The Positives

+ Portfolio occupancy up 1.5ppts YoY from 91.7% to 93.2%, led by Singapore (+1.8ppt), Australia (+1.8ppt) and the US (+1.6ppt). UK occupancy dip of 0.8ppt due to non-renewals. Singapore's occupancy improved 1.8ppts YoY to 90.2% due to better leasing at business parks and logistics assets. 70% of demand was driven by tenants in the IT & data centres (25.5%), biomedical (24.6%), engineering (11.4%) and chemicals (8.5%). Australia's +1.8ppt occupancy gains were driven by logistics assets. US occupancy increased 3.1ppts QoQ from 91.4% to 94.5% due to the improvement in occupancy of its newly acquired logistics portfolio. The portfolio of 11 logistics assets was acquired in Nov 21 at an acquisition occupancy of 92.6%. AREIT managed to lease out all the vacant space by end-Dec.

+ FY21 average portfolio reversions were positive at 4.5% (FY20: 3.8%). Reversions in Singapore came in at 2.9%, positive across all asset classes. Business parks (+2.9%) captured demand from new economy industries such as tech, biomedical and chemical, as well as government tenants. Reversions for logistics came in at +4.4%, pulling demand from 3PL tenants. Reversions for US business parks came in at +22.6% due to under-market passing rents while UK data centres delivered +6.2% reversions.

The Negative

- Delays in AEI/development timelines with slight cost escalations. Labour, supply chain constraints and cost of compliance with healthy-safety requirements for projects undergoing construction during the pandemic has led to delays and slightly higher construction cost. Delivery of some projects have been pushed back between 1-4 quarters, such as the redevelopment of iQuest, which has been delayed from 4Q23 to 4Q24. Projects completed in FY21/22 delivered ROIs close to their initial projections. Initial projected ROIs for the Grab build-to-suit and the redevelopment of UBIX were 6.1% and 7.7% respectively and were completed on 30 Jul 21 and 7 Jan 22, with ROIs of 6.0% and 6.7% respectively.

Outlook

Possible NPI margin compression due to cost inflation. Energy costs are likely to fluctuate upwards as most of AREIT’s electricity is generated from fuel sources. The management estimates that electricity costs, which accounts for c.20% of OPEX, could increase by 50-70% in FY22. As there are no fixed rates or bulk discounts available to hedge the rising electricity costs, the management will try to offset the higher electricity costs through cost containment measures. Tenant leases have clauses which allow the adjustment of service costs, providing AREIT possible recourse to pass through higher inflation driven OPEX.

Leveraging scale to drive value. AREIT’s AUM as at 31 Dec 21 stands at S$16.3bn, comprising 217 properties. Asset concentration risk is low, with its largest assets, Galaxis, representing 4.3% of revenue. Given the size of its asset base, AREIT’s sizable debt headroom of S$4.8bn to reach 50% gearing allows it to take meaningful strides into new asset classes in overseas markets, while its low asset concentration risk allows it to undertake AEIs and redevelopments without significant impact to earnings. During the year, AREIT completed S$2.1bn of acquisitions/developments and S$23.3mn of asset enhancement initiatives (Figure 1). It also divested five properties for total sales proceeds of S$247.9mn. There are six AEIs and redevelopments ongoing worth S$647mn (Figure 2), expected to be delivered between 1Q22 to 2Q25. From AREIT’s prior experience, refreshed properties have enjoyed higher-than-market take-up rates.

Ninety percent of AUM are new economy assets such as business space, high-spec assets, data centres and logistics properties. “Old economy” assets such flatted factories and light industrial assets represent 6% of AUM. Some of these assets are in prime industrial areas such as Tai Seng and Serangoon and could receive some convert-to-suit demand or be redeveloped into new economy assets such as data centres or high spec properties. The management will try to secure one of the data centre licences from the government in the near future. Repositioning of assets, such as converting light-industrial assets to high-spec asset, allows AREIT to command higher rents and keep its portfolio future ready.

Maintain BUY, DDM TP lowered from S$3.65 to S$3.52

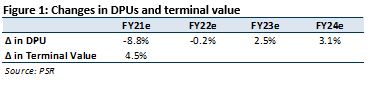

FY22-25e DPUs dip 2.1-49% after factoring in higher OPEX. Our DDM-based TP is lowered by 3.6% to S$3.52 due to lower DPUs and higher COE of 6.12% (prev. 6.0%), after factoring a higher risk-free rate. AREIT remains our top pick for the sector in view of its scale and diversification. The REIT also continues to forge a future-ready portfolio by increasing its exposure to growth sectors of the economy such as knowledge economy, technology and e-commerce.

+ Positives

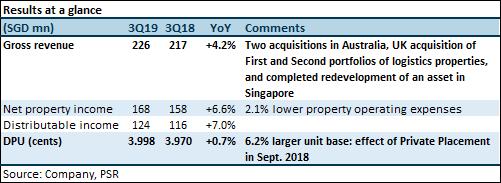

+ Pick-up in occupancy. Portfolio occupancy improved QoQ from 90.6% to 91.3%, led by Singapore (+1.0ppt), Australia (+0.9ppt) and the US (+0.3ppt). There was a slight dip of 0.2ppt in the UK due to a non-renewal. Singapore occupancy rose to 87.9% following full occupancy at 31 Joo Koon Circle, a light industrial property which was vacant back on 31 Mar 2021. The property is now fully leased to a biomedical tenant on a 20-year lease. Australian occupancy improved to 95.8% after a lease was signed at a logistics asset in Sydney. This brought the asset’s occupancy to 54%, from zero in 1Q21. UK occupancy remained high at 98.2% despite the 0.2ppt dip.

+ 2Q21 reversions of +8.9% lifted 1H21 reversions to +6.4% (1Q21: +3.0%). Singapore reversions were +3.4%, better across the asset classes except integrated development, where reversions were down 3.1% for two small leases. Reversions for logistics, high-spec, business space and light industrials came in at 4.9%, 4.8%, 3.7% and 1.3% respectively. Reversions in the US were strong at 26.3%, towering above 1Q21’s 6.2%. In-place rents for its US portfolio, which comprises business space, are 10-30% below market, which should provide positive reversions in the coming years. New leases in 1H21 were primarily signed with the biomedical (34%), IT (19.5%) and lifestyle, retail & consumer-product (9.4%) sectors.

- Negative

- Policy-related vacancies in Singapore. Assets built on JTC land are subject to the JTC’s anchor-tenant and subleasing policies. They also have to adhere to URA zoning rules for the use of space. Some vacancies have been attributed to these policies, which may take longer lead times to replace anchor tenants.

Outlook

A higher plot ratio has been approved for the redevelopment of 1 Science Park Drive, formerly leased to TÜV SÜD. This will increase the land’s GFA by 3.5x from 30k sqm to 100k sqm. Preliminary plans are three vertical campuses, fitted with IT and life-science specifications. Given significant development costs of S$800mn-1bn, AREIT may redevelop this property via a JV with sponsor CapitaLand (CAPL SP, BUY, TP S$4.28). This will leave headroom for it to pursue other AEI, redevelopment and build-to-suit opportunities. More details will be released at a later date.

1Q21 update

+ Positive

+ Reversions at 3.0%. US and Singapore reversions were 6.2%and 2.9% respectively. Singapore reversions were mixed, with positive reversions of 5.6%, 2.8% and 0.8% for logistics, business parks and light industrials respectively. Reversions for high-spec and integrated development assets were -0.9% and -2.7%.

- Negative

- 1Q21 portfolio occupancy slid QoQ from 91.7% to 90.6%, under non-renewals in Australia and Singapore. Singapore occupancy fell QoQ from 88.4% to 86.9% on the back of a 14.9ppt decline at 138 Depot Road and 0% occupancy at TÜV SÜD PSB Building which will be redeveloped (4Q21: 100%). Australia’s occupancy shed 2.5ppts to 94.9% following a non-renewal at 1 Distribution Place (1Q21 0%, 4Q20 100%). Occupancy is expected to improve as the manager has lined up tenants for the space.

Acquisition of remaining 75% stake in Galaxis from CapitaLand for S$543.8mn

AREIT’s acquisition of this stake comes 13 months after its initial 25% investment in Galaxis, acquired from MBK Real Estate Asia Pte Ltd. The agreed property value of S$720mn on a 100% basis represents a 2% discount to the market value of Galaxis and a 14.3% appreciation since AREIT’s initial investment (Figure 1). AREIT has raised S$420mn from private placements and will issue an additional S$83mn new units as partial payment to CapitaLand (CAPL SP, Buy, TP S$4.38) for the remaining 75% stake. The issue will increase its share base by 4.2%.

Galaxis is currently held by a private limited company and is subject to a 17% corporate income tax. With full ownership of Galaxis, AREIT can apply for limited liability partnership conversion, allowing unitholders to enjoy tax transparency on the income from Galaxis. Expected DPU accretion on a pro-forma basis, assuming a 6-month conversion approval process, is 0.46%.

AREIT declared a DPS of 5.63 Singapore cents for the period 1 January 2021 to 13 May 2021, forming 35% of our FY21e DPU, broadly in line with our full year forecast.

Positives

+ Portfolio occupancy stable at 91.7%, -0.2ppt/+0.8pppt QoQ/YoY. Singapore occupancy rose from 87.9% to 88.4%, lifted by the logistics sector. New demand came from government agencies (22.7%), logistics and supply chains (16.2%), biomedical and agri/aquaculture (11.5%) and engineering (10.0%).

+ FY20 reversions in the green at 3.8%, reflecting better leasing for its Singapore portfolio in 1H20. There were also strong reversions of 16.7% and 14.0% in the US and Australia. About 20.9% of Singapore leases will expire in FY21, mostly in business (41%) and logistics (22%) parks. Due to longer WALEs in its overseas portfolio, only 7%/5.7%/5.5% of leases will be expiring in the US/Australia/UK.

+ Gearing improved YoY from 35.1% to 32.8%, after its S$1.2bn ERF in 4Q20. AREIT raised more funds in advance of acquisitions to give it greater financial flexibility. Balance sheet remained strong with interest coverage at 4.3x and formidable S$5bn headroom to the 50% leverage limit.

Negative

- Handful of non-renewals. There were some non-renewals during the year. A 9,494 sqm logistics asset at Changi North and a 15,421 sq m light-industrial asset at Joo Koon Circle ended the year vacant. Occupancy at 7,915 sq m Cintech II also fell to 0% in 3Q20 but AREIT was able to lease the building fully to a government agency by 4Q20. Some pre-terminations are expected following the recent rollout of the Singapore government’s ReAlign Framework. However, AREIT’s manager shared that the impact should be minimal at 0.1% of GRI.

Outlook

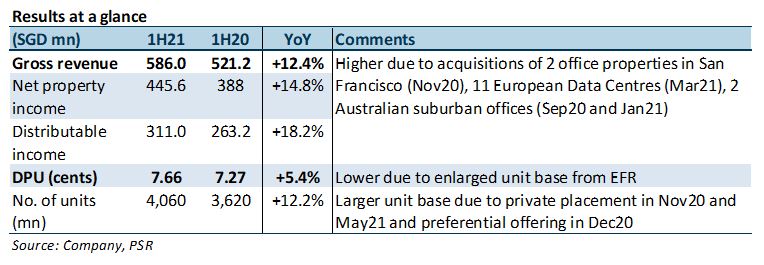

AREIT announced the acquisition of two Class A office buildings in San Francisco and its S$1.2bn EFR on 10 November 2020. Proceeds will be used to part-fund its acquisition of two US office buildings, a suburban office in Sydney, Australia and a portfolio of data centres (DC) in Europe. Its EFR will increase its share base by 10%. The US and Australian acquisitions were completed on 21 November 2020 and 13 January 2021 respectively. Negotiations and due diligence for the European data-centre portfolio remain in progress.

Construction slippages in 2020 have led to the rollover of new industrial supply to 2021. The leasing environment remains challenging as landlords keep rents competitive to attract new tenants. Still, AREIT expects tenant retention to be 60-70%, similar to historical levels. It has guided for flat to mid-single-digit reversions for all its markets. Demand is likely to emanate from the technology, precision engineering and biomedical sectors. Singapore continues to be an attractive location for manufacturers. AREIT’s manager said it has conducted viewings for several prospective foreign tenants. Construction costs have crept up due to compliance costs with health and safety measures. Costs for contracts locked in before COVID-19 may tick up 2-3%. New construction quotes may cost up to 15% more.

Maintain BUY. DDM-based TP raised from S$3.61 to S$3.73

We drop FY21e/22e DPUs by 8.8%/0.2% (Figure 1) as we incorporate its acquisition of the: i) two Grade A office buildings in the US; ii) suburban office in Sydney; iii) logistics asset under development in Brisbane; iv) portfolio of European data centres; and v) its S$1.2bn ERF. We also updated our leasing assumptions. We have assumed it will be acquiring the S$1.5bn European data-centre portfolio at an NPI yield of 6% and LTV of 40% sometime in 3Q21.

We continue to favour AREIT for its scale and diversification. Stock catalysts are expected from acquisitions and redevelopment. We forecast DPU growth of 9.6% for FY21e as acquisitions and redevelopment/AEI start contributing.

Positives

+ One more in the bag. AREIT announced its acquisition of MQX4 on 18 September 2020. This is a suburban office under development in Macquarie Park, Sydney, bought at a "as if completed" market valuation of S$161mn. The completed asset will have a net lettable area of 19,384 sqm, comprising 17,753 sqm of office space and 1,631 sqm of retail space. The acquisition will be funded with debt and/or internal resources and carries an initial NPI yield of 6.1%. A 3-year rental guarantee can provide upside if AREIT can lease out the property before the rental guarantee period ends. Completion of the land sale is expected in 4Q 2020, and of MQX4, around mid-2022. This is AREIT's third acquisition YTD, following its purchase of a 25% stake in Galaxis and a logistics asset under development in Kiora Crescent, Yennora, Sydney in March and July 2020 respectively.

+ Portfolio occupancy up from 91.5% to 91.9%. Singapore occupancy rose from 87.9% to 88.8%, supported by higher occupancy at Cintech II (30 Sep 2020: 100%, 30 Jun 2020: 0%) and a logistics asset, 40 Penjuru Lane (30 Sep 2020: 98.8%, 30 Jun 2020: 85.5%). This was partially offset by a decline in Australian occupancy from 98.4% to 97.5% due to a non-renewal at 92 Sandstone Place, Brisbane. Take-up was mainly driven by the government and logistics and supply-chain companies.

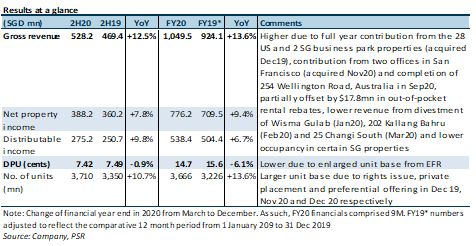

+ Gearing improved from 36.1% to 34.9%; cost of borrowing down from 2.9% to 2.8%. Gearing improved largely due to S$300mn non-call green perpetuals issued at 3.0%, which are counted as equity in gearing calculations. Total gross borrowings and perpetual securities to unitholders’ funds amounted to 63.3%. Adjusted interest coverage, which includes interest payment for the perpetuals, is estimated at 3.9x (2018: 4.2x). This is amply above the MAS' 2.5x minimum. Earnings are expected to be underpinned by its diversified rental income from industrial assets which have shown resilience to the economic downturn. Out-of-pocket rebates totalled just 2% of FY20e revenue.

Negative

- Portfolio rental reversion of -2.3%. Despite better occupancy, Singapore reversions were a negative 2.8%. Larger space signed with negative reversions wiped out AREIT’s +11.5% reversions in the US. Aside from business parks’ positive 4.5%, reversions for the other asset classes were flat or negative: Logistics and Distribution Centres (-16.2%), High-Specification (-3.3%), Light Industrial (-1.4%) and Integrated Development (flat). 9M20 portfolio reversions came in at +4.2%. We think low-single-digit positive reversions for FY20e are still achievable owing to stronger leasing locked in in 1H20.

Outlook

Subdued leasing is expected as companies continue to put business and expansion plans on hold out of caution. Singapore industrial rents were weak in 3Q20 while sector occupancy only crept up due to warehouse leasing.

Upgrade to BUY with lower TP of S$3.61, from S$3.63

We adjust our forecasts to reflect its acquisition of MQX4. Our TP dips to S$3.61 due to higher debt and perpetual securities. Recent pullback in share price presents better entry price and total returns of 31.5% to our TP. As such we upgrade our call from Accumulate to BUY.

AREIT’s S$13.8bn portfolio comprises 197 properties across Singapore, Australia, the UK and the US. This results in low asset-concentration risks, with no property accounting for more than 4.6% of its revenue. Such geographical diversification and low tenant concentration - 1,450 tenants, the largest at <4% of revenue - help to attenuate the economic impact on its portfolio. Its portfolio weighted average security deposit is about 5.3 months of rental income.

Positives

+ Achieved positive portfolio rental reversions of +4.3%/+5.4% for 2Q/1H20. Portfolio reversions for 1Q20 came in at +8.0%. In Singapore, average rental reversion was +4.0% - business parks clocked +16.3% reversions due to certain assets in Changi Business Park; one renewal was by an international bank whose rent were marked-to-market upon renewal. Integrated Development penciled a 19.8% reversion due to Aperia while industrial and flatted factories achieved +5.1% reversions. -30.6% reversions for Hi-Spec asset class due to favourable rates offered to retain the tenant. Average rental reversion for Australia and the US were +16.6% and +16.2% respectively.

+ In it for the long haul - Forging ahead with acquisitions and AEIs. AREIT announced 2 acquisition YTD – acquisition of 25% stake in Galaxis was completed on 31 March 2020 at 3% discount to market value which the acquisition of a logistic asset under development (Kiora Crescent, Yennora, Sydney) was announced on 1 July 2020. During the quarter, AREIT completed 4 AEIs costing $22.9mn. In 2Q FY2020, S$16.3 million worth of new AEIs commenced across four properties.

+ Portfolio metrics remain healthy. Portfolio occupancy rate remained stable at 91.5% (1Q20: 91.7%), with improvements in Australia partially offsetting lower occupancies in SG and US. Aggregate leverage held steady at 36.1% (31 March 2020: 36.2%, 31 December 2019: 35.1%). Weighted average all-in cost of borrowing was maintained at 2.9% (31 March 2020: 2.9%, 31 December 2019: 2.9%)

Negatives

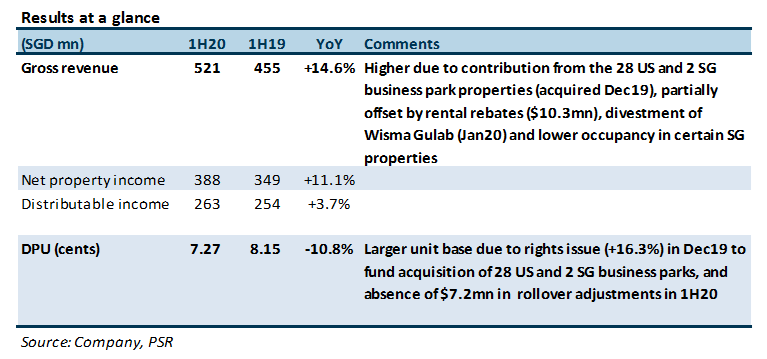

- 1H20 DPU fell -10.8% YoY due to larger unit base (+16.3%), rental waivers of $20mn and absence of rollover adjustments (1H19 +7.2mn).

Outlook

Rental rebates

Singapore (70% of AUM) - In line with the Singapore Government’s guidelines, AREIT has provided rent waivers to its tenants, amounting approximately S$20 million year-to-date. The actual amount to be disbursed will depend on the tenants’ eligibility assessment by the authorities. This amount is in addition to the Singapore Government’s property tax rebates and cash grants which will be fully passed through to eligible tenants. AREIT estimates that there are c.20% of SMEs in the portfolio.

Australia (13% of AUM) - Rent collection has been suspended from the F&B and retail tenants located at Ascendas Reit’s three suburban offices from April 2020 until their reopening. One lease of a leisure/hospitality tenant has been restructured and the tenant was provided with rent rebate. Rent waiver and deferment were offered to two small and medium enterprise (SME) tenants. The overall impact to AREIT is less than S$0.6 million.

United Kingdom (6% of AUM) - The rental payment frequency for some tenants has been changed from quarterly to monthly in advance and some rents have been deferred to the later part of the year to provide some cashflow relief to tenants.

United States (11% of AUM) - US$10,000 of rent rebates have been provided to date.

Maintain ACCUMULATE with and higher TP of S$3.62 (prev. $3.29)

We adjust our estimates to reflect the acquisition of the 25% stake in Galaxis and the acquisition of the Australian logistic asset at Kiora Crescent. Our TP is raised to $3.62 mainly due to a lower beta assumption, which lowered our cost of equity from 6.45% to 6.0%. We expect FY20e DPU yield of 4.8% at current entry price.

We see the merits of AREIT’s S$12.75 bn portfolio comprising of 197 properties spanning across Singapore, Australia, UK and the US, which results in low asset concentration risk (no property accounts for more than 4.6% of revenue). AREIT’s geographically diversified portfolio and low tenant concentration risk (1,490 tenants, the largest tenant accounts for <4% of revenue) also helps to reduce the impact to the portfolio. Arrears for 1Q20 was below 1%, largely in line with historical numbers. Distribution visibility remains high – management does not think that they will need to retain distributions due to AREIT’s strong cash position S$561 million comprising of S$361 million in cash and S$200 million in committed facilities) to meet cashflow needs.

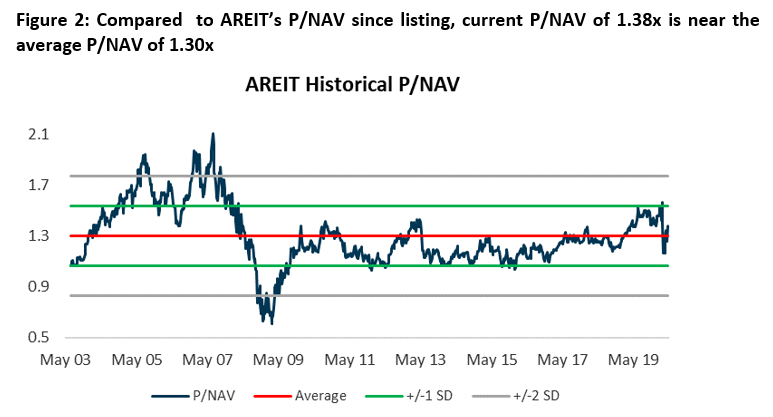

Despite its P/NAV of 1.6x which is on the high side, we think AREIT’s stability is due to tenant and geographical diversification and track record of DPU accretive acquisitions and AEIs justifies its premium. We think that AREIT’s low cost of borrowing (2.9%) and P/NAV which is at a premium presents a conducive environment for more acquisition.

Outlook

+7.7% rental reversions on SG lease in 1Q20, SG occupancy improved 1.4ppts to 88.6%. Portfolio occupancy also improved 0.8ppts to 91.7%. Reversions of 7.7% came in slightly above management’s guidance of mid-single-digit reversion, attributed to stronger reversions at business parks (+15.6%) and hi-spec (+12.2%). Of the 28,000sqm of new demand, 11% came from COVID-related demand (i.e. for storage of essential goods). The management is cautious about the leasing for the rest of the year, expecting reversions to come in flat for the full year.

AREIT’s geographically diversified portfolio and low tenant concentration risk (1,490 tenants, the largest tenant accounts for <4% of revenue) helps to reduce the impact to the portfolio. Arrears for 1Q20 was below 1%, largely in line with historical numbers. Distribution visibility remains high – management does not think that they will need to retain distributions due to AREIT’s strong cash position ($290mn in cash and cash equivalents and $200mn in committed facilities) to meet cashflow needs.

During April when the circuit breaker was enforced, a significant number of tenants remain in operation. The management shared that 40% of business park, 50% of hi-spec and 90%-100% of logistic and light industrial tenants were in operation. With the SG government tightening the definition of businesses providing essential service, a reduction in these numbers is expected. The relatively high percentage of operational tenants, especially in assets where telecommuting is not possible (light industrial and logistics), does give some comfort regarding the degree of business disruption and the number of tenants that may require rental deferments/waivers.

Singapore (71% of AUM)

C.$20mn in property tax rebates received from the Singapore government will be passed on to all tenants. Only F&B and retail tenant will receive an additional 1-month rental rebate from AREIT. These F&B and retail tenants account for <1% of SG portfolio GRI and the additional rebate will cost AREIT $2mn. The management is prepared to offer additional help, albeit in a target manner to tenants who are more in need of help.

Australia (13% of AUM)

Suspended rent collection from retail/F&B tenants (<1% of Australia rental income) from April until lockdown is lifted. 9 logistics and travel tenant have asked for rental relief.

United States (10% of AUM)

No rental rebates given to date, 16 tenants asking for rental rebates (c.$20m worth of rent)

United Kingdom (6% of AUM)

No rental rebates given to date. However, AREIT has allowed some tenants to change their rental payments from quarterly (3 months) in advance to monthly in advance, to help tenants with their cashflow.

Portfolio at risk

The management assessed that c.15% of tenants in the portfolio are SMEs or are in industries that are likely to be impacted (i.e. aviation, F&B, retail, Oil & Gas, hospitality/leisure).

Maintain ACCUMULATE with and lower TP of S$3.18 (prev. $3.31)

We incorporate the acquisition of the 28 US, 2 SG and 1 Australian business parks, the divestment of 3 SG assets and AEI of iQuest, and lower our occupancy assumptions to reflect weaker economic outlook.

DPU of 16.74 cents represents a yield of 5.6%. If we were to assume 1 month of rental rebates to paid out to SG tenants (c.$67mn), FY20e DPU would be 7.1% lower at 15.55cents, representing yield of 5.2%.

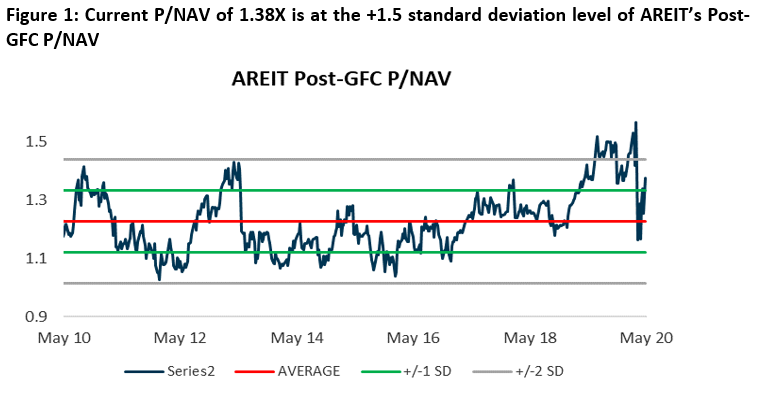

Despite its P/NAV of 1.38x which is at the +1.5 s.d. level (post-GFC), we think its’s stability is due to tenant and geographical diversification and track record of DPU accretive acquisitions and AEIs justifies its premium and will provide stable FY20e yields of 5.6%.

The Positives

The Negatives

Change in financial year-end from 31 March to 31 December

The current financial year is nine months from 1 April 2019 to 31 December 2019 (“FY2019”). Regular distributions to Unitholders of AREIT shall be for the six months ended 30 September 2019 and three-month period ended 31 December 2019. Thereafter, the regular distributions shall be made on a semi-annual basis for every six months ending 30 June and 31 December each year.

Outlook

Divestment of No. 8 Loyang Way 1 (Light Industrial) for S$27.0m at 14.4% premium to market value and 8.0% premium to purchase price is expected to be completed in 2Q19.

Businesses are likely to remain cautious given the weak manufacturing sector outlook and slowing GDP growth in Singapore. However, the future is not as bleak for AREIT given their low expiries of 9.3% of SG GRI for FY19 (FY20 19.7%). Industry occupancy has held steady at 89.3% for the past two quarters and the new supply of industrial space coming on to the market in FY19/20 (which represents 1.6%/3.6% of existing supply) is already 90%/39% pre-committed. This should provide industrial rents support amidst the softer economic outlook.

Upgrade to ACCUMULATE with a higher target price of $3.31 (prev $2.88).

Our higher target price is mainly due to the lower interest rate assumption and higher revenues forecasts from the persistent signing of above-market rents. Lower cost of equity of 6.6% has been applied in our DDM calculations (prev. 6.9%).

The Positives

The Negatives

Outlook

Three AEIs and a redevelopment project were announced. The redevelopment project will reposition 25 and 27 Ubi Road 4 from two light industrial assets into a one high specification industrial asset (with an enlarged floor plate). As high specification assets command higher rents than light industrial assets, repositioning the asset will allow AREIT to double rents while avoiding competing with future (light industrial) supply scheduled to come into the area. For context, market rents for high specification and light industrial asset are S$1.57 and S$3.15 psf per month respectively.

8% of the Australia portfolio’s GRI will be up for renewal in FY20, with 74% of lease expiries coming from Sydney. The rental market in Sydney is strong, having experienced 4% rental reversions for the past 12 consecutive quarters.

Downgrade to Neutral due to rich valuations; unchanged target price of $2.88

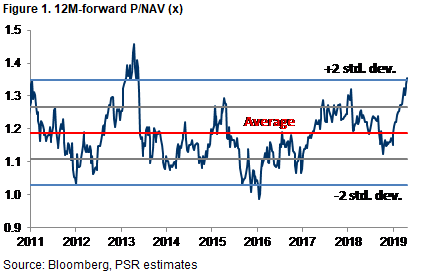

AREIT is currently trading at a rich valuation of P/NAV of 1.41x, which has crossed the +2s.d. level. We believe that such rich valuations are not well supported, given that the current rental market is more competitive with less robust rental reversions as compared to 2013 when similar valuations were last observed. 4Q12/1Q19 occupancy rate and rental index for the industrial sector were 93.7%/88% and 100/93.5 indicating a stronger market propping up valuations.

The Positives

The Negatives