Description

AT&T Inc. (NYSE:T) is a provider of communications and digital entertainment services in USA and the world. The Company operates in four segments: Business Solutions, Entertainment Group Consumer Mobility and International. The Company offers its services and products to consumers in the United States, Mexico and Latin America and to businesses and other providers of telecommunications services worldwide. It also owns and operates three regional TV sports networks, and retains non-controlling interests in another regional sports network and a network dedicated to game-related programming, as well as Internet interactive game playing. Its services and products include wireless communications, data/broadband and Internet services, digital video services, local and long-distance telephone services, telecommunications equipment, managed networking, and wholesale services.

Source: Thomson Reuters

Investment Rationale

T looks set to get its approval for its deal to merge with Time Warner (NYSE:TWX). We find the merger to be very compelling, allowing T to produce and distribute their new content across multiple media platforms, perhaps creating their own Netflix like service. The deal is also compelling from a financial standpoint as TWX is a faster growing and higher Free Cash Flow (FCF) margin company. The launch of the new iPhones may also be a nice tailwind for the company. T is trading below its 5 year historical average and is yielding about 5.41%. Along with its strong balance sheet and strong cash flows, we are bullish on T and believe that T is attractively valued at current price

Recent Price Action: T has been struggling since the start of the year when it hit its 52 week high of USD 43.03 in January. Subsequently, the share price continued to tumble to its last done price of USD 36.26, a fall of about 14.74% YTD. Recently, T has shown signs of rallying and closed about 3% above its 52 week low of USD 35.10, which it hit on 8th September.

Merger with TWX: T first announced their intention to merge with TWX late last year, with unanimous approval by the board of directors of both companies. TWX’s library of content is extensive, listing Warner Brothers’ DC franchise (Justice League and Wonder Woman) as well as Home Box Office (Game of Thrones) among its collection. The deal would combine that library of content with AT&T’s ability as one of the largest broadband providers in the USA (3rd largest by subscribers) to distribute that content. T would be able to push TWX content to its mobile and broadband customers and reap the advertising revenue displayed while consumers consume that content. While President Trump had previously stated his opposition to the deal, likely what led to T’s tumble in share price, the review of the merger had reached an advanced stage. While the deal has not yet been approved, we believe that T will eventually be given the approval for the deal to go through.

From a financial standpoint, the merger will also be very beneficial to T. Management has projected about USD 1 bn in cost saving synergies within 3 years of the merger’s completion. With the wireless provider industry in USA facing headwinds and falling revenues, T is not an exception to this, its latest quarter revenue revealed a fall of about 1.8% YoY. TWX, on the other hand, was able to grow its latest quarter revenue by 5.5% YoY. As such, if the merger goes through, T would be taking on a faster growing business.

TWX is also a much less capital intensive business, with a capital expenditure for the trailing twelve months ended in Jun 2017 of USD 472 Mn. In contrast, T is a very capital intensive business, with its capital expenditure for the trailing twelve months ended in Jun 2017 at USD 23.5 bn.

As such, we believe that the merger deal will be very beneficial to T on a qualitative standpoint, the new company having a vast library of content and the means to easily distribute that content, as well as a quantitative standpoint, the acquisition helping to diversify T’s revenue and adding a less capital intensive and higher FCF margin business to T.

5G and iPhone tailwinds: T has also been rolling out its 5G network. With today’s culture of consuming digital content on the go, high speed internet is more important than ever in the bid to attract consumers to subscribe to their services. 5G networks allow consumers to use bandwidth intensive applications like streaming at speeds as high as 1 Gb per second. This also has synergies with their TWX merger, enticing its subscribers to stream its content more often.

Besides that, the launch of the new iPhone X, 8 and 8 Plus will also likely prove to be a significant tailwind for T. T has about 135 mn wireless phone subscribers, and is the 2nd largest wireless phone service provider in the USA. With the release of the new iPhones, we expect many providers, T included, will be offering deals to entice consumers to upgrade their plans and devices. Additionally, with Black Friday approaching, we believe that T will also capitalize on that together with the new iPhones to bring customers in.

With faster wireless internet speeds coming and new devices from Apple, we believe that there are tailwinds behind T to propel its business forward.

Valuations: T closed at USD 36.26. It trades at a PER of 17.04, which is significantly below its 5 year average of 22.31. It has an Operating Margin of 18.38% and a Net Profit margin of 9.83%. Compared to its peers, Verizon trades at a 12.01, Comcast Corporation trades at a PER of 18.72. T pays a div of USD 1.96, representing a yield of about 5.45%, with a payout ratio of 0.78. T is also a Dividend Aristocrat, with a history of 32 years of consecutive dividend increases and is the only telecom company in the list. T has an Interest Coverage Ratio of 5.25 and Free Cash Flows of USD 15.81 bn. Our Target Price of USD X.00 is set based on Technicals.

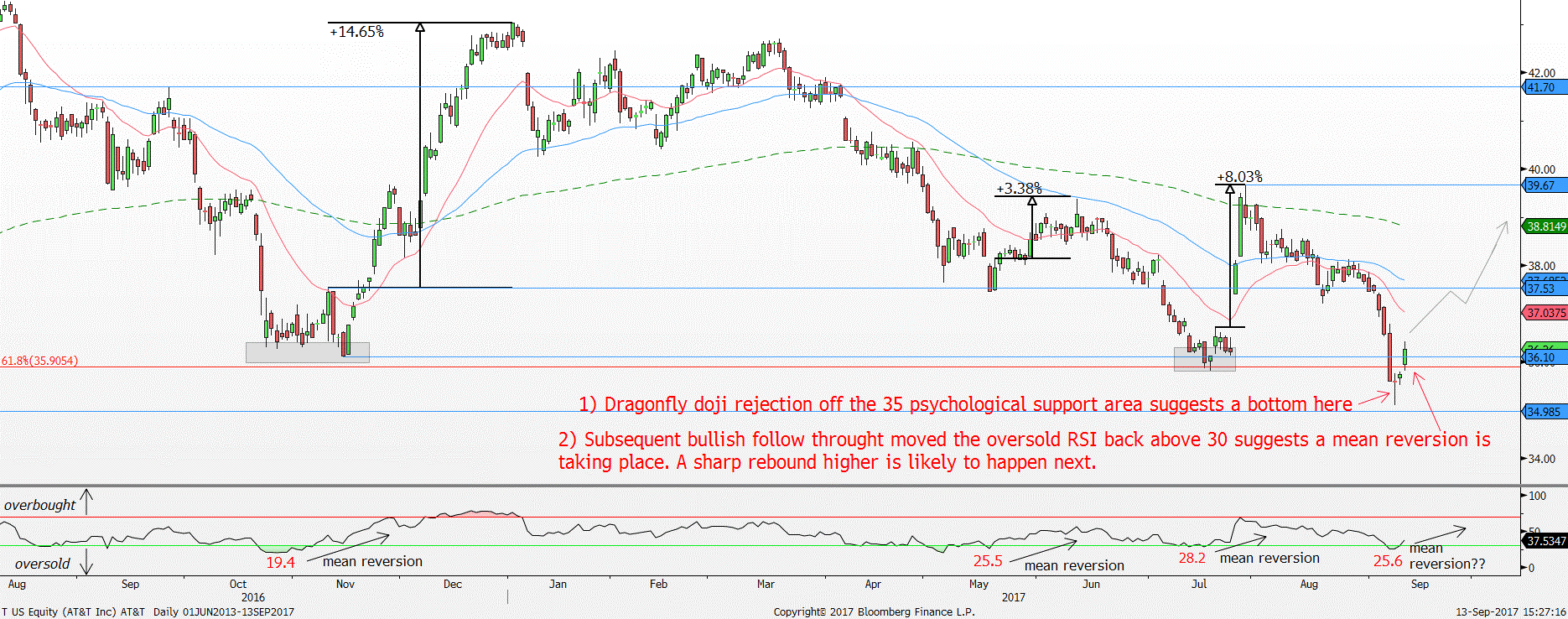

Technicals: T has been falling sharply since March 2017 and more recently in July after the 200 day moving average capped the bullish recovery. The heavy selling has resulted in the Relative Strength Index (RSI) signalling an oversold condition in August as it fell to an extreme low of 25.6. RSI measures the momentum, and a reading above 70 suggests overbought condition while a reading below 30 suggests oversold condition.

T Daily chart – rebound in sight

Support 1: 35.00 Resistance 1: 37.53

Support 2: 34.00 Resistance 2: 39.67

Red line = 20 period moving average, blue line = 60 period moving average, Green line = 200 period moving average

Source: Bloomberg, PSR

T tends to react well when the RSI is at either extreme. When the RSI reverts to the mean from the overbought or oversold extremes, price tends to enter into a robust reversal.

For instance, in October 2016, the RSI dived into the oversold condition and reached an extreme low of 19.4 on 26 October 2016. Price reversed sharply thereafter signalled by the RSI mean reverting off the 19.4 low. The confirmation of the bottom was when the RSI moved back above 30 on 7 November 2016 with price rallying 14% subsequently.

A similar pattern is happening now after the recent sharp sell-off as the RSI entered into oversold condition. The support off the 35.00 psychological area seems to be holding up firmly for now as price formed a dragonfly doji rejection on 8 September 2017. The bullish reversal continued to work subsequently as price rebounded back above the 36.00 and 61.8% Fibonacci retracement level showing some sign of strength. Moreover, the bullish reversal since 8 September has lifted the oversold RSI back above the 30 range suggesting a mean reversion might be happening.

Hence, we expect the 35.00 psychological support area to hold and a continued sharp rebound to follow through for price to retest the 39.37 resistance area followed by 41.70.

Conclusion: We are bullish on T due to 1) its potential from its merger with TWX, 2) 5G and iPhone tailwinds and 3) its dividend and valuation. As such, we believe that stock has been oversold and with recent signs of recovery, we are bullish.

![]()

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: