CapitaLand Ascott Trust – Resilience from stable income sources

- Limited financial details were disclosed in this business update. 1Q26 distributable income was stable YoY, supported by the release of past divestment gains (just under S$10mn) to offset income loss from the temporary closure of The Cavendish London (TCL) for renovations and Madison Hamburg for works at the carpark, as well as interest savings from lower rates.

- Excluding TCL, as well as acquisitions and divestments, 1Q26 portfolio RevPAU increased 1% YoY despite ongoing geopolitical tensions. On a reported basis, RevPAU declined 2.8% to S$137 mainly due to properties undergoing AEI. Portfolio occupancy remained stable YoY at 77%.

- Upgrade from ACCUMULATE to BUY with an unchanged DDM-TP of S$1.08 due to the recent share price weakness. CLAS remains our top pick in the hospitality sector, given its geographical diversification and broad-based guest mix. In addition, 67% of 1Q26 gross profit came from stable income sources, while its growing exposure to the living sector (18% of AUM) offers greater resilience across market cycles. We expect low single-digit portfolio RevPAU growth in FY26e, supported by the U.S. portfolio, which should benefit from stronger lodging demand ahead of the upcoming FIFA World Cup 2026. Management is expected to utilise past divestment gains to offset the earnings impact from The Cavendish London AEI through completion in 2027, underpinning stable FY26e DPU. The impact of the Middle East conflict on CLAS is likely to be limited, as utility costs are largely either borne by lessees or tenants, or fixed through at least end-2026. In addition, any moderation in international travel arising from the conflict and higher airfares could potentially be offset by stronger domestic and regional demand. The current share price implies an FY26e dividend yield of 6.8%.

The Positives

+ Resilient performance despite geopolitical headwinds. Excluding acquisitions,

divestments, and properties undergoing AEI, 1Q26 portfolio RevPAU grew 1% YoY on a

same-store basis, with all key markets registering RevPAU growth. On a same-store

basis, Australia, Japan, Singapore, the UK, and the USA recorded RevPAU increases of

7%, 3%, 2%, 1%, and 7%, respectively. We expect low single-digit RevPAU growth in

FY26, supported by improving occupancy and stronger performance in the USA amid the

upcoming FIFA World Cup 2026. In addition, the U.S. PBSA portfolio, which saw some

weakness in the academic year (AY) 2025–2026 due to increased supply in some

markets, is showing improvement for AY 2026–2027, commencing in August 2026, with

over 80% pre-leased and revenue growth expected.

+ Strong financial position with low borrowing cost. The effective borrowing cost

declined 0.1 ppt QoQ to 2.8% and is expected to remain stable for FY26e, with 78% of

debt on fixed rates. S$689mn of debt, or 21% of total debt, is due for refinancing in 2026.

Gearing is healthy at 38.9%, and the interest coverage ratio is at 3 times.

The Negative

- nil

CapitaLand Ascott Trust – Stable DPU for 2026

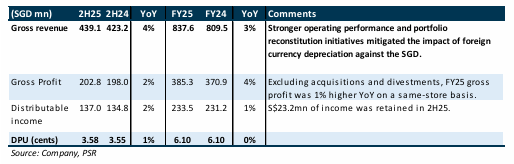

- FY25 DPU of 6.10 Singapore cents was stable YoY, in line with our expectations. Income available for distribution rose 11% YoY to S$256.7mn, driven by stronger operating performance and portfolio reconstitution initiatives. After retaining S$23.2mn to fund asset enhancement initiatives (AEI) and working capital, total distribution to unitholders rose 1% YoY to S$233.5mn.

- 4Q25 portfolio RevPAU rose 2% YoY to S$180 (FY25: S$161, up 3% YoY), driven by a 2ppt increase in occupancy to 83%. CLAS reported a 1.7% increase in portfolio valuations for the year, driven by stronger operating performance.

- Maintain ACCUMULATE with a higher DDM-TP of S$1.08 (prev. S$1.05) as we roll forward our forecasts. CLAS remains our top pick in the hospitality sector, underpinned by its balanced mix of stable (FY25: 65%) and growth income streams, alongside strong geographical diversification for earnings resilience. We expect low single-digit portfolio RevPAU growth in FY26e, supported by improving occupancy. CLAS has guided to a stable DPU YoY for FY26e at 6.1 Singapore cents, supported by past divestment gains used to offset the impact of major ongoing AEIs. There is over S$300mn of such gains still available on the balance sheet. The current share price implies an FY26e dividend yield of 6.2%.

The Positives

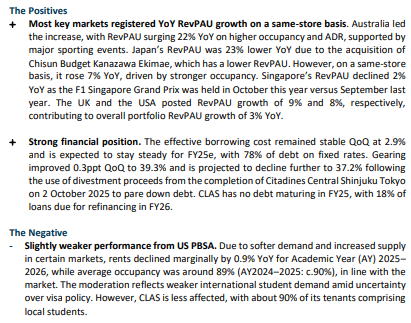

+ All key markets registered YoY RevPAU growth on a same-store basis in 4Q25.

Australia, Singapore, and the USA recorded RevPAU increases of 8%, 8% and 9%,

respectively, while Japan and the UK reported RevPAU declines of 42% and 2%,

respectively (Figure 1). Japan’s performance was impacted by acquisitions and

divestments, while the UK was affected by the winding down of The Cavendish London

in preparation for AEI. On a same-store basis, Japan’s RevPAU rose 11% YoY, and the

UK’s increased 10%. We expect low-single-digit RevPAU growth in FY26, supported by

improving occupancy.

+ Strong financial position. The effective borrowing cost was unchanged QoQ at 2.9% and

is expected to remain stable for FY26e, with 78% of debt on fixed rates. Gearing

improved from 39.3% to 37.7% QoQ following the repayment of debt using divestment

proceeds. The interest coverage ratio remains healthy at 3 times.

CapitaLand Ascott Trust – Committed to maintaining stable dividends

- Limited financial details were disclosed in this business update. 3Q25 gross profit rose 1% YoY, supported by stronger operating performance and portfolio reconstitution, partially offset by foreign currency depreciation against the SGD and a one-off land tax adjustment relating to a property in Australia. Excluding acquisitions and divestments, gross profit was 2% lower YoY due to the tax adjustment.

- 3Q25 portfolio RevPAU rose 3% YoY to S$163, driven by higher average occupancy of 83%, up from 79% in 3Q24. In the US, the student accommodation sector experienced softer performance due to increased supply in certain markets.

- Downgrade to ACCUMULATE from BUY with an unchanged DDM-TP of S$1.05 due to the recent share price performance. CLAS remains our top pick in the hospitality sector, underpinned by its balanced mix of stable (69%) and growth income sources, as well as strong geographical diversification that enhances resilience. We expect low single-digit portfolio RevPAU growth in FY25e, supported by improving occupancy. CLAS has guided for stable dividends YoY for FY25e at 6.1 Singapore cents. We therefore forecast a S$5mn top-up to distributable income from prior divestment gains, with c.S$350mn still available on its balance sheet. The current share price implies an FY25e dividend yield of 6.4%.

CapitaLand Ascott Trust – Committed to stable DPU despite upcoming AEIs

- 1H25 DPU of 2.53 cents (-1% YoY) was in line with our estimates at 42% of our FY25e forecast, with seasonally stronger performance expected in the second half of the year. Stronger operating performance, portfolio reconstitution, and asset enhancement initiatives (AEIs) drove a 6% YoY increase in gross profit. Excluding acquisitions and divestments, gross profit was 4% higher YoY on a same-store basis. Excluding one-off items, core DPU was stable YoY at 2.40 cents.

- Portfolio RevPAU rose 3% year on year to S$159, driven by higher average occupancy of 78% compared to 75% in 2Q24. Following six completed AEIs in FY24, three more were announced, with one completed in 2Q25. Four AEIs remain, including The Cavendish London, with a total CAPEX of c.S$205mn. The divestment of Somerset Olympic Tower Tianjin was completed in 2Q25 at a 50% premium to book value.

- Maintain BUY with an unchanged DDM-TP of S$1.05. CLAS remains our top pick in the sector, supported by its mix of stable (66%) and growth income sources, as well as geographical diversification, which enhances resilience with stronger markets offsetting potentially softer ones. We expect low-single-digit portfolio RevPAU growth in FY25e, driven by improving occupancy. CLAS has over S$300mn in prior divestment gains on its balance sheet, which could be used to offset the absence of contributions from assets undergoing AEIs. Our estimates remain unchanged. The current share price implies an FY25e dividend yield of 6.6%.

CapitaLand Ascott Trust – Downside protected from stable income sources

- Limited financials were provided in this business update. 1Q25 gross profit rose 4% YoY, driven by improved operating performance and contributions from new properties, which offset the lost income from divestments. Excluding acquisitions and divestments, gross profit rose 1% YoY.

- 1Q25 portfolio RevPAU increased 4% YoY to S$141 due to higher average occupancy of 77% (1Q24: 73%). Two DPU-accretive acquisitions (1.6%) were made in Japan in 1Q25, namely Ibis Styles Tokyo Ginza and Chisun Budget Kanazawa Ekimae, at a blended NOI yield of 4.3%.

- Maintain BUY with an unchanged DDM-TP of S$1.05. We lower our FY25e/26e DPU estimates by 4% to account for downtime from upcoming AEIs. CLAS remains our top pick in the sector, supported by its mix of stable (70%) and growth income sources and geographical diversification, which enhance resilience amidst potential weakness in consumer sentiment from global uncertainties. We expect mid-single-digit portfolio RevPAU growth in FY25e, driven by improving occupancy and six AEI completions in FY24. CLAS has over S$300mn in prior divestment gains on its balance sheet, which the manager may deploy to offset the absence of contributions from assets undergoing AEIs. The current share price implies an FY25e dividend yield of 7%.

CapitaLand Ascott Trust – Growth on all cylinders

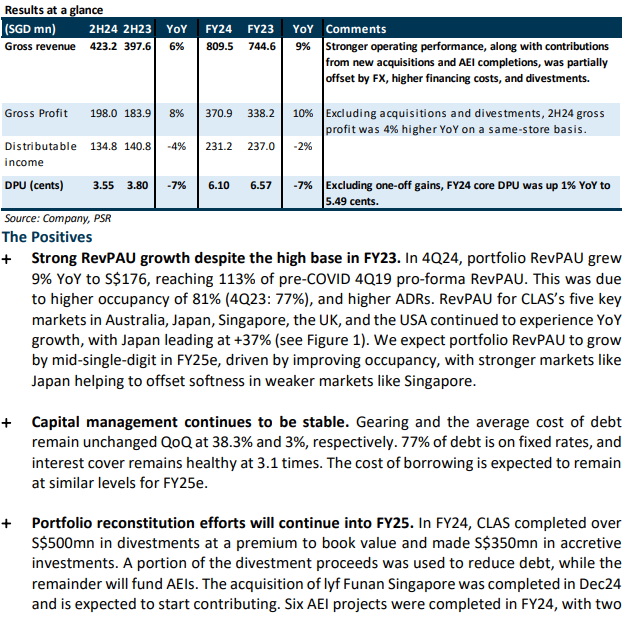

- FY24 DPU of 6.10 Singapore cents (-7% YoY) was in line with our FY24e estimates. Excluding one-off gains, the core DPU of 5.49 Singapore cents increased by 1% YoY, driven by stronger operating performance, acquisitions, and completed asset enhancement initiatives (AEIs). However, this was partially offset by divestments, ongoing AEIs, higher financing costs, and the depreciation of foreign currencies against the Singapore Dollar.

- 4Q24 portfolio RevPAU increased 9% YoY to S$176 despite the high base, reaching 113% of pre-Covid 4Q19 levels. This was driven by a higher average occupancy of 81% (4Q23: 77%) and increased average daily rates (ADR) across the portfolio. Over S$500mn in assets were divested at a premium to book value in FY24, unlocking S$74mn in net gains.

- Maintain BUY with a higher DDM-TP of S$1.05 (prev. S$1.04) as we roll forward our forecasts. We lower our FY25e DPU estimates by 3% on higher finance costs assumptions. CLAS remains our top pick in the sector, supported by its mix of stable and growth income sources and geographical diversification, which enhance resilience amidst global uncertainties. We expect mid-single-digit portfolio RevPAU growth in FY25e, driven by improving occupancy, with overseas assets offsetting softer demand in Singapore due to the absence of major concerts. CLAS still holds over S$300mn in previous divestment gains on its balance sheet, some of which will be utilized in FY25e to offset the absence of contributions from assets that will be undergoing AEIs. The current share price implies an FY25e dividend yield of 7%.

CapitaLand Ascott Trust – Portfolio reconstitution efforts bearing fruit

- Limited financial details were provided in this business update. 3Q24 gross profit rose 8% YoY, driven by stronger operating performance and portfolio reconstitution initiatives, which included S$350mn in acquisitions and S$500mn in divestments at premium to book value YTD. Excluding acquisitions and divestments, gross profit rose 2% YoY.

- 3Q24 portfolio RevPAU increased 3% YoY to S$158 despite the high base, reaching 105% of pre-Covid 3Q19 levels. This was due to a higher average occupancy of 79% (3Q23: 77%), which was 92% of pre-Covid levels. Revenue from France grew 11% YoY, driven by the Paris Olympic Games.

- Maintain BUY with an unchanged DDM-TP of S$1.04. There has been no change in our estimates. CLAS remains our top pick in the sector owing to its mix of stable and growth income sources and geographical diversification, which provide resilience amidst global uncertainties. We have not factored in any capital gain top-ups from previous divestment gains in FY24e; any top-ups would represent potential upside. RevPAU YoY growth has reached its lowest level since 2Q21. We expect mid-single-digit portfolio RevPAU growth in FY25e, driven by improving occupancy, with overseas assets helping to offset softer demand in Singapore due to the absence of major concerts or events like Coldplay and Taylor Swift. The current share price implies an FY24e/25e dividend yield of 6.6%/7.1%.

CapitaLand Ascott Trust – Olympics to support stronger 2H24

▪ 1H24 DPU of 2.55 cents (-8% YoY) was in line with expectations and formed 43% of our

FY24e forecast, with seasonally stronger performance expected in the second half of the

year. 1H24 revenue increased by 11% YoY due to stronger performance of the existing

portfolio and contributions from new acquisitions, partially offset by divestments and

foreign currency exchange. Despite stable distributable income YoY, DPU was down due

to the enlarged share base from the equity fundraising exercise in 3Q23.

▪ 2Q24 portfolio RevPAU rose 4% YoY on a high base to S$155, reaching 102% of pre-

COVID 2Q19 levels. This was attributable to higher room rates; 2Q24 average portfolio

occupancy was stable YoY at 75%.

▪ Maintain BUY with an unchanged DDM-TP of S$1.04. We increase our FY24e/25e DPU

estimates by 1%/4% on stronger operating performance in Japan and France, partially

offset by higher interest expense. CLAS remains our top pick in the sector owing to its

mix of stable and growth income sources and geographical diversification, which provide

resilience amidst global uncertainties. Growth in RevPAU going forward will be driven

by portfolio occupancy as average daily room rates (ADR) stabilise. The current share

price implies an FY24e/25e dividend yield of 6.6%/7.1%.

CapitaLand Ascott Trust – Occupancy to improve with ADRs stabilising

- No financials were provided in this business update. 1Q24 gross profit rose 15% YoY due to stronger operating performance and contributions from new properties. It was 7% higher YoY on a same-store basis.

- 1Q24 portfolio RevPAU rose 6% YoY to S$135, in line with pre-COVID 1Q19 levels. 1Q24 average portfolio occupancy was stable YoY at 73%, and it was at 88% of pre-COIVD levels.

- Upgrade from ACCUMULATE to BUY with an unchanged DDM-TP of S$1.04 due to the recent share price performance. FY24e DPU is slightly lowered by 2% on higher interest costs assumptions. CLAS remains our top pick in the sector owing to its mix of stable and growth income sources and geographical diversification, which provide resilience amidst global uncertainties. Growth in RevPAU going forward will be driven by portfolio occupancy as ADR stabilises. The current share price implies an FY24e/25e dividend yield of 6.6/6.8%.

The Positives

- 1Q24 RevPAU grew 6% YoY to S$135, in line with pre-pandemic 1Q19 pro-forma RevPAU mainly due to higher ADRs. Average portfolio occupancy was stable YoY at 73% - it was down 4ppts QoQ due to seasonality. RevPAU for CLAS’s five key markets in Australia, Japan, Singapore, UK, and the USA continued to improve YoY (see Figure 1) and exceed pre-COVID 1Q19 levels on a same-store basis (excluding units under renovation).

- Strong capital management. Gearing and interest cover remained healthy at 37.7% and 3.7x, respectively. CLAS’s effective borrowing cost increased 60bps QoQ to 3%, mainly due to a higher proportion of GBP and EUR debt arising from the new acquisitions. Despite this increase, CLAS’s borrowing costs remain relatively low compared to those of its industry peers. 82% of debt on a fixed rate. Additionally, we think CLAS will recall its S$150mn, 3.88% perpetual bond at its first call date in Sep 24 to save on interest costs. Gearing will remain below 40% even if debt fully funds this.

- Portfolio recycling is in full swing. In Jan 2024, CLAS acquired Teriha Ocean Stage, a rental housing property in Fukuoka, Japan, for JPY 8bn with an estimated net operating income yield of 4% on a stabilised basis. Five properties were divested in 1Q24, and they were Courtyard by Marriott Sydney-North Ryde in Australia, Hotel WBF Kitasemba East, Hotel WBF Kitasemba West and Hotel WBF Honmachi in Osaka, Japan, and Citadines Mount Sophia Singapore. All assets were divested at a premium above book value, locking in net gains of over S$25mn. Proceeds from the divestments have been used to par down higher interest rate debt.

The Negatives

CapitaLand Ascott Trust – Further upside from occupancy growth

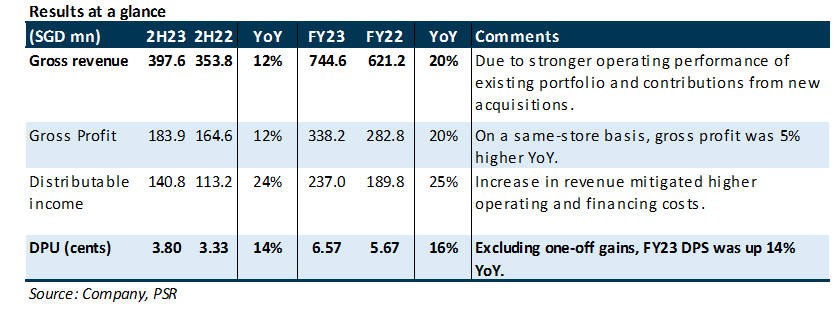

- FY23 DPU of 6.57 cents (+16% YoY) exceeded our expectations by 11.7% due to a one-off realised exchange gain. Excluding one-off items, adjusted DPU increased 14% YoY to 5.44 cents, which was 93% of our forecast.

- 4Q23 portfolio RevPAU rose 4% YoY to S$161, reaching 103% of pre-COVID 4Q19 levels mainly due to higher average daily rates (ADR). Average portfolio occupancy was stable QoQ at 77% (4Q22: 78%), and it was at 92% of pre-COIVD levels.

- Downgrade from BUY to ACCUMULATE with an unchanged DDM-TP of S$1.04 as we roll forward our forecasts. FY24e/FY25e DPU is raised by 3%/6% after lowering our interest costs assumptions. CLAS remains our top pick in the sector owing to its mix of stable and growth income sources and geographical diversification. Growth in RevPAU going forward will come from higher portfolio occupancy, as ADR growth would slow from the high base. The current share price implies an FY24e/25e dividend yield of 6.5/6.8%.

The Positives

- 4Q23 RevPAU grew 4% YoY to S$161, reaching 103% of pre-pandemic 4Q19 pro-forma RevPAU mainly due to higher ADRs. Average portfolio occupancy was stable QoQ at 77% (4Q22: 78%). RevPAU in Australia, Japan, Singapore, UK and USA continued to exceed pre-COVID 4Q19 levels on a same-store basis. Japan saw a spike in RevPAU by 90% YoY after its re-opening to independent leisure travellers in Oct 2022. Performance in China and Vietnam continued to improve, with RevPAU at 86% and 88% of 4Q19 levels respectively.

- Proactive capital management. Gearing and interest cover remained healthy at 37.9% and 4x, respectively. CLAS’s effective borrowing cost remained unchanged at 2.4% QoQ, with 81% of debt on a fixed rate. We expect the FY24 cost of debt to increase to c.2.9% after refinancing 18% of its total debt (c.S$563mn) due in FY24. A 50bps increase in CLAS’s borrowing cost will impact full-year DPU by 0.08 Singapore cents.

- Higher portfolio valuation. CLAS’s portfolio valuation rose 2% as stronger operating performance and outlook mitigated the impact of higher discount and cap rates across all markets (except for Japan). Markets with valuation gains include Australia, Europe, Japan, Singapore, and UK. Separately, CLAS is divesting Citadines Mount Sophia Singapore for S$148mn, 19.4% above book value. The exit yield for this transaction is 3.2%, and CLAS will recognise a net gain of c.S$14.6mn. The divestment is expected to be completed in 1Q24.

The Negatives

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report