Amazon.com Inc. – Custom silicon a structural advantage

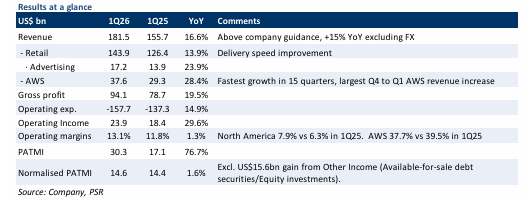

- 1Q26 revenue was in line with expectations, while 1Q26 Adjusted PATMI underperformed due to higher tax expense. 1Q26 Revenue/Adjusted PATMI were at 23%/18% of our FY26e forecasts.

- The revenue growth is mainly pushed by AWS (+28% YoY), the fastest growth in 15 quarters and advertising (+24% YoY). AMZN’s guidance for CAPEX spend in FY26e remains unchanged at US$200bn. Normalised PATMI was flat YoY due to higher tax expense.

-

We downgrade our recommendation from BUY to ACCUMULATE due to recent stock price movement, with an unchanged target price of US$280. Our estimates remain unchanged, with a WACC of 5.6% and a terminal growth rate of 5%. We think Amazon is well-positioned in AI, leveraging its full-stack capabilities, including custom chips (Trainium and Graviton), partnerships with OpenAI and Anthropic, and a unique dataset to drive ecosystem stickiness and capture long-term growth.

The Positives

+ AWS growth reaccelerates further with strong AI-driven demand. AWS revenue +28% YoY,

the fastest in 15 quarters, driven by both core cloud migration and expanding AI workloads,

including model training, inference, and agentic applications. Bedrock continues to gain

traction, with 170% QoQ growth in customer spend, reflecting strong adoption. Demand

visibility showing sustained growth momentum, with a $364bn backlog (~+93% YoY, excluding

the Anthropic deal). Management reiterated its commitment to continued heavy CapEx

investment, with high confidence in monetisation given that a substantial portion of capacity

is already backed by customer commitments. AWS operating margins declined 180bps due to

elevated CapEx.

+ Custom silicon emerging as a structural advantage. AMZN’s in-house chip business

continues to scale rapidly (+40% QoQ), placing it among the top 3 data center chip businesses

globally. Trainium chips deliver 30–40% better price performance vs alternatives, and are

already largely sold out across current and next-generation capacity, with strong multi-year

commitments from major AI labs. Management highlighted that custom silicon could save

tens of billions in CapEx annually and provide several hundred basis points of margin

advantage, reinforcing its role as a key differentiator. This vertical integration strengthens

AWS’s cost structure and pricing power, particularly as AI workloads scale. We believe this

positions AMZN well for further data center market leadership

+ Retail and fulfilment efficiency driving operating leverage. AMZN continues to improve

efficiency in its retail business, with unit growth (+15% YoY) outpacing cost growth (outbound

shipping costs +12% YoY, fulfilment expenses +9% YoY). Perishable sales have scaled over 40x

YoY and are driving higher engagement (AMZN is now the #2 grocer in the U.S.), with

customers ordering nearly 3x more items and spending >80% more when including groceries,

reinforcing larger basket sizes and supporting both customer experience and operating

leverage.

Amazon.com Inc. – US$200bn CAPEX in FY26

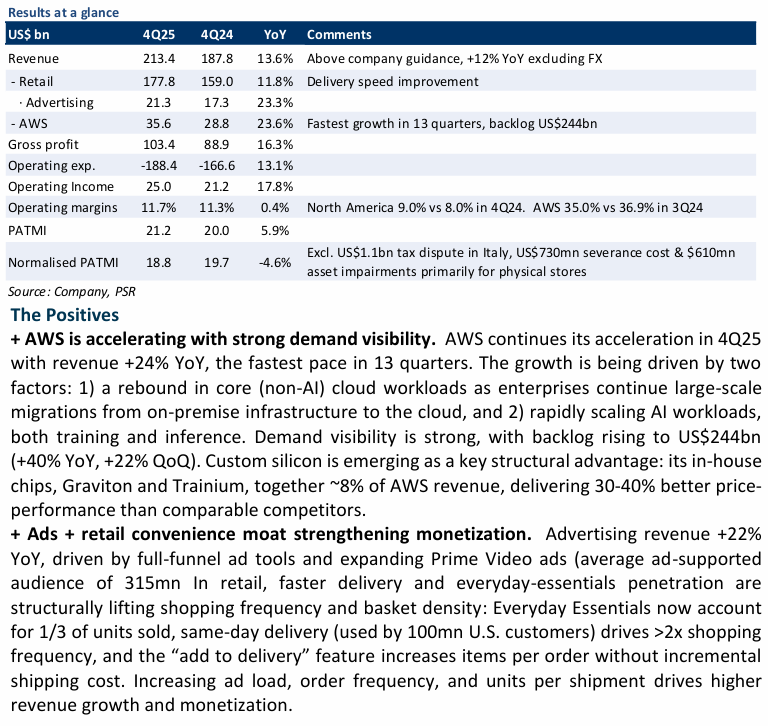

- 4Q25 adjusted PATMI were in line with expectations, while revenue outperformed due to strength in AWS (+24% YoY), the fastest growth in 13 quarters. FY25 Revenue/Adjusted PATMI were at 101%/100% of our FY25e forecasts.

- TTM free cash flow -71% YoY due to increased investment in AI. AMZN has guided +60% YoY CAPEX spend in FY26e.

- We increase our FY26e revenue by 2% and PATMI by 4% to account for the growing demand in AWS as well as continued cost discipline efforts in the retail segment. We increase our FY26e CAPEX by 30% to account for the higher-than-expected AI investment. We also reduce equity beta from 0.8 to 0.75 because AMZN’s earnings volatility has declined structurally, with AWS now representing a larger share of operating profit. We roll over another year of valuations and decrease our DCF target price to US$280 (prev. US$290). We upgrade our recommendation from ACCUMULATE to BUY due to the recent price rally.

Amazon.com Inc.- AWS growth accelerating

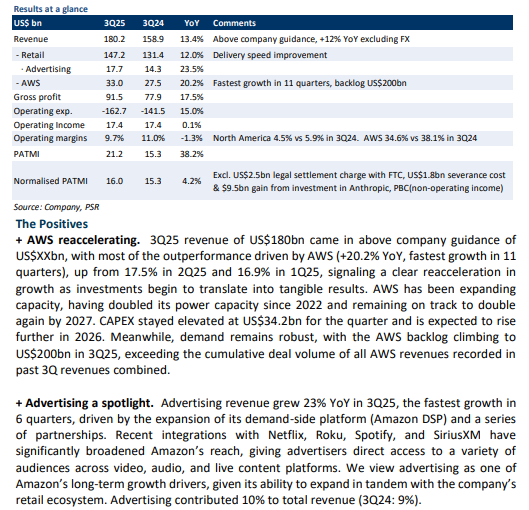

- 3Q25 revenue/Adjusted PATMI grew 13%/4% and were in line with expectations. 9M25 Revenue/Adjusted PATMI were at 70%/79% of our FY25e forecasts.

- The primary revenue driver was AWS (+20% YoY) and advertising (+24% YoY). AWS's operating margin compressed 3.5% YoY to 34.6%, due to heavy AI investment. Retail margin compressed 1.4% due to US$1.8bn severance cost and US$2.5bn legal settlement charge.

- We increase our FY25e revenue by 1% and PATMI by 6% to account for the growing demand in AWS as well as continued cost discipline efforts in the retail segment. We increase our DCF target price to US$290 (prev. US$260). We downgrade our recommendation from BUY to ACCUMULATE due to recent price rally. WACC of 6.4% and a terminal growth rate of 5% remaining unchanged. AMZN’s outlook remains strong with AWS reaccelerating.

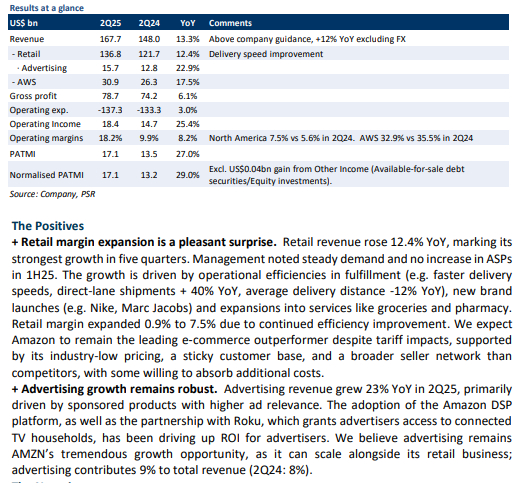

Amazon.com Inc.-Growth prospects still intact

- 2Q25 revenue/PATMI was in line with expectations. 1H25 Revenue/PATMI was at 46%/55% of our FY25e forecasts.

- The primary revenue driver was AWS (+18% YoY) and advertising (+23% YoY). AWS's operating margin compressed 2.9% YoY to 32.9%, due to heavy AI investment. Retail margin increased 0.9% due to efficiency improvement.

- We keep our FY25e revenue and PATMI assumption unchanged. We maintain our recommendation of BUY, with the same DCF target price of US$260, WACC of 6.4% and a terminal growth rate of 5% remaining unchanged. We remain positive on AMZN as we continue to see strong momentum in both retail and AWS. AMZN’s scale, sourcing flexibility, and strategic focus leave it well positioned to manage macro risks while AWS demand remains robust.

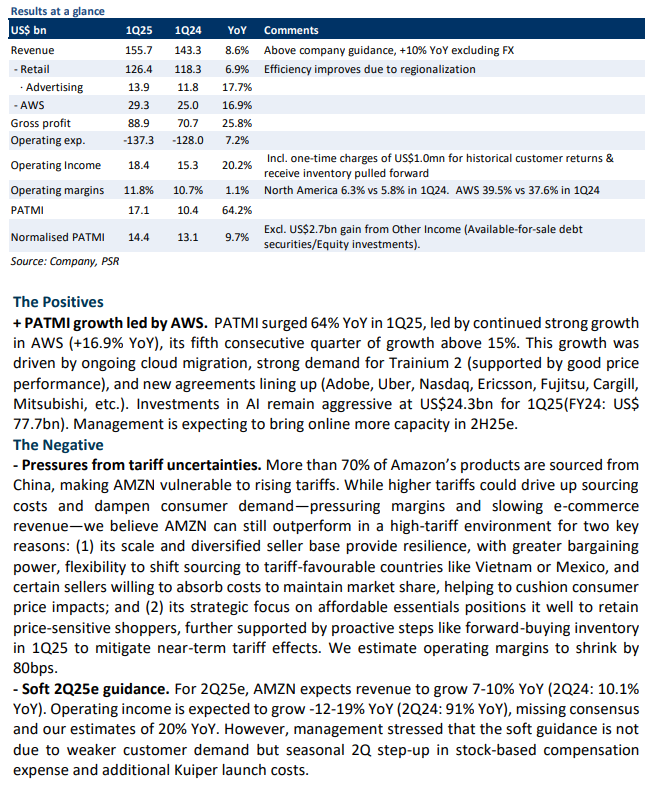

Amazon.com Inc. – Price fall gives an opportunity

- 1Q25 revenue was in line with expectations. 1Q25 Revenue/PATMI was at 22%/26% of our FY25e forecasts.

- The primary revenue driver was AWS (+17% YoY). AWS operating margin rose 1.9% YoY to 39.5%, driven by server capacity optimisation, which helps lower infrastructure cost. AMZN is focusing on low-priced essentials to mitigate tariff uncertainty risks.

- We lower our FY25e revenue estimate by 1% and PATMI by 2% to reflect the dampening of customer demand and retail margin pressure due to higher tariffs. Due to recent share price weakness, we upgraded our recommendation from ACCUMULATE to BUY and lower our DCF target price to US$260 (prev. US$270). The company’s strong momentum in AWS continues to scale profit meaningfully, helping offset pressures in retail.

Amazon.com Inc. – Strong results yet soft guidance

- 4Q24 revenue was in line with expectations. PATMI outperformed due to increasing operating leverage and cost discipline (3.1% YoY higher operating margins). FY24 Revenue/PATMI was at 100%/112% of our FY24e forecasts.

- The primary revenue driver was AWS (+19% YoY). AWS operating margin rose 7.3% YoY to 36.9%, driven by cost control and an extended server lifespan (contributed to a 200bps expansion).

- We roll over another year of valuations. We decrease FY25e revenue and PATMI by 1% to reflect the leap-year effect, decrease in the useful life of services and increase in the useful life of heavy equipment. Due to recent share price strength, we downgrade our recommendation from BUY to ACCUMULATE and raise our DCF target price to US$270 (prev. US$240). We believe AMZN is well-positioned in generative AI and should benefit from cloud migration as it is still in early stage.

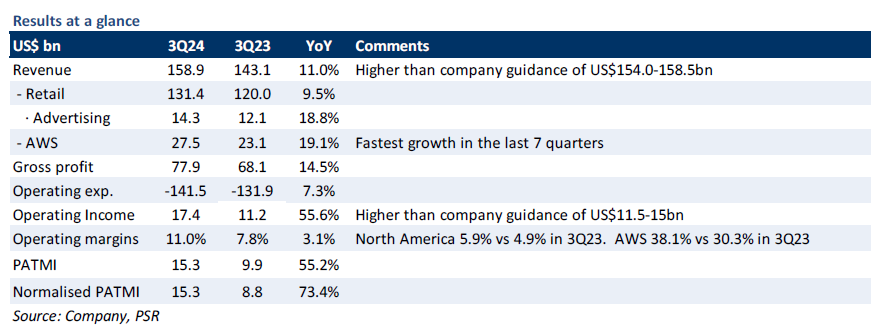

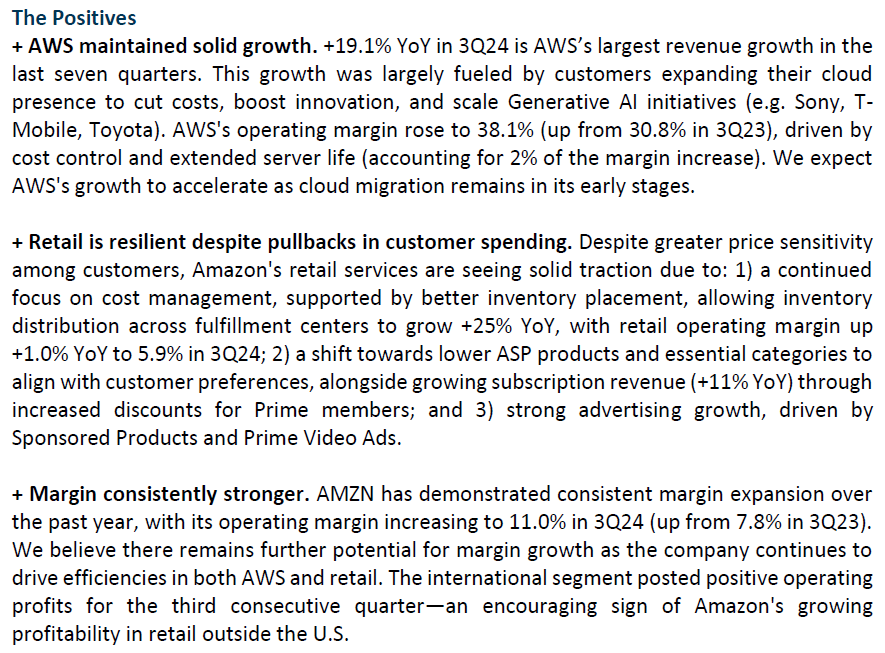

Amazon.com Inc. – Strong Third-Quarter Profitability

- 3Q24 revenue was in line with expectations. PATMI increased by 73% YoY due to continued cost-reduction efforts and increasing profitability and contribution from AWS. 9M24 Revenue/PATMI was at 70%/79% of our FY24e forecasts.

- +19% YoY AWS growth was the main driver of total revenue. AWS operating margin increased 6.8% YoY to 38.1% due to cost control and the extension of server useful life, contributing to AMZN’s overall 3.2% YoY operating margin expansion.

- We keep our FY24e revenue unchanged but increase PATMI by 6% to reflect the improving efficiencies, lowered costs, and higher operating margins from retail and AWS. We raise our DCF target price to US$240 (prev. US$220). We downgrade our recommendation from BUY to ACCUMULATE as we account for recent share price performance. We believe AMZN is well-positioned in generative AI and should benefit as cloud migration remains in its early stages.

Amazon.com Inc. – AWS Continues to Accelerate

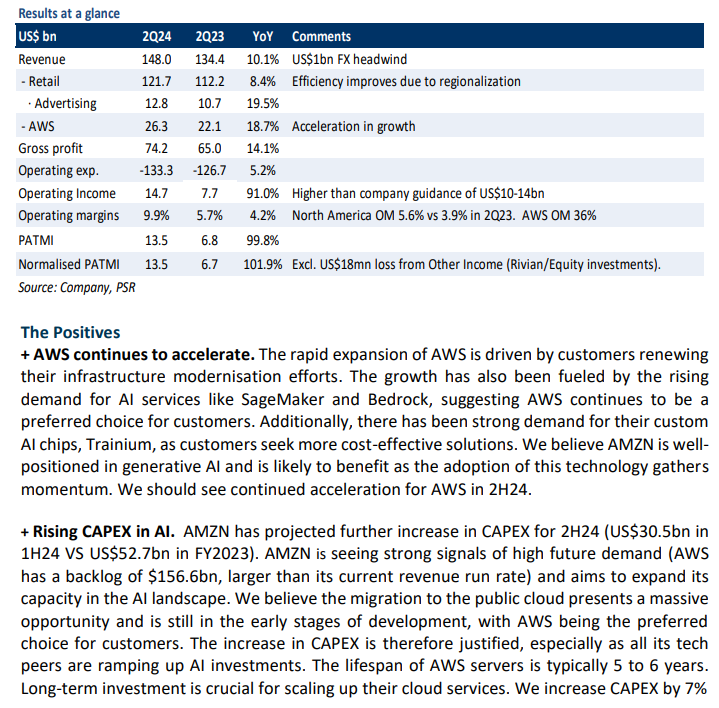

- 2Q24 revenue/PATMI was in line with our expectations. 1H24 revenue/PATMI was at 45%/55% of our FY24e forecasts.

- Better-than-expected AWS strength (19% YoY) continues to support growth driven by customers migrating workloads from on-premises to the cloud. Retail growth decelerated, in line with the company’s growth guidance, due to customers being cautious with spending.

- We maintain the BUY recommendation with an unchanged target price of US$220.00, WACC of 6.4%, and terminal growth rate of 5%. We increase our FY24e PATMI/CAPEX forecast by 8%/7% to account for margin improvement and higher CAPEX spending. Margin strength is from scaling up of AWS and advertising, as well as AMZN’s improvements throughout the network that helps lower costs and improve delivery speeds.

Amazon.com Inc.- More AWS growth ahead

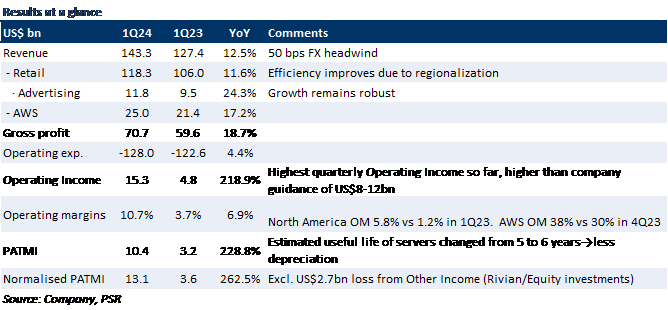

- 1Q24 revenue/PATMI meet our expectations at 22%/26% of our FY24e forecasts. 1Q24 revenue grew 12.5% YoY to US$143.3bn led by continued strength in AWS and advertising. Operating income benefited from lower depreciation due to a change in useful life of servers (~US$900mn in 1Q24)

- AWS revenue growth accelerated (17.2% YoY), driven by: 1) the end of the cost-optimizing trend as companies pivot towards newer initiatives to modernize their infrastructure; 2) accelerated demand for Gen AI; 3) strong emphasis on security and operational performance that appeals to customers. >85% global IT spend still remaining on-premises, highlighting significant growth headroom ahead.

- We maintain the BUY recommendation but raised our DCF target price to US$220.00 (prev. US$215.00), with an unchanged WACC of 6.4% and terminal growth rate of 5%. Our FY24e revenue estimates remain unchanged, while we increased our PATMI by 4% to account for lower expenses, a result of improved cost efficiencies.

The Positives

+ AWS showing more signs of reaccelerating. Revenue of US$143 bn is at the top-end of the company’s guidance, with most of the outperformance driven by AWS (13.2% YoY) and Advertising (26.8% YoY). The high growth of AWS is fueled by customers migrating workloads from on-premises to the cloud. Gen AI services are seeing a strong demand signal, evidenced by extended contracts and larger commitments (e.g., Perplexity AI/Workday). Management has disclosed a significant increase in Capex for 2024 to bolster AWS growth, indicating the company's confidence in AWS expansion prospects.

+ Improvement in margins. AMZN continues reaping the benefits of regionalizing its operations and has shown progress in bringing the cost structure down further (e.g. consolidation of units into fewer boxes). Its first-quarter operating income is at an all-time high of $15.3 bn, beating the company’s top-end guidance of US$12.0 bn. Consequently, the operating margin stood at 10.7% (reaching double-digits for the first time), a substantial increase from 3.7% in 1Q23. Notably, the international business achieved positive operating income for the first time in over two years. AWS’s operating margin reaches an all-time high of 37.6%.

The Negative

- Potential pullback in consumer spending. AMZN's hinted at potential signs of a slowdown in consumer spending. Despite growth in retail revenue, management noticed that customers are cautious about their expenditures, seeking bargains and opting for lower-priced alternatives. This trend appears to persist into the second quarter, especially for the European market. AMZN has guided a revenue growth between 7% and 11% in 2Q24e, including an unfavourable foreign exchange impact of 60 bps.

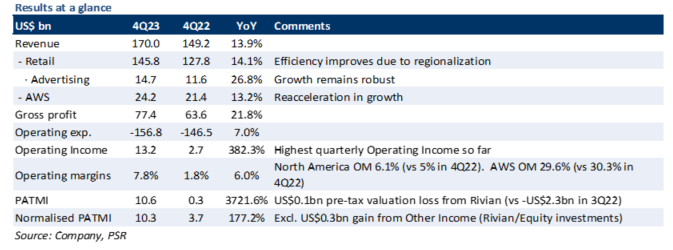

Amazon.com Inc. – Improving efficiency through regionalization

- 4Q23 revenue was in line with our expectation, while PATMI exceeded. The PATMI outperformance was due to cost efficiencies and higher operating leverage. 4Q23 Adj. PATMI grew ~3x YoY. FY23 revenue/PATMI was at 100%/111% of our FY23e forecasts.

- Operating income for 4Q23 grew ~5x YoY due to the benefits of network regionalisation in the US and strong advertising growth. Operating margin grew to 7.8%, an increase of 6.0% YoY.

- Due to higher operating leverage, we raise our FY24e PATMI by 58%. Our revenue forecast remains unchanged. We roll over an additional year of valuations and maintain our BUY recommendation with a raised DCF target price of US$215 (prev. US$190) to reflect our assumptions. Our WACC/growth rate of 6.4%/5% remains unchanged.

The Positives

+ Retail operating income was driven by regionalization and efficiency. AMZN’s retail operating income improved by 382% YoY. North American/International segment’s operation income increased from -US$0.2bn/-US$2.2bn in 4Q22 to US$6.5bn/-US$0.4bn in 4Q23, primarily driven by cost-cutting and lower transportation rates. North America benefit from regionalisation and expansion of last-mile delivery facilities, increasing same day deliveries by 65% YoY. Improved inventory placement drove faster deliveries and lowered transportation distances (cost to serve declined by >US$0.45 per unit). We foresee revenue growth to continue in the long term as lower costs lowers ASPs, improving affordability. This, together with faster delivery speed, should lead to greater purchase consideration & frequency.

+ Advertising growth remains robust. Advertising revenue grew 27% YoY in 4Q23, primarily driven by sponsored products with higher ads relevancy. AMZN benefits from being able to collect its own first-party data, and has been able to efficiently convert this data into more efficient and relevant ads for consumers, driving up ROI for advertisers. We believe advertising remains AMZN’s great growth opportunity as it has the ability to scale alongside its retail business, advertising only contributes 8% of the company’s total revenue presently.

+ AWS seeing stabilization in growth. AWS revenue was up by 13.2% YoY in 4Q23, compared to 12.3% and 12.2% YoY in 3Q23 and 2Q23. AWS revenue growth has dipped in previous quarters due to customers moderating their spending. The recent acceleration in growth rate suggests that this effect has bottomed out. Accelerated new deals and backlog conversion is expected to drive growth. Management has indicated that the acceleration in growth will continue into FY24, driven by accelerating demand in Gen AI. AWS’ order backlog grew ~40% YoY in 4Q23.

The Negative

- Nil.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report