Apple Inc. – Great earnings shadowed by rising memory cost

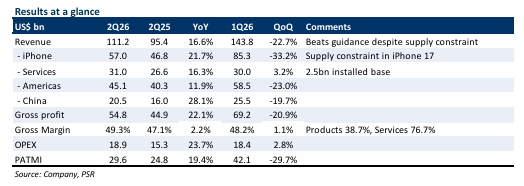

- Both 2Q26 revenue and PATMI exceeded our expectations. Revenue grew 16.6% YoY, the fastest growth in four years, mainly driven by faster-than-expected growth in iPhone (+22% YoY) and the China market (+28% YoY). 2Q26 revenue/PATMI were at 55%/56% of our FY26e forecasts.

- Strong demand for iPhone 17 and MacBook continues, with demand exceeding supply. Management guided 3Q26 revenue growth of 14–17% YoY, supported by continued strength in iPhone and MacBook. However, rising memory costs are expected to intensify in the coming quarters, presenting a longer-term margin headwind.

- We maintain our NEUTRAL recommendation, with a higher DCF target price of US$280 (prev. US$260). We raise our FY26e revenue and PATMI assumptions by 2% and 1%, respectively, to account for stronger-than-expected iPhone 17 growth. WACC of 6.5% and terminal growth of 3.5% remains unchanged. AAPL’s ability to sustain product-led growth while translating its AI investments into meaningful user adoption and monetisation will be key to supporting its valuation.

The Positives

+ Strong iPhone 17 and MacBook momentum expected to carry into next quarter. 2Q26

revenue grew 17% YoY, driven by iPhone (+22% YoY) and Mac (+6% YoY). The strong demand

is supported by a robust iPhone 17 upgrade cycle (high customer satisfaction, new features,

and Apple Intelligence integration) and by MacBook Neo’s attractive pricing, which is driving

new user adoption. Both product lines are currently supply-constrained. iPhone is impacted

by tight advanced-node (3nm-class) SoC capacity (expected to ease in 3Q26), while Mac

constraints are likely to persist for several months. Management guided 3Q26e revenue

growth of 14–17% YoY.

+ Continued shareholder returns support valuation and capital discipline. AAPL announced

an additional US$100bn share repurchase authorization and a 4% dividend increase,

reinforcing its commitment to returning excess cash. This signals confidence in the durability

of cash flows and provides valuation support and downside protection, particularly in a period

of rising costs and elevated investment. Importantly, it also reflects Apple’s disciplined capital

allocation, balancing ongoing reinvestment in AI and product development with consistent

shareholder returns.

Apple Inc. – Booming iPhone 17 VS soaring memory costs

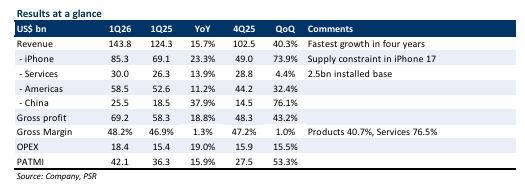

- 1Q26 revenue and PATMI were within our expectations. Revenue grew 16% YoY, fastest growth in four years, mainly driven by growth in iPhone (+23% YoY) and China market (+38% YoY). 1Q26 revenue/PATMI were at 31%/34% of our FY26e forecasts.

- Demand for the iPhone 17 lineup remains strong, with current demand outpacing supply. Management guided 2Q26e revenue growth of 13–16% YoY, supported by continued iPhone sales momentum. Rising memory costs are expected to become more pronounced in the coming quarters, posing a margin headwind in the long run.

- We raise our FY26e revenue and PATMI assumption by 2% and 3%, respectively, to account for the strong growth in iPhone 17. We have also increased our terminal growth rate from 3.0% to 3.5% to reflect the long-term monetization potential from AAPL’s collaboration with Gemini, which strengthens Apple Intelligence and supports sustained ecosystem engagement. We upgrade our recommendation from REDUCE to NEUTRAL, raising the DCF target price to US$260 (prev. US$230). WACC of 6.5% remains unchanged. We remain cautious on AAPL, as the stock is still in a “prove-it” phase, particularly at a ~30.7x forward FY26 P/E. Ultimately, AAPL’s ability to sustain product-led growth and execute a successful Siri rollout will be critical to underpinning its current valuation.

The Positives

+ Strong iPhone 17 cycle continues. AAPL delivered a record quarter, with total revenue of

US$143.8bn (+16% YoY), driven by iPhone revenue of US$85.3bn (+23% YoY), an all-time high

for the product. Demand remains strong, leaving AAPL with very lean channel inventory and

a constrained supply (mainly due to constrained advanced-node (3nm-class) SoC capacity).

The strength of the cycle is broad-based, supported by record upgraders across geographies

and double-digit growth in switchers. AAPL expects iPhone-led momentum to continue and

guided 2Q26E revenue growth of 13–16% YoY. We see the iPhone 17 cycle as durable. The

upcoming Siri rollout (supported by AAPL’s collaboration with Google Gemini) will further

reinforce the upgrade narrative and provide additional upside. We forecast iPhone sales +14%

YoY in FY26.

+ China market rebound a pleasant surprise. China revenue +37.9% YoY, marking a sharp

rebound after four years of flat to negative growth. The iPhone 17 lineup has resonated

strongly with Chinese consumers, evidenced by double-digit growth in in-store traffic and

robust upgrader and switcher activity. Notably, this strength was achieved despite the later

release of the iPhone 17 Air, and Apple Intelligence not yet being available in the Chinese

market. iPhone ranked among the top three smartphones in China during the quarter. Given

that China contributes ~18% of AAPL’s total revenue, a rebound in the region represents a

meaningful upside for AAPL.

Apple Inc.-Strong outlook, yet no real game changer

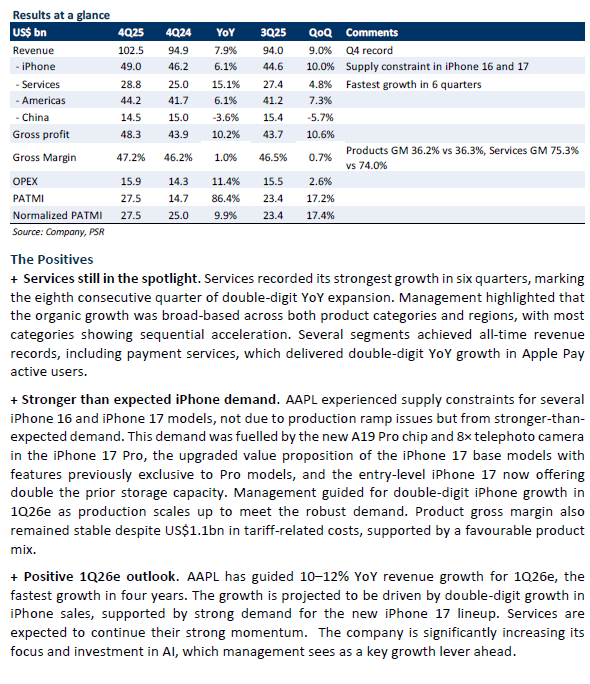

- 4Q25 PATMI was within our expectations, while revenue underperformed slightly due to supply constraints in iPhone 16 and 17. FY25 revenue/PATMI were at 98%/100% of our FY25e forecasts. Revenue grew 8% YoY, mainly driven by growth in iPhone (+6% YoY) and Services (+15% YoY).

- China revenue fell 4% YoY. Management remains positive, expecting the China market to return to growth in 1Q26e, with overall revenue projected to rise 10–12% YoY (the fastest pace in four years), supported by double-digit iPhone sales growth.

- We raise our FY26e revenue and PATMI assumption by 1% and 5% respectively, to account for the higher-than-expected growth in iPhone. We roll over another year of valuations and maintain our recommendation of REDUCE, with a raised DCF target price of US$230 (prev. US$200). WACC of 6.5% and a terminal growth rate of 3% remain unchanged. Apple’s AI rollout thus far has been disappointing, with no game-changing AI to trigger a major product upgrade cycle. We continue to remain cautious.

Apple Inc.- Thin on design, thinner on investor sentiment

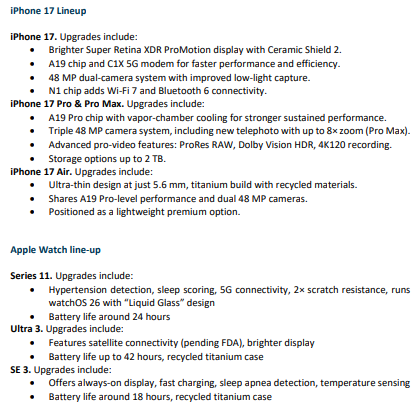

Apple hosted its “Awe-Dropping” launch event on 9 September, unveiling the iPhone 17 line up, including the ultra-thin iPhone Air (5.6 mm vs normal iPhone 16 7.8mm and 16 Pro 8.3mm)

- Upgrades include the new A19 Pro chip, C1X 5G modem, N1 networking chip, enhanced cameras, and tougher Ceramic Shield 2.

- Apple also introduced AirPods with on-device AI features, including real-time language translation and voice isolation, as well as the Apple Watch Series 11 with improved health tracking and a thinner design.

- Apple is absorbing the tariff impact by keeping prices unchanged or slightly lower (for same-series, same-storage iPhones), which adds pressure on margins.

- Our valuations remain unchanged. Our DCF target price remains unchanged at US$200, with a WACC of 6.5% and a terminal growth rate of 3%. We downgrade our recommendation from NEUTRAL to REDUCE due to the recent share price rally. We maintain a cautious outlook on Apple, due to near-term headwinds from tariffs, elevated CAPEX, and no significant AI innovation to help with persistent weakness in products and the China market.

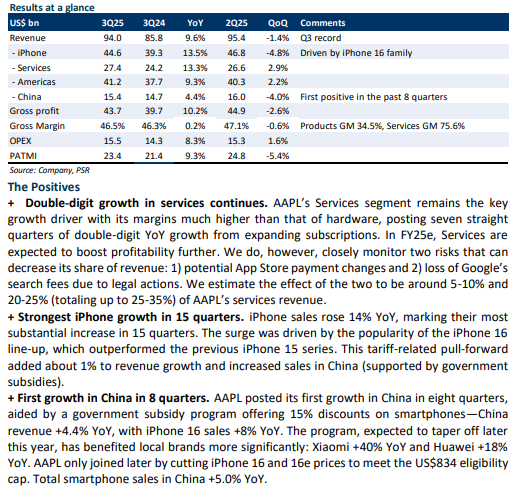

Apple Inc.- Good results, but still cautious

-

3Q25 results were within our expectations. 9M25 revenue/PATMI were at 75%/76% of our FY25e forecasts. Revenue grew 10% YoY, mainly driven by growth in iPhone (+14% YoY) and Services (+13% YoY).

-

China market +4.4% YoY, first positive in the past eight quarters, driven by accelerated iPhone sales supported by Chinese government subsidies. Management expects a tariff cost of US$1.1bn in 4Q25e

-

We keep our FY25e revenue and PATMI assumption unchanged. We maintain our recommendation of NEUTRAL, with the same DCF target price of US$200. WACC of 6.5% and a terminal growth rate of 3% remain unchanged. We maintain a cautious outlook on AAPL, as near-term tariff headwinds continue to weigh on margins. iPhone sales and the strength of the China market are also unlikely to last.

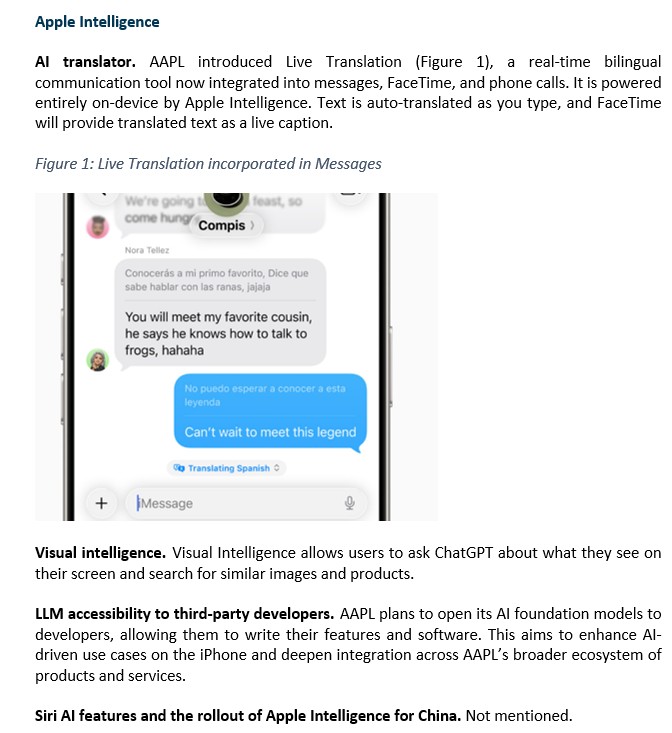

Apple Inc. – AI is playing catch-up at WWDC

Apple held its annual Worldwide Developers Conference (WWDC) on 10 June, during which it unveiled a redesign across its platforms and updates to iOS 26, iPadOS 26, watchOS 26, macOS 26 (Tahoe), and visionOS 26.

- Upgrades centered primarily on visual enhancements such as the new “Liquid Glass” design, along with minor software refinements

- Few AI innovations were announced (AI translator, LLM accessibility to third-party developers, and Visual Intelligence), most of which trail behind rivals like Google, not enough to address growing competitive pressures.

- Our valuations remain unchanged. We maintain our NEUTRAL recommendation with an unchanged DCF target price of US$200. WACC of 6.5% and a terminal growth rate of 3% remain unchanged. We maintain a cautious outlook on Apple, due to near-term headwinds from tariffs, elevated CAPEX, and no significant AI innovation to help with persistent weakness in products and the China market.

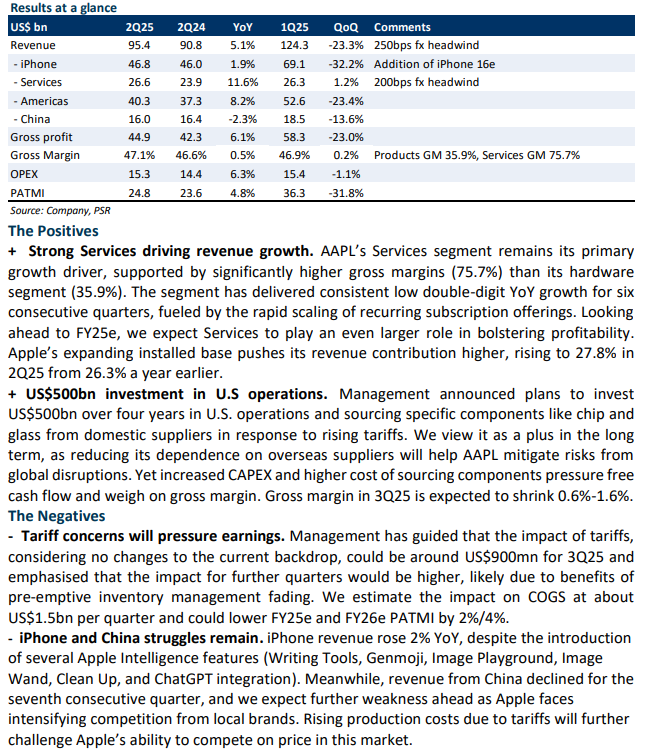

Apple Inc.- Tariff troubles and growth struggles

- 2Q25 results were within our expectations. 1H25 revenue/PATMI were at 51%/54% of our FY25e forecasts. Revenue grew 5% YoY, mainly driven by growth in Services (+12% YoY), and gross margin expanded 0.5% YoY.

- iPhone sales +1.9% YoY, with regional strength offset by continued weakness in China (-2.3% YoY).

- We lower our FY25e and FY26e PATMI estimates by 2% and 4%, respectively, to account for the lower gross margin due to rising tariffs. We adjusted FY25e and FY26e’s CAPEX by 1.2x and 2.3x to account for the higher investment in US operations. We maintain our recommendation of NEUTRAL, with a lowered DCF target price of US$200 (previously US$235). WACC of 6.5% and a terminal growth rate of 3% remain unchanged. We maintain a cautious outlook on Apple, due to near-term headwinds from tariffs, elevated CAPEX, and persistent weakness in products and the China market.

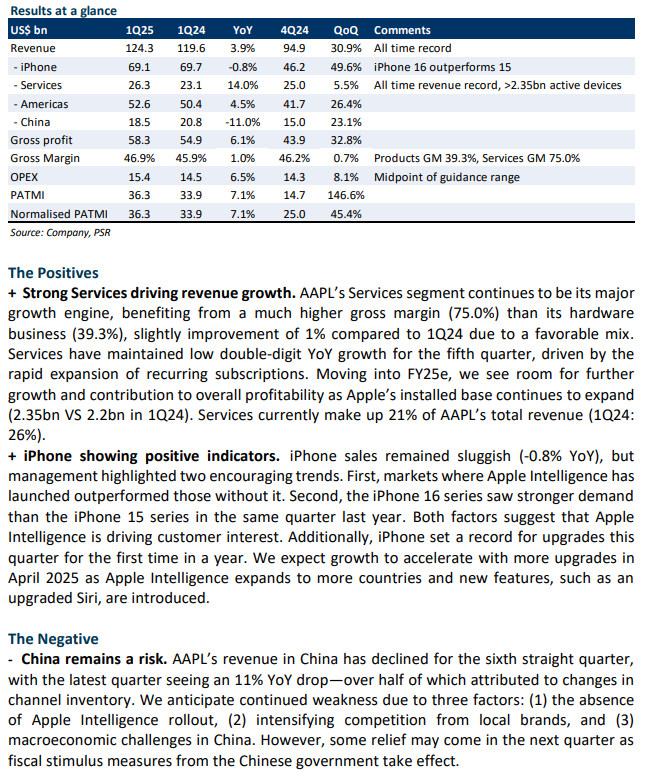

Apple Inc. – All according to plan

·1Q25 results were within our expectations. 1Q25 revenue/PATMI were at 29%/32% of our FY25e forecasts. Revenue grew 4% YoY, mainly driven by growth in Services (+14% YoY) and gross margin expanded 1% YoY.

· iPhone sales dropped 0.8% YoY, with regional strength offset by continued weakness in the China market (-11.0% YoY).

· Our FY25e forecast remains unchanged. Our DCF target price remains at US$235, with a WACC of 6.5% and a terminal growth rate of 3%. Due to recent price performance, we downgrade our recommendation from ACCUMULATE to NEUTRAL. iPhone sales have not yet seen a spike, due to the very gradual and limited rollout of the regions and features. We expect it to be backloaded in 2H25 and FY26, especially after more regions and features are made available.

Apple Inc. – iPhone strength with Apple Intelligence rollout

· 4Q24 revenue was within our expectations, while PATMI missed due to a one-time income tax expense of US$10.2bn to the Irish government. FY24 revenue/PATMI were at 97%/92% of our FY24e forecasts. iPhone growth of 6% YoY and Services growth of 12% YoY were the standout.

· The iPhone 16 series is benefiting from growing interest in Apple Intelligence, which began a gradual rollout this Oct. Sales increased across all regions except China, where local competition continues to weigh on performance. iPad/Mac/Wearables remain muted, with ongoing weakness expected into 1Q25e.

· Our FY25e forecast remains unchanged. We roll over another year of valuations and upgrade our recommendation from NEUTRAL to ACCUMULATE with a raised DCF target price of US$235 (prev. US$215), with a WACC of 6.5% and a terminal growth rate of 3%. The gradual rollout of Apple Intelligence may take time, but we are confident it will positively impact the iPhone replacement cycle in FY25 and FY26.

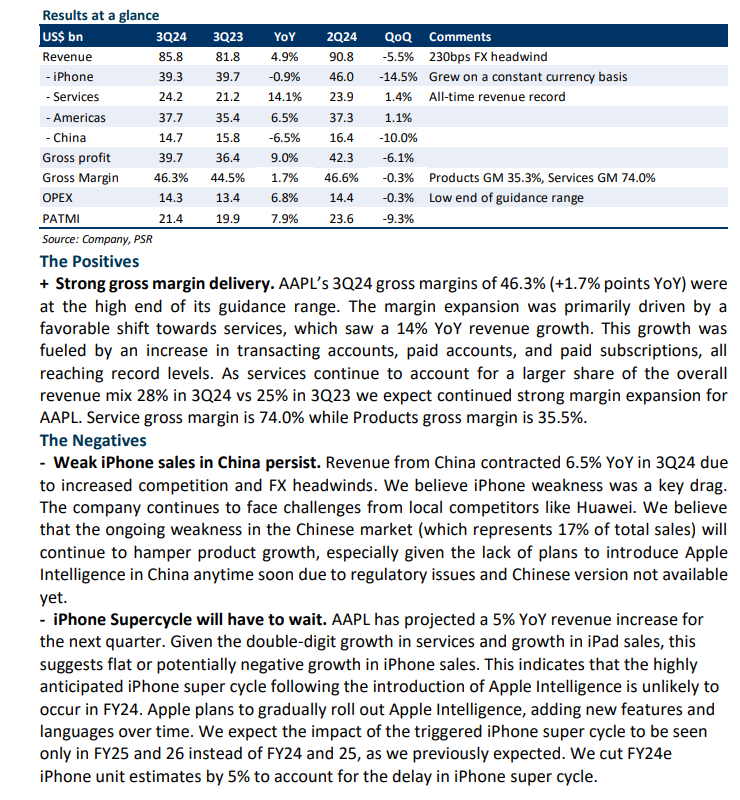

Apple Inc. – Supercycle unlikely in 2024

- 9M24 revenue/PATMI was in line with expectations at 73%/77% of our FY24e forecasts. 3Q24 revenue growth of 5% YoY is led by strong services business (14% YoY)

- We expect a soft 4Q24 for AAPL due to ongoing weak iPhone sales in China and slower-than-expected global iPhone refresh cycles. However, a significant iPhone refresh super cycle is expected in FY25.

- We maintain a NEUTRAL rating. We decrease our target price to US$215 (prev. US$220.00), with a WACC of 6.5% and a terminal growth rate of 3%. We raised service margin by 2% to account for the margin improvement and cut FY24e iPhone unit estimates/revenue/PATMI by 4%/4%/2% to account for the delay in iPhone super cycle.

Get access to all the latest market news, reports, technical analysis

by signing up for a free account today!

Login

The full article is only available for premium content subscribers. To continue reading this article, please log in:

Not a Premium Content Subscriber yet? Sign up here!

- Home >

- Phillip Research Report