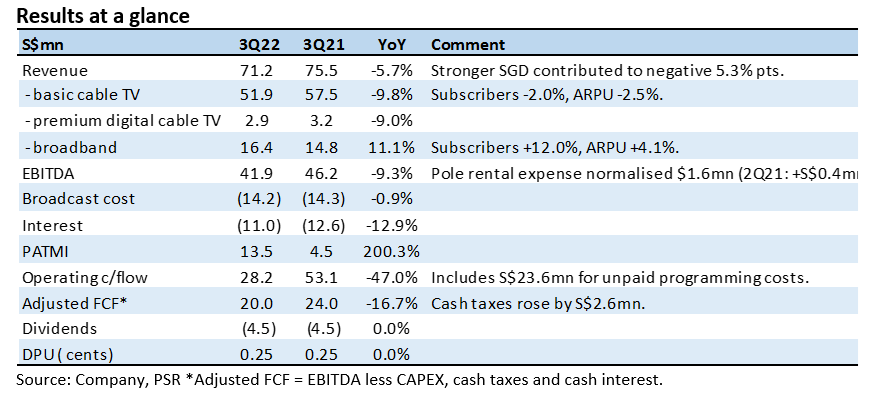

The Positive

+ High margin broadband growth. Broadband continues to grow strongly led by higher subscriber growth and improvement in ARPU. Monthly subscribers expanded by 9k to 307k as marketing efforts together with wireless operators continue to gain traction. ARPU has risen 4% YoY to TWD379 (S$16.72) with more subscribers opting for higher speeds.

The Negative

- Rising broadcast and content costs. Despite the 10% decline in basic cable TV revenue to S$51.9mn, content cost was stable at S$14.2mn. As a percentage of revenue, content cost in this quarter is a record 30.4% (excluding non-subscription revenue) of cable TV revenue.

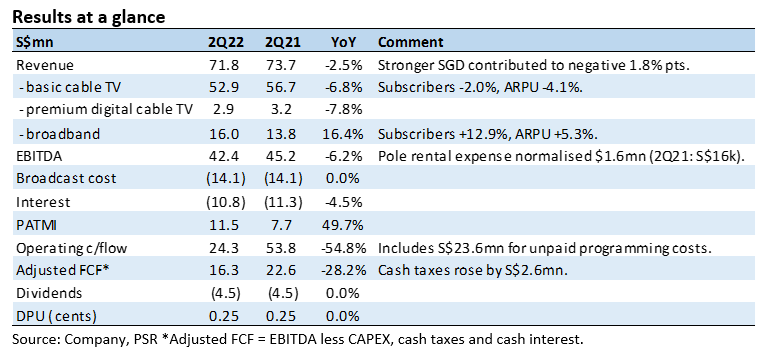

The Positive

+ Broadband growth with some 5G. Broadband revenue grew from both higher volumes and prices. Net subscribers added in 2Q22 were 9,000 (2Q21: +9,000) and ARPU rose 5% YoY to TWD377. Higher speed broadband plans are driving prices and partnership with mobile operators is helping to gain more subscribers. 5G backhaul revenue was disclosed at around $1.1mn in 1H22. This compares with the S$1.6mn in FY21.

The Negative

- Secular decline in basic cable. No change to the continuing weakness in basic cable TV revenue. It is the 18th consecutive quarterly decline of subscribers. Local content is still popular but piracy issues and aggressive IPTV are driving the loss of subscribers and the need to provide more discounts for customer retention.

Outlook

A competitively priced broadband that is 40-50% cheaper than peers together with a collaboration with mobile operators have driven both volumes and prices higher. While ARPU is 20% lower than cable TV, the margins are higher because there is no content cost. Content cost around 30% of cable TV revenue. Broadband can keep group revenue stable with 5G the new growth catalyst. Of the S$1.44bn debt, S$1.3bn is onshore TWD dollar debt of which 93% (or S$1.2bn) is hedged at a fixed rate of 0.94% until 30Jun25. The offshore S$154mn debt is floating rate of base plus 1.6-1.9%. A 100bps rise in SIBOR will increase interest by S$1.5mn, so not a significant impact to free cash flow.

Upgrade to BUY from ACCUMULATE with an unchanged target price of S$0.15

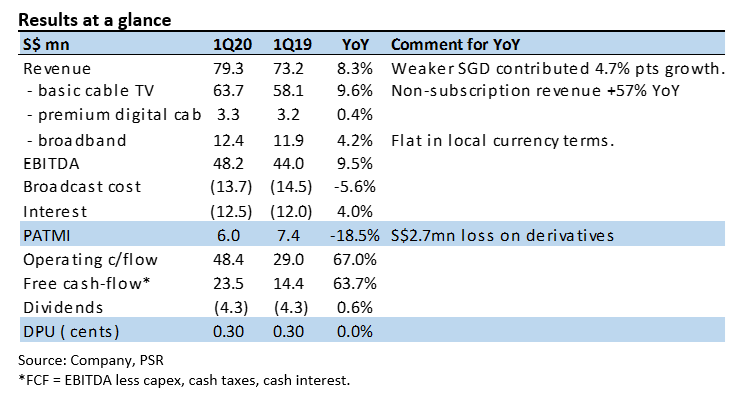

APTT’s attractive dividend yield of 8.5% is well supported by free cash flows. Our FY22e PATMI is raised S$14mn from lower effective tax, interest rate and depreciation assumptions.

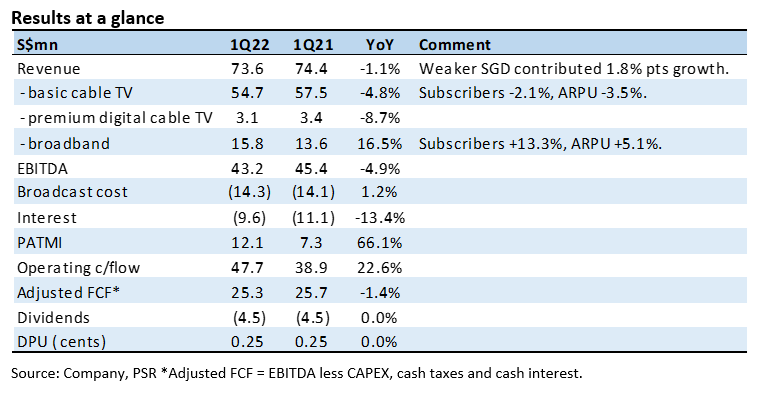

The Positive

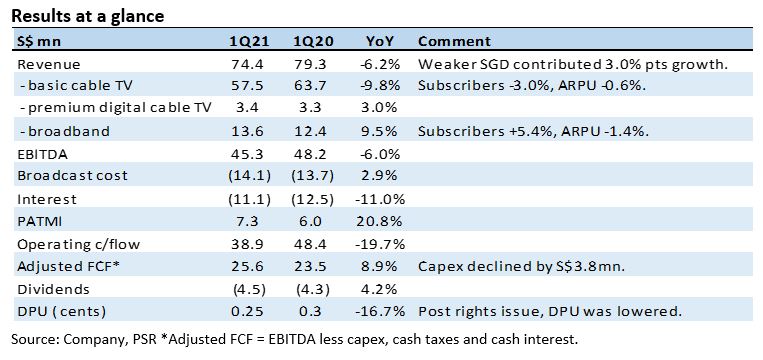

+ Broadband growth from higher prices and subscribers. Broadband added 7,000 subscribers (1Q21: +5000), while ARPU rose 5% YoY to TWD373. ARPU has expanded QoQ for the fourth consecutive month. Higher speed broadband plans of 300Mbps to 1Gbps are driving the rise in ARPU. Only 40% of its cable TV subscriber use APTT broadband.

The Negative

- Non-subscription cable TV revenue at a record low. Basic cable TV declined 5% YoY to S$54.7mn. The largest contraction was from the 10% drop in non-subscription revenue to S$7.5mn. Leasing channels to third parties (e.g. home shopping networks) is expected to deteriorate further as households shift their spending towards online shopping.

Outlook

We believe higher interest rates will not impact the ability to sustain dividends. From the S$1.5bn debt outstanding, around S$1bn has interest rates fixed or swapped to a fixed rate of 0.89%. The more expensive S$160mn Singapore dollar offshore loans bear an interest of 2.6%. We expect S$60mn of the loan to be pared down from the current $127mn cash holdings. The remaining S$300mn unhedged offshore loans will be partially hedged. Assuming a 1% rise in interest for unhedged S$500mn loans, increment interest is S$5mn. There is sufficient buffer from S$80mn annual FCF to cover the $18mn dividend. APTT aims to lower current net debt to EBITDA of 7.4x to 5x-6x to lower borrowing costs.

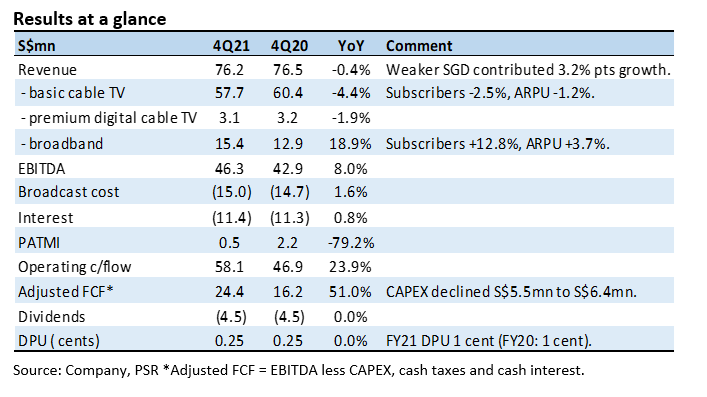

The Positives

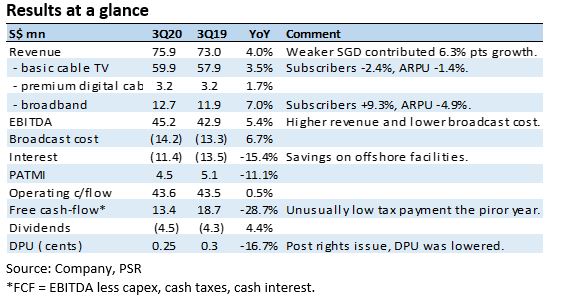

+ Broadband ARPU and subscriber numbers expanded. Net adds for broadband rose by 8,000 subscribers (4Q20: +2000). This is a major turnaround from a year ago. ARPU rose around 4% YoY to NT$369. This is also the third consecutive QoQ expansion in ARPU. The reason for the growth has been higher speed plans of 300Mbps to 1Gbps that the wireless operators (Far EasTone and Taiwan Mobile) are successfully signing up.

+ FCF grew. Free cash-flows rose S$8.2mn to $24mn. The jump was due to improvement in EBITDA (+S$3mn) and lower CAPEX (+S$5mn).

The Negative

- Higher interest expense expected. The interest rate hedges for the onshore debt of around NT$28bn (S$1.35bn) expire on 31Dec21. Hedges will be placed this year to lock-in rates for another two to three years until the 2025 refinancing. A 20 bps rise will increase interest expense by around S$2.7mn.

Outlook

The growth in broadband revenue is close to replacing weakness in cable TV. Higher interest rates in FY22 will be offset by lower content costs. The upside catalyst will be maiden revenues from 5G data backhaul from mobile operators.

Maintain ACCUMULATE with an unchanged target price of S$0.15

APTT pays an attractive dividend yield of 7.4% well supported by cash flows.

The Positives

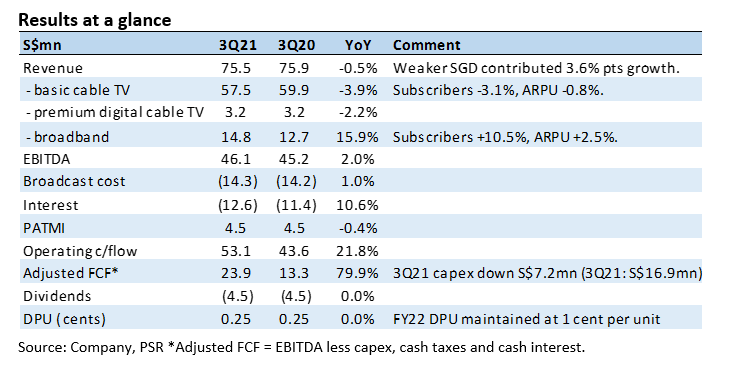

+ Free cash-flows grew due to lower capex. Free cash-flows generated was $24mn, providing sufficient support to the quarterly dividends of S$4.5mn. Growth in cash-flows stemmed from the S$10mn decline in capital expenditure and stable EBITDA.

+ Broadband revenue growth accelerating. 3Q21 broadband net adds in subscribers was a record 10,000 to 274,000. Attractive pricing plus partnerships with various mobile operators helped. The rise in net adds was accompanied by an improvement in ARPU. Joint marketing with mobile operators has allowed APTT to widen their pool of customers. Mobile operators can sell bundled plans with APTT fixed broadband.

The Negative

- Core cable secular weakness intact. Cable TV subscribers have been on a decline for more than 15 quarters. The main factors are piracy, aggressive IPTV prices and a saturated cable TV market.

Outlook

Despite improving cash-flows, APTT will maintain DPU at 1 cent for FY22. The focus is to reduce borrowings and refinance the more expensive offshore debt (interest margin 4.1% to 5.5%) with onshore facilities as net debt to EBITDA metrics improve.

Downgrade from BUY to ACCUMULATE with an unchanged target price of S$0.15

Our downgrade in recommendation is due to the recent share price appreciation. APTT pays an attractive dividend yield of 7.4% well supported by cash flows.

The Positive

+ Growth in broadband. Broadband revenue expanded almost 10% YoY in 1Q21. Net subscriber adds were 5,000, the highest in four quarters with ARPU almost unchanged. APTT has been partnering wireless operator shops to distribute their high-end 500MB/1GB broadband plans since end-2019.

The Negative

- Cable TV still shrinking. Cable TV revenue declined around 10% YoY in 1Q21. Subscription revenue was stable at S$49mn but non-subscription dropped 43% to S$8.4mn due to an absence of in-house content sales and lower channel leasing revenue. Both were popular during the lockdown in Taiwan.

Outlook

We expect FCF to be stable despite weaker revenue as capex is trending down the next two years. Investments in the past three years have driven homes to fibre node density from 750 to 250 currently. This should be sufficient to meet demand for 5G data backhaul. We lower our FY21e capex by 10% to S$45mn.

Maintain BUY and target price of S$0.15

Current dividend yield of 9% from a S$18mn payout is well supported by FCF of S$77mn. Our FY21e earnings forecast is largely unchanged.

The Positive

+ Lower capex from FY20. YTD capex is down almost S$10mn. APTT is guiding for lower capex from 2020 onwards. Hefty investments to increase fibre capacity are slowing down. These investments were made to raise the bandwidth of its broadband offerings and in preparation for its 5G data backhaul business from mobile operators.

The Negative

- Cable TV still softening. Cable TV subscribers were down 5,000 this quarter (2Q20: -4,000). The churn was due to piracy and competitively-priced IPTV. Mitigating the decline is the growth in both premium digital TV and broadband. Total subscriber base is up 2% YoY to 1.19mn.

Outlook

Financials this year have been lifted by a strong Taiwan dollar, by around 6%. Operationally, we are incorporating lower revenue and EBITDA for FY21e, to factor in lower cable TV revenue. However, FCF should rise with lower capex. APTT reiterates that 5G data backhaul will be an opportunity and the key component of its broadband business in the next few years.

Maintain BUY and TP of S$0.15

Our BUY remains premised on a yield of 8.5% and sustainable operating cash flows. Annual FCF of S$45mn is expected to cover dividend payouts of S$18mn, with upside potentially from 5G data backhaul revenue. We have not modelled 5G in our numbers pending more data points from APTT.

The Positives

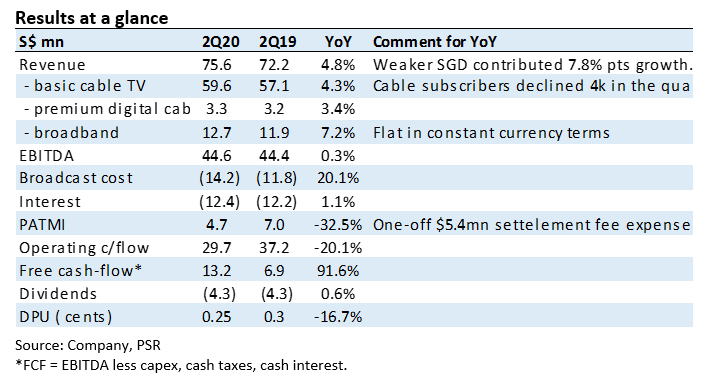

+ Free-cash flows (FCF) remains healthy. FCF of $13mn this quarter more than covers the dividend payment of $4.3mn. Dividends payable will rise to S$4.5mn per quarter after the higher share base post rights issue. The higher FCFs was due to a fall in capex by around S$5mn YoY.

+ Broadband subscriber still grows. Broadband subscribers continue its steady climb for the eleventh consecutive quarter to 246,000. Revenue rose 7% YoY but down 0.6% in constant currency terms following ARPU decline of 9% YoY compensated by subscribers rising 9.3% YoY.

The Negatives

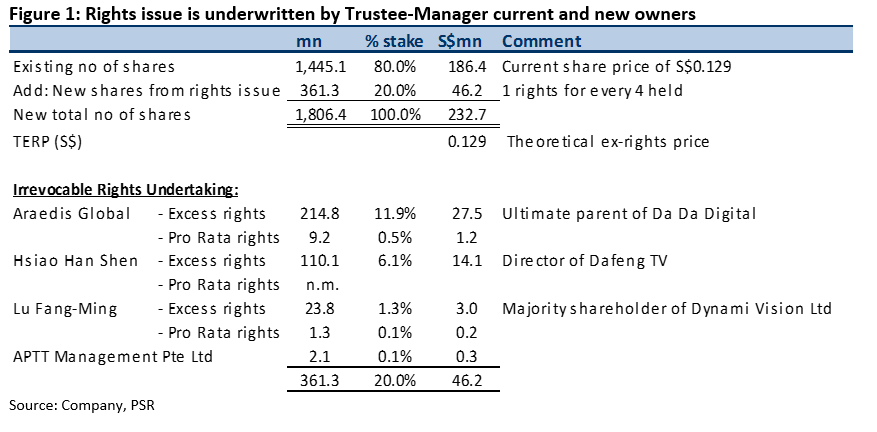

- Dividend cut to 0.25 cents per quarter. As expected, following the rights issue, APTT lowered dividends to 0.25 cent per quarter (previously 0. 30 cents). APTT will announce their FY21 dividend policy in 3Q20 results.

- One-off S$5.4mn settlement expense. There was a S$5.4mn one-time programming settlement fee paid by APTT to the content agents. It is additional programming cost after negotiations that started in 2019.

- Jump in broadcasting cost. There was an unexpected jump in broadcast and production cost. The reason was timing in accruing the cost but will stabilize on an annual basis. We are assuming programming expense was lower last year on expectations that negotiations with broadcasters for lowering cost would be successful. This did not materialize.

Outlook

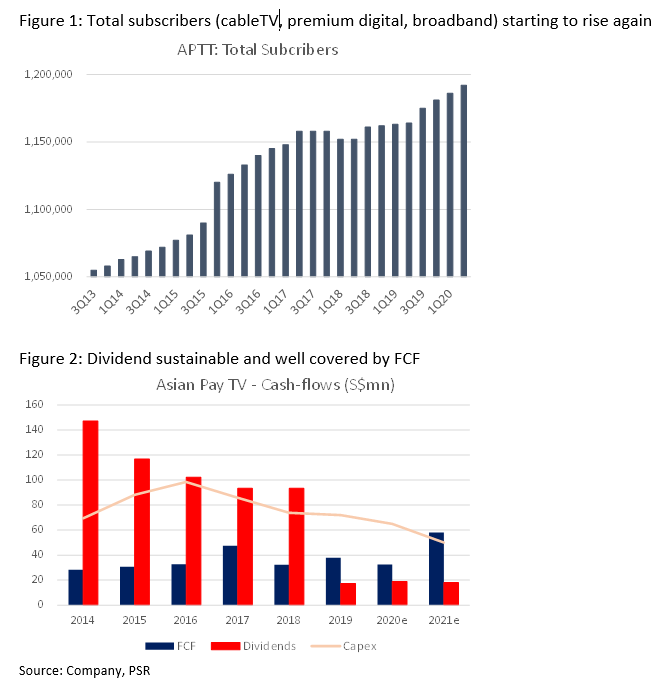

Cable TV remains the weak spot with subscribers contracting around 4,000 per quarter. But total subscribers for APTT, including broadband and premium digital TV, have started to rise (Figure 1). Total subscribers are rising around 2% per year but blended ARPU* is declining by 5%. We still expect total revenue to contract. We raised our EBITDA forecast by 4% due to the change in foreign exchange assumption. Other changes in our forecast were higher broadcast and programming cost, the inclusion of the settlement fee and incorporating proceeds from the rights issue.

*Blended ARPU based on total revenue less total subscribers

Maintain BUY and unchanged target price of S$0.15

The three reasons for our BUY recommendation are as follows:

The Positives

+ Revenue is better than expected. We were modelling around 4% YoY decline in revenue. Excluding the currency impact, revenue rose 3.6% in local currency terms. Non-subscription jumped 57% to S$14.9mn due to the sale of certain in-house content to channels plus additional advertisement revenue. Such revenues are lumpy.

+ Broadband revenue stable. Broadband revenue rose 4% but was flat in constant currency terms. ARPU declined 12% to NT$350 per month (S$16.6), but new subscribers responded to the lower price plans by expanding 10% YoY to 242k. Another positive was that the fall in ARPU of NT$6 on QoQ basis was the smallest in seven quarters.

+ Capex well contained so far. 1Q20 capex dipped to S$11mn or 14% of revenue. We were modelling 23% of revenue or S$65mn. Nevertheless, the company did highlight that there was some deferral in capex and 1Q20 fall is not representative of the expected downtrend in capex.

The Negatives

- Effective DPU has been cut. Following the rights issue, APTT will be lowering their DPU from 0.3 cents to 0.25 cents per quarter. The cut in dividends is only effective upon completion of the rights issue. Also, APTT will review its FY21 dividend policy in their 3Q20 results.

Outlook

Broadband is the bright spot with the growth in subscribers offsetting the weakness in ARPU. Core cable TV remains problematic with cable TV subscribers falling close to 3% p.a. Therefore, the ability to reduce capex will be critical to offset the falling cash-flows from cable TV business.

Upgrade to BUY and target price lowered to S$0.15 (previously S$0.165)

We were disappointed with the 16.7% cut in DPU accompanying the rights issue. The effective dividend yield drops by around 1.5% points post announcement of the rights issue. Nevertheless, we are upgrading our recommendation from NEUTRAL to BUY:

The larger driver to the share price in future will be the ability to generate new revenue streams from data backhaul services offered to wireless operator rolling out 5G. APTT has said revenues will be material, but there is little visibility on the quantum and timeline.

Details of the rights issue:

The Positives

+ Cable TV ARPU flat QoQ. ARPU finally stabilise QoQ after falling for 13 consecutive quarters. However, subscribers are still contracting at a rate of around 5,000 per quarter.

+ Broadband revenue turning more stable. Another positive operating data was the flat QoQ broadband revenue. Subscribers responded well to the lower prices, as a result, Broadband subscribers rose 10% YoY in 4Q19. However, the pricing strategy resulted in a 12% YoY fall in ARPU. Nonetheless, this is a high margin business as there is no content cost and only the modem cost during installation.

+ Content cost falling to stabilize EBITDA. The run-rate for broadcast cost was around S$16mn per quarter two years ago. This has declined to around S$13mn in FY19. 4Q19’s content cost was down almost 11% YoY.1

The Negatives

- FY19 capex still elevated. FY19 Revenue and EBITDA is down around 6% YoY. However, capital expenditure remains unchanged at $75mn. Capex was incurred to deploy more fibre in the network, especially for the data backhaul business. Guidance is for capex to trend down in FY20e. Another drain on cash-flow was $20mn spent on intangibles in FY19.

Outlook

There are some positives we can look forward to in FY20e for APTT – (i) Further signs of stability in operational data which will signal business sustainability; (ii) Capital expenditure (and investments in intangibles) will start to trend downwards, as guided by APTT; (iii) Revenue from data backhaul from Taiwan mobile operators begin to contribute more meaningfully to APTT.

Maintain NEUTRAL and target price unchanged at S$0.165

Our target price of S$0.165 is maintained. We raised our FY20e EBITDA by 3% as we revised our revenue estimates upwards, and lowered further content cost. We peg APTT at around 10x EV/EBITDA. This is a 10% valuation discount to its much larger Taiwanese peers (Figure 2).

We look for further signs of revenue or EBITDA to stabilise before any re-rating and valuation discount to peers to be even narrower.