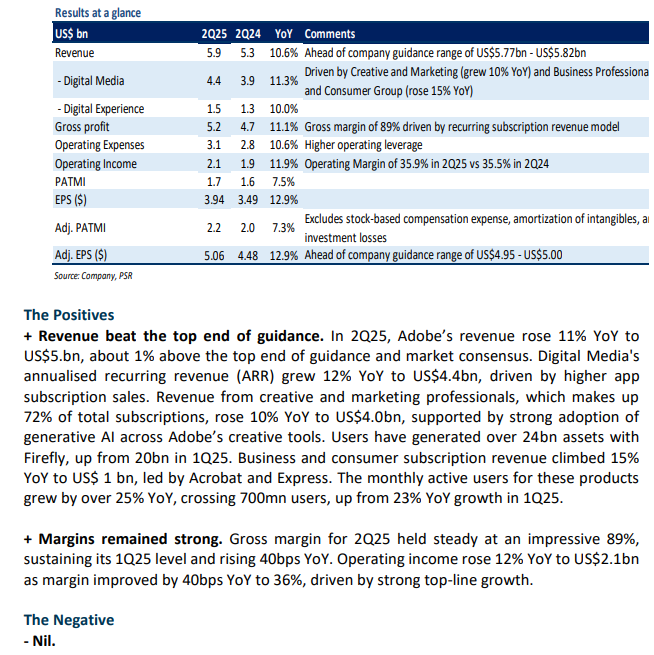

The Positives

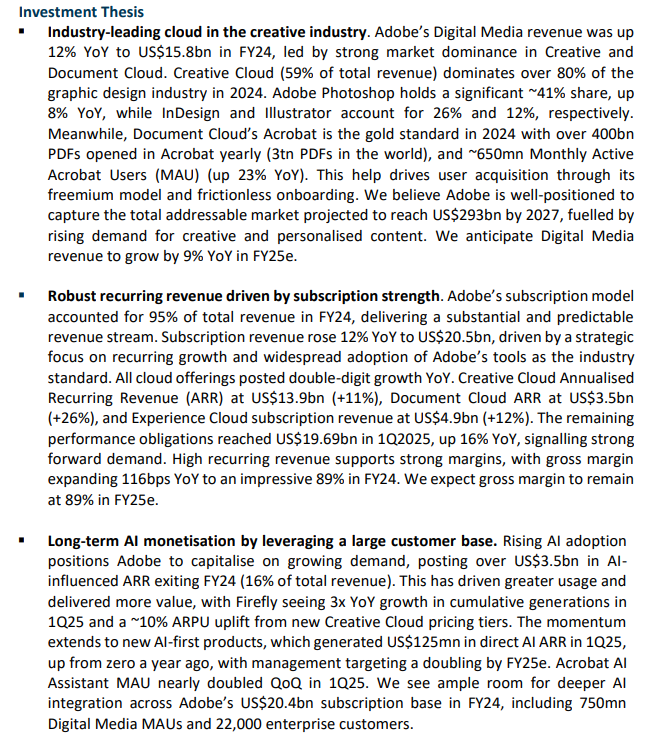

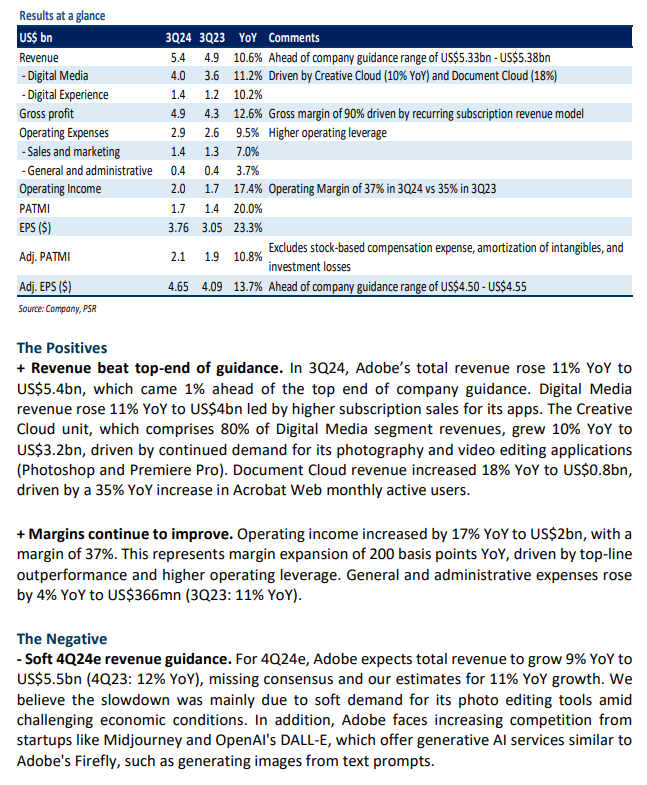

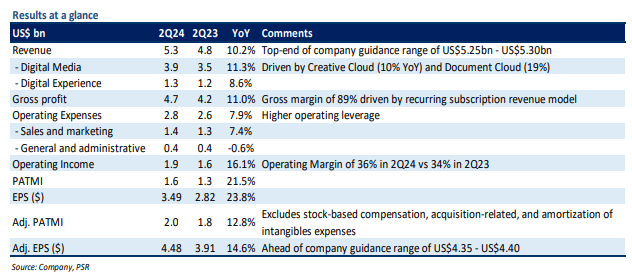

+ Net new Digital Media ARR beat guidance. Digital Media segment revenue increased by 11% YoY to US$3.9bn. Net new Digital Media annualized recurring revenue, or ARR, was US$487mn for the quarter, exceeding the US$440mn company guidance, driven by subscriber growth and new product innovations (Express for Business, Firefly services, and Acrobat AI). Within the Digital Media segment, Creative Cloud revenue rose 10% YoY to US$3.1bn, and Document Cloud revenue jumped 19% YoY to US$782mn. The growth was mainly led by continued demand for its photography and video editing applications (Photoshop and Illustrator) as well as PDF and e-signature solutions. Acrobat Web’s free monthly active users grew by 60% YoY driven by an explosion of PDF consumption through Chrome and Edge extensions.

+ Operating margins expanded on higher operating leverage. Operating income grew 16% YoY to US$1.9bn as margins expanded by 180 basis points YoY. The margin improvement was mainly due to top-line upside and continuous improvements in cost efficiencies, as expense growth slowed to 8% YoY (2Q23: 13% YoY). General and Administrative expenses were down 1% YoY. We raise our FY24e adj. PATMI by 2% on higher operating leverage.

The Negative

- Creative Cloud segment faced pricing headwinds. In 2Q24, the net new Creative Cloud annualized recurring revenue dropped by about 9% YoY to US$322mn. We believe the drop is mainly because of tough comparisons as price increases over the last two years has started to roll-off. In addition, Adobe faces increasing competition from startups like Midjourney and OpenAI's DALL-E, which offer generative AI services similar to Adobe's Firefly, such as generating images from text prompts.

The Positives

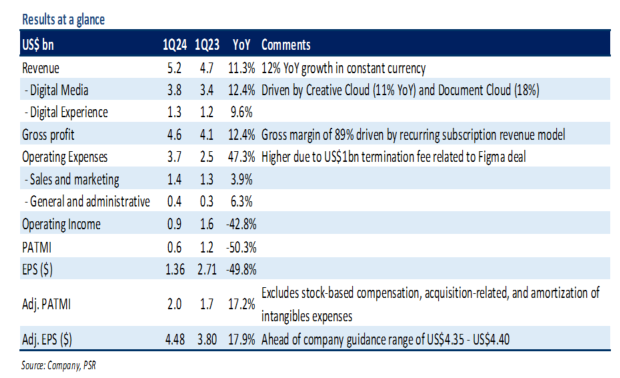

+ Revenue beat top-end of guidance. In 1Q24, Adobe’s total revenue rose 11% YoY to US$5.2b, which came 1% ahead of the top end of company guidance. Revenue from the Digital Media segment grew 12% YoY to US$3.8bn, with Creative Cloud revenue growing to US$3.1bn (up 11% YoY) and Document Cloud growing to US$0.8bn (up 18% YoY). This growth was mainly fueled by continued demand for its photography and video editing applications (Photoshop and Illustrator) and Acrobat PDF and e-signature solutions. Management highlighted that Acrobat Web’s monthly active users, or MAUs, spiked 70% YoY and surpassed 100mn users in the quarter.

+ Margins continue to improve. Gross and adj. net profit margins expanded by 80bps and 200bps YoY, respectively. The margin improvement was mainly due to top-line upside and higher operating leverage, including careful sales and marketing spend. Adj. PATMI increased by 17% YoY to US$2bn.

The Negative

- Soft 2Q24e revenue guidance. For 2Q24e, Adobe expects total revenue to grow 9% YoY to US$5.3bn. Management highlighted that the slowdown is mainly because of tough comparisons as price increases over the last two years has started to roll-off. Meanwhile, the new pricing for Creative Cloud apps with Firefly AI tools would become a tailwind towards the end of FY24e as it hits larger customer base at renewals. In addition, Adobe faces increasing competition from startups such as Midjourney and OpenAI's Dall-E, which offer gen-AI services similar to Adobe’s Firefly like generating images from text prompts.

The Positives

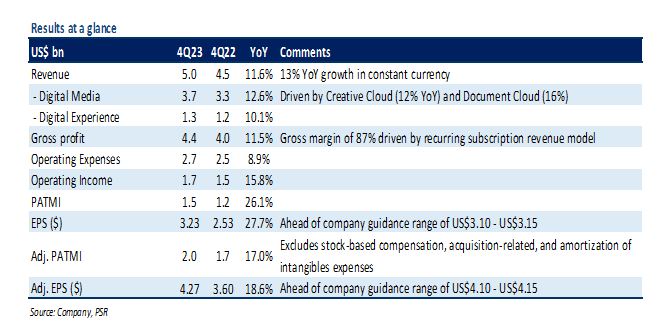

+ Revenue growth driven by Digital Media vertical. 4Q23 revenue grew 12% YoY to US$5.0bn, in line with the company guidance. Digital Media segment revenue rose 13% YoY to US$3.7bn led by higher subscription sales for its creative software applications. Adobe's Creative Cloud unit, which makes up 80% of Digital Media segment revenues, reported revenue growth of 12% YoY to US$3.0bn. The growth was mainly led by strong demand for its photography and video editing applications (Photoshop and Illustrator). Management highlighted that users have generated over 4.5bn images so far using its generative AI functionality Firefly compared with 3bn in October. Document Cloud revenue grew by 16% YoY to US$721mn (20% of Digital Media revenues) driven by continued demand for PDF and e-signature solutions. Management highlighted that Acrobat Web’s monthly active users, or MAUs, spiked 70% YoY while Acrobat Mobile surpassed 100mn MAUs in the quarter.

+ Improvements in margins. Adobe reported an impressive gross margin of 87% as the company reports the bulk of its sales from recurring revenue. Operating margins expanded 120bps YoY driven by continued focus on operational discipline, including careful investments in research and development as well as sales and marketing. Net margins expanded 340bps YoY driven by higher operating leverage, lower tax expense, and a 2.5x increase in interest income. PATMI rose 26% YoY to US$1.5bn.

The Negative

- Soft FY24e revenue guidance. For FY24e, Adobe expects total revenue to grow 10% YoY to US$21.4bn at the midpoint, which was below our estimate of US$21.8bn. The soft guidance was primarily due to a lower-than-expected impact from the pricing changes. Management highlighted that the price increase in November would impact less than half of the Creative Cloud base and expects a material impact in 2H24e and beyond.

The Positives

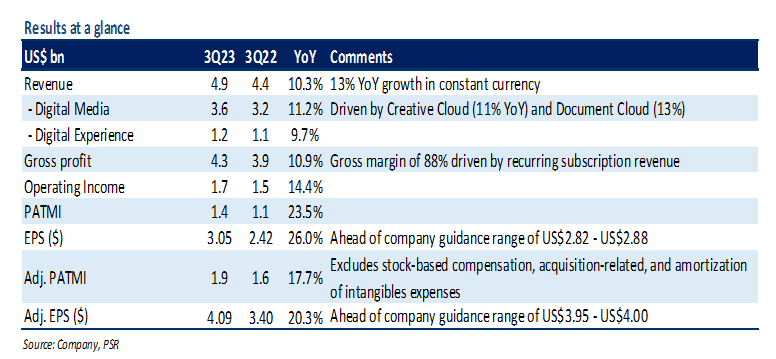

+ Creative Cloud momentum remained robust. Adobe’s Creative Cloud business comprises 81% of Digital Media segment revenues. Creative Cloud revenue grew 11% YoY to US$2.9bn (14% YoY in constant currency). Net New Creative Cloud annualized recurring revenue, or ARR, was US$332mn during the quarter, with a total Creative Cloud ARR of US$12bn. The growth was mainly led by strong demand for its photography and video editing applications due to a surge in both the creation and consumption of digital media. Management highlighted that the company has integrated its generative AI offering Firefly into flagship products Photoshop and Illustrator, with more than 3mn beta release downloads. Key customer wins for Creative Cloud in 3Q23 include Amazon, SAP, and Take-Two Interactive.

+ Continued strength in Document Cloud. Document Cloud sales grew 13% YoY to US$685mn, accounting for 19% of Digital Media revenues. Net new Document Cloud ARR was US$132mn, exiting the quarter with Document Cloud ARR of US$2.6bn. The growth was primarily driven by continued demand for Acrobat PDF solutions across computing devices and e-signature capabilities. Management highlighted that Acrobat Web monthly active users spiked by 70% YoY led by growth in documents opened through Chrome and Edge extensions. Key customer wins in 3Q23 include Citibank, GlaxoSmithKline, and Morgan Stanley.

The Negative

- FX impacted revenue growth. Adobe generates 40% of its total revenue from international markets. The company’s revenue was negatively impacted by the strengthening of the US dollar relative to most other currencies, including the Euro, British pound, and Japanese yen. In 3Q23, FX headwind to revenue was about US$125mn (~10% of PATMI).

The Positives

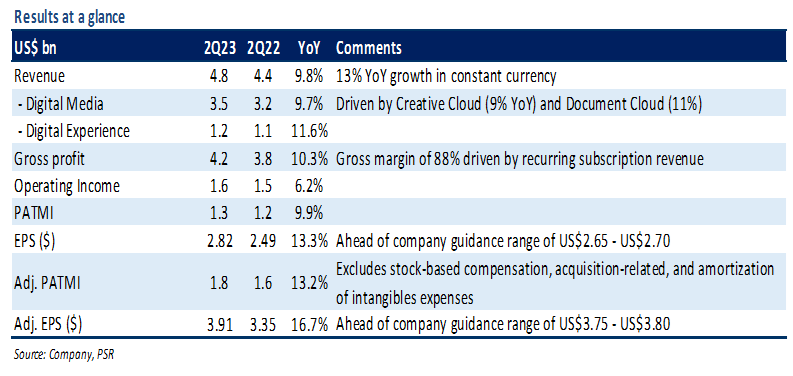

+ Firefly beta adoption was robust. Creative Cloud sales grew 9% YoY to US$2.9bn (14% YoY in constant currency) led by booming content demand. Net new Creative Cloud annualized recurring revenue (ARR) was US$354mn, exiting the quarter with Creative Cloud ARR of US$11.6bn. In 2Q23, Adobe released a beta version of Firefly, its generative AI offering for creating content using text prompts. Management noted that Firefly-powered capabilities integrated into Photoshop and Illustrator have generated 500mn digital assets so far. While the focus remains on driving broad-based adoption, Adobe plans to publish additional information regarding AI monetization later this year. Key customer wins for Creative Cloud in 2Q23 include NVIDIA and Ernst & Young.

+ Strong momentum in Document Cloud. Document Cloud revenue was US$659mn, up 11% YoY (14% YoY in constant currency). Document Cloud ARR grew by 17% YoY to US$2.5bn, adding US$116mn during the quarter. The growth was mainly due to strong demand for Acrobat with integrated Sign capabilities across the web, desktop and mobile. Management noted that Acrobat web monthly active users grew by 50% YoY driven by an explosion of PDF consumption through Chrome and Edge extensions. Key customer wins in 2Q23 include Boston Consulting Group, Novartis, and T-Mobile.

The Negative

- Negative impact of FX. Adobe’s revenue was negatively impacted due to the strengthening of the dollar against several key foreign currencies, including the Euro, British pound, and Japanese yen. In 2Q23, FX headwind to revenue was about US$150mn (~12% of PATMI).

Outlook

For FY23e, Adobe now expects GAAP EPS of US$11.20 on total revenue of US$19.3bn (prev. GAAP EPS of US$11.00 on revenue of US$19.2bn) taking the midpoint (Figure 1). The company also bumped its net new Digital Media ARR forecast to US$1.75bn from US$1.70bn driven by product-led growth initiatives, including Adobe Express and generative AI tools. Notably, we expect AI-driven revenues to be modest in 2H23e given they are still in the early stages. Meanwhile, the company lowered its Digital Experience segment revenue forecast to US$4.88bn (prev. US$4.98bn) due to cautious enterprise buying behaviour resulting in an elongated sales cycle, additional deal approval layers and deal size compression.

For 3Q23e, Adobe is guiding for revenue of US$4.85bn, up 10% YoY, and GAAP EPS of US$2.85, both at the midpoint of its guidance. Management also guided Digital Media and Digital Experience segment revenues to be US$3.56bn and US$1.22bn, respectively.

Adobe reiterated its belief that its pending US$20bn acquisition deal of design startup Figma should close by the end of FY23e. Cash flow generation continues to be strong, with the company generating about US$2bn in Free Cash Flow in 2Q23, ending the quarter with US$5.5bn in cash and cash equivalents.

The Positives

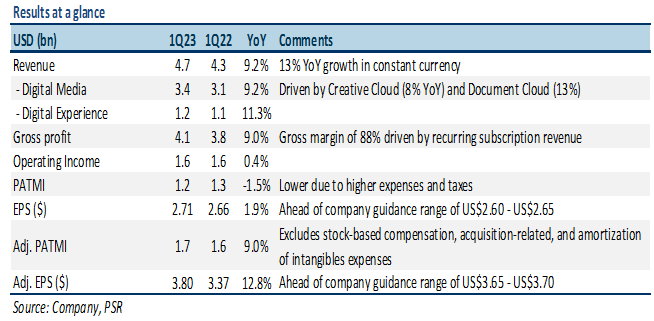

+ Demand for Creative Cloud remains resilient. Creative Cloud revenue was US$2.8bn, up 8% YoY (13% YoY in constant currency). Creative Cloud annualized recurring revenue (ARR) grew by 8% YoY to US$11.3bn, adding US$307mn during the quarter. The growth was primarily driven by continued demand for its photography, imaging and video applications due to the surge in digital content creation. Key customer wins in 1Q23 include Accenture, Disney, BBC, and Nintendo.

+ Document Cloud strength continues. Document Cloud sales grew 13% YoY to US$634mn (16% YoY in constant currency) – the fastest growth of any segment in the quarter. Net new Document Cloud ARR was US$103mn, exiting the quarter with Document Cloud ARR of US$2.4bn. The growth was mainly due to its PDF capabilities and growth in e-signature transactions within Acrobat. Management noted that Acrobat is now the default PDF viewer in Microsoft Edge, which has an estimated 1bn users. Key customer wins in 1Q23 include HP, JPMorgan Chase, Samsung, and Verizon.

The Negative

- Pressure from foreign exchange rates. Adobe’s revenue was negatively impacted due to the strengthening of the dollar against several key foreign currencies, including the Euro, British pound, and Japanese yen. In 1Q23, the unfavorable foreign exchange rate movement negatively impacted revenue by approximately US$200mn (or ~16% of PATMI).

The Positives

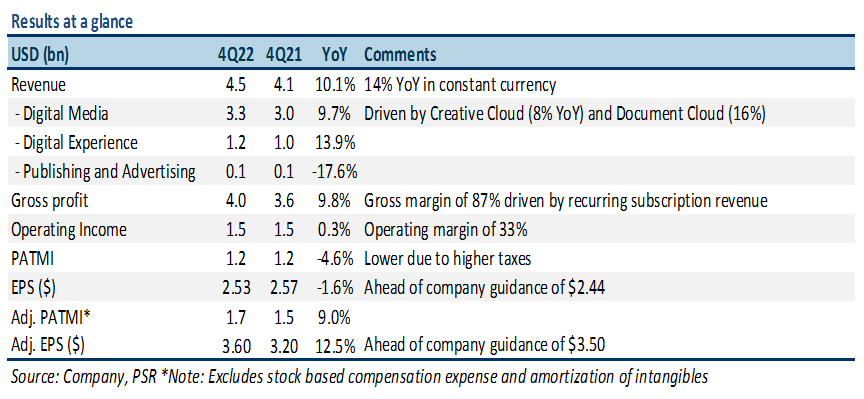

+ Strong growth across business segments. In 4Q22, revenue grew 10% YoY (14% in constant currency) to US$4.5bn, which was in line with our estimates. The growth was driven by 10%/14% YoY increases in Digital Media and Digital Experience revenues to US$3.3bn and US$1.2bn, respectively. In the Digital Media segment, Creative Cloud revenue grew 8% YoY to US$2.7bn driven by strong demand for its design software tools (Photoshop, Adobe Express, and Frame.io) from creative professionals and smaller and medium-sized enterprises. Document Cloud revenue grew 16% YoY to US$619mn due to its PDF capabilities and growth in e-signature transactions within Acrobat. Digital Experience revenue, which includes analytics and marketing software, increased by 14% YoY to US$1.2bn. Key customer wins include Meta, Deloitte, and Delta Air Lines.

+ Maintained high margins. In 4Q22, Adobe reported an impressive gross margin of 87%. This is mainly because the company generates the majority of its sales (>90%) from recurring subscription revenue. Adj. operating margin (excluding stock-based compensation expense and amortization of intangibles) was 45%, which was in line with 4Q21. Adobe generated US$2.2bn in free cash flow in 4Q22. This translates to a 49% free cash flow margin.

The Negatives

- FX continues to be a headwind. Adobe’s revenue was negatively impacted due to the strengthening of the dollar against several key foreign currencies, including the Euro, British pound, and Japanese yen. In 4Q22, FX headwind to revenue was about US$175mn (15% of PATMI). Adobe projects nearly US$750mn headwind from FX in FY23e.