Description

The Walt Disney Company (NYSE:DIS) is an entertainment company. The Company operates in four business segments: Media Networks, Park and Resorts, Studio Entertainment and Consumer Products & Interactive Media. The Media Networks segment includes cable and broadcast television networks, television production and distribution operations, television and radio stations. Under the Parks and Resorts segment, the company designs and develops new theme park concepts and attractions and resort properties. The Studio Entertainment segment products and acquires live-action and animated motion pictures, direct to video content, musical recordings and live stage plays. It also develops and publishes games, books, magazines and comic books.

Source: Thomson Reuters

Investment Rationale

DIS has the best content portfolio in the industry. The company owns Walt Disney Studios, Pixar Animation Studios, Marvel Studios and Lucasfilm Ltd. Collectively; these studios have been dominating box offices around the world and DIS has many upcoming movies set to continue that domination. Revenue generation from content does not stop at box office sales for DIS, with merchandising, theme parks etc. also contributing to the company’s bottom line. As the company continues to own rights to some of the most valuable intellectual properties (IPs), we believe that DIS remains well positioned to continue reaping the benefits from being the king of content. Along with its strong balance sheet and strong cash flows, we are bullish on DIS and believe that DIS is attractively valued at current price

Recent Price Action: Since its previous earnings results in May, the company has been on a down trend, falling from about its 52-week high of USD 116.10 to about its YTD low of USD 103.30. Recently, DIS has shown signs of rallying and closed about 3.75% up to USD 107.09.

Upcoming Blockbusters: DIS has been firing on all cylinders when it comes to the production of content. In 2016, of the top 10 highest worldwide grossing films, DIS produced 5 of them (with all 5 being the top 5): Captain America: Civil War, Rogue One: A Star Wars Story, Finding Dory, Zootopia, and The Jungle Book. Collectively, DIS claimed an estimated 26.3% Market Share of box office sales. YTD in 2017, DIS has 3 movies in the top 10 Worldwide grossing films; Beauty and the Beast, Guardians of the Galaxy Vol 2 and Pirates of the Caribbean: Dead men tell no tales. With half the year to go, DIS still has several highly anticipated films to be released this year. Star Wars: The Last Jedi, the sequel to 2015’s huge success, Star Wars: The Force Awakens, which is the 3rd highest grossing film of all time, is set to release in Dec 2017. Thor: Ragnarok, which is set in the Marvel Cinematic Universe (which as a franchise has earned nearly USD 3.8 bn in 2016, almost USD 1.5 bn more than the Harry Potter series), will release in Nov 2017 and finally a short film set in DIS’s bestselling Frozen, Olaf’s Frozen Adventure, which will release in theaters along with Pixar’s new film Coco in Nov 2017.

DIS reported USD 2.70 bn in operation income from their Studio Entertainment segment in 2016, up 37% YoY. As mentioned above, content revenue contribution does not stop at the box office for DIS. By capturing the imagination of consumers in theaters, DIS is able to translate that to sales of consumer goods and theme park attendance. Of note, Star Wars: Galaxy’s Edge, which is set to open in 2019, is a prime example of DIS monetizing their IPs past the box office stage. DIS earned USD 3.30 bn operating income on USD 16.97 bn in revenue from their Parks and Resort segment.

Direct to Consumer (DTC) streaming: ESPN, a key contributor to DIS revenues, has of late been a thorn in the side of DIS. With falling subscription numbers and lower cable viewership numbers, ESPN numbers has been the bane of DIS’s earnings results, with the market focusing on its recent poor performance. However, we believe that the concerns related to ESPN, while valid, might be overblown. The company has invested in BAMtech, with plans to launch a collaboration stream a multi sports subscription service. While the available content is not the full ESPN content, we believe that this represents a valid channel that DIS can distribute content to consumers should the fall in subscription numbers accelerate.

Besides sports offerings, as mentioned earlier, there is very high demand for DIS content, and we believe that there will be many lucrative deals with streaming services, such as Netflix or Amazon Prime, to have DIS content on their platform. As such, we believe that market concerns about falling cable subscription numbers are overblown.

Valuations: DIS’s closed at USD 107.09. It trades at a PER of 18.67, slightly below its 5 year average of 19.77. It has an Operating Margin of 25.74% and a Net Profit margin of 13.35%. Compared to its peers, Twenty-First century Fox Inc trades at a 16.94, Time Warner trades at a PER of 18.80. While DIS trades a PER that is comparable to its peers, given how dominating DIS’s content portfolio is and the potential for growth from it, we believe that DIS should trade at a premium compared to its peers. DIS pays a div of USD 1.56, representing a yield of about 1.46%, with a payout ratio of 26.4%. DIS has an Interest Coverage Ratio of 32.61 and Free Cash Flows of USD 8.44 bn in 2016. Our Target Price of USD 116.00 is set based on Technicals.

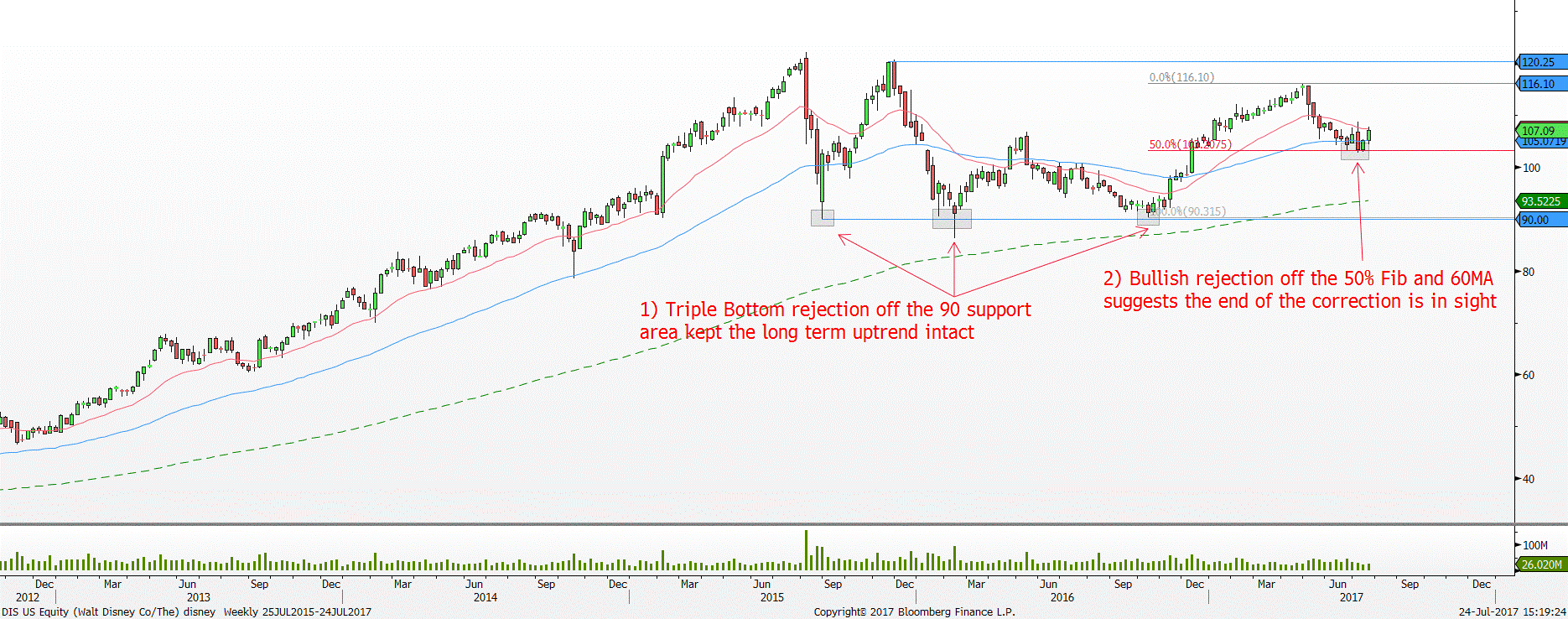

Technicals: DIS has been trending up steadily since October 2016 after the 90.00 psychological support area kept a floor on price. The uptrend continued until April 2017 where price experienced a correction of approximately 11%.

DIS weekly chart

Red line = 20 period moving average, blue line = 60 period moving average, Green line = 200 period moving average

Source: Bloomberg, PSR

Nonetheless, the long term uptrend remains intact as price continues to be supported off the confluence of 50% Fibonacci retracement level and 60 week moving average. The rebound off the 102.72 seems to be forming the next higher low point within the uptrend.

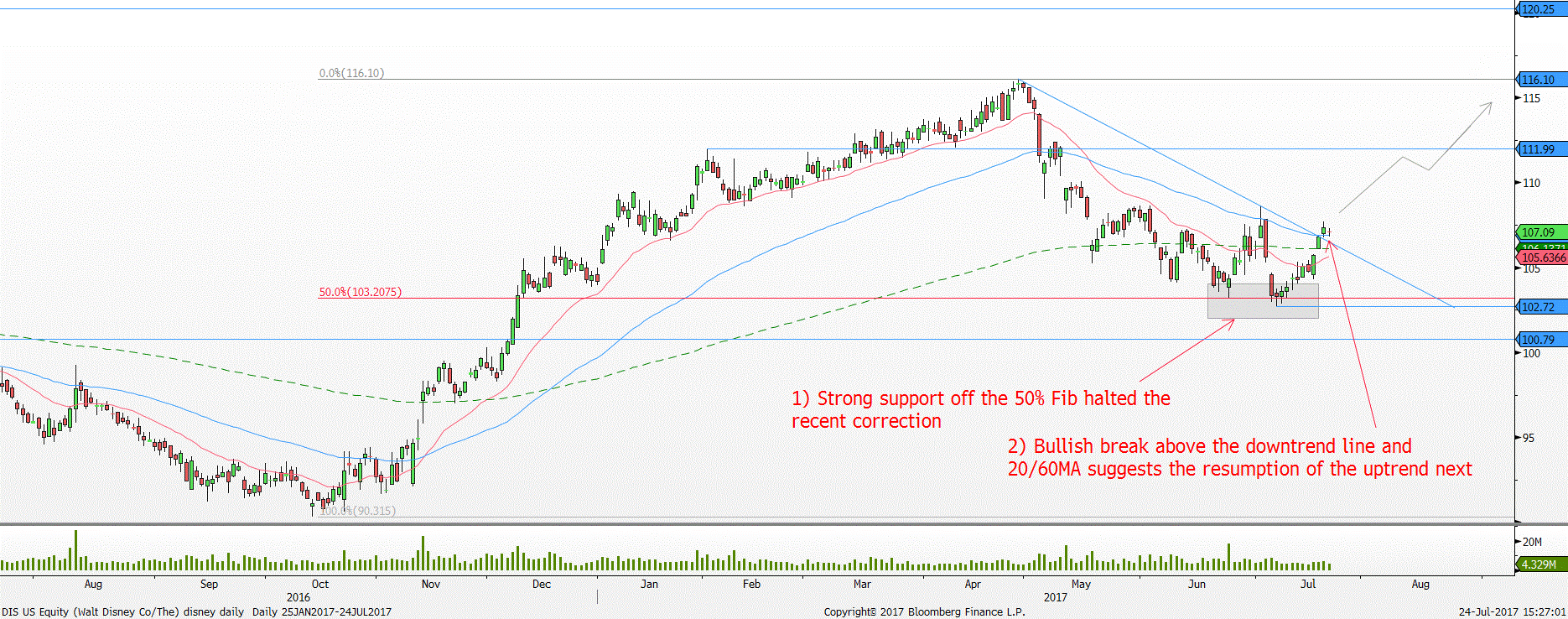

Zooming into the daily time frame suggests the bullish narrative is returning shown by the recent bullish break above the downtrend line on 20 July 2017. Moreover, price has also succeeded in closing above the 20 and 60 day moving average signals an acceleration in the bullish momentum.

DIS daily chart

Support 1: 102.72 Resistance 1: 112.00

Support 2: 100.79 Resistance 2: 116.00

Red line = 20 period moving average, blue line = 60 period moving average, Green line = 200 period moving average

Source: Bloomberg, PSR

Expect the uptrend to resume next for price to retest the 116.00 resistance area followed by 120.00.

Conclusion: We are bullish on DIS due to 1) its dominant content portfolio and upcoming blockbusters, 2) its transition to streaming and 3) its strong balance sheet and valuation. As such, we reiterate our belief that the stock was oversold after its earnings and with recent signs of recovery, we are bullish.

![]()

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: