The Positives

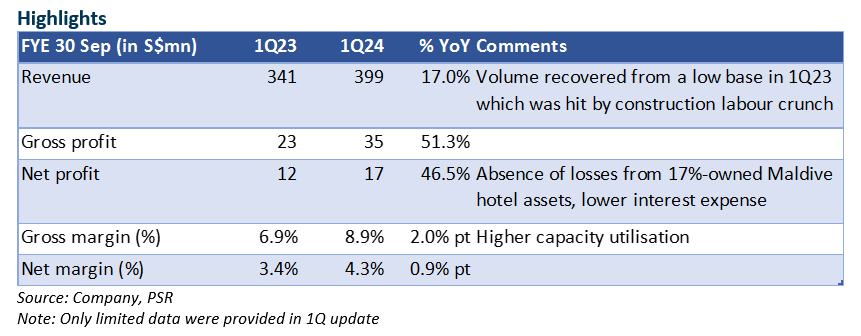

+ 1Q24 net profit surged by 46.5% YoY, on the back of volume recovery from a low base in the year earlier, the absence of losses from the 17%-owned Maldives hotel assets, and lower interest expenses. We estimate that steel prices were about 17% lower YoY.

+ Gross margin was 2.0% points higher YoY, which reflects a higher utilisation rate at its fabrication plant and possibly lower freight costs.

+ Net debt at end-Dec 23 of S$207mn was flat versus S$196mn at end-Sep 23, despite the jump in sales, suggesting still healthy working capital and no collection stress. Lower steel prices also free up trade financing needs. Net gearing as at end-Dec was 0.46x.

The Negative

- nil

The Positives

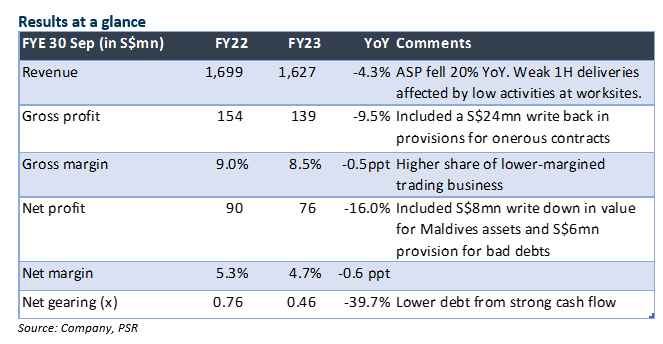

+ Revenue and net profit rebounded in 2H23, after a weak 1H when sales of steel products were curtailed by safety rules imposed at construction sites. 2H23 revenue and net profit were flat YoY, despite the ASP decline of 27% YoY (our estimate), implying strong volume recovery.

+ Gross margin was lower (-0.5% pt to 8.5%) due to higher share of lower-margined trading business (25% of revenue). We expect it to recover to 9% in FY24e when fabrication and manufacturing volume rises. Demand for steel products remains strong. BRC’s orderbook of S$1.3bn is underpinned by mainly public sector projects.

+ Net gearing improved to 0.5x (Sep 22: 0.8x) from strong operating cash flow. EBITDA to interest expense improved to 1.5x (FY22: 2.3x).

The Negative

- nil

Outlook

Net profit growth is expected to resume with a stable ASP and stronger order deliveries. Construction demand is expected to remain robust, led by public housing, record government land sale programmes and infrastructure projects.

Maintain BUY with unchanged TP of $1.99

BRC trades at an attractive 8.9% dividend yield and 1x P/B for FY24e.

The Positives

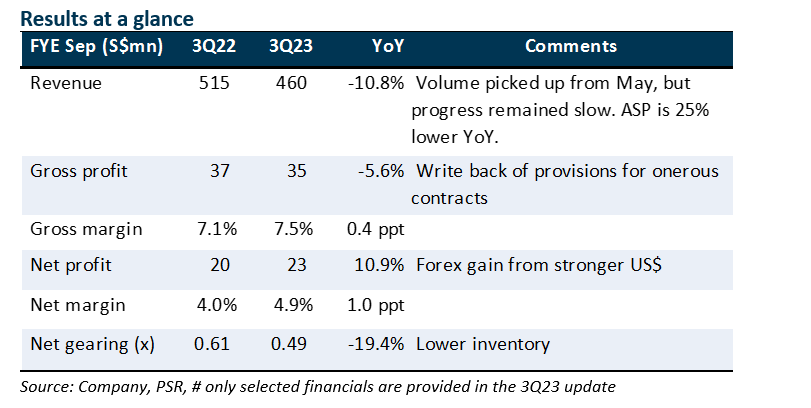

+ Volume and construction activities picked up from May (>2x higher MoM), though they are still below pre-COVID levels. Construction progress is hampered by the shortage of dormitory beds, workers and step-up in safety enforcement on worksites and construction personnel. Demand, however, remains robust, underpinned by public housing, record government land sales for private housing, and infrastructure projects. BRC has an orders on hand of S$1.34bn.

+ BRC is largely insulated from potential bad debts through credit insurance. Some construction companies are facing financial stress due to lower-margin legacy projects, project delays and rising costs. For BRC, the impact is non-delivery/cancellation of outstanding orders, but there is no collection risk for jobs that have been delivered.

The Negative

- Net margin remains low at 4.9%. We think margins might not return to FY22’s 5.3% due to higher share of trading business which are lower-margin, and large-scale infrastructure projects.

The Negative

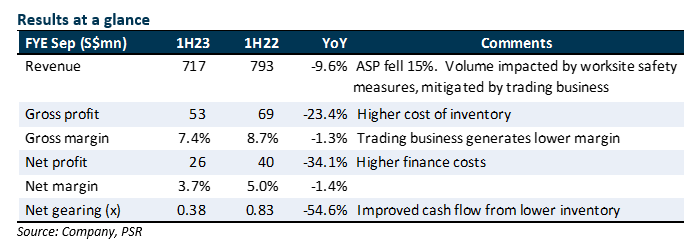

- 1H23 earnings came in at only 31% of our FY23e estimates. The shortfall was due to lower order deliveries, which was impeded by low construction progress at work sites to meet heightened safety measures. The measures are mandated to last till end-May, but activities are picking up with improved safety conditions. BRC booked more lower-margined trading businesses during the period, and gross margin fell 1.3% pt to 7.4%. Interest costs rose 170% YoY to S$6.3mn, resulting in 34.1% YoY decline in 1H23 net profit.

The Positives

+ Net gearing improved to 0.38x (Sep 22: 0.76x). With easing of steel prices and freight costs, inventory holdings were brought down. Credit terms from suppliers become more favourable, leading to strong operating cash inflow of about S$0.608/share.

+ Orderbook edged higher to S$1.42bn (Sep 22: $1.4bn), as demand remains robust. BCA estimates that progress payments, which represent work done and revenue booked, to grow by 9-20% in 2023. We estimate about 60% of the orderbook are for jobs in the public sector which are less volatile and payments are more certain. While the delay in construction work had affected cash flow and credit conditions of some contractors, we do not see any risk of default that could impact building material suppliers.

The Negatives

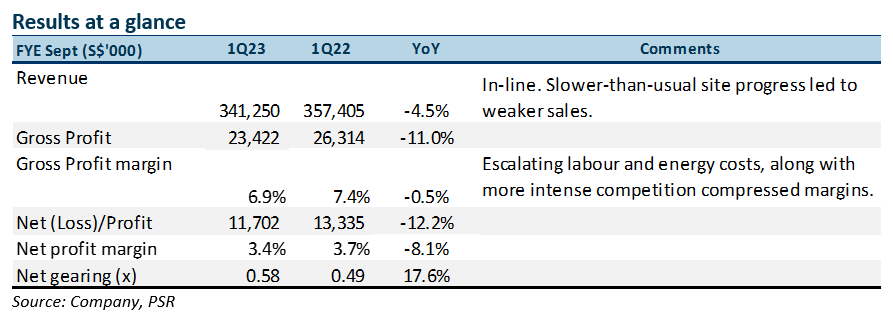

- 1Q23e earnings below expectations, at 11% of our estimates. Revenue was in line with our estimates, as we accounted for a seasonally weak 1H23 that was further weighed down by the Heightened Safety period that was in place. Margins however, were ~1% below our estimates as escalating costs, particularly for labour and energy weighed along with more competition for new contracts, as the industry competed to overcome the shortfall in delivery volumes.

- Heightened Safety period extended by another three months. As a result of the Heightened Safety period imposed by the MOM, local construction projects are, in general, progressing slower than expected. The time-outs and punitive measures imposed on the sector have slowed construction progress. We expect the Heightened safety period to continue to weigh on earnings for 9M23 after the MOM extended the Heightened Safety period by another three months till end-May.

The Positive

+ Construction order book remained healthy at $1.4bn (vs $1.4bn in 4Q22), above our $1.35bn estimates. Strong demand for public housing and infrastructure projects in Singapore continued to boost the Group’s order books. BRC Asia is benefitting from the backlog of projects that were postponed during the Covid-19 pandemic and the higher number of public housing projects that are being launched to meet demand. The construction sector is also recovering at a faster pace with 4Q22’s growth at 10.4% YoY vs 7.8% in the preceding quarter. We estimate that half of its order book will be fulfilled within the next 15-18 months.

The Positives

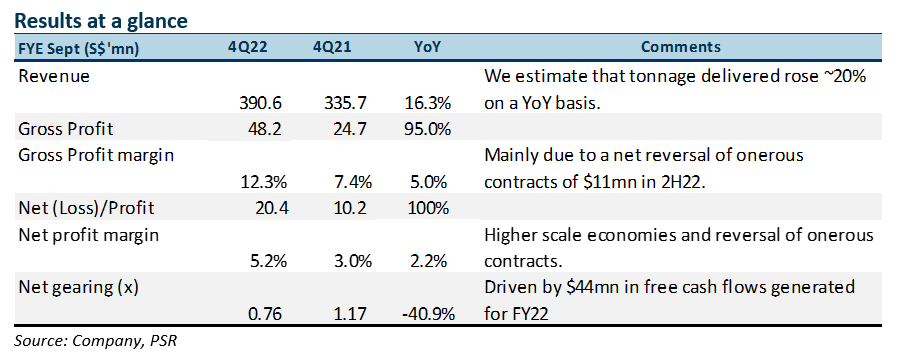

+ FY22 net profit ahead of our expectations at 112% of our FY22e forecasts. Revenue was in line at 99% of FY22e. Earnings were above expectations as higher-than-expected volume moved despite the “Heightened Safety” period imposed by the Ministry of Manpower (MOM) from 1 Sept to 28 Feb 2023. The measures were announced after a spate of workplace fatalities since the start of the year prompted the MOM to intervene in the sector.

In view of its strong results, the Group has declared a total of 12 cents of dividends (~55% payout), comprising 6 cents final and 6 cents special dividend to reward shareholders. FY22 dividends of 18 cents represents a dividend yield of 9.8%, exceeding our 16 cents estimate.

+ $11mn net reversal for onerous contracts made. With steel rebar prices declining ~20% in 2H22, the Group benefitted from $11mn of write-backs in onerous contracts. For FY22, the Group generated a net reversal of provision of onerous contracts of $12.8mn. Correspondingly, GP margins improved 500bps for the period.

The management has guided for further reversals in onerous contracts for FY23 should steel prices remain at these levels.

+ Construction order book grew to $1.4bn (vs $1.135bn 3Q22), above our $1.2bn projections. Strong demand for public housing and infrastructure projects in Singapore continued to boost the Group’s order books. BRC Asia is benefitting from the backlog of projects that were postponed during the Covid-19 pandemic and the higher number of public housing projects that are being launched to meet demand.

The Negatives

- Construction site activity levels adversely affected by workplace fatalities and dengue. As of 1 Sept 2022, the number of workplace fatalities stands at 36 for whole of 2022, up from the 28 workplace fatalities reported for the first six months of 2022, many of which were in the construction industry. As a result of the Heightened Safety period imposed by the MOM, local construction projects are, in general, progressing slower than expected. The time-outs and punitive measures imposed on the sector has slowed construction progress.

The Positives

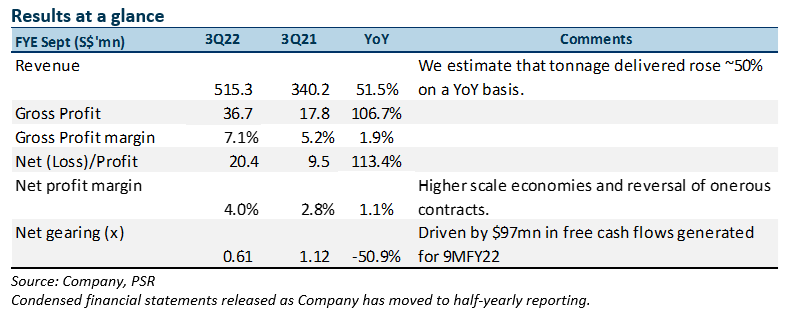

+ 9MFY22 revenue and net profit was in line with our expectations at 75%/75%. Net profit rose 113.4% YoY driven by the continued recovery in the construction sector and the moderation of steel prices. We estimate that volumes grew ~30% YoY in 3Q22, driven by the increase in work activity at construction sites. According to the Ministry of Trade and Industry (MTI), the local construction sector grew 3.8% in the second quarter, faster than the 1.8% growth in the preceding quarter. This was in part due to the relaxation of border restrictions on the inflow of migrant workers.

+ Net reversal for onerous contracts made in 3QFY22. Steel rebar prices declined ~6% during the period. We believe the Group benefitted from write-backs in onerous contracts in the latest quarter with steel prices moderating. Recall that for 1H22, the Group benefitted from a $1.8mn net reversal for onerous contracts as contracts were being fulfilled with steel rebar prices down 13.6% during that same period. The Group generated $69mn in free cash flows in 3QFY22, that was used to lower gearing to 0.61x from 0.83x in 1H22.

+ Construction order books inched up slightly to $1.135bn (vs $1bn 2Q22). Strong demand for public housing and infrastructure projects in Singapore continued to drive up the Group’s order books. BRC Asia is benefitting from the backlog of projects that were postponed during the Covid-19 pandemic and the higher number of public housing projects that are being launched to meet demand.

The Negatives

- Construction site activity levels adversely affected by workplace fatalities and dengue. In the first six months of 2022, the Ministry of Manpower (MOM) reported 28 workplace fatalities, many of which were in the construction industry. This led to a call for companies to conduct a safety time-out on 9 May 2022. In addition, in 1H22, more than 12,000 cases of dengue cases were reported, far exceeding the 5,258 cases logged in the whole of 2021. This resulted in a spate of stop-work orders issued by the authorities to construction sites, which impeded construction progress.

Outlook

Construction sector continue to see faster pace of recovery in 2Q22; increase in activity for rest of 2022 expected. The Group’s order book inched up to $1.135bn from $1bn as the construction sector continues its recovery. We estimate that half of its order book will be fulfilled within the next 12-15 months.

According to the MTI, in absolute terms, the value-add of the sector is still below its pre-pandemic level, but improved to 23.7% from 25.3% as activity at construction worksites continued to be weighed down by labour shortages. Despite this, we see the labour shortage situation easing with the relaxation of border restrictions and remain positive on the outlook for the sector.

HDB has announced that it will ramp up the supply of new build-to-order (BTO) flats over the next two years to meet the strong housing demand from Singaporeans. It plans to launch up to 23,000 flats per year in 2022 and 2023, which represents a significant increase of 35% from the 17,000 flats launched in 2021. Changi Airport’s Terminal 5 project will resume after being put on hold for two years due to the Covid-19 pandemic.

With an approximately 65% market share in the reinforced steel industry, we continue to see BRC Asia as a key beneficiary of the construction sector recovery.

The Positives

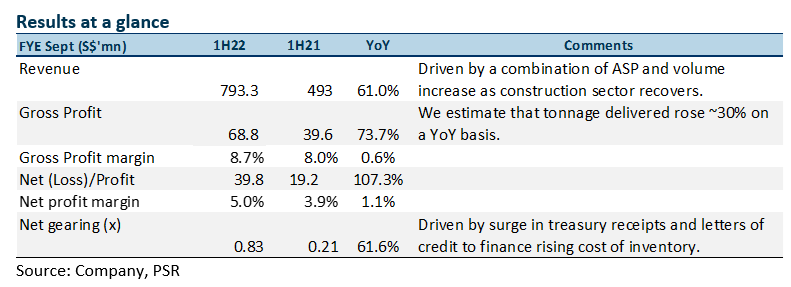

+ 1HFY22 revenue and net profit exceeded our expectations. We estimate that order deliveries went up ~30% YoY as activity levels at project sites escalated in the last few months. As Singapore started to relax foreign labour restrictions, the influx of foreign workers – estimated at 15,000 – started to gather pace and has resulted in activities in the construction site picking up.

On the back of its strong set of half-year results, the Group has declared an interim dividend of 6 Singapore cents for 1HFY22, 2 cents higher than for the same period last year, signaling the management’s confidence in the near-term outlook of the Group.

+ $1.8mn in net reversal for onerous contracts made in 1HFY22. The Group benefitted from a $1.8mn net reversal for onerous contracts in 1H22 as contracts were fulfilled, though this was offset by additional provisions made for deliveries beyond the period. With the steel rebar price having risen 18% to S$1,300 per tonne since the start of the geo-political conflict in Ukraine in February this year, we expect provisions for onerous contracts to remain elevated for FY22e and FY23e.

+ Provision for impairment loss on trade receivables fell over 60% on a YoY basis in 2QFY22 aided by the recovery of the construction sector and government support. The local construction sector’s growth accelerated in 1Q22 to grow by 2.8% on a QoQ seasonally-adjusted basis from 4Q21’s 2.1% as industry-led pilot schemes to bring back foreign workers to the sector bore fruit. Despite concerns over supply chain disruptions to the construction industry from China’s lockdowns and the upsurge in raw material prices due to the Russia-Ukraine conflict, the construction sector’s recovery remains well with government support cushioning the impact of external factors. HDB for instance, is partnering with its contractors to enhance their stockpiles of building materials by procuring them in advance to mitigate potential disruptions.

HDB has also extended the period of protection against steel price fluctuations, and is supplying contractors with more concreting materials at protected prices. This has helped to mitigate the higher cost of materials faced by suppliers.

The Negatives

- Net gearing to remain elevated with higher steel rebar prices. Net gearing rose 340bps on a QoQ basis along with the rise in inventory of the Group. We expect gearing for FY22e-23e to remain elevated as we forecast firmer steel prices in 2022. We are not overly concerned with the uptick however, as the bulk of its short-term loans and borrowings are letter of credit and treasury receipts used to finance inventory purchase for order fulfillment.

We estimate that the Group is currently operating at ~70% capacity, and management guided that there is still room for capacity to increase when required. We do not expect any material capex spend for FY22.

Outlook

Construction sector see faster pace of recovery in 1Q22; expects escalation of activity for rest of 2022. The Group’s order book remained above $1bn as the construction sector continues its recovery. We estimate that half of its order book will be fulfilled within the next 12-15 months.

According to the Ministry of Trade and Industry, in absolute terms, the value-added of the sector remained at 25.3% below its pre-pandemic level, as activity at construction worksites continued to be weighed down by labour shortages. Despite this, we see the labour shortage situation easing with the relaxation of border restrictions and remain positive on the outlook for the sector.

HDB has announced that it will ramp up the supply of new build-to-order (BTO) flats over the next two years to meet the strong housing demand from Singaporeans. It plans to launch up to 23,000 flats per year in 2022 and 2023, which represents a significant increase of 35% from the 17,000 flats launched in 2021. Minister for Transport S Iswaran also recently announced that Changi Airport’s Terminal 5 project will resume after being put on hold for two years due to the Covid-19 pandemic.

With an approximately 65% market share in the reinforced steel industry, we continue to see BRC Asia as a key beneficiary of the construction sector recovery.

The Positives

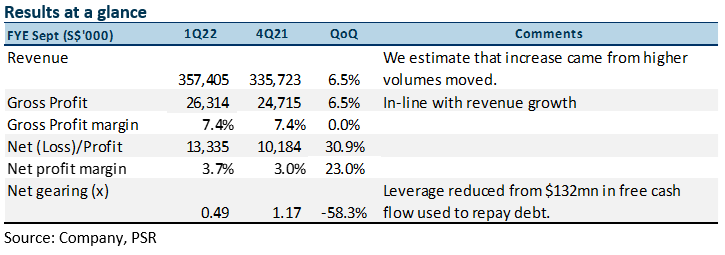

+ 1Q22 net profit exceeded our expectations. In spite of the resurgence of COVID-19 in Singapore, we estimate that order deliveries went up as disruptions to construction schedules were minimised with more frequent testing. The 6.5% higher QoQ sales (from the Group’s voluntary update) also came as a surprise because of the seasonally weaker 1H of the financial year. Despite the strong beat, we are keeping our forecasts for FY22e unchanged as we monitor the overall recovery of the construction sector.

The Group’s order book inched up to $1.3bn from $1.2bn as the construction sector continues its recovery. We estimate that half of the order book will be fulfilled within the next 12-15 months.

+ Significant deleveraging of Group’s balance sheet. The Group benefitted from a free cash inflow of $132mn for the quarter, which was used to deleverage its balance sheet. We believe a significant portion of the cash inflow was used to repay the trade facilities that it takes on to procure steel raw materials.

Despite the lower gearing ratio in 1Q22, we still expect gearing for FY22e-23e to remain elevated as we forecast firmer steel prices in 2022. Even though steel prices corrected by about 30% late last year, they have since rebounded by ~19% underpinned by prospects of strong demand supported by China’s plans of infrastructure investment in a bid to boost economic stability.

Outlook

Easing border restrictions to aid further recovery in the construction sector. With higher vaccination rates (~88%), we believe the government will progressively loosen border restrictions to alleviate the tightness in the labour market. The number of seasonally adjusted job vacancies in the overall economy rose to an all-time high of 98,700 in September 2021. The number of vacancies is especially acute in sectors which rely most on foreign workers, such as construction and manufacturing. In the first half of 2021, the total number of foreign workers declined by 32,600. The seasonally adjusted job vacancy to unemployed person ratio rose to 2.09 in September 2021, from 1.63 in June 2021. We therefore believe the government will progressively facilitate the safe inflow of new foreign workers to alleviate the manpower crunch while ensuring that the risk of COVID-19 importation is well-managed to protect public health. The Ministry of Health recently announced the easing of measures for travellers from various countries, including Malaysia.

BCA upgrades forecasts of construction demand for 2022. The BCA has upgraded its forecasts of construction demand for 2022 to $27bn-32bn per year from the original $25bn-32bn per year, comparable with the preliminary $30bn in 2021. The BCA also projects that demand for building materials will increase in tandem with the increased construction demand. Steel rebar demand is forecasted to grow to 1mn-1.2mn tonnes in 2022, representing ~22% YoY increase.

We note that BCA’s forecasts for average construction demand in 2022-2025 excludes the development of Changi Airport Terminal 5 and expansion of the two integrated resorts. As our forecasts have not included these projects, there is upside if they go live.

In the near term, projects in the pipeline that will likely support the group’s growth are the Singapore Science Centre’s relocation, the Toa Payoh integrated development, Alexandra Hospital redevelopment, Bedok’s new integrated hospital, Phases 2-3 of the Cross Island MRT Line and the Downtown Line’s extension to Sungei Kadut.

With an approximately 65% market share in the reinforced steel industry, we continue to see BRC Asia as a key beneficiary of the construction sector recovery.

The Positives

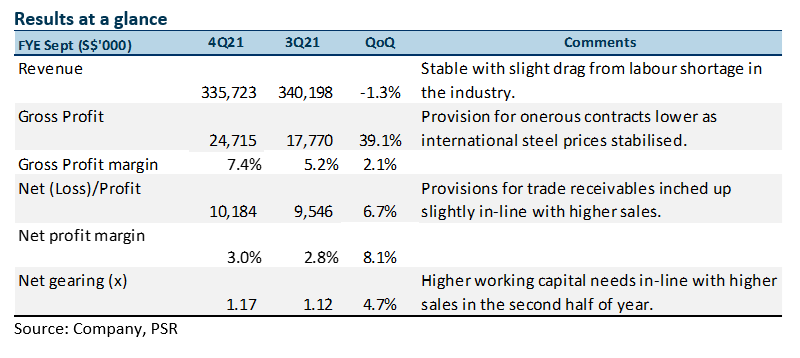

+ FY21 net profit exceeded our expectations by 24.2%. In spite of the resurgence of COVID-19 in Singapore, order deliveries went up as disruptions to construction schedules were minimised with more frequent testing. The beat also came from share of results of associates, which generated a profit of $1mn, reversing the $14.5mn loss last year as the Group reversed the impairment loss as a result of improved occupancy in both its hotel and resort following the easing of travel restrictions in the Maldives.

The total contracts awarded for Jan-Sept 2021 in the construction sector were $21.7bn, surpassing 2020’s $21bn. BRC has sizeable amount of projects in the pipeline, with its order book steady at about S$1.2bn. We estimate that half of the order book will be fulfilled within the next 12-15 months.

+ Total dividend for FY21 stands at 12 cents/share, exceeding our forecast of 8 cents. On top of the interim dividend of four cents already paid, the company has proposed a final dividend of four cents per share and a special dividend of four cents, bringing full-year dividend to 12 cents per share. This represents approximately 61% of earnings, translating into an 8.1% yield.

+ Gross profit margin and provision for receivables impairment better than expected. With steel prices easing slightly in the last few months, provisions for onerous contracts also eased, resulting in gross profit margins improving QoQ. Total provisions for impairment loss on trade receivables was S$2.7mn in FY21, or 2.3% of total sales. This was lower than our 3% estimate despite the continued challenges faced in the construction industry.

The Negative

- Net gearing inched up to 1.17x from 1.12x as working capital needs increased due to higher inventory costs and sales. Total borrowings increased by another S$40.9mn in 4Q21 as higher sales necessitated higher working capital. Despite steel prices easing slightly in the last few months, they remain elevated. We therefore expect inventory costs and net gearing to remain high in FY22-23e.

Outlook

Easing border restrictions could aid further recovery in the construction sector. With higher vaccination rates (~85%), we believe the government will progressively loosen border restrictions to alleviate the tightness in the labour market. The number of seasonally adjusted job vacancies in the overall economy rose to an all-time high of 92,100 in June 2021. The number of vacancies is especially acute in sectors which rely most on foreign workers, such as construction and manufacturing. In the first half of 2021, the total number of foreign workers declined by 32,600. The seasonally adjusted job vacancy to unemployed person ratio rose to 1.63 in June 2021, exceeding 1 for the first time since March 2019. We therefore believe the government will progressively facilitate the safe inflow of new foreign workers to alleviate the manpower crunch while ensuring that the risk of COVID-19 importation is well-managed to protect public health. The Ministry of Health recently announced the easing of measures for travellers from various countries, including Malaysia.

Construction sector improved marginally in the third quarter of 2021. Based on advance estimates from the Ministry of Trade and Industry, the Singapore economy grew by 0.8% on a QoQ seasonally-adjusted basis in the third quarter of 2021, a reversal from the 1.4% contraction in the preceding quarter. The construction sector shrank by 0.4% QoQ seasonally adjusted, improving from the 2.4% decline in the previous quarter. The Building and Construction Authority expects construction demand to improve to S$23-28bn in 2021 from S$21bn last year. The public sector is expected to contribute 65% of the new contracts or S$15-18bn, to meet stronger demand for public housing and infrastructure.

BCA also forecasts that average construction demand in 2022-2025 will be S$25-32bn per year, excluding the development of Changi Airport Terminal 5 and expansion of the two integrated resorts. The public sector is expected to contribute 56% to the demand.

As our forecasts have not included these projects, there is upside if they go live. In the near term, projects in the pipeline that will likely support the group’s growth are the Singapore Science Centre’s relocation, the Toa Payoh integrated development, Alexandra Hospital redevelopment, Bedok’s new integrated hospital, Phases 2-3 of the Cross Island MRT Line and the Downtown Line’s extension to Sungei Kadut.