The Positives

+ Strong residential sales. Strong demand in China and higher ASPs lifted sales to RMB14.8bn, 12.1% higher YoY. This was despite a 3.2% decline in units sold: 5,100 in FY20 vs 5,268 in FY19. About RMB10.5bn of sales will be recognised from 2021 onwards. Units sold in Singapore were up by 5.3x HoH in 2H20 on the back of strong demand. This is expected to continue, backed by consumer confidence for residential products. Full year, a 10-week closure of showflats and an absence of new launches in Singapore at the height of the pandemic brought units sold to 220, 56% lower than FY19’s 501.

+ Record 14,200 keys signed. Despite an arduous year for the hospitality sector, CAPL’s predominantly long-stay serviced-residence platform signed a record 14,200 keys. This brought its total signed to 122,607 keys. Of these, 52,884 or 43% have yet to commence operations. In FY20, 3,900 units in 25 new properties came online, adding to fee revenue. Another 17,000 keys will become operational in FY21.

+ Sustained retail recovery, high occupancy. Shopper traffic and tenant sales in China and Singapore have slowly inched back to pre-COVID levels. Committed occupancy for retail, office and industrial was resilient at above 88.2%/85.0%/87.6% (Figs 1-3).

+ Active capital-recycling. Although markets were frozen for the most part of FY20, the group managed to hit its S$3bn divestment target. CAPL and its listed REITs divested S$3.04bn of assets (FY19: S$5.9bn), realising portfolio gains of S$154mn (FY19: S$436mn).

The Negative

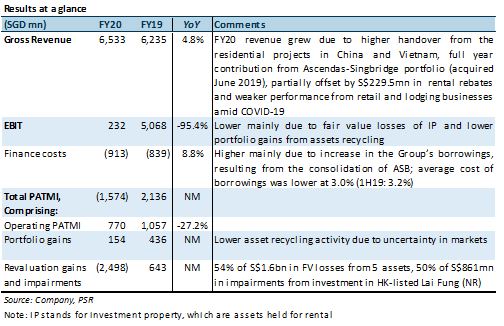

- Revaluation and impairment losses. A S$1.6bn downward fair-value adjustment represented 4.7% of the Group’s investment-property value. Five assets made up 55% of the revaluation losses. Newer assets such as CapitaMall Westgate, RCCQ and Jewel Changi Airport were opened between 2017 and 2019 and were still ramping up operations. As such, they were more affected by COVID-19 disruptions. Tianjin International Trade Centre and Ion Orchard suffered from a lack of MICE and tourist spending due to border closures. About 50% of the impairment losses were attributed to CAPL’s 20% stake in HK-listed Lai Fung (1125 HK, Not Rated). This investment was marked to market and written down as Lai Fung’s strategic direction has diverged from CAPL. CAPL is looking for buyers for its stake in this property company.

The Positives

+ Strong momentum in residential sales. Residential sales in China grew 40% QoQ to c.1,900 units. Singapore’s 3Q20 sales were three times the 35 units sold in 1H20. Handovers were on track in Vietnam, with their YTD value almost tripling from the same period last year.

+ Sustained recovery in Retail and Lodging. Tenant sales continued to improve, to 17% and 31% below pre-COVID levels in Singapore and China. Back in June 2020, they were 19% /42% below. Malls maintained their occupancy in the 87.9-99.8% range. Although reversions in Singapore were -4%, China’s reversions were positive or flat. In the Lodging segment, occupancy increased 40-50% QoQ while RevPAU improved 22% QoQ, but still down 52% from 2019 levels. Despite a longer recovery runway for the hospitality sector, CAPL signed 3,500 keys in 3Q20. This brought its YTD signed to 6,400 keys as franchisees and asset owners validate the value proposition and resilience of the service residence asset class.

+ Digitalisation gaining traction. CAPL’s digital retail ecosystem comprising CapitaStar, eCapitaMall and Capita3Eats have shown results in driving tenant sales. More than 2,000 tenants have been onboarded on the three platforms, up 25% QoQ. eCapitaVoucher sales in Singapore have increased by c.229% YTD. The 13mn CapitaStar members registered appear to underscore the success of its spend-and-be-rewarded strategy. Since the launch of Ascott Star Rewards (ASR) in April 2019, direct bookings and online revenue have grown by 35% and 20% respectively. This lifted margins as direct bookings cut out commissions payable to accommodation-listing platforms and promote brand stickiness. As CapitaStar points are fungible with ASR points, the digital ecosystem encourages cross-selling. This should further entrench CAPL’s position as a diversified real-estate juggernaut.

The Negative

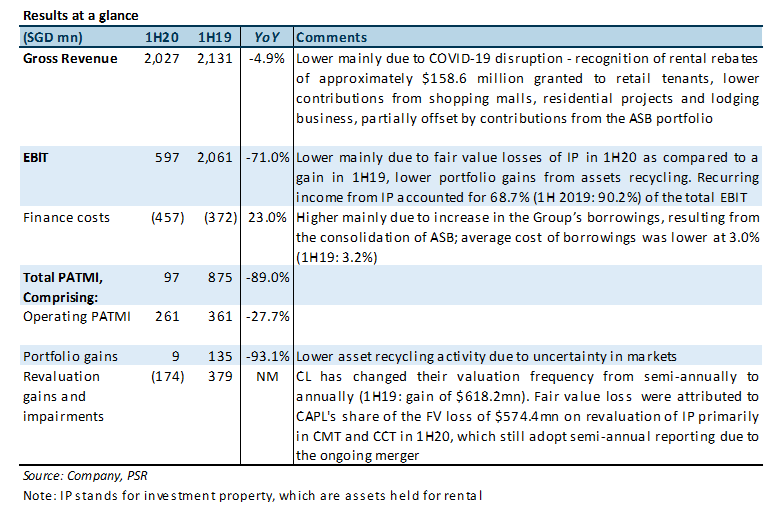

- Earnings and valuations hurt by COVID-19. 1H20 PATMI was down 89% YoY, arising from a subdued operating environment and lower-than-expected capital recycling. Market weakness will likely result in downward revaluations at year-end and impairment assessment for equity investments. CAPL’s FY20 financial performance could be materially affected. However, operations in 1H20 yielded positive cash flows and the impairments to come will have a bearing on profitability rather than cash flows.

Outlook

Momentum is strong in the development segment while leasing headwinds persist in the retail, commercial and industrial sectors. The recovery in hospitality is somewhat stunted, hinging on the vaccine timeline. CAPL is focusing on digitalisation to build stickiness and future-proof its portfolio, while conserving cash.

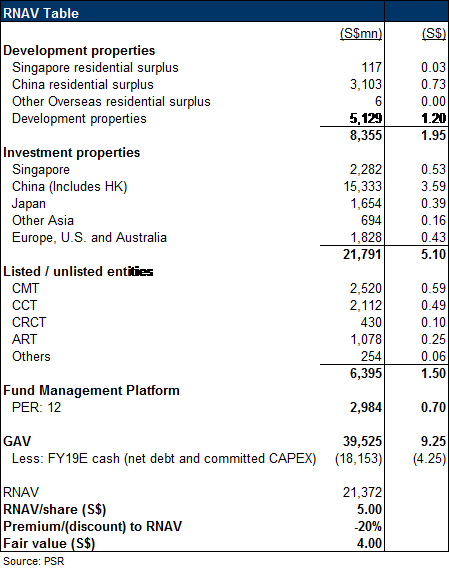

Maintain BUY and TP of S$3.82

No change in our estimates. Our TP remains based on a 20% discount to RNAV. CAPL is our top pick in the sector. Portfolio diversification and decades of experience in real estate should help it ride out near-term headwinds.

The Positives

+ Green shoots in China (42% of AUM) and Retail (28% of AUM) portfolio - Residential sales offices in China were progressively reopened in March. 1Q20's sales included the 288 units in La Botanica (Xi'an) that were sold out within 4 days of the 24 March launch date. Strong demand momentum continued in 2Q - all 528 units of La Botanica (Xi'an) and 194 units in Parc Botanic (Chengdu), which were launched in May, have been sold at pre-COVID average selling prices. Sell-through rate in China remains high at 92% of launched units, and on track to launch 4,000 more units in 2H20. Most FY20 handovers are expected to be delivered in the 2H20. While most countries are slowly emerging from lockdowns, 95% of office tenants and 89% of business park tenants in China have resumed operations in their premises. CAPL's core retail markets (China, Singapore, Japan and Malaysia) show evidence of recovery in footfall and tenant sales (Figure 1).

+ Opportunities to future-proof operations amidst adversity. The COVID-19 pandemic has accelerated CAPL's digitalisation initiatives for the retail and residential segment. The closure of non-essential trade impacted CAPL's retail and residential business. CAPL responded with virtual tours for leasing and residential projects, as well as the launch of its e-commerce (eCapitaMall) and online food ordering (Capita3Eats) platforms in June, which would not only help boost tenant sales, but also drive new business, and create an ecosystem for customer and tenant stickiness, future-proofing the retail segment.

+ Experienced, future-forward diversified real estate player. CAPL’s strategic investment in wholly-owned flexible workspace operator, Bridge+, will provide Core+Flex solutions in these times of changing occupier strategies (i.e. dedensification, flexible and scalable space needs). There are currently 9 Bridge+ locations operating in China, Singapore and India, with 20 more Bridge+ locations to be launched over the next 24 months. CAPL’s portfolio of complementary office and business park foot print across core geographies also allows CAPL to capture hub-and-spoke demand from tenants looking to average down the cost of space. While international travel bans put pressure on the lodging segment, CAPL’s predominantly service residence (SR) and rental housing portfolio has a lower breakeven occupancy and is geared towards long stays, which helps to provide a steady-state occupancy, mitigating the impact to the lodging portfolio (1H20 RevPAU: -43% YoY, occupancy: c.50%). Additionally, CAPL managed to sign 6,500 keys YTD, as investors validate the value proposition and resilience of the SR asset class.

The Negatives

- 1H20 EBIT -71% YoY, dragged down by lodging (-82.5%) and retail (-25.3%) segments. $300mn in rental waivers for retail tenants, containment measures and restrictions on travel and mobility has impacted these two segments the most. The lower EBIT was mainly attributable to fair value losses on investment properties in 1H20 as compared to a gain in 1H19, and lower portfolio gains from assets recycling. Despite a weaker operating environment, CAPL managed to generate $300mn net cash from operating activities. Balance sheet remains strong with $14bn in cash and undrawn credit facilities. Healthy take-up of script dividends scheme will also help to conserve $388mn in cash for the Group.

Outlook

Vietnam residential inventory running low, hampered by longer approvals process. CAPL has secured 3 to 4 projects in Vietnam. However, the longer approval process has stalled launches, hindering the Group’s ability to replenish the pipeline.

CAPL remains committed to their annual divestment target of S$3bn. Asset recycling activity in 1H20 has been muted in light of the uncertainty, which should pick up in 2H20 as markets stabilise and investment activity returns. CAPL’s strategy remains to divest non-core assets while achieving a more balanced asset distribution – CAPL may trim heavier asset classes such as retail (28% of AUM) and commercial (21% of AUM).

Maintain BUY with lower TP of S$3.82 (prev. S$3.94).

We trim our FY20e revenue by 2.1% as we factor in additional rental rebates and a longer than anticipated recovery in the lodging segment. Our TP, which is based on a 20% discount to RNAV, was cut by 3.0% from $3.94 to $3.82, after incorporating an enlarged share based from the script dividend scheme. We believe CAPL’s diversified portfolio and experience as a real estate player puts it in good position to mitigate near-term headwinds.

The Positives

+ Recurring income from fees and investment property to provide stable cashflow. Fund management income at $76.5mn was 54.2% higher YoY, due to the higher AUM (REITs and PR Funds) of $74.8mn post-combination with ASB.

+ Commercial and industrial segments resilient for now. These two segments make up 21% and 9% of FY19’s EBIT respectively and the number of tenants expected to require tenant support is far less compare to the retail tenants.

+ Strong balance sheet with S$13bn in cash and undrawn facilities. Net-debt-to-equity of 0.64x corresponds to c.S$2.4bn debt headroom. Currently, CAPL has no covenants attached to their loans, which the management credits to their strong position and good relationships. Lenders continue to keep credit lines open – CAPL managed to secure S$400mn by way of two bilateral green loans at lower rates, lowering the Group’s overall implied interest rate from 3.2% to 3.0%.

+ Robust recover in residential sales in China. All 288 units at La Botanical (Xi’an) were sold out withing 4 days after they were launch on 24 March 2020. Residential sales have picked up across China, since sales offices reopened, with units selling at higher prices than units in the same launch.

The Negatives

- Lodging and retail segments most impacted. The restrictions on travel and mobility has impacted these two segments the most. As at the end of April 2020, 52 out of a total of 485 properties owned or operated by the Group remained closed. The management commented that this is expected to put pressure on occupancy levels and RevPAU, which will in turn impact fee income for CAPL’s operated properties, and rental income for SR on CAPL’s balance sheet. Despite the long-staying clientele in SR, CAPL’s 1Q20 RevPAU’s fell 22%. 1Q20 shopper traffic fell by 10.8% and 52.0% YoY in SG and China.

- Vietnam residential inventory running low, hampered by longer approvals process. While the group remains positive on Vietnam’s outlook, the longer approval processes has hindered the Group’s ability to replenish the pipeline.

Outlook

The Group has elected to adopt half-yearly reporting and will be conducting valuations on an annual basis instead of semi-annually.

In China, all 15 malls that were closed during the nationwide lockdown in February have reopened. As at end-April, 85% of tenants have resumed operations. Trades that tend to draw crowds such as entertainment, cinemas and enrichment centres have not gotten the relevant approvals to commence operations. However, the Group has shared that shoppers are still cautious, and footfall has not recovered. In Singapore, c.25% of tenants categorised as essential services remain open during the circuit breaker period (7 April to 1 June 2020).

The development segment experienced delays in construction timelines and an absence of sales due to closure of showrooms during the lockdown period. In Vietnam, domestic and international travel restrictions have resulted in delays in handovers as buyers are prevented from finalising documentation.

Revaluation risk may arise in this uncertain environment. While CAPL’s strong cash position means that the Group is not under any pressure to liquidate assets, lower asset values may reduce the pace of capital recycling. Instead, the management is on the lookout to pick up counter-cyclical assets or assets/businesses at good valuations. However, CAPL remains committed to their annual divestment target of S$3bn. To date the Group has made gross investments of S$447mn and gross divestments of S$373mn.

Maintain BUY with lower TP of S$3.94 (prev. S$4.20).

We lower our FY20e revenue by 14.1% as we factor in the lower earnings from the rental rebates offered and weaker lodging revenues. Our TP, which is based on a 20% discount to RNAV, was cut by 6.2% from $4.20 to $3.94, after incorporating the lower revised valuations for the REITs.

The Positives

+ Surpassed gearing target of 0.64x ahead end-2020 timeline. CAPL divested S$5.9bn worth of assets (double the S$3bn FY19 target), achieving net debt/equity of 0.63x as at end-2019. This affords the group a debt headroom of S$13.1bn (in cash and undrawn debt facilities) to redeploy capital. 64% of divestments were injected into listed REITs/BTs, which will grow AUM in the fund platform. CAPL maintains a divestment target of S$3bn for FY20.

+ Sold 5,268 units with sales value worth RMB13.2bn in FY19. This compares to the 4,938 units worth RMB12.5bn sold in FY18. The group estimates c.RMB10.1bn worth of units will be handed over and 7,000 units will be released for sale in 2020.

The Negatives

- Vietnam residential inventory running low, hampered by longer approvals process. While the group remains positive on Vietnam’s outlook, stricter approval process is an impediment to replenishing land bank and getting project approvals.

Outlook

We expect FY20e to be another active year for CAPL. With a stronger balance sheet and weaker economic environment, we think CAPL will use the opportunity to pick up assets at better valuations and at the same time shed non-core assets. With the group’s 160K keys under management target, S$100bn AUM ambitions for the fund management platform, redevelopment opportunities in SG and plans to deepen its presence in India and Vietnam, we see sustainable growth for CAPL.

The group will be shifting to half-yearly reporting and conducting valuations on an annual basis instead of semi-annually.

Impact of Covid19

Currently, 12 out of 48 malls in China are still closed. Residential sales were affected due to government mandated closure of showrooms due to the Covid19 situation. Showrooms have since reopened and sales momentum is picking up.

CAPL’s lodging platform of predominantly serviced residence assets and are less affected by the Covid19 than full-service hotels, due to the 70-80% corporate-driven, longer-staying clientele. Average occupancy in Singapore is c.70% while occupancy in China ranges 50%-70%. This compares to the occupancy of 10%-50% for hotels.

Footfall at SG malls fell by 50% after the DOSCON was upgraded to orange. It has since improved to -5% pre-Covid19 levels. Despite this, gross turnover for Jan20 was in line with FY19, with suburban malls experiencing better footfall and sales.

Maintain BUY with unchanged TP of S$4.20.

We remain positive on CAPL and maintain our BUY with an unchanged target price of S$4.20. Our target price translates to a FY20e P/NAV ratio of 0.75x and an total return of 22.1%.

We attended CapitaLand’s Investor Day on 29 November 2019 where the group’s management shared the strategy for growth, echoed their value-driven investment evaluation process and addressed some of the questions from investors and analyst. The key takeaways from CapitaLand Investor Day 2019 are:

2019 has been a monumental year for CAPL. We witnessed the merger of CAPL with Ascendas Singbridge (ASB) which was completed in June. The merger brought with it:

CAPL achieved their 2019 divestment target of S$3bn, which is aimed at helping the group lower post-ASB acquisition gearing of 0.73x to 0.64x by end-2020. CAPL divested S$5.9bn in non-core assets, S$3.8bn of which were to their REITs and funds, bringing the total effective divestments to S$4.9bn as at 21 November 2019.

Scale, focus, balance and agility are the four key pillars underpinning their strategy.

Questions regarding how CAPL will deploy capital and evaluate investments in new markets were answered with the same underlying message: CAPL will focus on value creation, play to their strategic advantages, while considering the risk-return profile and maintaining agility.

CAPL will deploy capital in areas where they have presence in, or when considering investments in new territories or verticals (eg: data centres), they will do so only if they can achieve a meaningful scale for relevance and influence. The key geographies of focus for the respective business segments (development, fund management and lodging) have been identified, and they will seek to utilise their strategic advantage to create and unlock value.

With sustainability, stability and risk management as key considerations, CAPL will maintain the 50-50 spilt between Developed and Emerging Markets when allocating capital. Lowering gearing from the current 0.69x to 0.64x is one of the key targets as this would afford CAPL the flexibility and agility to seize opportunities.

Traditionally thought of a real estate developer and manager, CapitaLand has grown other segments of the business such that the development portion only accounts for <20% of EBIT. >80% of EBIT is derived from recurring rental income from Investment Properties, providing greater income stability and visibility across cycles.

3 Growth Engines:

I. Development: Core Markets Play

CAPL’s development business will be focused in the four key markets where they have an established track record and see growth potential - Singapore, China, Vietnam and India. The group has more the 25 years of operational track record in these territories.

Key competitive advantages and strengths by market:

Singapore: Growth and redevelopment opportunities within existing portfolio

China: Business Park, Industrial and Logistics portfolio added by ASB further differentiates CapitaLand China from peers.

Vietnam: First mover advantage in a developing country with favourable macroeconomic characteristics (strong GDP growth, ongoing urbanisation, growth in educated upper and middle-income groups, township and commercial development opportunities)

India: Riding on the global digitalisation trend through the world’s largest IT sourcing destination

II & III. Fund Management and Lodging Platform to provide recurring fee income

The fund management platform and CAPL’s Lodging Platform are the two engines driving recurring fee income and are essential to achieving the 10% ROE target. CAPL earns fees from the management of the asset in the various REITs and private funds, as well as management contract fees from management of service residences franchised under the Ascott, Citadines, Somerset and Lyf brands.

Maintain BUY with unchanged TP of S$4.20.

Our target price translates to a FY19e P/NAV ratio of 0.75x.

The Positives

+ Deleveraging on track. Post CAPL-ASB combination gearing reached a historical high of 0.73x (FY17/FY18 0.49x/0.5x), in line with management expectations. The management has set forth a plan to deleverage to 0.64x net debt/equity by end-2020 through their annual asset recycling target of S$3bn. Total divestments for 1H19 reached S$3.4bn, of which $1.2bn have been completed. CAPL is on track to reach their 0.64x gearing ahead of the end-2020 target. Divestments net of investments, on an effective-interest basis, for YTD 8M19 was $1.2bn. Capital recycling efforts have unlocked $135mn ($171mm excluding ABS-related transaction costs of $36mn) in capital gains.

+ NPI-growth driven revaluation gains. 2Q19 revaluation gains contributed $346.5mn (60%) to total PATMI, however these revaluation gains were operationally driven - 10 properties of the properties (Figure 3) accounted for c.58% of the revaluation gains reported higher NPI yields. Average portfolio NPI yield for 1H19 was 4.5%, an increased from 4.2% in FY18.

The Negatives

- China sell-through rates for units launch in 2Q19 deteriorated to 80% (1Q19 c.90%). However, overall sales rate remained healthy at 93% of all launched units and management commented that the demand from upgraders and first-time owners is still strong. CAPL strategy to pace their launches to wait out the easing of price caps has yielded 19% QoQ increase in sales price for 2Q19.This is after the 53% QoQ growth in sales price in 1Q19. On a half-year basis, units sold and sales values were 73% and 31% higher YoY.

Outlook

The outlook is positive. The gradual relaxation of the price caps in China has yielded 53%/19% QoQ increase in sales price for 1Q19/2Q19. We remain optimistic about the remaining 3,078 units to be launched in 2H19.

In Singapore, CAPL achieved healthy sell-through rates of 72.5% (or 27% of total project) at the launch of One Pearl Bank in July 2019 and will be launching the Sengkang Central mixed-use development (JV with CDL) in 3Q19.

CAPL’s recurring income portfolio continues to be grounded on healthy operating metrics and will increasingly be the bedrock of its earnings. The merger with ASB increased the number of private funds from 17 to 23. Fund assets under management grew 28.1% from S$55.1bn to S$70.6bn.

The signing of c.7,100 keys YTD19 brings the number of keys under management to 107,154. If the signing momentum persists, CAPL’s Lodging segment will be on track to achieve its 160,000 key target by 2023. The Lodging segment made up 14.4% of 1H19 EBIT ($291mn/$2,061mn), of which 41% ($118mn) was attributed to recurring fee income from management contracts. Currently, 44% (47,480 units) are still under development and do not contribute fee revenue. We expect the Lodging segment to play an increasingly important role in supporting CAPL’s recurring income and as more units come online. The management previously guided that upon stabilisation, every 10,000 keys will generate c.S$25mn of fee income.

Apart from the potential redevelopment of Liang Court, together with CDL and the two listed trusts, ART and CDLHT, CAPL mentioned that the group will be looking into the possible rejuvenation of the industrial assets in the Jurong area.

Upgrade to BUY with higher TP of S$4.20 (prev. S$4.00).

We update our forecasts to reflect the incorporation of ASB and raise our TP to S$4.20. Our target price translates to a FY19e P/NAV ratio of 0.75x.

The Positives

+ Lodging segment shining with resilience. CapitaLand Lodging was the sole segment that reported YoY growth for both revenue (+14.4%) and EBIT (+328%), mainly on the back of higher revenue from Synergy Global Housing and contribution from Tauzia (acquired in 3Q18). EBIT from this segment was propped up by gains from the divestment of Ascott Raffles Place Singapore in Jan 2019. Excluding this one-time gain, EBIT from this segment would still have risen c.31%. In addition, The Ascott Ltd had in April secured 14 contracts to manage over 2k units across eight countries and is on track to achieve its targeted 160k units by 2023 (YTD 2019: 101.5k).

+ Solid sales for China projects. Projects launched in 1Q19 achieved a high sell-through rate of c.90%. It sold out the launches of Chengdu Century Park (East) (99% sold) and La Botanica developments (fully sold), with the latter only being launched in March 2019. >5k units are to be ready for the rest of 2019, with more than a quarter coming from the La Botanica development alone.

The Negatives

- Lower handover of units this quarter due to timing differences. 1Q19 saw lower handover of units for both Singapore and China. To juxtapose, 1Q18 saw significant completion of a phase from The Metropolis in Kunshan – which comprised c.85% of the units handed over that quarter. We note that these are just timing differences and the Group is still on schedule for the completion and handover of existing projects in China. The Management communicated that bulk of the units handover will be back-ended into 2H19.

Outlook

Outlook is positive. Healthy momentum is still expected to persist for the 5.2k residential units expected to be launched for the rest of the year. There had been a recent easing of residency requirements in China (also known as the hukou system), with certain cities encouraged to scrap the system altogether or to lower the requirements. CAPL’s Management expects a gradual relaxation of the price caps in light of this, albeit in a gradual and controlled manner.

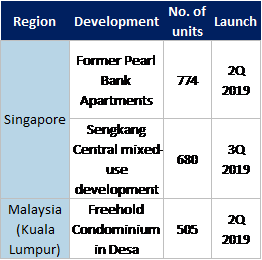

In Singapore, CAPL is set to launch the former Pearl Bank Apartments development in 2Q19 and the Sengkang Central mixed-use development in 3Q19. The Group also has a development in Malaysia launching in 2Q19. Residential launches in Vietnam on the other hand are likely to see a slowdown due to initial curbs from certain new Government policies – where approvals for new developments will likely also see delays. However, the Management clarified that demand is still robust for Vietnam residential and much of the units handover will be back-ended into 2H19.

CAPL’s recurring income portfolio continues to be grounded on healthy operating metrics and will increasingly be the bedrock of its earnings. Its fund management platform had been bearing fruits – in April, the Group successfully set up its maiden discretionary equity fund, CapitaLand Asia Partners I (CAP I), which would invest primary in value-add and transitional pan-asian commercial assets. CAP I secured US$391.3mn (c.S$528.3mn) for its first closing. During the quarter, the Group also launched its first discretionary real estate debt fund, CREDO I China, which will invest in offshore US dollar-denominated subordinated instruments for real estate in China’s first- and second-tier cities. CREDO I China has to-date raised 70% of the target capital raise of US$750mn (c.S$1bn) – CapitaLand has a 10% stake in this fund.

Figure 1: CapitaLand's upcoming project launches in Singapore and Malaysia

Maintain Accumulate with unchanged TP of S$4.00

We maintain our Accumulate rating with an unchanged target price of S$4.00. Our target price translates to a FY19e P/NAV ratio of 0.78x.

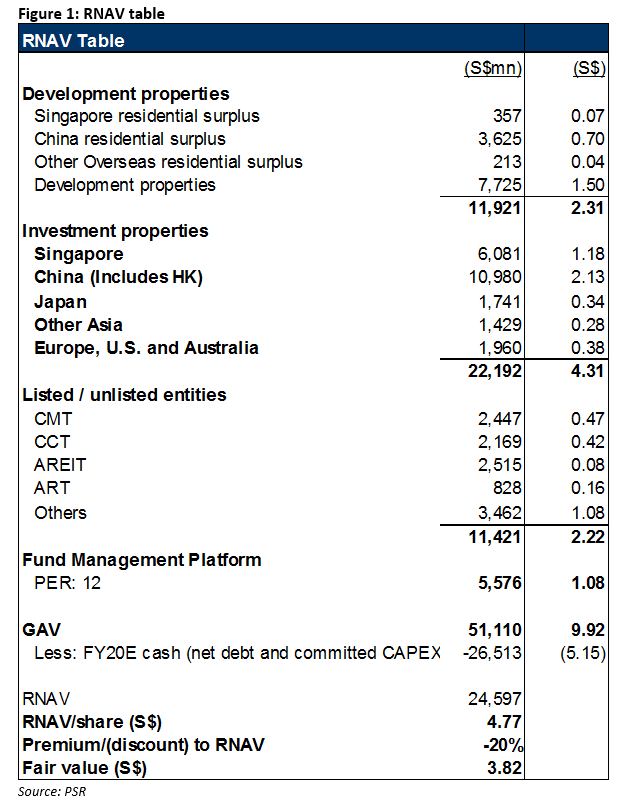

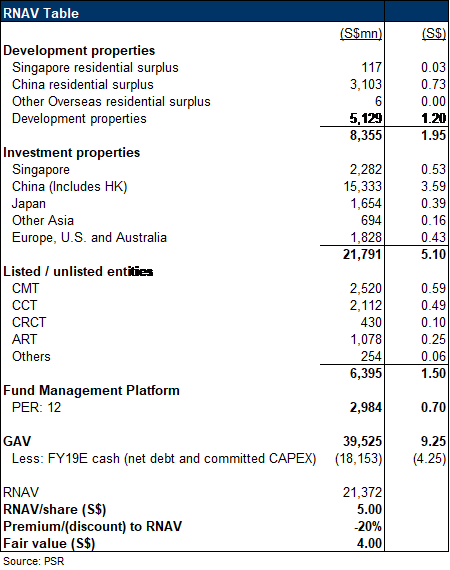

Figure 2: RNAV Table

Our RNAV figures do not include components that would arise from the proposed acquisition of Ascendas-Singbridge (ASB).

The proposed acquisition of ASB was approved by its shareholders at an EGM held on 12 April 2019. Subject to obtaining regulatory approval, the acquisition is expected to complete by 30 June 2019.

The Positives

+ Stable portfolio occupancy and higher tenant retention rate. Stable occupancy across the portfolio. Full occupancy was maintained at Tampines Mall despite the opening of Jewel in April 2019. Tenant retention was also higher at 88.9% (1Q18/4Q18: 82.3%/82.9%).

+ Funan pre-leased at 90% occupancy. Notwithstanding an initial fitting-out period of 3-6 months, Funan is expected to contribute to CMT from 2H19 onwards. The retail and office components of Funan are currently 90% leased (4Q18: 80%). Media reports revealed that various government bodies have leased office space at Funan. The Ascott Ltd’s lyf-branded serviced residence at Funan is also expected to commence operations in 2020.

The Negatives

+ Still-weak rental reversions. Despite an improvement from the average 0.8% rental reversion achieved in FY18, the 1.2% reversion in 1Q19 is lagging behind that of its peers such as Starhill Global REIT and Frasers Centrepoint Trust. Tenant sales also slid 0.5% YoY in 1Q19, dragged down by a wider mix of trade categories than in 1Q18.

Outlook

IMM (second biggest contributor by GRI) had its lease renewed for another 30 years on 23 Jan 2019 (initial 30+30 year lease from 23 Jan 1989). With the Jurong Lake District shaping up under the URA’s Draft Master Plan 2019, we not only expect reversions at this asset (as well as Westgate) to trend up going forward but for a progressive valuation uptick. The re-commencement of operations at Funan is expected to progressively improve portfolio operational metrics.

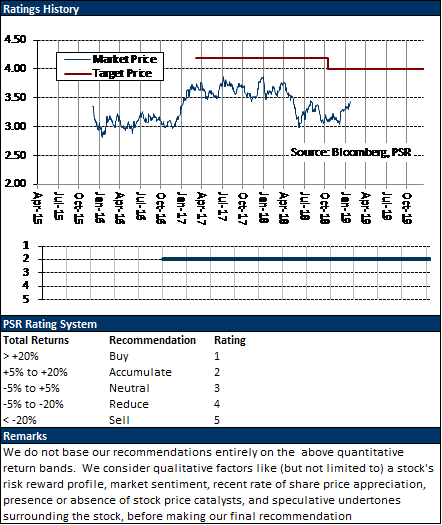

Maintain NEUTRAL with higher TP of S$2.21 (prev S$2.09).

We adjust our target price to reflect a lower cost of equity. Our target price translates to a 5.4% distribution yield and a P/NAV of 1.06x.

The Positives

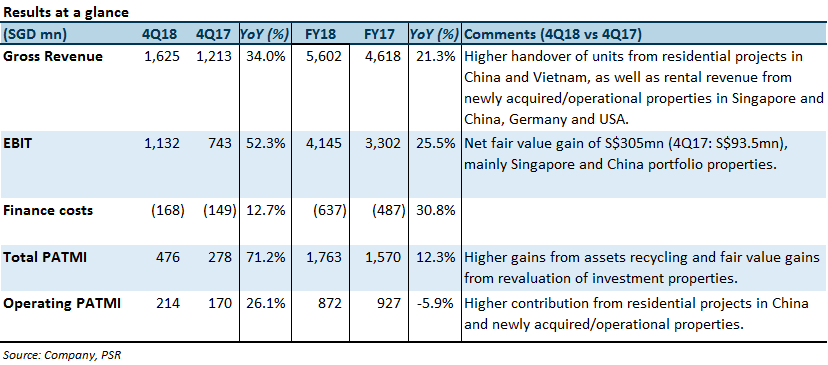

+ Strong bump-up in China residential sales. >85% take-up rate for all launches in 4Q18 – fully selling out the quarter’s launch for Parc Botanica in Chengdu. It was indeed a stronger quarter for the China residential segment, as was previously guided by the management. 4Q18 saw close to 2x sold units and sales value than in the same quarter last year. China residential sales was lower on a full-year basis due to the lower inventory available and delay of certain launches due to the property cooling measures.

+ ROE increased for third year running. ROE of 9.3% was achieved in FY2018, notably from the revaluations and impairments. Stripping out the gains from the sale of The Nassim units in 1Q17, FY18 operating PATMI would have increased 14% YoY, potentially tipping overall ROE levels closer to double-digit range – which is the Group’s eventual goal. ROE level could be further built up from its recurring income stream as well as fees from its private funds – which will receive a boost from Ascendas-Singbridge (ASB) (assuming a successful acquisition of them by CAPL).

+ Operationally healthy on all fronts.

Retail: On a same-mall basis, tenant sales across all geographies continued to record positive growth YoY in FY18.

Office: China – 92% occupancy for matured projects with average rental reversion of +4% for FY18. Singapore – above 99% committed occupancy, well above market committed occupancy of 95% with rents holding steady.

Lodging: FY18 RevPAU increased +4% YoY on a same-store basis, driven largely by Europe (+12%), Singapore (+11%) and China (+5%).

The Negatives

- Certain new launches in China still to be deferred due to cooling measures. CAPL had previously deferred several launches due to ongoing cooling measures and restrictions in selling prices across certain projects.

Outlook

Outlook is positive. Healthy momentum is expected to persist for the c.7k units expected to be launched this year. While the main hurdle now is the persistent delay in the launches for the China residential segment (its largest development portfolio), we understand that margins would still be a healthy double-digit figure for all existing projects even if taking into account the current price caps. CAPL’s recurring income portfolio has been grounded on healthy operating metrics and is expected to increasingly be the bedrock of its earnings.

Going forward, the anticipated acquisition of ASB will bring in new geographies and new business verticals for CAPL, further boosting its recurrent income portfolio and moving well towards its targets of 20/80 development/investment properties and 50/50 emerging/developed markets.

Deleveraging of S$3bn will be the next step to whip CAPL’s balance sheet back to a 0.64x leverage ratio (pro-forma: 0.72x) by the Group’s targeted Dec 2020 – this is where we could see more asset recycling.

Maintain Accumulate with unchanged TP of S$4.00

We maintain our Accumulate rating with an unchanged target price of S$4.00. Our target price translates to a FY19e P/NAV ratio of 0.75x.