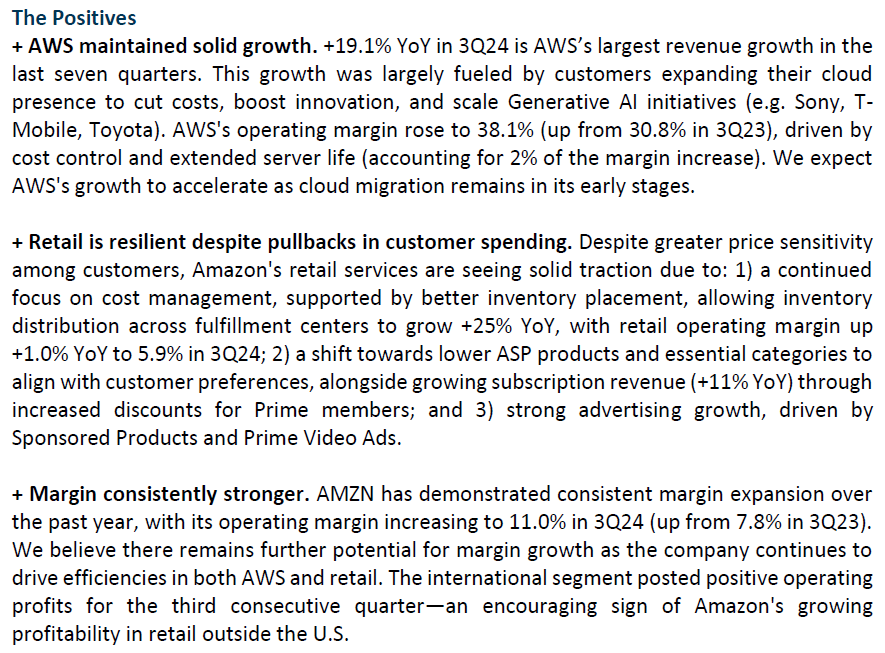

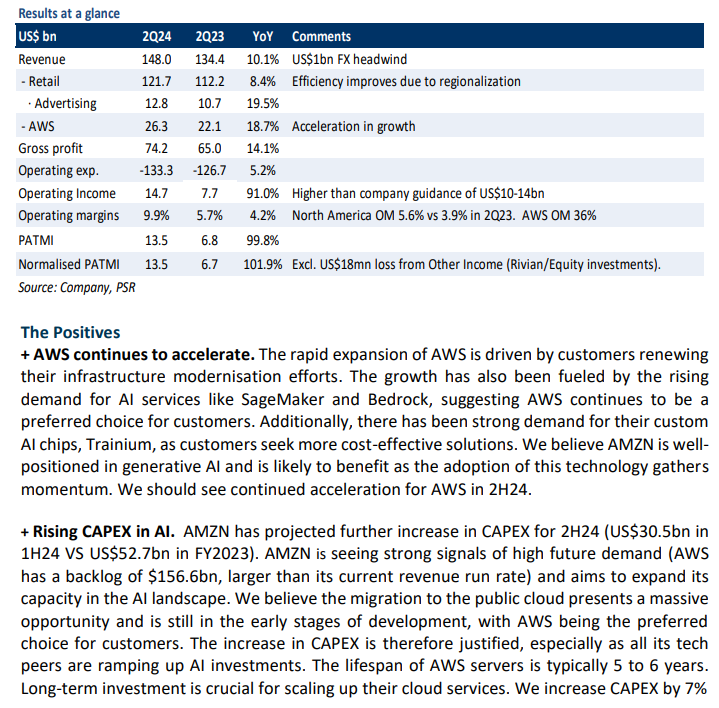

The Positives

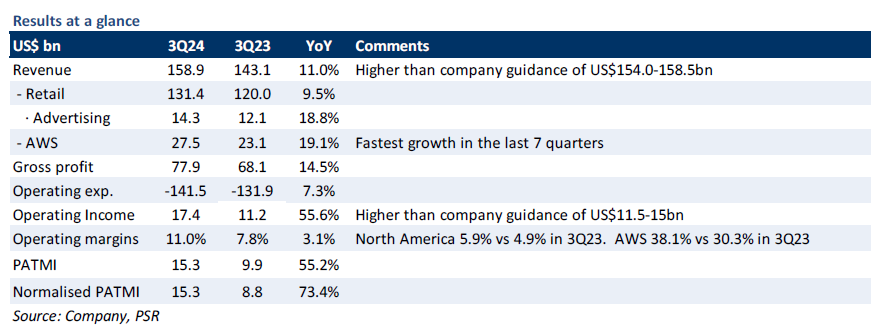

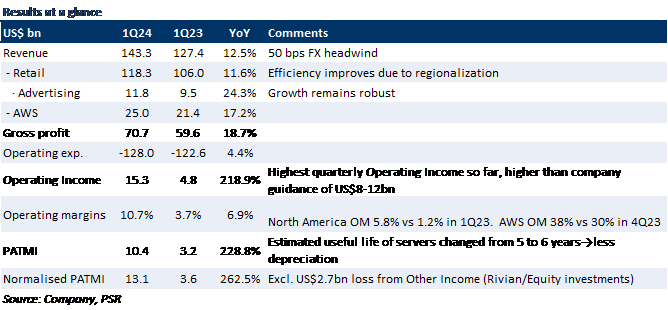

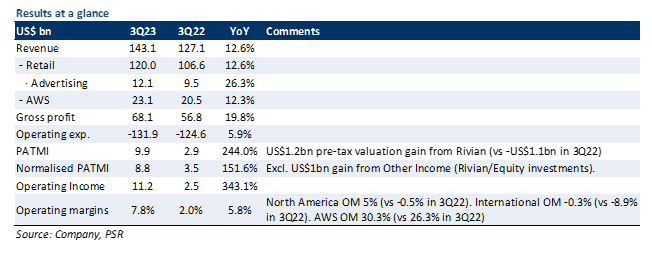

+ AWS showing more signs of reaccelerating. Revenue of US$143 bn is at the top-end of the company’s guidance, with most of the outperformance driven by AWS (13.2% YoY) and Advertising (26.8% YoY). The high growth of AWS is fueled by customers migrating workloads from on-premises to the cloud. Gen AI services are seeing a strong demand signal, evidenced by extended contracts and larger commitments (e.g., Perplexity AI/Workday). Management has disclosed a significant increase in Capex for 2024 to bolster AWS growth, indicating the company's confidence in AWS expansion prospects.

+ Improvement in margins. AMZN continues reaping the benefits of regionalizing its operations and has shown progress in bringing the cost structure down further (e.g. consolidation of units into fewer boxes). Its first-quarter operating income is at an all-time high of $15.3 bn, beating the company’s top-end guidance of US$12.0 bn. Consequently, the operating margin stood at 10.7% (reaching double-digits for the first time), a substantial increase from 3.7% in 1Q23. Notably, the international business achieved positive operating income for the first time in over two years. AWS’s operating margin reaches an all-time high of 37.6%.

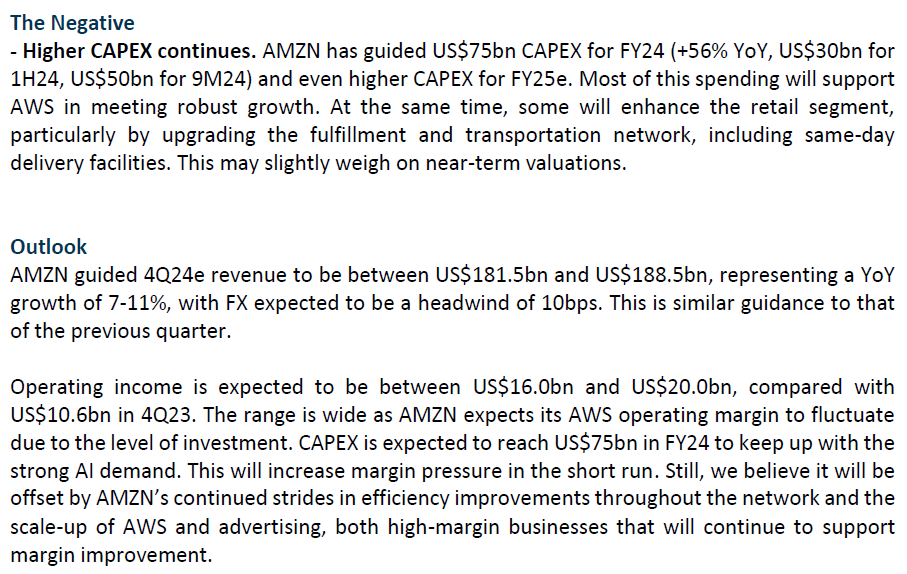

The Negative

- Potential pullback in consumer spending. AMZN's hinted at potential signs of a slowdown in consumer spending. Despite growth in retail revenue, management noticed that customers are cautious about their expenditures, seeking bargains and opting for lower-priced alternatives. This trend appears to persist into the second quarter, especially for the European market. AMZN has guided a revenue growth between 7% and 11% in 2Q24e, including an unfavourable foreign exchange impact of 60 bps.

The Positives

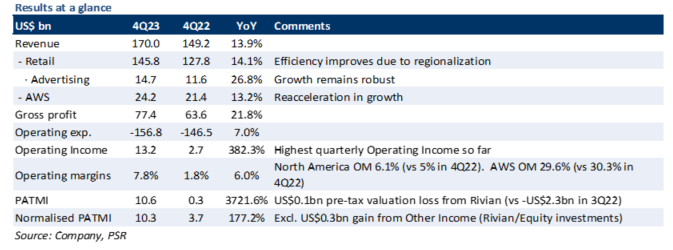

+ Retail operating income was driven by regionalization and efficiency. AMZN’s retail operating income improved by 382% YoY. North American/International segment’s operation income increased from -US$0.2bn/-US$2.2bn in 4Q22 to US$6.5bn/-US$0.4bn in 4Q23, primarily driven by cost-cutting and lower transportation rates. North America benefit from regionalisation and expansion of last-mile delivery facilities, increasing same day deliveries by 65% YoY. Improved inventory placement drove faster deliveries and lowered transportation distances (cost to serve declined by >US$0.45 per unit). We foresee revenue growth to continue in the long term as lower costs lowers ASPs, improving affordability. This, together with faster delivery speed, should lead to greater purchase consideration & frequency.

+ Advertising growth remains robust. Advertising revenue grew 27% YoY in 4Q23, primarily driven by sponsored products with higher ads relevancy. AMZN benefits from being able to collect its own first-party data, and has been able to efficiently convert this data into more efficient and relevant ads for consumers, driving up ROI for advertisers. We believe advertising remains AMZN’s great growth opportunity as it has the ability to scale alongside its retail business, advertising only contributes 8% of the company’s total revenue presently.

+ AWS seeing stabilization in growth. AWS revenue was up by 13.2% YoY in 4Q23, compared to 12.3% and 12.2% YoY in 3Q23 and 2Q23. AWS revenue growth has dipped in previous quarters due to customers moderating their spending. The recent acceleration in growth rate suggests that this effect has bottomed out. Accelerated new deals and backlog conversion is expected to drive growth. Management has indicated that the acceleration in growth will continue into FY24, driven by accelerating demand in Gen AI. AWS’ order backlog grew ~40% YoY in 4Q23.

The Negative

- Nil.

The Positives

+ Margins continue to improve. Gross and operating margins expanded by ~300bps and ~600bps YoY, respectively. Operating income more than tripled YoY to a record level of US$11.2bn, beating the top-end of US$8.5bn company guidance. The retail business benefitted from the lower cost to serve because of its fulfillment network regionalisation initiative in the US, easing inflationary pressure in line-haul, ocean, and rail shipping rates, as well as the strong 26% YoY growth of its advertising business (7% of revenue). AWS operating margin also expanded by 600bps QoQ and 400bps YoY, back to the level last seen in 2Q22, primarily driven by headcount reductions in the business and lower energy costs.

+ AWS growth stabilised. Segment revenue was up by 12% YoY, in line with management’s guidance of stabilising growth. Despite customer cost-optimisation efforts being relatively elevated compared to 2022, it is starting to meaningfully attenuate as more companies shift their focus towards deploying new workloads. Management expects the rate of such optimisations will continue to ease in the next several quarters. Furthermore, AMZN indicated that it signed several deals with customers that will take effect in 4Q23, including those where existing customers expand their AWS deployments and move away from short-term contracts to commitments ranging between 1-3 years. Hence, we expect growth will start to re-accelerate in the near term.

+ Strong free-cash-flow. Trailing-twelve-months (TTM) FCF was US$21.4bn, tripling QoQ and a US$41bn improvement YoY. This was driven by the increased operating income in both retail and AWS segments, improved leverage on fixed costs and working capital efficiency.

The Negative

- Nil.

The Positives

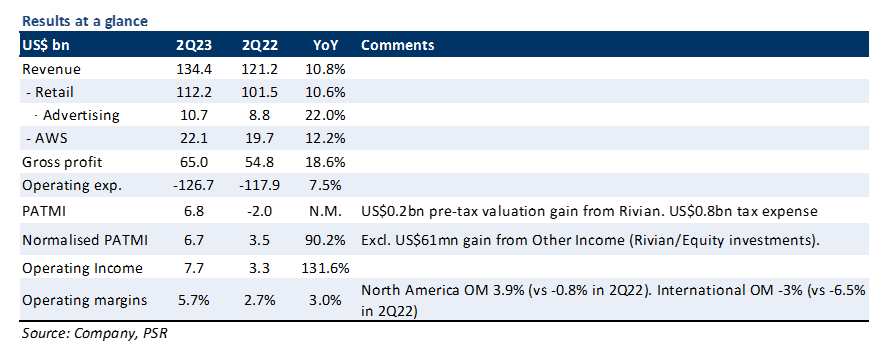

+ Revenue beats guidance. 2Q23 revenue grew 10.8% YoY to US$134.4bn, above the top end of US$133bn company guidance. International segment revenue growth re-accelerated QoQ as it was up by 9.7% YoY, from a growth of 1% YoY in 1Q23, as macro conditions continue to improve. Advertising growth also improved, increasing by 22% YoY (vs 21% in 1Q23) to US$10.7bn (7.9% of total revenue), with Amazon’s performance-based advertising offerings being the largest contributor. AWS was up 12% YoY, slightly above company guidance of 11%.

+ AWS growth stabilising. Despite customers continuing to optimise costs in 2Q23, management said it has started seeing some customers shift their focus towards innovation and new workload deployments. Amazon sees the trend continuing into 3Q23 and it expects the optimisation efforts to ease further, suggesting that growth has bottomed out. Hence, we believe there is a possibility of re-acceleration in 2H23, particularly in 4Q23, as Amazon rolls out its new AI services while customers gradually increase their spending on AWS.

+ Efficiency enhancements drive operating leverage. Gross and operating margins each expanded by ~300bps YoY, with operating income more than doubling to US$7.7bn from US$3.3bn in 2Q22. This was driven by the reduction in the cost to serve (shipping and fulfillment costs) as Amazon is seeing easing inflation headwinds, particularly in fuel prices, linehaul rates, ocean and rail rates. In addition to that, it is also benefitting from the headcount reductions (which fell by 4% YoY or 62,000 employees) and a lower CAPEX. The company’s regionalisation initiative is paying off as it reduced the number of touches for packages by 20% and miles traveled to deliver packages to customers by 19%, resulting in less transportation costs and faster delivery speed.

+ Strong free-cash-flow. Trailing-twelve-months (TTM) FCF was US$7.9bn, the first positive FCF since 3Q21. The improvement was driven by increased operating income as a result of higher operating leverage and the moderating inflationary pressure, as well as lower CAPEX.

The Negative

- Nil.

The Positives

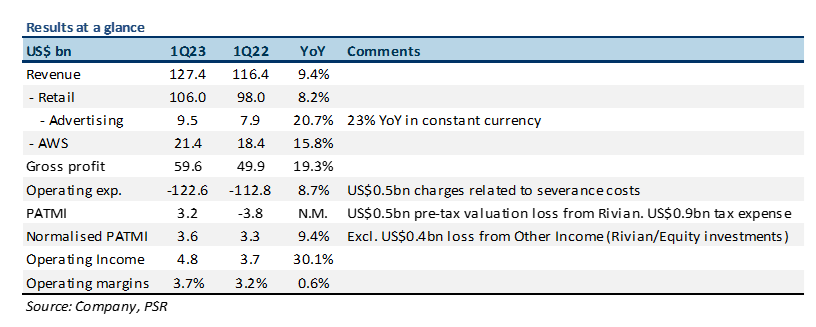

+ Revenue beats guidance. 1Q23 revenue grew 9.4% YoY (11% in constant currency) to US$127.4bn, above the top end of US$126bn company guidance. International segment revenue increased 1% YoY following negative growth since 4Q21 (-8% YoY in 4Q22 and -6% in 1Q22) as inflation in Europe starts to decline. Advertising revenue grew 21% YoY (23% in constant currency) to US$9.5bn (7.5% of total), reflecting continued strong demand for its advertising services. AWS was up 16% YoY, in line with guidance despite facing cloud spending optimisation efforts by customers.

+ Improvements in margins. Operating income was US$4.8bn, up 30% YoY and slightly above company guidance of US$4bn, as margins expanded by 190 bps QoQ and 60 bps YoY, despite incurring severance-related charges of US$0.5bn. North America segment posted an operating income of US$898mn (1.2% margins vs -2% in 1Q22) after recording losses since 4Q21, while International segment’s negative margins also declined QoQ to -4.3% from -6.5% in 4Q22. These improvements were due to revenue growth outpacing growth in fulfillment and shipping costs as inflationary pressure eases with reduction in shipping rates, fuel, and electricity prices. The margin expansion was partially offset by QoQ contraction in AWS to 24% from 24.3% in 4Q22 as customers opted for lower-tier products.

The Negative

- Further growth deceleration for AWS in 2Q23. AWS YoY growth for April was estimated to be ~5% lower than that of 1Q23 as enterprises continue efforts in optimising their spending and management expects this trend to persist at least through 2Q23, implying a further growth deceleration to ~11%. However, Amazon reiterated that its new customer pipeline remains robust and there is a strong ongoing set of workloads that is migrating to AWS. Management also indicated that its existing customers are extending their expiring contracts and will continue to engage with AWS.

The Positives

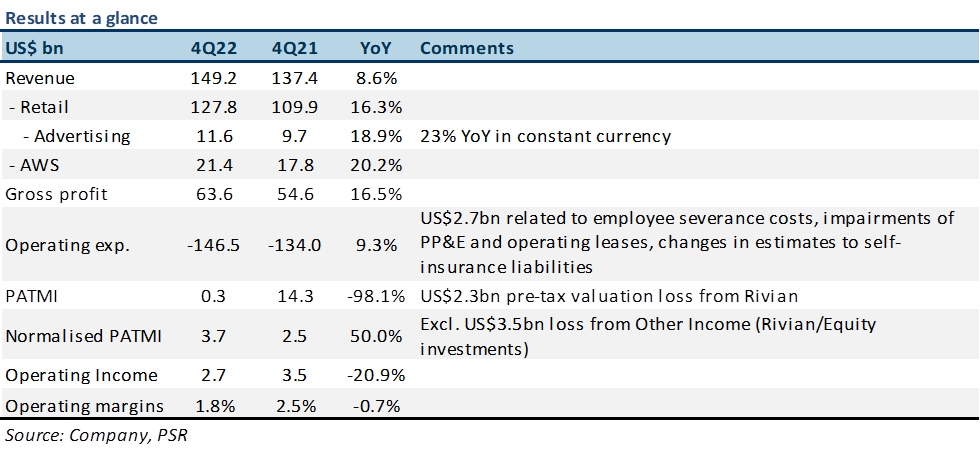

+ Revenue beats guidance. 4Q22 revenue grew 8.6% YoY (12% in constant currency) to US$149.2bn, slightly above the top end of US$148bn company guidance. Retail sales were boosted by Prime Early Access Sales in October and Thanksgiving-Cyber Monday holiday weekend sales outperformance. Prime saw record new sign-ups during Rings of Power launch window. AWS remains the fastest growing segment, up 20% YoY, and was the sole contributor to the overall operating income of US$2.7bn.

+ Advertising continues bucking industry trends. Advertising grew 19% YoY to US$11.6bn (7.7% of total 4Q22 revenue) while competitors continue to see advertising revenue decline. Amazon continued to see inflow of advertising demand from sellers, vendors, and brands during the competitive holiday season, even as sellers were being frugal with their marketing budgets in the current macroeconomic environment.

The Negative

- 1Q23 AWS growth expected to decelerate. AWS YoY growth for January 2023 was in the mid-teens as enterprises continue their efforts in optimizing their spending by opting for lower-cost products. Management expects these optimization efforts to be the key headwind for AWS over the next few quarters. However, Amazon indicated that its new customer pipeline remains robust as many are putting plans in place to migrate to the cloud and commit to AWS for the long term.