The Positives

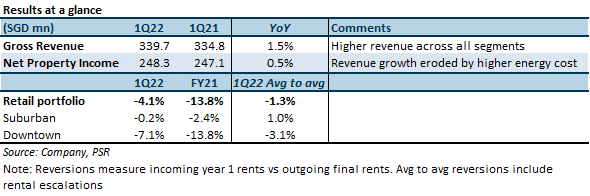

+ Narrowing negative reversions reflective of improving tenant sentiment. 1Q22 retail reversions came in at -4.1% compared with FY21's -7.9%, with reversions at suburban malls improving from -2.4% to -0.2% and downtown malls narrowing from -13.8% to -7.1%. CICT renewed 7% of retail NLA in 1Q22, with retention rate coming in at 91%. Despite 5.3% YoY decline in footfall, 1Q22 tenant sales gained 0.6% YoY, driven by driven by discretionary trades such as fashion, accessories and beauty. Retail occupancy came in at 96.6% (-0.2ppts QoQ), due to leases expiring in Clarke Quay ahead of its impending AEI, excluding which occupancy would be 98.3%.

+ Office reversions came in at +9.3%, attributed to Singapore assets. CICT signed c.8mn sq ft of space in 1Q, 12% of which are new leases from tenants in the financial services, IT, media and telecommunications and manufacturing and distribution. Occupancy for the Singapore office portfolio improved from 90.4% to 92.3% but remains below market average of 93.8%. Significant occupancy gains at Six Battery Road (+8.7ppts), CapitaSpring (+7.0ppts) and Asia Square Tower 2 (+1.9ppts). Backfilling of Six Battery Road and Capital Tower still in progress, with occupancy coming in at 88.4% and 76.6% respectively. CICT is in advanced negotiations with several tenants for space at Capital Towers which would bring occupancy to c.94% if concluded. Tenant retention rate was high at 95.5%, albeit with some tenants choosing to downsize. We understand that some bank tenants who have previously downsized are requesting for more space.

The Negative

- Higher electricity cost expected in FY22. Electricity accounts for c.5% of OPEX. The impact of rolling onto new electricity contracts at tariffs that are 90% higher YoY, will be felt in 1Q22 as well as in FY23 when the fixed contracts expire. The management is reviewing increasing the service charge but articulated that the higher electricity cost may be partially offset through higher gross turnover rents when retailers raise prices to cope with inflationary costs.

The Positives

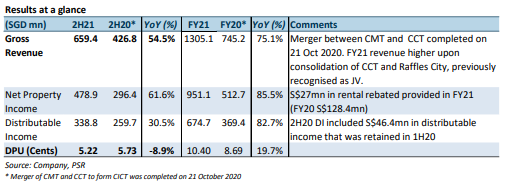

+ Recovery in tenant sales and narrowing negative reversions support improving tenant sentiment. Full-year retail reversions narrowed to -7.3% (1H21: -9.1%). Suburban and downtown reversions were -2.4% and -13.8% respectively. Tenant retention remains stable at 82% (FY20 84.5%). Broader recovery amongst trade categories was observed from the 12.2% YoY growth in total tenants' sales, with nine out of 15 trade categories showing YoY growth. However, FY21 tenant sales psf was still below pre-pandemic levels, at 87.8% of FY19's monthly average. Rental support has also eased – FY21 rental waivers came in at S$27mn, slightly more than half a month of rent, compared to the S$128.4mn in rebates disbursed in FY20.

+ Valuation uplift of 3.5% or S$752.8mn YoY. Retail assets saw a modest 3% valuation uplift on the back of recovering performance while cap rates remain unchanged. Office and integrated development assets accounted for 45% and 52% of the revaluation gains, owing to cap rate compressions for office assets and CapitaSpring achieving TOP in Nov 21. Clarke Quay and Raffles City took a S$52mn and S$107mn write-down due to CAPEX provisions for upcoming AEI works. Valuation for Gallileo fell by 13.2% of S$76mn as valuers factored in the exercise of lease break option by Commerzbank, which will bring forward the lease expiring from 2029 to 2024.

+ Portfolio reconstitution and entry into new market. CICT divested its 50% stake in OGS for S$640.7mn at an exit yield of 3.17%, 9.1% above valuation price on 30 Sep 21. It also entered a new market, Australia, making a A$1.1bn investment in two Grade A office buildings and 50% interest in integrated development, 101-103 Miller Street and Greenwood Plaza. These three Australian acquisitions carry an average NPI yield of 5.1% and a pro-forma DPU accretion of 2.8%. Post-acquisition, Australia represents c.5% of AUM. Capital recycling continued into FY22 - CICT announced the sale of JCube for S$340.0m at NPI yield of c.4%, 21.9% above FY21 valuation, realising net gains of S$56.7mn.

+ Positive

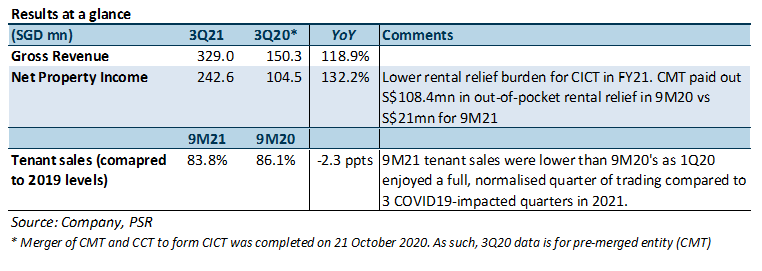

+ Tenant sentiment recovering. 9M21 retail reversions improved to -8.0% from -9.6% as at 6M21, -3.8% and -14.3% for suburban and downtown malls respectively. Average incoming vs average outgoing rents have also narrowed QoQ from -4.4% to -3.5%. Tenant sentiment continues to recover, with positive reversions for some suburban leases. New to market/portfolio and expansions account for 65.5% and 34.5% of 3Q21 retail leases, of which F&B and Beauty & Health account for 62.3% and 15.5%. Office leasing enquiries grew 1.3x QoQ, driven by expansion (38%), relocation (32%), consolidation (23%) and new set-up space (7%) enquiries. 5.4%/26.3% of office expiries by GRI remain for FY21/22. CICT has begun renewal discussions for 19.4% of FY22 expiries. CICT continues to sign leases above market rents although 9M21 reversions still in the negative single digits.

- Negative

- Tightened restrictions dampened leasing, depressing occupancy. Softer leasing due to the two-pax group size during the second P2HA and stabilisation phase have reduced physically viewings. Retail occupancy dipped QoQ from 97.0% to 96.4% due to Atrium@Orchard (-2.1ppts), Clark Quay (-2.6ppts) and Bugis+ (-2.8%). 9M21 tenant sales dipped to 83.8% of 2019 levels (6M21 86.3%) due to tightened restrictions. Slight decline in office occupancy QoQ from 93.0% to 92.6% due to downsizing at CapitaGreen (-3.6%) and Asia Square Tower 2 (-1.9%).

Outlook

Leasing continues to recover although dampened by the containment measures. Office physical occupancy remains low at 15.7%. Relaxation of safe management measure and return to office should provide an uplift for tenant sales and carpark revenue.

Committed occupancy at CapitaSpring continues to creep up, landing at 83.1% as at end-Sep21, with another 7.2% of leases under advance negotiation. Majority of tenants are expected to move in and begin contributing to income in 2H22. CICT is repositioning Raffles City to an upscale shopping destination and has garnering good interest from prospective fashion, beauty and lifestyle retailers. AEI works to reconfigure the space previously occupied by Robinsons into smaller units and improved vertical connectivity within the mall are expected to be completed in 4Q22. Plans to reposition Clark Quay are still under discussion.

CICT granted S$19mn in rental rebates for 1H21, equivalent to 0.3months in rent waivers. The management is forecasting another c.$10mn for 2H21. Our FY21e DPU forecast of 10.19 Scnts factors in a more conservative 1 month of rental rebate for FY21 versus the management’s current estimate of c.0.5 months.

Maintain ACCUMULATE and DDM-based TP of S$2.54

No change in our forecasts. Current share price implies 4.8%/5.6% FY21e/22e DPU yields. Catalysts could include stronger-than-expected sales growth, asset enhancement initiatives to unlock value and portfolio reconstitution.

The Positives

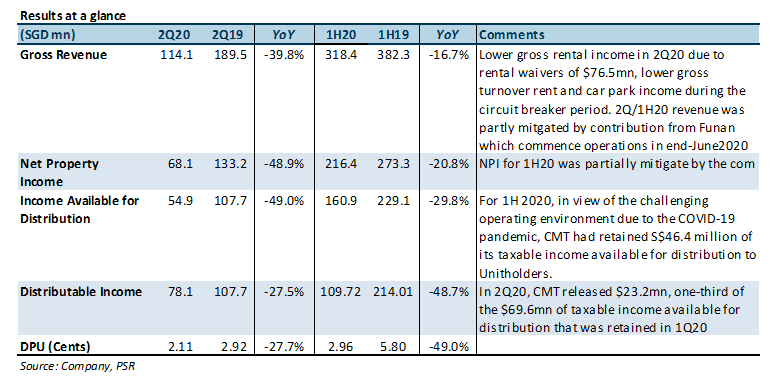

+ Tenant sales fell by a smaller magnitude (-15.4%) compared to footfall (-40.6%). This was due to the strong performance by Supermarkets (+18.6%) and pent-up demand for Books & Stationery (+0.7%). CapitaLand also launched e-commerce platform (eCapitaMall) and online food ordering platform (Capita3Eats) on 1 June 2020 which was able to help tenants capture some sales, adding to tenant sales.

+ Eked out +0.1% rental reversions in 2Q20 (1Q20: 1.6%). Reversions were a mixed, with with downtown and suburban malls clocking both positive and negative rental reversions. There were non-renewals of c.2% of NLA in the quarter. 7.6% of leases by GRI remains for the FY20. Occupancy remained high at 97.7%, although it has come down from 99.3% as at 31 December 2020. We are expecting a softer leasing environment for the 2H20.

The Negatives

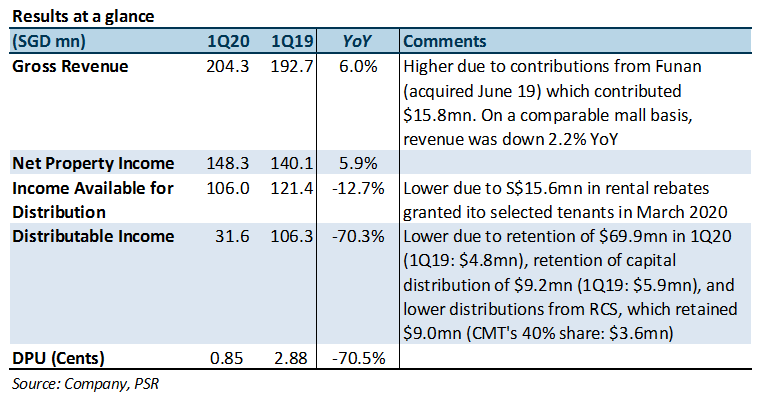

- Amount of rental rebates increased from $114mn to $154.5mn. The amount of rental relief committed as at 30 June 2020 was $154.4.5mn which comprised rental waivers from landlord, property tax rebates and cash grant (to be reimbursed by the government) and rental relief to qualifying SME tenants (based on CMT’s estimation of 60% SME tenants). This was $40.5mn higher than the $114mn (including property tax rebates) committed in April 2020, but largely attributed to the cash grant for SMEs from the government which are on a pass-through basis. Pending clarification from the authorities on definition and prescription of SMEs under the “New Rental Relief Framework for SMEs” (COVID-19 Bill), CMT may have to increase the amount of rental support given.

- Portfolio valuations fell 2.5% (including RCS 2.7%). Valuations were lower by -0.6% (Junction 8) to -4.8% (Clark Quay). The valuations were largely driven by lower market rents and rental growth rates due to economic uncertainties and COVID-19. There was no change in capitalisation rate assumptions.

Outlook

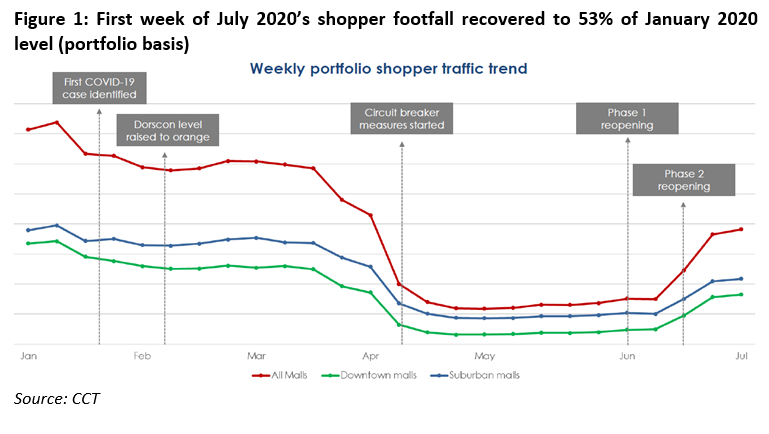

95% of CMT’s tenants are operating and shopper footfall has recovered to 53% of January 2020 levels as of the first week of July (1H20: 40.6%, Figure 1). Footfall at suburban malls was c.58% of January levels, with stronger suburban mall registering up to 80% of normalised footfall. Footfall at downtown malls ranged between 40-55%, averaging 49%.

Tenant relief package

In addition to the rental rebates of $154.5mn, CMT has also waived turnover rent and allowed tenants to release one month security deposits to offset rents. On average, CMT collects 3 to 5 months of security deposit from tenants. The release of 1 month’s security leaves 2 to 4 months of security deposits as a safety net.

Leases with higher risk-sharing

Maintaining occupancy remains a high priority. Apart from granting rental deferments, CMT allowed lease restructuring as a more holistic solution for tenants in this uncertainty environment. Going forward, we can expect the more leases with risk sharing. While structuring leases with higher risk-sharing, CMT will aim to keep occupancy cost between c.18%, consistent with historical occupancy cost. The management shared that they will be prepared to offer leases with more risk-sharing in the initial years for selected new-to-market brands (e.g. 1st year – pure GTO rents, 2nd and 3rd year some fixed rent tagged to certain level of sales).

CMT employed this strategy with Funan, which has a comparatively higher number of tenants on lease structures with a larger GTO component. In the long run, higher risk-sharing may increase the demand for retail space as the lower fixed rents makes it more economically viable for new-to-market brands to give the brick-and-mortar model a go – 30% of Funan’s tenant are new-to-market brands.

Maintain BUY with an unchanged TP of $2.33.

Maintain BUY with an unchanged TP of $2.33. We are keeping our estimates unchanged as we have previously incorporated c.$80mn of out-of-pocket (OOP) rental rebates, above the $76.5mn OOP rebates guidance for 1H20. Our FY20e/20e DPU presents a FY20e DPU yield of 5.8%/6.3%.

The Positives

+ One-third of FY20’s lease expiries renewed in 1Q20 with average reversion of 1.6%. Out of the 21.3% of leases (by GRI) expiring in FY20, 11.9% of leases by GRI remains for the year. While the positive rental reversion achieved in 1Q20 is not indicative of future reversions which are expected to be mildly negative, the comparatively low expiries remaining for FY20 is a mild consolation. A higher 28.5% of leases will expire in FY21. The management is prioritising occupancy rates and will exercise creativity and flexibility in their leasing strategy.

The Negatives

- 1Q20 tenant sales down 7.5% YoY. Tenant sales for the top 5 trade categories which contribute >70% of gross rental income fell 6.5%. The only trade category which experienced positive tenant sales were the Supermarket (+13.1%) and Books & Stationery (+0%).

- Pre-terminations at Clark Quay in the low-single digits, by NLA. Pre-terminations from a mixed basket of trade categories. Reasons for pre-termination varied, some due to headquarter issues, and others were terminating a few months in advance.

Outlook

Full impact of the circuit breaker (7 April to 1 June 2020) will be felt in 2Q20. Only c.25% of portfolio tenants were operating in April. Footfall in April during the circuit breaker was 40% lower as compared to in January 2020.

Tenant relief package

CMT has committed to $114mn (inclusive of property tax rebates) of tenant relief, which translates to 100% rental rebates for April and May for almost all retail tenants, and allowed tenants to use 1 month of security deposit to offset rents in March. On average, CMT collects 3 to 5 months of security deposit from tenants. The release of 1 month’s security leaves 2 to 4 months of security deposits as a safety net.

Leases with higher risk-sharing

Potentially more leases with higher profit-sharing and lower fixed components will be seen in the future. The COVID-19 situation has highlighted the vulnerable positions retail tenants are in, with their thin margins as well as the market’s expectation for landlords to have “more skin in the game”. In the near-term, CMT will exercise flexibility in their leasing strategy, which may mean shorter lease terms with higher risk-sharing.

The management commented that they are prepared to take on more risk-sharing and we have seen CMT employ this strategy with Funan, which has a comparatively higher number of tenants on lease structures with a larger GTO component. In the long run, higher risk-sharing may increase the demand for retail space as the lower fixed rents makes it more economically viable for new-to-market brands to give the brick-and-mortar model a go – 30% of Funan’s tenant are new-to-market brands.

Upgrade to BUY with lower TP of S$2.22 (prev. $2.70).

We lower our forecasts to reflect the rental rebates and weaker retail outlook. Our cost of equity assumption is raised by 105bps to 7.25%. The rental rebates will lower FY20e DPU by 14.2% - FY20e DPU is cut from 12.51cents to 10.78cents representing a DPU yield of 5.9%.

We upgrade our call to BUY on attractive valuations – P/NAV at 0.87x is attractive compared to the 1.09x to 1.29x range CMT has been trading at in the last 3 year.

The Positives

+ FY19 NPI grew 1.3% YoY on a comparable mall basis. Revaluation gains of S$17.6mn largely driven by better performance at malls – cap rates holding steady except for office component of Funan – cap rate compression of 10bps tied to tapering office supply.

+ Positive rental reversions of 0.8% for FY 19 amidst weak retail outlook and substantial supply. Rental reversions for FY19 were +0.8% over the initial signing rents (typically committed three years ago). Positive reversions ranging 0.4% to 3.5% were observed for all malls except RCS (-0.1%), CQ (-2.1%) and Bedok Mall (-6.5%).

+ Portfolio remained high at 99.3% as at 31 Dec 2019. Tenant retention was high at 83%.

The Negatives

- Falling tenant sales. Despite an improvement in shopper traffic (+1.4%), tenant sales for 1H19 fell by 1.3% (Figure 1). However, tenant sales psf/month for the top five trade categories that contributed >70% of gross turnover (GTO) income improved 1.0% in FY19. These were F&B (+2.9%), Supermarket (+1.2%), Beauty & Health (+0.9%), Fashion (-0.4%) and Department Stores (-5.3%).

What’s in the news?

Proposed merger of CapitaLand Mall Trust (CMT) with CapitaLand Commercial Trust (CCT)

CMT will acquire all the issued and paid-up units of CCT. The consideration for each CCT unit comprises 0.72 new units of CMT and S$0.259 in cash, resulting in an illustrative value of S$2.1238 per CCT share. The consideration implies a gross exchange ratio of 0.82x, based on the issue price of S$2.59 per CMT unit. The new entity, CapitaLand Integrated Commercial Trust (CICT) will be a proxy for Singapore commercial real estate, investing in retail, office or integrated development assets, with overseas developed market exposure capped at 20%.

The cash component will be paid using debt facilities. EGMs will be in May 2020 with targeted completion being June 2020.

What do we think?

We like it. We view the merger as a strategic and pre-emptive move that paves the way for accelerated growth. The proposed merger provides growth opportunities for CMT and risk diversification benefits for CCT that would have been challenging for them to achieve individually otherwise. To attain this magnitude of growth opportunity and risk diversification, both REITs must shed their old mandates – the proposed merger provides this opportunity. The merged entity will combine two champions in their respective asset classes, providing a solid foundation to unlock a myriad of scale-related advantages: Growth and Resilience.

Key benefits of the merger are highlighted in Figure 3.

Outlook

Retail rents bottomed out and started climbing in 2H19. Despite substantial supply coming onto the market in 2019, rents and occupancy showed marginal improvement. Better differentiation, active tenant management and retention will help CMT malls retain their attractiveness as retail space providers. We like CMT for the following reasons:

Balanced revenue from portfolio of 15 downtown and suburban malls - CMT’s earnings are backed by necessity spending at suburban malls, while enjoying exposure to the more discretional and tourism spending at central malls. Maintained consistently high portfolio occupancy of c.99%.

Willing and able to undertake redevelopment projects to create and unlock value – Funan reopening ahead of schedule on 28 June 2019. The redevelopment project cost S$360mn resulted in a mixed-use asset comprising a retail, office and hospitality (not part of CMT’s portfolio) components. Funan realized S$391mn in revaluation gains upon achieving TOP status in June 2018 and a further S$24mn in 4Q19. The redevelopment of Funan helped to refresh, strengthen and futureproof their portfolio. CMT’s track record and expertise as a mall operator is evident from their consistently high portfolio occupancy of c.98% in the last 8 years.

Superior Mall Management: Turning E-commerce threats into online-to-offline (O2O) opportunity – Competition from E-commerce will continue to vie for the same retail pie but CMT has created opportunity amidst struggle. CMT has been very active and in trying to embrace E-commerce players with their Taobao retail concept store at Plaza Singapura (Nomadx) and Funan. Their centrally located malls (Raffles City, Funan, Bugis, Plaza Singapura etc.), in addition to their loyalty program to increase customer stickiness (CapitaStar) makes CapitaLand malls good flagship store locations for e-commerce players who are looking to have and/or build an offline (physical) presence, starting with one central store and expanding via the CMT ecosystem.

Upgrade to ACCUMULATE with unchanged TP of S$2.68.

We upgrade CMT to ACCUMULATE. Our target price translates to a 4.9%/5.1% FY20e/FY21e distribution yield and an upside of 5.1%. Our TP does not include the effects of the merger. The merger will give CMT a new runway for growth and acquisition and allow the enlarged REIT to compete for or under take mixed-use redevelopments projects.

The Positives

+ Third quarter of positive rental reversions. Rental reversions for 3Q19 were +1.2% over the initial signing rents (1Q19/2Q19 +1.2%/+1.8%). Positive reversions ranging 0.4% to 3.4% were observed for all malls except RCS, CQ and Bedok Mall (-0.1 to -2.2%).

+ Portfolio occupancy improved 0.6ppts QoQ. Occupancy improved across all malls except for RCS (-1.0ppts) and Lot One (-0.6%, due to ongoing AEIs).

The Negatives

- Third quarter of contracting retail sales. Despite an improvement in shopper traffic (+1.3%), tenant sales for 1H19 fell by 1.3%, slightly worse off than 1Q19/2Q19’s -0.5%/-0.9%. However, tenant sales psf/month for the top five trade categories that contributed >70% of gross turnover (GTO) income improved 1.2% YTD. These were the F&B (+3.3%), Fashion (+0.4), Beauty & Health (+0.8%), Department Store (-5.9%) and Supermarket (+0.7%).

Ramp-up in occupancy at Funan’s office space is on track. Physical occupancy increased from 25% to 50% (as at 30 September 2019), with physical occupancy to reach committed levels (98%) by early 2020.

Retail sector outlook remains weak with the retail sales index excluding motor vehicles (RSI Ex. MV) in the red since the start of 2019 (Figure 2). CMT’s decline in tenant sales was persistently less pronounced than the fall in RSI Ex. MV (YTD -1.3% vs -1.8%1) (Figure 1).

Ongoing AEI and tenant rejuvenations are being carried out at Lot One to increase the space taken by the library and reconfigure the cinema layouts to increase the number of screens.

Maintain NEUTRAL with unchanged TP of S$2.68.

Our target price translates to a 5.4%/6.3% FY19e/FY20e distribution yield and a P/NAV of 1.35x.

The Positives

+ Better rental reversions albeit weaker occupancy. Rental reversions for 2Q19 were +1.8% over the initial signing rents (1Q19 +1.2%). Positive reversions were observed for all malls except Raffles City Singapore (RCS). The highest reversions came from Lot One (+5.6%), Westgate (+4.3%) and IMM Building (+4.2%). However, portfolio occupancy fell by 50bps QoQ from 99.8% in 1Q19 to 98.3% in 2Q19, contributed by CQ (-400 bps), Bedok Mall (-110bps), and IMM (-90bps).

+ Funan did not cannibalize RCS. Due to the different concept and tenant mix at Funan, the opening of Funan did not cannibalise RCS. Contrary, it increased the footfall at RCS.

The Negatives

- Weaker retail sales. Despite an improvement in shopper traffic, tenant sales for 1H19 fell by 0.9% YoY, slightly worse off than 1Q19’s -0.5%. Eight out of 14 trade sectors recorded negative growth with Home Furnishing (-22.4%), and IT & Telecommunications (-12.9%) and Electrical & Electronics (-9.8%) recording the worst contraction in sales. The weakness in these trade sectors was due to the softer property market and lengthening of the mobile device replacement cycle. We were comforted that tenant sales psf/month improved 1.2% YoY, and the top five trade categories that contributed >70% of gross turnover (GTO) income were the ones that registered growth in tenant sales. These were the Sporting Goods (+8.5%), Jewellery & Watches (+3.8%), F&B (+3.5%), Fashion (+1.6) and Shoes & Bags (+1.3%).

- Tampines and Bedok Mall cannibalized by Jewel; weaker tenant sales recorded. Since opening in April 2019, Jewel (owned by Sponsor, CapitaLand) has drawn crowds from the Tampines and Bedok Mall. As of 2Q19 (3 months after the opening), tenant sales for Tampines and Bedok Mall have settled at the c.-5% and c.-2%.

Outlook

Funan opened ahead of schedule, on 28 July 2019, with the occupancy of the retail mall in the 80%. Targeting at millennials, 30% of the tenants are new-to-market. More risk-sharing is expected as these new-to-market brands will negotiate for a higher portion (percentage) of variable GTO rent and lower base rent. Revenues will pick up in September 2019, where the majority of the office tenants are scheduled to move in.

7% of the leases by GRI are up for renewal in 2019, which highest lease renewals coming from RCS (17.1%), Tampines Mall (10%) and IMM Building (9.7%).

AEI and tenant rejuvenations are being carried out at J Cube and Lot One. It will commence in 3Q19. Estimate cost of AEI is c.$20mn and will increase the space taken by the library and reconfigure the cinema layouts to increase the number of screens.

Maintain NEUTRAL with higher TP of S$2.68 (prev. S$2.36).

We adjust our forecast to incorporate the revenues from Funan as well as reduced the risk-free rate owing to the lower interest rate environment – and in doing so, our cost of equity is reduced from 6.90% to 6.55%. Our target price translates to a 5.4% distribution yield and a P/NAV of 1.09x.