Report type: Weekly Strategy

“Possibility of both price and wage increases, acceleration of inbound consumption”

The dollar-yen exchange rate exceeded 150 yen per dollar for the first time in 32 years in overseas markets on 20/10. At the same time, RENGO (Japanese Trade Union Confederation) announced that in next year’s spring labor offensive, it will demand a 5% wage increase, the highest level in 28 years, including a uniform base salary increase and regular salary increases.

In August this year, the year-on-year rate of increase in the monthly labor statistics/total cash payrolls, and the national CPI (excluding fresh food and energy) was 1.7% (up 0.4 points from the previous month) and 1.6% (up 0.4 points from the previous month) respectively, showing signs of hovering around 2%. In the 11 October, 2022 issue of this Weekly’s “Corporate Price Outlook in the BOJ’s Tankan”, we had shown the outlook for price increases in one, three, and five years, as well as sales price forecasts with growth rates above those rates. At a discussion session in Washington, D.C., on 15/10, BOJ Governor Kuroda emphasized his stance to continue large-scale monetary easing to support the economy, saying that “price increases in Japan are temporary because they are not accompanied by wage increases”. This in turn implies that an “exit strategy” to reduce monetary easing will be considered when rising prices are accompanied by rising wages.

If the weak yen boosts inbound consumption by foreign visitors to Japan, encourages factory production to return to Japan from China, and accelerates the rate of increase in wages and prices, a major trend in the stock market will naturally take shape in the not-too-distant future, centering on exit strategies. At that time, a strong market can be expected, especially for megabanks and other banking stocks.

Even for inbound-related stocks, the share prices of airline and electric railway stocks, which are regarded as the main focus of market trading in this sector, are still left at low levels compared to 2019, before the spread of Covid-19. Looking at the closing prices on 20/10 on a relative index basis with the end of 2019 as 100, Japan Airlines (9201), ANA Holdings (9202), JR East (9020), and JR Tokai (9022) are all still in the 80-84 range. The July-September 2022 financial results of the three major US airlines (American Airlines, United Airlines, and Delta Air Lines), which are spearheading the recovery of the economy, show that the number of people who flew exceeded that of the same period in 2019. On top of that, a further increase in demand is expected from individuals who have been holding off on travel due to the spread of Covid-19. In this regard, there is little basis for assuming that the stock prices of major domestic air and electric railway stocks will catch up only to the levels at the end of 2019.

At the Communist Party Congress, held once every five years in China, President Xi Jinping strongly restrained Taiwan and the US by stating that he would “never renounce the use of force” over the unification of Taiwan. Being wary that 2027, when President Xi’s third term in office will end, will be the 100th anniversary of the founding of the Chinese People’s Liberation Army, the Biden administration has accelerated the provision of arms to Taiwan. As a result, amongst Japanese equities defense-related stocks may become more prominent.

In the 24/10 issue, we will be covering Kitoku Shinryo (2700), Alpen (3028), Serverworks (4434) and Japan Airlines (9201).

Kitoku Shinryo Co., Ltd (2700) 5,010 yen (21/10 closing price)

・Opened in 1882 in Kabuto-cho, Nihonbashi, as Kimura Tokubei Shoten, a rice dealer. Operates four businesses, namely, rice business, which makes and sells milled rice and brown rice, feed business, egg business, and food business, which manufactures and sells rice flour, processed foods, and other products.

・For 1H (Jan-Jun) results of FY2022/12 announced on 9/8, net sales decreased by 0.9% to 53.944 billion yen compared to the same period the previous year, and operating income increased 2.1x to 810 million yen. In the rice business, there were strong sales to convenience stores and a pickup in eating-out demand, but domestic rice transaction prices fell and sales to household products at mass merchandisers were weak. Improvements in inventory and purchasing had successfully resulted in profits.

・For its full year plan, net sales is expected to decrease by 4.5% to 103.0 billion yen compared to the previous year, operating income to increase by 90.0% to 1.0 billion yen, and annual dividend to increase by 10 yen to 60 yen. Purchasing in response to the supply-demand environment and the establishment of multiple purchasing routes are expected to continue to contribute to profits. The Food Price Index for September released by the UN Food and Agriculture Organization (FAO) was 136, up 5.5% from the same month the previous year. CBT wheat futures have also been on a reversal uptrend since July. Substitution demand for relatively low-priced rice and rice flour is therefore expected.

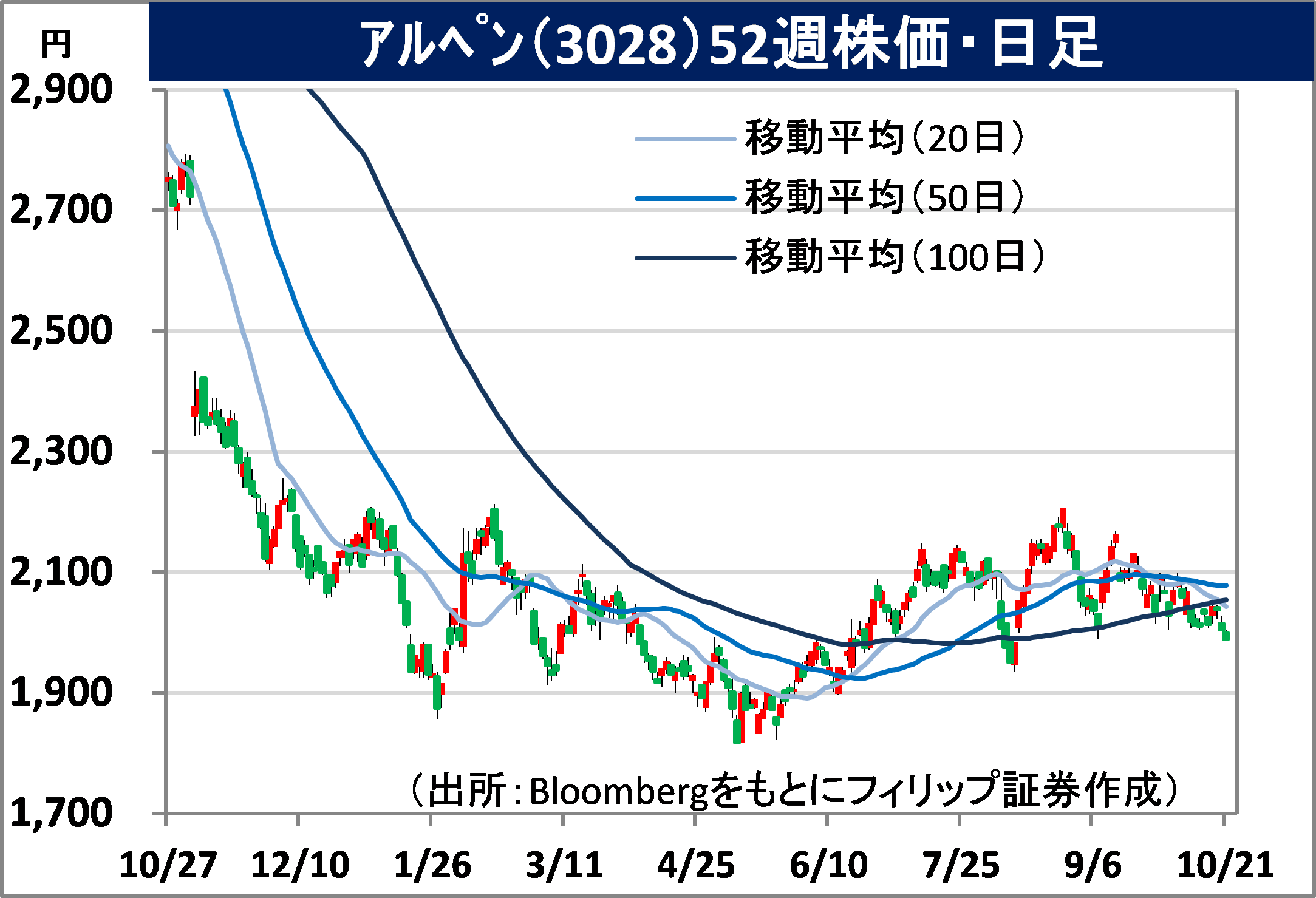

Alpen Co., Ltd (3028) 1,989 yen (21/10 closing price)

・Established in Nagoya in 1972. Founding business was the development of own-brand products for ski equipment. In addition to the Winter Division, company manufactures and sells sporting goods in the Golf, Sports Lifestyle, Competitive/General Sports, and Outdoor Divisions.

・For results of FY2022/6 announced on 4/8, net sales decreased by 0.4% to 232.332 billion yen compared to the previous year, and operating income decreased by 52.6% to 7.153 billion yen. Existing-store sales of golf products were strong due to an increase in the number of people playing this sport where crowds do not gather, and sales of winter goods also increased thanks to snowfall. On the other hand, Sports Lifestyle, Competitive/General Sports, and Outdoor businesses dropped.

・For its FY2023/6 plan, net sales is expected to increase by 6.7% to 248.0 billion yen compared to the previous year, operating income to increase by 0.7% to 7.2 billion yen, and annual dividend to remain unchanged at 50 yen. Company’s priority strategy is to improve the convenience of both real stores and EC by responding to the EC market in the digital domain. With an increase in foreign tourists, and the government’s “nationwide travel support” program, ski resorts and winter sports are expected to be active with the arrival of the first season in three years without movement restrictions.

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: