The Positives

+ Continued recovery. 3Q20 cash revenue (excluding straight-line income recognition) recovered to -7.5% of 3Q19 levels (Figure 1). This was an improvement from June’s 9.5% YoY drop in turnover rent. Turnover rent is used as a proxy for tenant sales as Dasin does not disclose this metric. MoM, turnover rent recovered from January through June (Figure 2). But as monthly turnover rent was also not disclosed, we rely on 3Q20 cash revenue to gauge the recovery in tenant sales.

+ Lease renewals reduced FY20 expiring lease from 13.8% to 8.1%. Portfolio lease expiries by GRI fell from 13.8% in 2Q20 to 8.1% in 3Q20. The majority will be from Xiaolan, Ocean and Shiqi. Historically, these three assets maintained high occupancies of 98-99%. The steady recovery in their tenant sales is encouraging and may return confidence to tenants who have been delaying their renewal decisions.

The Negatives

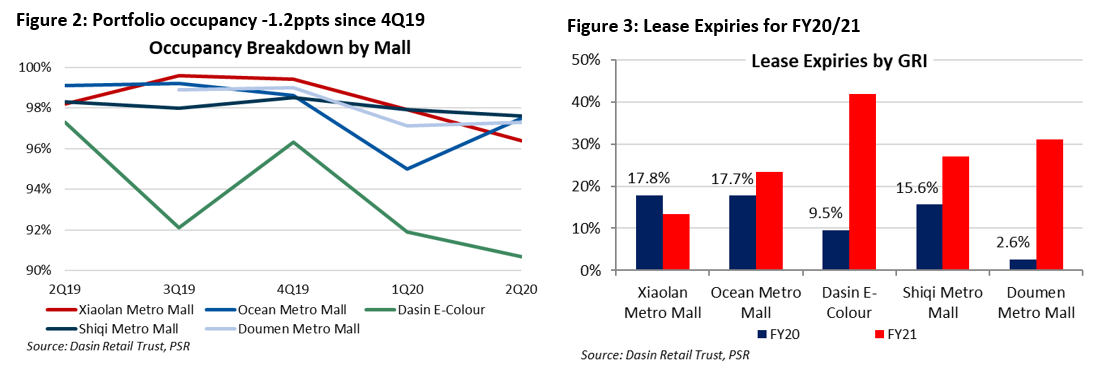

- Portfolio occupancy dipped QoQ from 97.0% to 96.1% (3Q19: 98.6%). The most notable decline was at Dasin E-Colour, which fell from 90.7% in 2Q20 to 85.1%. This was 11.2ppts lower than 3Q19’s 96.3%. Dasin E-Colour was affected by the closure of nearby universities during lockdowns. They are the mall’s primary catchment. The mall is the smallest in Dasin’s portfolio, accounting for 4.14% of its 9M20 revenue. The rest of its malls sustained high occupancy of above 95%. The property manager will use this period of weaker leasing to refine its tenant mix and reposition mall offerings.

- Termination of remaining 9-year lease with Superior City Department Store. Superior’s lease was for 15 years from 28 December 2014 to 27 December 2029 for c.12,000 sqm (17.6%) of space at Ocean Metro Mall. This was terminated on 8 November 2020 as the department store struggled financially. Zhongshan Dasin Metro-Mall Merchant Investment Co. Ltd., an interested party of the Trust, will be leasing the space for a year at similar rents as Superior. AEI will be undertaken over the next year to carve up the space into smaller sections. The work will be done progressively so as to minimise disruptions to operations.

Typically, conversion from single tenancy to multi-tenancies will allow the landlord to charge higher rentals as discounts are usually given for larger spaces.

Outlook

Opportunity for rental reversions through AEI

Department stores are struggling. Hence, while the pre-termination of such a long lease reduces income visibility, Dasin has the opportunity to recalibrate and enhance the mall’s offerings. Dasin last completed AEI at the Ocean Metro Mall in 2Q20. This similarly involved carving up sizeable space. In a bid to enhance the mall’s competitiveness, the Trustee-Manager had commissioned a market research study and negotiated the early termination of a 9,085sqm lease with a “furniture and finishing” tenant. The space returned was dissected and leased out to tenants providing goods and services for children. Rental reversion was 42.9%. About 2,500sqm of space has been leased out to a children’s playground operator, with the remainder leased to children’s education and enrichment tenants.

Benefits from transformation of Greater Bay Area

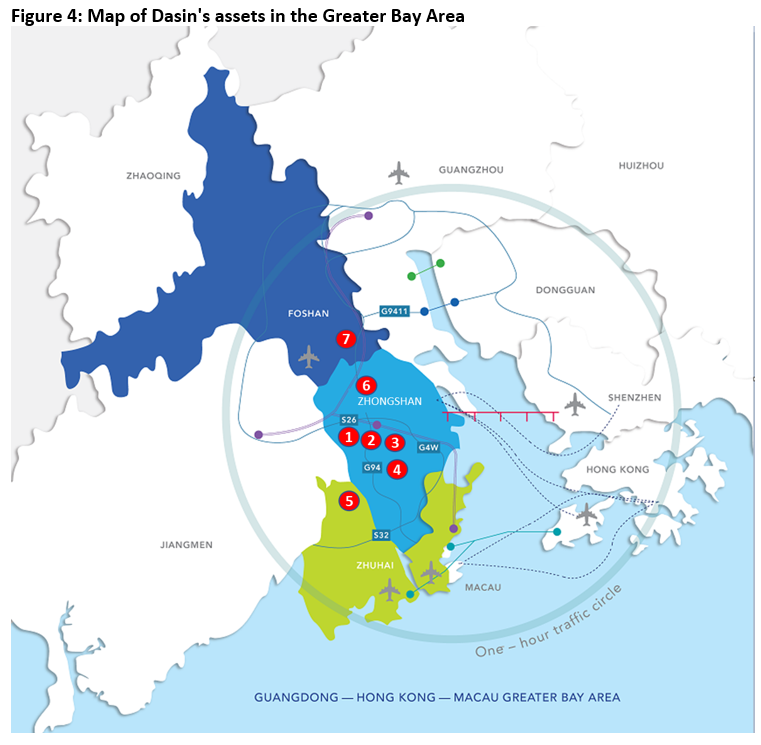

China intends to develop its Greater Bay Area into a booming financial hub under its 13th 5-Year Plan in December 2016. Up-and-coming financial exchanges will be located in Guangzhou (for carbon-emission futures trading) and Macau (a NASDAQ-like market for start-ups). With this transformation, the population in Greater Bay Area is forecast to grow by 43% over the next 15 years, to 100mn. All seven of Dasin’s malls are located in the Bay: five in Zhongshan, one in Foshan and the last in Zhuhai. All are within a 1-hour traffic radius of Greater Bay Area cities (Figure 4). As Tier-2 cities, they provide affordable housing to surrounding Tier-1 cities like Guangzhou and Shenzhen. Zhongshan is primed to benefit from its location at the mid-point of the Bay as well as the Shenzhen-Zhongshan bridge which is under construction. When completed in 2024, the bridge will slash travelling time between the two cities from one hour and 15 minutes to 30 minutes.

Income visibility from lease structure

Dasin’s assets maintain high occupancy of 97%. WALE by GRI is 4.0 years. Only 4% of its leases by GRI are on pure turnover terms. About 20% are structured as the higher of base or turnover rents. Another 12% are fixed while 64% are fixed with built-in rent escalations of 3-10% per annum.

Upgrade to BUY, albeit with lower TP of S$0.90, from S$0.91

We lower FY20/21e DPU by 4.0%/1.8% to factor in an enlarged share base following its recent share offering. Upgrade from ACCUMULATE to BUY with stock catalysts expected from the population growth in the Greater Bay Area, potential acquisitions, and rental uplift post-AEI. Our DDM TP dips from S$0.91 to S$0.90. It translates to FY20e/21e DPU yields of 6.3%/7.2%.

Dasin continues to have an ROFR pipeline of 18 properties in four cities. Six are still under construction. During IPO, major unitholders waived a portion of their distribution entitlement to support DPU yields. The percentage of units under distribution waiver will dwindle to 0% by 2022. Dasin will have to grow its DPUs to offset an increasing unit base, in order to prevent deterioration of its DPU yields. The percentage of units under distribution waiver stands at 25% and 11% for FY20 and FY21 respectively. Dasin acquired three assets from its sponsor in the last two years and we expect it to tap its ROFR pipeline again to keep DPU yields stable.

Risks to our view and valuation include a slowdown in discretionary consumption and a second wave of virus outbreaks in China.

The Positives

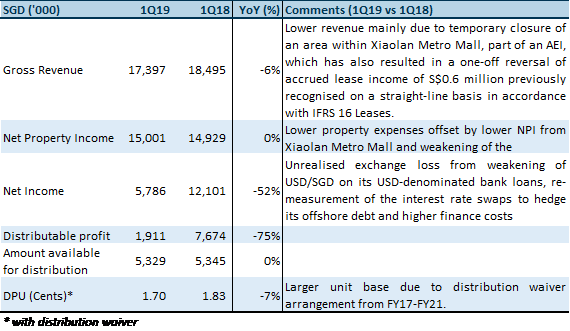

+ June 2020 turnover rent recovered to 90.4% of 4Q19 average, lifted by the easing of lockdown measures (Figure 1). 4% of leases are on pure turnover basis, a proxy for tenant sale, which have exhibited a similar recovery.

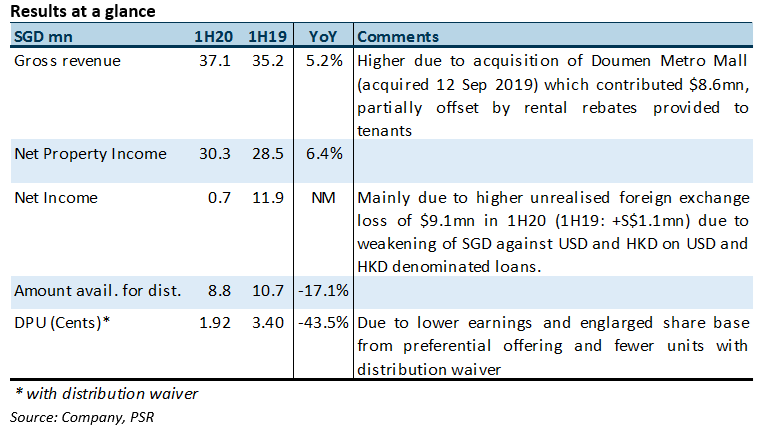

+ Portfolio occupancy inched by 0.2ppts QoQ to 97.0% (4Q19: 98.8%). 9,085sqm (13.2%) of NLA in Ocean underwent AEI in 4Q19. Due to COVID-19 disruptions, completion was delayed from 1Q to 2Q. Since then, occupancy at Ocean improved by 2.5% QoQ (Figure 2.), securing rental reversion of 47% over previous rents. Separately, rents signed in 2Q were flattish, likely to remain flat for 2H20. Occupancy at Dasin E-Colour fell 5.6ppts to 90.7% since 4Q19. Tenant trading at Dasin E-Colour was affected by the closure of schools (universities), which are the mall’s primary catchment. Dasin E-Colour is the smallest mall in the portfolio, accounting for 3.3% of 1H20’s revenue.

+ NPI margin improved to 81.6% in 1H20, from 80.7% in 1H19, mainly due to lower operating expenses from lower electricity charges and property tax, as well as property tax rebates provided by the government. Dasin has provided c.S$8mn in out-of-pocket rental rebated for tenants, which translated to c.1month in rental waivers. The management does not foresee offering any additional rebates, given the recovery in tenant trading, which is has recovered to near pre-COVID levels.

The Negatives

- Portfolio valuation fell by 4.6% in RMB terms, due to lower expected rental growth rate, higher discount rate and terminal cap rate assumptions assumed by valuers. In SGD terms, valuations fell by a lower 2.5% due to the strengthening of RMB against SGD.

- 13.8% of leases by GRI expiring in FY20 to be renewed, majority coming from Xiaolan (17.8%), Ocean (17.7%) Shiqi (15.6%) (Figure 3). Historically, these three assets are strong performers have maintained high occupancies of 98% to 99%. As such, we are optimistic on the leasing demand for these malls. A noteworthy 13.8% of leases by GRI (3.5% by NLA) has yet to be renewed (Figure 2), likely due to the uncertainty and softer leasing sentiment in 1H20. The steady recovery in tenant sales is encouraging and may return confidence to tenants who were delaying renewal decisions.

Outlook

Income visibility from lease structure

Assets maintain high occupancy of 97% and WALE by GRI of 4.0 years. Only 4% of leases by GRI are on pure turnover terms, 20% of leases are structured as higher of base rent or turnover rent, 12% of leases are fixed while 64% of leases are fixed with build-in escalation ranging 3% to 10% per annum.

AEIs and refreshing of the malls tenant mix have borne fruit

Xiaolan Metro Mall underwent and AEI on 5% of NLA in 1Q19, which yielded reversions of 44% over previous rents. Similarly, the most recent AEI for 9,085sqm (13.2%) of space at Ocean Metro Mall over the 4Q19 to 2Q20 period has secured rental reversion of 47%.

Acquisition update

The acquisition of Shunde and Tanbei Metro Mall was completed on 8 July 2020 and will contribute c.12% to revenue. Dasin will relook at acquisitions plans in FY21.

Positioned to benefit of transformation of the Great Bay Area

China’s plans to transform the Greater Bay Area (GBA) into a booming financial hub was announced in the 13th 5-year plan in December 2016. The up-and-coming exchanges are located in Guangzhou (for carbon emission futures trading) and Macau (NASDAQ-like market that helps start-ups). With this transformation, the population for Greater Bay Area is forecast to grow by 43% over the next 15 years to around 100 million. All 7 of Dasin’s malls are located within the GBA - 5 in Zhongshan, 1 in Foshan and 1 in Zhuhai, and are within a 1-hour traffic circle of GBA cities (Figure 4). As Tier 2 cities, they provide affordable housing alternatives for the surrounding Tier 1.5 cities like Guangzhou and Shenzhen. Zhongshan is primed to benefit from its location in the midpoint of the GBA, as well as the Shenzhen-Zhongshan bridge which is under construction (est. completion 2021), and will slash traveling time between these two cities from 1hour and 15minutes to 30minutes.

We remain positive on the inorganic growth prospects for Dasin. There remains a ROFR pipeline of 18 properties spanning four cities – six of which are still under construction, which will help to mitigate the DPU gap as the distribution waiver progressively falls off. The number of units under distribution waivers was 38.2% in 2019 and will fall to 24.3% and 19.3% in FY20 and FY21, increasing the number of units that are entitled distributions over the years.

Key risks to our valuation: slowdown in discretionary consumption, second wave of virus and lingering fear and deferment of discretionary spending.

Maintain ACCUMULATE with unchanged target price of S$0.91.

Our TP translates to a FY20e/21e DPU yield of 6.1%/6.9%.

The Positive

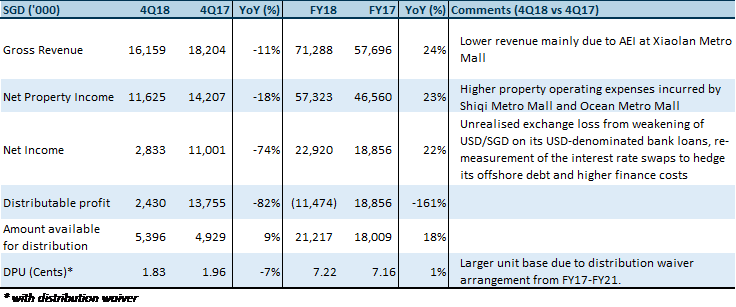

+ Healthy portfolio metrics, protected by lease structure. Dasin’s portfolio is underpinned by assets with high occupancy of 96.8% and long WALE by GRI of 4.5 years. Only 4% of leases by GRI are on pure turnover terms, 20% of leases are structured as higher of base rent or turnover rent, 12% of leases are fixed while 64% of leases are fixed with built-in escalation ranging 3% to 10% per annum. For reference, on a same-store basis, 4Q19 revenue grew by 6.5% in RMB terms and 4.5% in SGD terms, due to built-in escalations.

+ Creating opportunity through crisis. 42 live broadcasts were hosted by influencers and tenants via the live streaming on the “Dasin Hui” app, which has a membership base of 420,000. These broadcasts were conducted from 2 March to 28 April 2020 to drive tenant sales.

The Negative

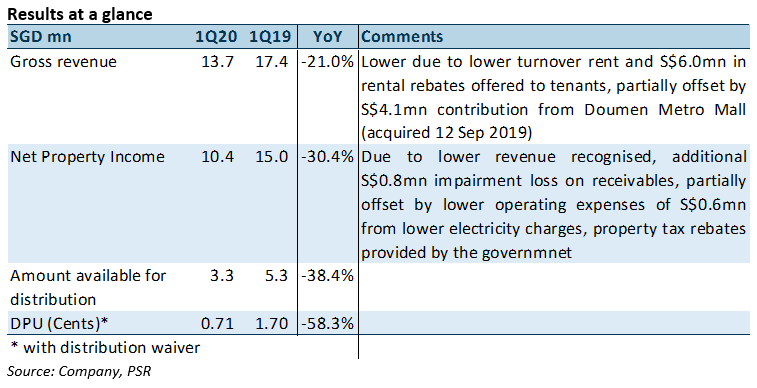

- Malls resumed normal operating hours by March, but March and April turnover rent was still 37% and 32% below 4Q19 levels. All 5 of Dasin’s malls remained operational throughout 1Q20, although operating hours were shortened from 10AM to 4PM from 26 January 2020, except for tenants providing essential services such as supermarkets and certain F&B outlets. Trades that attract larger crows such as cinemas, KTVs, skating rings and bookstores were temporarily closed. Shiqi Metro Mall, Xiaolan Metro Mall, Dasin E-Colour and Doumen Metro Mall resumed normal operating hours since 24 February 2020, while Ocean Metro Mall reverted to its normal operating hours on 2 March 2020, after 31 and 43 days of shortened operating hours respectively. KTVs at all 4 malls resumed operation on 15 May 2020 after 111 days of closure, however tuition and enrichment centres remain closed. Turnover rent, as a proxy for tenant sales, fell by 64% in February when the operating hours were shortened, but recovered to -37% and 32% after normal operating hours were reinstated.

- Portfolio occupancy fell by 2.0ppts QoQ to 96.8% due to lower occupancy across all malls. Dasin managed to renew 74% of the leases expiring in 1Q20. However, occupancy was lower due to non-renewals, as well as space that was vacant due to ongoing AEIs.

Outlook

AEI works for 9,085sqm (13.2%) of space at Ocean Metro Mall commence in 4Q19. The completion of the AEI has been delayed from 1Q20 to 2Q20 due to the COVID-19 outbreak. Approximately 70% of construction work was completed as at 31 March 2020. The AEI was undertaken in a bid to enhance the mall’s competitiveness. Trustee-Manager undertook a market research study and negotiated the early termination of lease with a “furniture and finishing” tenant. The space returned will be carved up and leased out to tenants providing goods and services targeted at children. The space has been full committed, securing rental reversion of 47% over previous rents. 2,500sqm of space will be leased out to children’s playground operator, with the remaining space leased to children education and enrichment tenants.

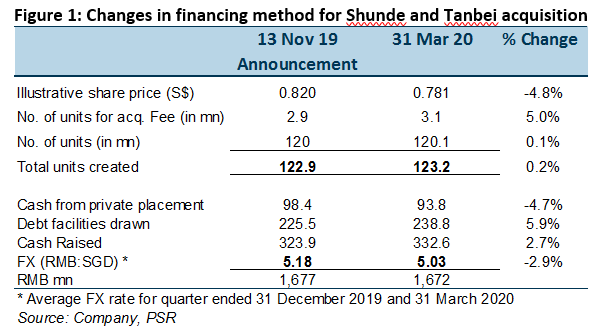

The joint acquisition of Shunde Metro Mall and Tanbei Metro Mall were approved at the EGM on 20 December 2019. We were anticipating a mid-1Q20 completion. However, the COVID-19-induced volatility in the global markets has resulted in delays in the private placement, and consequently the completion of the acquisition. Financing of the acquisition has been adjusted in light of the depreciation of share price and weakening of the Singapore dollar against Renminbi. We think the acquisition is headed for a 3Q20 completion.

We remain positive on the inorganic growth prospects for Dasin. There remains a ROFR pipeline of 18 properties spanning four cities – six of which are still under construction, which will help to mitigate the DPU gap as the distribution waiver progressively falls off. The number of units under distribution waivers was 38.2% in 2019 and will fall to 24.3% and 19.3% in FY20e and FY21e, increasing the number of units that are entitled distributions over the years.

Key risks to our valuation include: slowdown in discretionary consumption, second wave of virus and lingering fear and deferment of discretionary spending.

Maintain ACCUMULATE with higher target price of S$0.91.

We push back the acquisition of Shunde and Tanbei Metro Malls from 1Q20 to 3Q20. Along with the S$7.9mn in rental rebates for FY20, our FY20e DPU was slashed by 16.9%. We also factored in higher vacancy rates for FY20e and FY21e, as well as lower rental reversions. Our DPU translates to a yield of 6.3% for FY20e and 6.8% FY21e.

We expect Dasin to acquire 2 to 3 more assets in order to maintain a c.8% DPU yield by the time the distribution waiver falls off completely in FY22. As such we raise our terminal growth rate from 0.5% to 1.5% to better reflect the pace of acquisitions. The adjustments to our forecasts resulted in a higher TP of $0.91.

Phillip Securities Research has received monetary compensation for the production of the report from the entity mentioned in the report.

The Positive

+ Three acquisitions announced in FY19 and built-in rental reversion to mitigate DPU gap. The number of units under distribution waivers was 38.2% in 2019 and will fall to 24.3% and 19.3% in FY20 and FY21, increasing the number of units that are entitled distributions over the years. The three acquisitions announced in FY19 (Shunde and Tianbei TBC in 1Q20), as well as the built-in rental escalations averaging 9% p.a. will help to increase earnings, closing the gap between the DPU with and without distribution waiver.

+ Healthy portfolio metrics, protected by lease structure. Dasin’s portfolio is underpinned by assets with high occupancy of 98.8% and long WALE by GRI of 4.1 years. High proportions of leases have minimum income guaranteed – 13% of leases are fixed while 66% of leases are fixed with build-in escalation ranging 3% to 10% per annum. Excluding the contribution from Doumen, 4Q19 revenue grew by 6.5% in RMB terms and 4.5% in SGD terms, due to built-in escalations.

The Negative

- Weaker China retail outlook dampened tenant sales. Tenant sales was positive in 1H19, however in 2H19 tenant sales came in flat, in line with the weaker China retail market.

Outlook

AEI works for 9,085sqm (13.2%) of space at Ocean Metro Mall commence in 4Q19. In a bid to enhance the mall’s competitiveness, the Trustee-Manager undertook a market research study and negotiated the early termination of a lease with “furniture and finishing” tenant. The space returned will be carved up and leased out to tenants providing goods and services targeted at children. The space has been fully committed, securing rental reversion of 42.9% over previous rents. 2,500sqm of space will be leased out to children’s playground operator, with the remaining space leased to children education and enrichment tenants, who will begin operating in 1Q20.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.

Impact of Covid-19

All 5 of Dasin’s malls, except the supermarkets within the malls, were closed from 28 January 2020 to 24 February 2020. All malls have resumed norming operating hours, except Ocean Metro Mall – operating hours shorter by 1 hour due to different mandates by different municipals. The manager is prepared to offer assistance to tenants affected by the outbreak and will do so on a case-by-case basis, pending a review of the extent of the tenant’s trading disruptions.

We remain positive on the inorganic growth prospects for Dasin. There remains a ROFR pipeline of 18 properties spanning four cities – six of which are still under construction. Key risks to our valuation remain the FX volatility and the depreciation of the RMB

Maintain ACCUMULATE with a lower target price of S$0.88.

Our target price of S$0.88 translates to a DPU yield of 7.1% for FY20e and FY21e. We expect Dasin to acquire 2 to 3 more assets to maintain a c.8% DPU yield by the time the distribution waiver falls off completely in FY22e.

The Positive

+ 15.3% ROI on AEI at Xiaolan Metro Mall. One of the AEI at Xiaolan was opportunistic embarked on after a restaurant tenant gave up half the space (2,500 sqm, 3.2% of mall NLA) of a lease with a 2026 expiry in 1Q19. This AEI costs S$0.8mn is expected to be completed by end-2019. The surrendered space will be carved up into eight smaller units for new F&B tenants. Six of the leases have since commenced in Aug 2019. Dasin is expecting to receive a 35% increase in rental post-AEI, translating to a c.15.3% ROI on the AEI.

The Negative

- Falling property valuation and NPI margins. Valuations fell by 1.1% to 3.3% across all four malls resulting in a S$21mn revaluation loss. This was due to lower rental growth rate assumptions used by the valuer. NPI margins were 75.4% for 2Q19 (2Q18 87.5%), 5ppts lower than DRT’s targeted annualised NPI margin of 80% due to higher operating expenses (+S$0.5mn) and higher stamp duty on leases (+S$0.3mn). As two of the malls (Ocean Metro and Dasin E-Colour) are relatively younger malls, we can expect rental growth from the refinement of the tenant mix, as well as selective AEIs, which will help to increase valuations in the mid-term.

What else is new?

Proposed acquisition of Doumen Metro Mall

Dasin announced the proposed acquisition of Doumen Metro Mall from the Sponsor on 30 June 2019. The agreed property value of RMB1,585mn (S$317.1mn) is a 23% discount to valuation and will increase the AUM by 21.8%, contributing 21.4% of revenue to the enlarged portfolio. The proposed acquisition is will likely be c.75% debt funded and will increase DRT’s gearing from 32.3% to 35.2%. As this is an interested-party transaction, the acquisition will be subjected to a shareholder vote at the EGM on 16 Aug 2019. If approved the transaction is expected completed by end-2019.

Key benefits of the acquisition are:

Recall that Dasin has a distribution waiver where two of Dasin’s largest shareholders elect to waive their rights to distributions (DPU) until FY22. The distribution waiver is meant to provide short-term DPU support to smoothen out the gestation period of the two younger malls in the portfolio, Dasin E-Colour and Ocean Metro Mall. The number of units that will not be entitled to distributions will decline over the years such that the “DPU support” will fall off gradually. With c.2.3 years until the end of the distribution waiver, the current gap between the DPU with and without the distribution waiver measures at 3.41 cents, almost double the current DPU without distribution waiver (3.81 cents).

The management has two ways to bridge the DPU gap – operationally driven organic growth or growing revenues inorganically through acquisitions. We will see more meaningful growth in revenues via acquisitions, as evident by the 12.1% accretion of real underlying DPU in the absence of the waiver. While current shareholders will be unaffected by the accretion and still receive the same dollar amount of DPU(Figure 1), the growth in earnings and underlying DPU will help to close the DPU gap and mitigates the possibility of a DPU cliff in FY22.

Outlook

We remain positive on the inorganic growth prospects for Dasin. There remains a ROFR pipeline of 20 properties spanning four cities – six of which are still under construction. Shunde Metro Mall, will be next likely acquisitions for Dasin.

Maintain ACCUMULATE with an unchanged target price of S$0.94.

Our target price of S$0.94 translates to a FY19e yield of 8.0% and a P/NAV of 0.65x. Key risks to our valuation remain the FX volatility and the depreciation of the RMB.

Results at a glance

Source: Company, PSR

The Positives

+ NPI margins improved across the board. While revenue declined on the whole, NPI was held up by lower property expenses across all assets, which relate to the lower maintenance, cleaning, advertising and promotion costs. Shiqi Metro Mall, Dasin’s largest contributor by GRI, saw its NPI margin improve to 87% in 1Q19 from 78% in 1Q18.

The Negatives

- Occupancy at Xiaolan Metro Mall fell to 95% from 99.2% in 4Q18. This was due to a new S$1.0mn AEI initiative at Xiaolan Metro Mall, its second biggest contributor by GRI. c.2.5k sqm of GFA on the fifth floor of Xiaolan Metro Mall has been closed for tenant reconfiguration, ahead of the original lease term expiry in 2026. The AEI is expected to complete in 3Q19.

Outlook

While occupancy will be depressed in the near term, favourable renewal and rental escalation rates are progressively expected at Xiaolan Metro Mall once the ongoing AEI is completed. We remain positive on the inorganic growth prospects for Dasin, with its ROFR pipeline of 20 properties spanning four cities – 14 of which have been completed. Doumen Metro Mall and Shunde Metro Mall, both completed in 2018, are possible acquisitions as they would provide Dasin the runway for growth.

Maintain ACCUMULATE with adjusted target price of S$0.94

Our target price of S$0.94 translates to a FY19e yield of 8.4% and a P/NAV of 0.60x.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report

Results at a glance

Source: Company, PSR

The Positives

+ Healthy reversions despite AEIs at Shiqi and Xiaolan. Rental reversion of 8.2%, on a portfolio basis, was achieved in FY18 despite AEIs done at Shiqi Metro mall and Xiaolan Metro mall (the two highest contributing malls, by GRI) through 2H18. The AEIs have been completed as end-Dec 2018 and full fitting-out of all new tenants is expected to complete by 1H19.

+ Average debt term-to-maturity doubled to 1.6 years. Dasin’s first tranche of offshore debt – comprising S$106.6mn and USD52.4mn, which was due to expire in Jan 2019 – had been extended by two years, to Jan 2021, at a lower interest margin (reduction of c.70bps). Less than 1% of its total debt is due in 2019.

The Negatives

- Slower-than-expected growth at “growth malls”. Excluding Dasin’s matured malls (Shiqi and Xiaolan), performance for its growth malls (Ocean Metro and Dasin E-Colour) fell short of our expectations as FY18 NPI for these two malls fell in excess of 4% YoY. Notwithstanding the effect of rental straight-lining, the bigger contributors to this dip stemmed from the loss of event space at Ocean Metro in 3Q18, as well as expenses incurred for its carpark renovation at Ocean Metro and higher operating expenses at Dasin E-Colour. We note that a significantly higher proportion of leases at Ocean Metro mall are now on the “fixed rent with built-in escalation” structure (as opposed to solely “fixed rent”), at 61% of the mall’s GRI (4Q17: 43%). This would provide more upside to the leases at Xiaolan Metro mall going forward, given that it is the newest and fastest growing mall in the portfolio.

Outlook

The AEIs done at Shiqi and Xiaolan malls will see renowned names such as Hai Di Lao enter the tenant mix. Favourable renewal and rental escalation are thus expected at these two malls going forward.

2018 saw the opening of two of its 20 pipeline malls, Doumen Metro mall and Shunde Metro mall, which could be among the immediate acquisitions as these newly opened malls would provide Dasin the runway for growth.

In addition, the blueprint for the Greater Bay Area Master Plan that was released on 18 Feb 2019 further entrenches the positioning for both Dasin’s existing and pipeline malls, which are spread across Zhongshan, Zhuhai, Foshan and Macau (all in the Greater Bay Area – figure 1).

A future macro catalyst would be the Shenzhen-Zhongshan Corridor, which is expected to be completed in 2024. It will be a 51km eight-lane highway that is expected to reduce travel time between Shenzhen and Zhongshan/Jiangmen by approximately 30 minutes.

Maintain ACCUMULATE with adjusted target price of S$0.94 (prev. S$0.95)

We adjust our target price to account for lower finance costs and certain changes to the lease structure arrangement. Our target price of S$0.94 translates to a FY19e yield of 8.2% and a P/NAV of 0.64x.

Results at a glance

Source: Company, PSR

The Positives

+ Robust occupancy and continued healthy reversions. Despite ongoing asset enhancement initiative (AEI) at Xiaolan Metro Mall, occupancy remains strong at 97.6% and positive rental reversions continue to be recorded in 3Q18. The Manager had communicated that the AEI at Xiaolan Metro Mall is expected to be completed this year and will yield renowned names such as Hai Di Lao.

The Negatives

- Higher cost of funds. Average all-in cost of borrowings for Dasin’s offshore debt increased by 30bps QoQ, of which only 40% is hedged. While the remainder of its 2018 debt had been fully refinanced in 3Q17, this upward movement in interest rates – especially when sustained in the current rising interest rates environment – could further inflate finance costs as we edge closer to 2019, with the first tranche of debt expiring in Jan 2019. Current gearing level was also a result of the decline in valuation of investment properties in 2Q17.

Outlook

Current gearing of 32.5% affords Dasin S$115mn of headroom (assuming 40% gearing) to pursue inorganic growth, which can be through third party or its ready pipeline of 20 properties – 12 of which have been completed.

Maintain ACCUMULATE with lower target price of S$0.95 (prev S$0.97)

We lower our target price to adjust for higher finance costs and changes in rental growth assumptions. Our target price of S$0.95 translates to a FY18e yield of 8.5% and a P/NAV of 0.58x.

The report is produced by Phillip Securities Research under the ‘SGX StockFacts Research Programme’ (administered by SGX) and has received monetary compensation for the production of the report from the entity mentioned in the report.