Company Background

Fortress Minerals (FML) is an iron ore concentrate producer in Malaysia. As FY2019 was the Group’s maiden year of commercial production, profitability margins were partly crimped by initial ramp-up costs and gestation. Its mining concession is located in Bukit Besi, Terangganu, Malaysia, with 7.18MT of reserves and 13 years of concession life.

FML explores, mines, produces and sells magnetite iron-ore concentrate. Steel is the world’s most commonly used metal and iron ore is a key ingredient in steel-making. FML sells primarily to steel mills in Malaysia and China.

Investment Merits

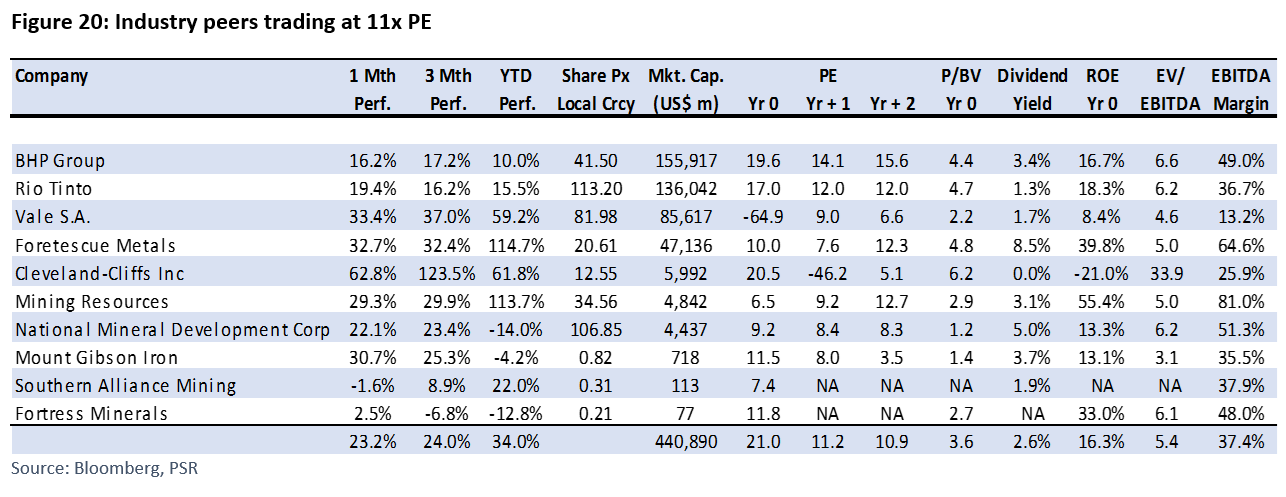

We initiate coverage with a BUY rating and TP of S$0.28. Our TP is based on 11x FY21e PE, in-line with industry average.

About FML

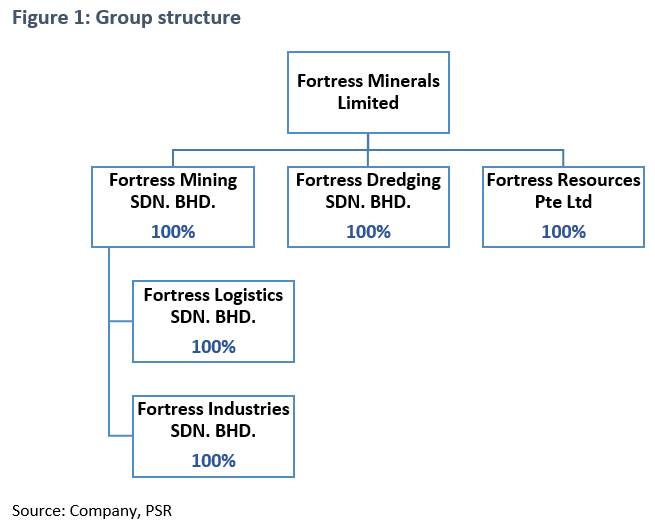

FML was incorporated in Singapore on 13 November 2017 as a private limited company. It was listed on the Catalist on 27 March 2019. It operates its mine through its subsidiary, Fortress Mining.

Business operations are located in Kuala Lumpur, Malaysia, though its Bukit Besi mine is situated in Bukit Besi, Terengganu, Malaysia.

REVENUE

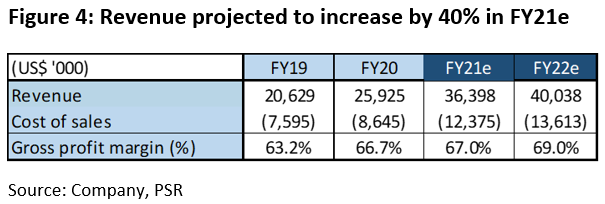

With the company’s first shipment of iron-ore concentrate in 2QFY19, revenue in FY20 increased 25.7% YoY to US$25.9mn. Sales revenue is calculated from average realised prices (per dry metric tonne, DMT) multiplied by the volume of iron ores sold. Average realised prices are benchmarked to the Platts Iron Ore index (IODEX), Daily Iron Ore Price Assessment for composition of 65% Fe CFR (cost and freight terms) North China.

Net profit in 1HFY21 was higher than the whole of FY20 on the back of higher volume sold. The latter compensated for lower average realised selling prices.

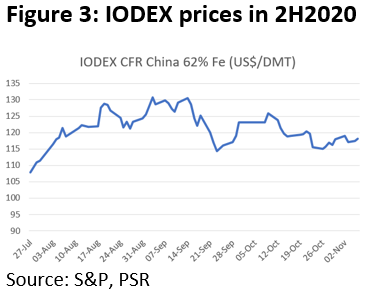

IODEX iron-ore prices have been above the US$110/DMT mark for the past two months (Figure 3). As iron-ore prices hit a seven-year high, FML is expected to realise higher revenue.

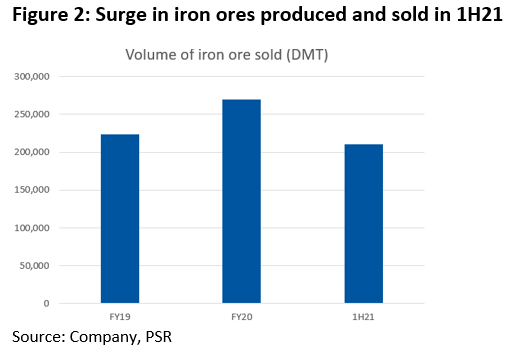

1HFY21 revenue was US$20.1mn. There was a 60% YoY surge in sales volume for 2QFY21, which good weather conditions partly contributed to. Assuming FML maintains production levels prior to 2QFY21, it should be able to achieve revenue of US$36.4mn for FY21e (Figure 4).

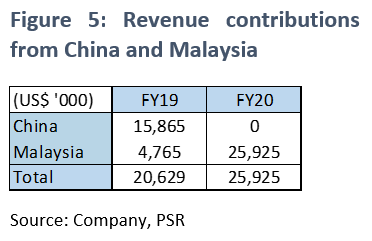

There was no revenue contribution in FY20 from steel mills in China (Figure 5). In 9MFY21, FML sold iron-ore concentrates to 3-4 major customers in Malaysia. It has been focusing on demand from domestic steel mills since 2019.

Offtake agreement. FML announced on 1 September 2020 that one of its subsidiaries, Fortress Resources, had inked a new one-year offtake agreement with a domestic steel mill in Malaysia. Fortress Resources will deliver 400,000 WMT of iron ore to this customer over 1 September 2020-31 August 2021. This volume is more than the total volume it sold in FY2020. The selling price of the iron ore concentrates will be based on a formula guided by the average of the available daily price of Platts for 65% Fe CFR North China, adjusted subject to the Fe content of each shipment of the deliverables.

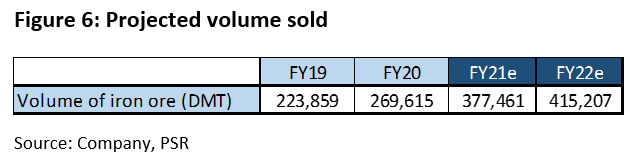

We estimate a 10% YoY increase in volume sold for FY22e (Figure 6).

EXPENSES

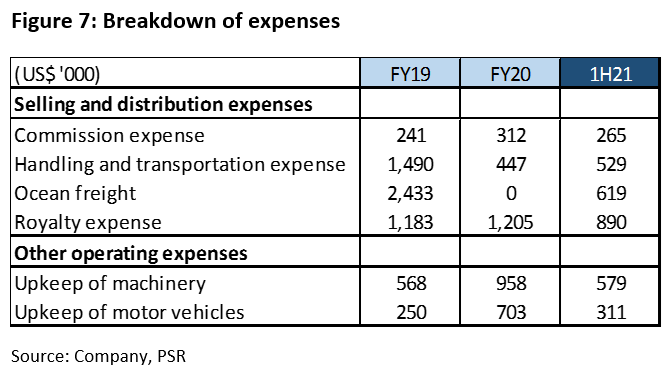

Main expense items in 1H21 were royalties payable to the State Government of Terengganu, and holder of mining leases for its concession, ocean freight, transportation, labour, plant and overheads.

FML pays a royalty fee directly to the State Government of Terengganu at the rate of 5.0% of revenue or as specified by the government, and holder of the mining leases at triple the rate of the former.

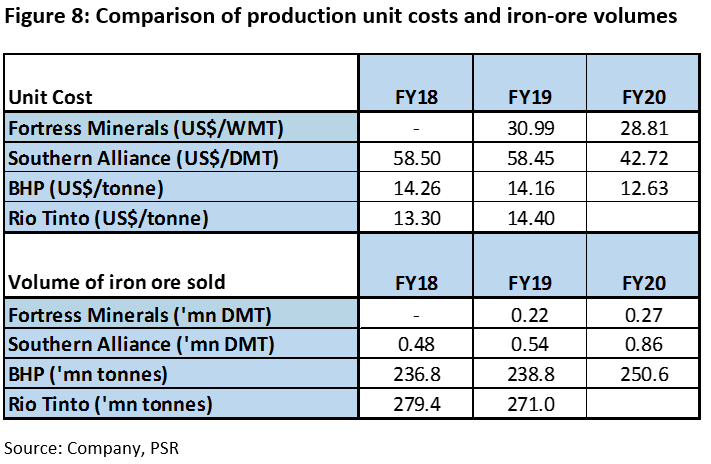

FML constantly takes steps to reduce its unit costs, including continuous implementation of productivity improvement and cost management strategies. The company managed to reduce average unit costs by 7.0% from FY19 to FY20. With larger volumes production, it should be able to benefit from economies of scale.

BALANCE SHEET

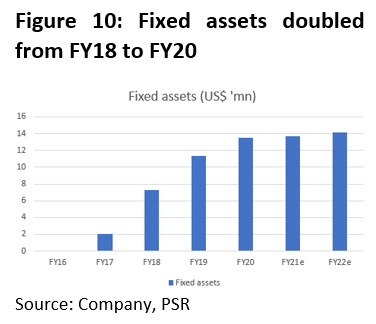

Assets. Fixed assets doubled from FY18 to FY20 (Figure 10), with plant and equipment increasing from US$7.3mn to US$13.5mn. This was the result of plant expansion.

Liabilities. FML has very low levels of borrowings. It had a net cash position of US$2.1mn in FY20.

CASH FLOW

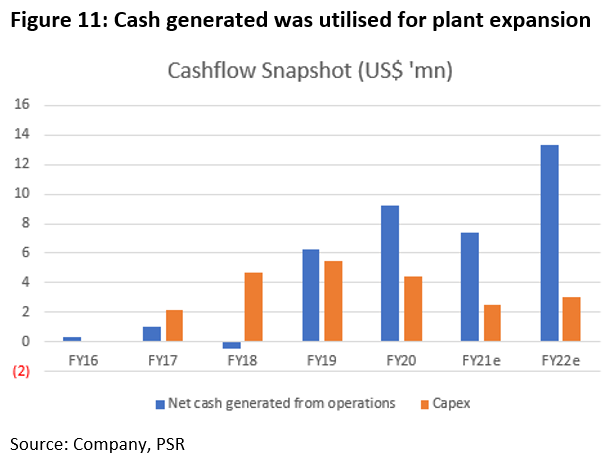

Cash flows have been strong since listing in 2019, considering commercial production only started in FY19 (April 2018). Cumulative operating cash flow from FY18 to FY20 was US$15mn. Capex averaged US$5mn for the same period.

Investment Thesis

Risks

INDUSTRY

Iron ore is the source of primary iron for the world’s iron and steel industries. About 98% of iron ores produced are converted into pig iron for steel-making, which is widely used in the construction of buildings, bridges, household appliances, transport vehicles, etc.

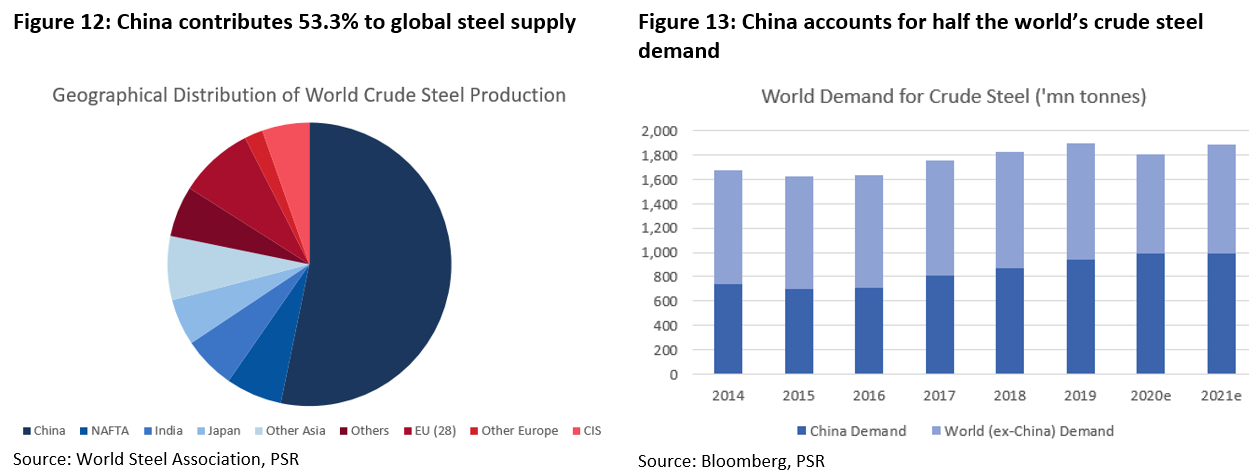

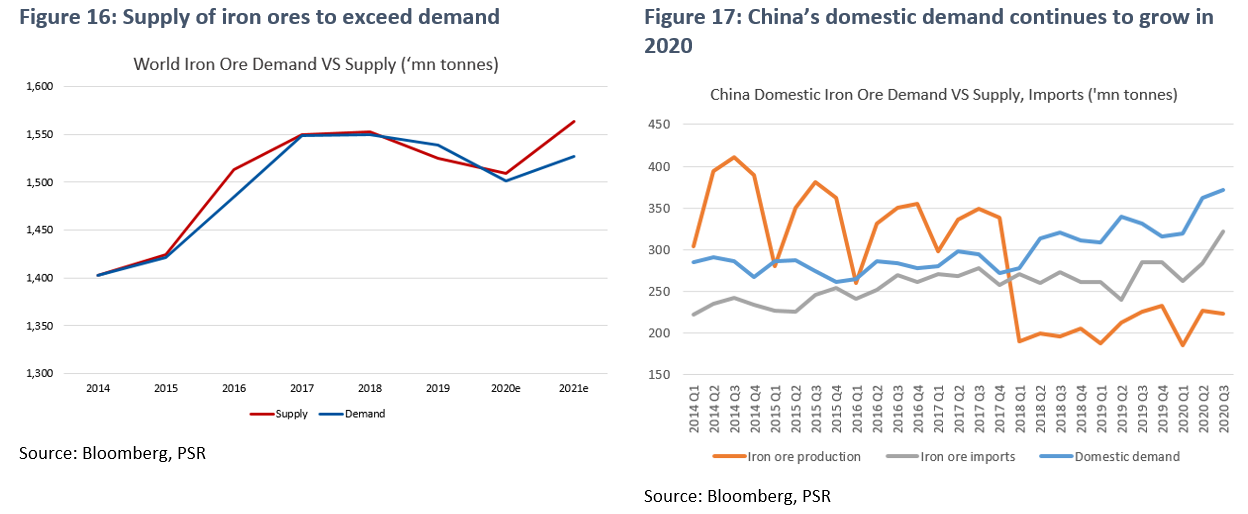

China is the world’s largest producer and consumer of crude steel. It accounts for 53.3% and 49.2% of the world’s production volume and demand respectively. It is also the world’s largest importer of iron ores, making up about 70% of the world’s demand. Demand from China has been supporting the uptrend in iron-ore prices since 2016.

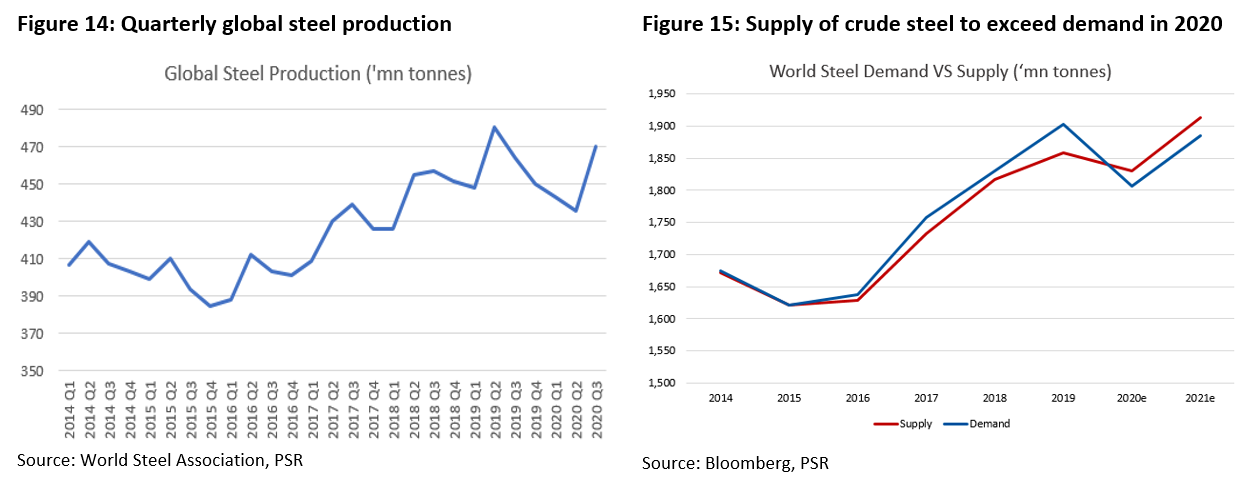

Steel production. With the manufacturing sector reeling from Covid-19 measures, steel production fell sharply in 2Q2020 (Figure 14). Recovery has been uneven across the countries, depending on their containment of the virus, stimulus measures, etc. As such, world steel consumption is expected to contract by 5% this year, before expanding in 2021 (Figure 15).

Iron ore. Being one of the first countries in the world to resume economic activities after its successful containment of the coronavirus, China’s domestic demand for iron ores and imports has been increasing since 2Q2020. China’s persistent demand combined with a seasonal drop in supply from Australia and Brazil have bumped up iron-ore prices. Throughout the pandemic, the prices of iron ore have been remarkably resilient, trading with low volatility.

Mid-term, iron-ore prices are expected to dip from their peak due to a restocking of supplies. In the short term, demand from China is expected to remain robust. For the rest of the world, we expect demand for iron ores to recover only from 2021.

Malaysia. The construction industry is the basic source of steel demand in Malaysia. In Malaysia’s Budget 2020, the government pledged to continue or revive mega-infrastructure projects such as the Bandar Malaysia central transport hub project. It is projected that steel consumption in the country will grow from 9.4mn tonnes in 2017 to 12.4mn tonnes in 2025, at a CAGR of 3.5%.

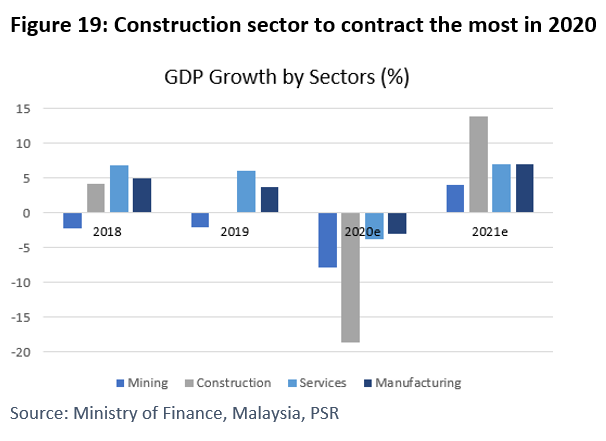

Under Malaysia’s more recent Budget 2021, the government has pledged to allocate more resources to “restart” the economy. GDP is expected to contract by 4.5% in 2020 due to the pandemic, before returning to 6.5-7.5% growth in FY21.

Outlook. The construction sector is expected to shrink 18.7% in 2020, led by significant contractions in all subsectors: civil engineering, residential and non-residential buildings. The sector is expected to return to growth of 13.9% in 2021.

Mining GDP is expected to contract by 7.8% in 2020 and increase by 4.1% in 2021.

For the first 9 months of 2020, the production of iron and steel bars and rods in Malaysia grew by 5.5% YoY. On the basis of a recovery in the economy and construction sector in 2021, demand for steel and iron ore is expected to increase.

FML faces competition from both PRC and global iron ore producers. There are 3 other main competitors in Malaysia. There are no figures available regarding the market share of these companies.

Fortress mainly serves their group of captive customers in Malaysia and has achieved remarkable growth in a short span of 2 years. The desire to achieve greater economies of scale through higher production volume will drive all iron-ore producers to continue their expansion plans, in terms of increasing processing capacity and acquisitions.

Valuation

We initiate coverage of FML with a BUY recommendation. Our TP is pegged to 11x FY21e PE (Figure 20).

FML has been trading at a discount to its larger peers in Australia and Brazil due to its smaller scale, liquidity and short history. With the higher (ROE) returns and faster growth than the industry, we believe FML should trade in-line with peers.

In the near term, the company may be affected by iron-ore prices coming down from their peak. Mid-term, demand and the price of iron ore should grow as Malaysia and China ramp up their steel production.

FML’s expanded capacity in the last two years has positioned the company well to meet higher demand. It also has considerable exploration upside in its mining concession, as only 5% of its concession has been explored so far.

The report is produced by Phillip Securities Research under the ‘Research Talent Development Grant Scheme’ (administered by SGX).

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note: