Summary

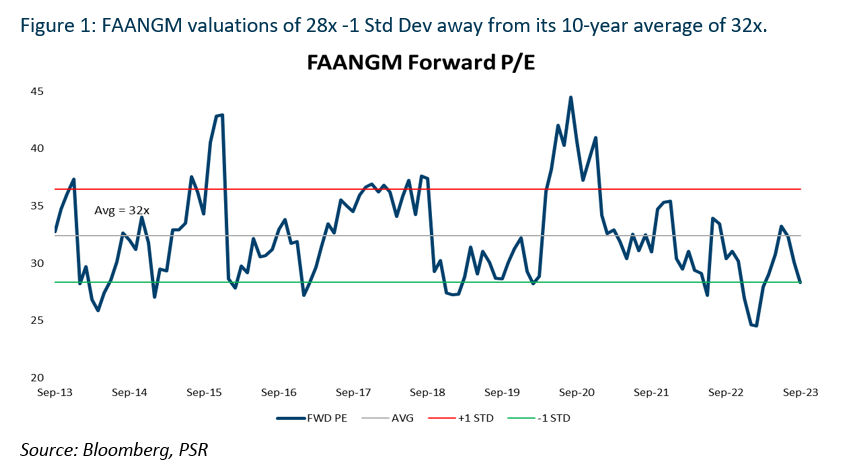

For September, FAANGM lagged the overall market for a 4th consecutive month, losing -5.7%. The S&P 500 and Nasdaq were also down -4.9% and -5.1%, respectively, as the overall market began to reprice a higher-for-longer interest rate narrative set by the Fed. The overall performance of FAANGM was underwhelming, with 5 of the 6 companies recording share price declines. It seems that growth investors are erring on the side of caution while awaiting earnings, with forward guidance from Big Tech companies expected to provide more clarity moving into 2024. Current FAANGM valuations are looking relatively more attractive, with its 12M forward P/E ratio (28x) moving -1 Std Dev away from its 10-year average.

Gainers: META was the biggest gainer (+1.5%) as it saw some price consolidation after a sharp decline in the prior month (Aug 23). In addition, positive news surrounding its developments in AI helped to sustain META’s share price.

Laggards: NFLX was the main laggard (-12.9%) likely due to concerns over tepid advertising revenue growth in the near term and vague long-term margin guidance. AAPL slipped -8.9% over weak semiconductor sales numbers from its partners and worries of a China government agency ban on the use of iPhones.

Review

Meta Platforms Inc (META US, ACCUMULATE, TP US$360)

Comment: Improvements in Meta’s new Quest 3 headset seem to be heading in the right direction, with a slimmer form factor from each upgrade and better overall performance. It is unclear whether Quest 3 could contribute meaningfully to the company’s revenue growth given the slowing sales in such hardware. Meta has also continued to leverage AI in developing new LLMs and other products to rival OpenAI, Google, and other AI-related companies.

Apple Inc (AAPL US, NEUTRAL, TP US$183)

Comment: We believe any potential iPhone sales growth will be driven by volume and mix as there is minimal increase in the average selling price (ASP). The iPhone lifecycle is estimated to be 3-4 years, implying that current iPhone 12 users are highly likely to upgrade this year. This presents a huge opportunity for Apple due to the large installed base of iPhone 12, as evidenced by the ~40% YoY iPhone sales growth back in FY21. However, the continued sales decline from major suppliers, such as Foxconn and TSMC, suggests that we should not expect an immediate rebound in sales growth. As for the new ban by China, we think it will not have a significant impact on Apple as it will only affect a fraction of the overall sales in the country.

Amazon.com Inc (AMZN US, BUY, TP US$175)

Comment: We believe the FTC lawsuit will not have a significant impact on Amazon’s financial performance in the near term. This is because such lawsuits typically take years to reach a verdict. Furthermore, the resolution sought by the FTC still remains unclear.

Netflix Inc (NFLX US, NEUTRAL, TP US$446)

Comment: The end of the Hollywood writers’ strike is a double-edged sword for Netflix, as content production can now continue, but it would seem at a higher price given the upgraded contracts for writers. This could hurt Netflix’s margin moving forward as costs rise, unless the company decides to increase subscription prices again. In addition, comments from the company’s CFO about ad revenue not contributing meaningfully to overall revenue growth in the near term, and vagueness surrounding long-term company margin guidance failed to shore up investor confidence.

Alphabet Inc (GOOGL US, BUY, TP US$144)

Comment: Given past experiences, the antitrust trial vs the DOJ could be an overhang for quite a while, with relatively unclear implications for GOOGL’s business. Additionally, GOOGL is also fighting to overturn a EUR2.4bn antitrust fine imposed by EU regulators in 2021, the first of 3 antitrust fines totalling EUR8.3bn.

Microsoft Corp. (MSFT US, ACCUMULATE, TP US$372)

Comments: For MSFT, we like the robust corporate demand for its cloud computing platform Azure and expect strong 1Q24e earnings results. Microsoft projects Azure revenue growth of 26% YoY in constant currency while Office 365 commercial revenue is expected to grow by 16% YoY. Meanwhile, Windows and Devices segment revenues will continue to decline due to continued PC market weakness.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: