Report type: Weekly Strategy

Will a string of good news for Japanese stocks absorb concerns?

The Nikkei Average has continued its upward trend since hitting a low of 26,632 points on 9/3. There are plenty of positive factors for Japanese stocks, including the following eight points:

① Robust trend of the number of foreign visitors to Japan in March, as announced by the Japan National Tourism Organization (JNTO), and the per capita travel spending of visitors to Japan from January to March, as announced by the Japan Tourism Agency, ② PM Kishida’s decision to present an “action plan” within this month that includes numerical targets for the establishment of supply chains in areas such as semiconductors as part of measures to promote investment from abroad, ③ Concerns about the earnings of US financial stocks were eased by the results of major banks and regional banks, as well as by the decision of Sumitomo Mitsui Financial Group (8316) to issue 140 billion yen in AT1 bonds (perpetual subordinated bonds), similar to bonds issued by Credit Suisse in Europe that had become worthless as a result of the acquisition by UBS, and as a sign of dispelling concerns over the financial system, Japanese financial and insurance stocks have bounced back and entered a rising phase, ④ Amid the global CPI growth rate remaining at a high level, investment money has been pouring into food, marine products, beverage and other related stocks on a global scale, as it has become easier to pass on increased costs to selling prices, ⑤ Companies such as NOK (7240), which produces oil seals for automobiles, are responding to the TSE’s request for improvement of low PBRs by announcing new medium-term management plans. Similar trends are expected to accelerate in the earnings announcements of Japanese companies, which are about to get into full swing, ⑥ The Jan-Mar GDP and March retail sales figures for China announced on 18/4 provide clues to a recovery in the Chinese economy, which is expected to benefit stocks with a high percentage of sales in China.

⑦ Factors that have been weighing down medical device makers, such as the tight management of medical facilities due to the Covid-19 pandemic, are improving, as seen in the earnings announcement of Intuitive Surgical, the maker of the da Vinci Surgical System in the US, ⑧ Nintendo (7974) has recorded record-high initial box office revenue for its animated movie based on the “Super Mario” game franchise, indicating that its business model transition to the use of abundant intellectual properties (IP) from its pillar of game operations is likely to show up in its financial results.

On the other hand, negative factors include: ① Concerns that aggressive price reductions by Tesla, a US electric vehicle (EV) company, will lead to lower profit margins for other automakers with relatively poor profit margins in the EV business, and ② some reasons for concern about overbuying in the short term could include the high “up-down ratio”, which represents the “number of rising stocks in 25 days divided by the number of falling stocks in 25 days” on the TSE Prime Market, as well as the “Nikkei Stock Average Volatility Index”, which is considered a fear index, hitting its lowest level since February 2020 on 19/4.

In the 24/4 issue, we will be covering Nisshin Seifun Group (2002), Toyo Suisan (2875), Olympus (7733), and Graphite Design (7847).

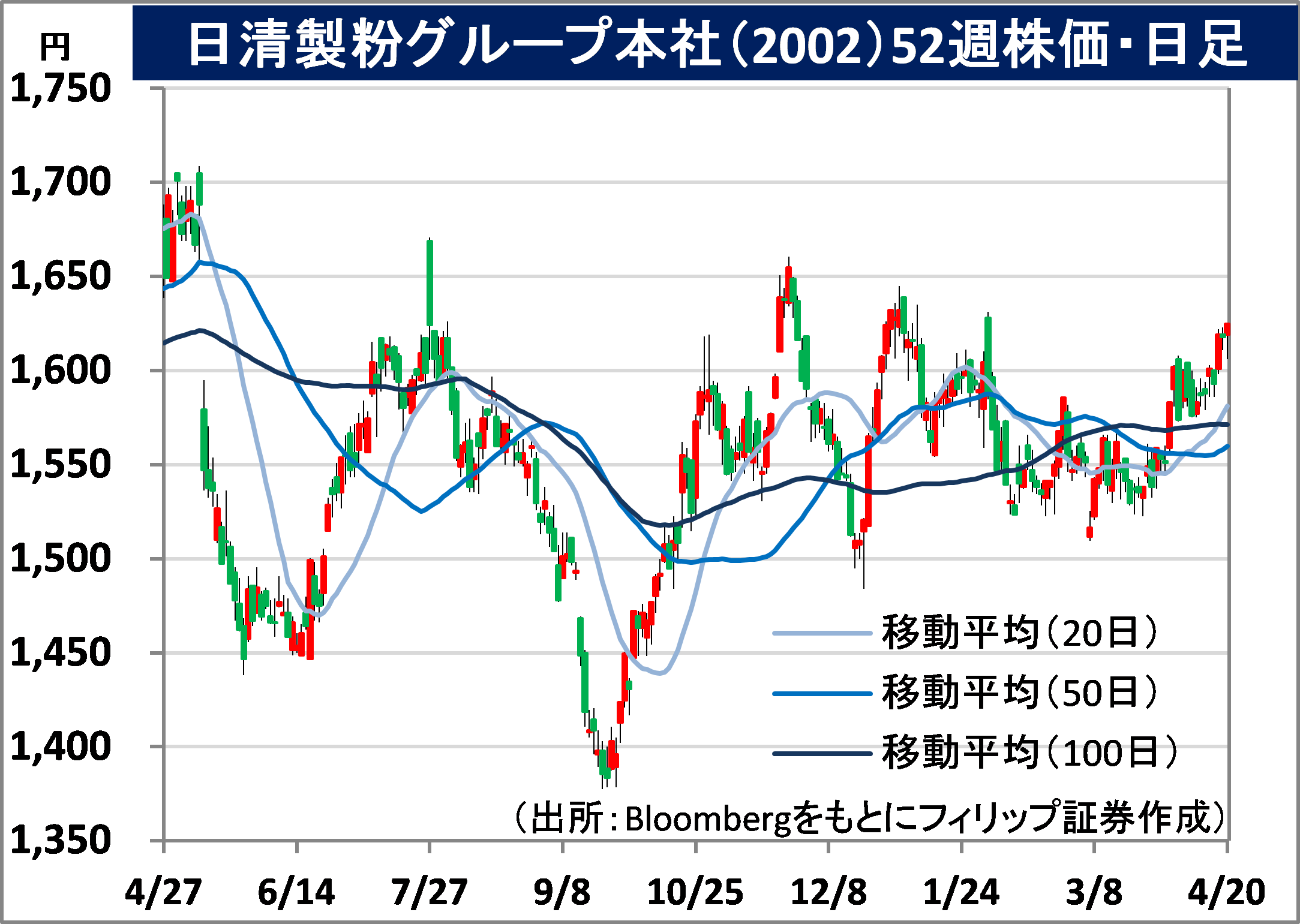

Nisshin Seifun Group Inc (2002) 1,617 yen (21/4 closing price)

・Founded Tatebayashi Flour Milling in 1900 in Gunma Prefecture (now Tatebayashi City). Operates a Flour Milling business handling flour, etc, a Processed Food business that manufactures and sells pasta, frozen foods, premixes, etc, a Prepared Dishes and Other Prepared Foods business, and an Engineering business.

・For 9M (Apr-Dec) results of FY2023/3 announced on 30/1, net sales increased by 18.7% to 600.0 billion yen compared to the same period the previous year, operating income decreased by 2.6% to 25.462 billion yen, and net income fell into the red to -22.9 billion yen due to impairment losses on the Australian flour milling business. The Flour Milling business remained strong both domestically and overseas with price increases, but in the Processed Food business, cost increases led to subsequent price revisions.

・For its full year plan, net sales is expected to increase by 14.8% to 780.0 billion yen compared to the previous year, operating income to increase by 12.1% to 33.0 billion yen, and annual dividend to remain unchanged at 39 yen. The flour milling industry has an advantage in terms of profitability as a business model that can easily pass on cost increases due to inflationary pressures through price increases. Last year, Kumamoto Flour Milling, which has a rice flour production line, became a subsidiary. Rice flour is attracting attention as a substitute for wheat when the market price of wheat soars, and the Ministry of Agriculture, Forestry and Fisheries (MAFF) is also aiming to promote rice flour to increase rice consumption.

Toyo Suisan Kaisha, Ltd (2875) 5,760 yen (21/4 closing price)

・Established in 1953 at Tsukiji Fish Market as Yokosuka Suisan. Operates six main businesses, namely seafood products, overseas instant noodles, domestic instant noodles, chilled foods, processed foods and refrigeration business. Ranks first in the US and Mexico for overseas instant noodle business, and second in the domestic instant noodle business.

・For 9M (Apr-Dec) results of FY2023/3 announced on 31/1, net sales increased by 21.3% to 325.3 billion yen compared to the same period the previous year, and operating income increased by 28.5% to 31.8 billion yen. In the overseas instant noodles business, which accounts for about 40% of total sales, sales increased 62% YoY and segment income increased 2.3x YoY due to strong sales of bagged noodles “Ramen” and cup noodles “Instant Lunch” in the US.

・For its full year plan, net sales is expected to increase by 22.5% to 443.0 billion yen compared to the previous year, operating income to increase by 37.9% to 41.0 billion yen, and annual dividend to remain unchanged at 90 yen. Demand for instant noodles continues to be high in the US, Mexico, and other overseas markets due to increasing levels of thriftiness associated with high levels of inflation. Aggressive efforts to strengthen the production system have been successful. US composite consumer price index (CPI) slowed to 5.0% YoY in March, but grain and grain product prices rose 13.6% YoY.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: