked 50% YoY to S$3.27bn due to a NIM surge of 66bps YoY to 2.12% (2Q22: +12bps, 3Q22: +32bps, 4Q22: +15bps, 1Q23: +7bps) despite loan growth remaining flat YoY. Increases in trade and non-trade corporate loans led by Singapore real estate acquisition financing were offset by lower consumer loans as wealth management loans declined. Management has lowered its NIM guidance from 2.10% to 2.05-2.10% and indicated that NIM has likely peaked in 1Q23 with the NIM decline to be gradual for the rest of 2023 due to an increase in funding costs.

+ Fee income rose 29% QoQ, YoY decline moderated to 4%. Fee income declined 4% YoY (3Q22: -13%, 4Q22: -19%) due to weaker market sentiment affecting wealth management and transaction service fees, which more than offset increases in card and investment banking fees. Nonetheless, fee income saw a recovery of 29% QoQ from broad-based growth. WM fees increased 39% QoQ to S$365mn due partly to seasonal effects, while investment banking fees spiked 91% QoQ to S$44mn from higher equity and debt capital market activity. Loan-related fees surged 80% QoQ to S$142mn, while transaction service fees rose 2% QoQ. However, card fees fell 7% QoQ to S$227mn due to seasonally-higher spending in 4Q22.

+ Other non-interest income rose 35% YoY. Other non-interest income rose 35% YoY and 25% QoQ, mainly due to an increase in treasury customer income and it being a seasonally higher quarter.

The Negatives

- Allowances rose 193% YoY. 1Q23 total allowances were higher 193% YoY due to higher GP of S$99mn for the quarter (1Q22: write- back of S$112mn) offset by a decline in SP to S$62mn (1Q22: S$167mn). Nonetheless, 1Q23 credit costs improved by 9bps YoY to 6bps as there was a decline in new NPLs by 89% to S$17mn for 1Q23. The NPL ratio declined to 1.1% (1Q22: 1.3%) as new NPA formation fell by 53% YoY. GP reserves rose slightly to S$3.83bn, with NPA reserves at 127% and unsecured NPA reserves at 229%.

- CASA ratio decline continues. The Current Account Savings Accounts (CASA) ratio fell 24% YoY to 52.4%, mainly due to the high interest rate environment and a continued move towards fixed deposits (FD). Nonetheless, total customer deposits increased 2% YoY to S$529bn. Management said that deposits and wealth management net new money benefited from flight-to-safety inflows in March 2023.