The Positives

+ New homes sales revenue the anchor for growth. Commission revenue from new launches rose 16% YoY in 1H20. It was the fastest-growing revenue segment for the company.

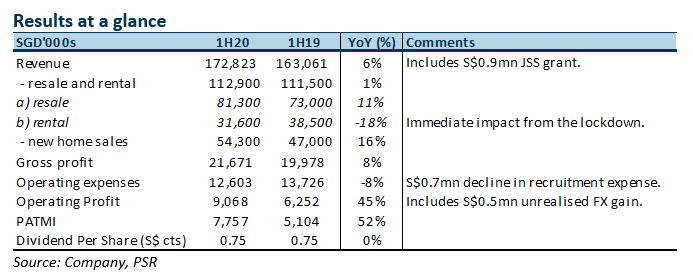

The Negatives

- Interim dividend unchanged. Despite the improvement in earnings, the interim dividend was kept unchanged. Despite the rebound in property transactions in July and August, concerns remain whether the weak economy will hurt buying sentiment in 4Q20.

Outlook

2H20 will bear the brunt of the lockdown especially new home sales and resale. There was no viewing of units from 7 April to 19 June. Another S$0.7mn from JSS grant can be expected in 2H20. A positive has been the company efforts to expand more aggressively the ERA model into SE Asia, such as Malaysia, Indonesia and Vietnam. This will lay the foundation for future growth outside Singapore.

Downgrade to NEUTRAL from ACCUMULATE with a lower target price of S$0.365 (prev. S$0.55)

We are lowering our recommendation due to the weaker than expected results and reducing our earnings estimates for FY20e and FY21e.

The Positives

+ New home sales surged 79% YoY. The spike in home sales volumes was in comparison to new home sales a year ago, due to the fall out from the July 2018 cooling measures. Revenue from new homes sales in 4Q19 was the 2nd highest in history. The lag between the transaction date of the property and revenue recognition is 3 to 6 months depending on the project.

The Negatives

- Provision for doubtful debts jumped in 4Q19. Provision for doubtful debts swung from write-back of S$300k to an allowance of S$869k. APAC has a policy of making full provision of a trade receivable when due more than a certain period outstanding. These are one-off provisions likely from resale and do not appear systemic. Disputes over commission are some triggers for the provision. Exposure is offset by a trade payable write-back in cost of services for the amount due to the agent. Total exposure is 10% of the provision.

- Taxes higher in 4Q19. The effective tax was 21% compared to 14% last year due to certain allowances not allowable. Full-year the effective tax was 19.4% (FY18: 17%).

- Dividends cut by 50%. Final dividend was cut 50% to 1.25 cents in-line (FY19: 2 cents) with the drop in earnings. Dividend payout ratio policy is still at least 50%.

Outlook

We expect earnings to rebound in FY20e. Transaction volumes are picking-up across all three core business segments – new home sales, HDB resale and private resale. Some of the other non-macro drivers to growth include agency force rising 8.6% YoY to 7,048 agents, ERA APAC Centre turning to profitability and secured agency rights to 25 projects for 2020 so far. Unclear at present is whether APAC will subsidise agency fees of S$230 per year. It is a sizeable S$1.6mn out of pocket expense for the 7,000 plus agents.

Other updates:

New Home Sales

Resale market

Covid-19

Maintain ACCUMULATE with an unchanged target price of S$0.55

We maintained our recommendation and target price. Our FY20e earnings cut by 13% on higher expenses and effective tax rate.

The Positives

+ Commission from rental has been resilient. Revenue from rental transactions has been resilient.

+ Agency force still expanding steadily. The agency force is now 7,034, an 8% rise for this year and almost 20% improvement from January 2018. Smaller agencies do not get access to new project launches. The almost 40% collapse in secondary transaction will encourage agents to shift to larger agencies.

The Negatives

- Operating expenses higher than expected. Expenses were hurt by two major items – annual agency renewal fee (S$250 per agent) to be borne by the company and losses from the newly acquired ERA APAC Centre property. Both items cost the company almost S$2mn. The APAC Centre should turnaround as the property is now fully occupied and is making better rental rates.

- New homes sales weaker than expected. Revenue from new home sales has been weaker than some peers. The extension of options may modestly overstate actual number of property transactions. Some investors may be willing to risk 1.25% (or 25% of 5% booking fee) of property value to buy time if the property market recovers.

Outlook

It will be a better year in 2020. Transaction volumes are recovering post cooling measures and there is a large pipeline of new projects. In 1H20, there will be at least 15 new projects or 5,181 units to be marketed.

Downgrade to ACCUMULATE with a lower target price of S$0.55 (prev. S$0.58)

Our lower target price is in-line with the cut in our earnings estimate in FY19e/FY20e.