Expect loans growth to remain on target

Between 10-15% of UOB’s loans book is trade related, with the bulk anchored out of South-East Asia. Hence we do not expect the trade war to pose significant risks to trade loans growth unless it escalates into an overall global slowdown. UOB has the largest proportion of property-related loans (50% of total loans) as compared to DBS (42%) and OCBC (42%). Mortgage-related loans at 27% of total loans, and building and construction at a further 23% of total loans. Due to drawdowns of previously approved loans, weakness in the property-related loan market may only be felt next year. Lending to the property developer market is expected to hold up in the short-term. To put things into context, for UOB to miss their full-year loans growth target by 1% point, housing loans and building and construction loans would have to contract 3-4% YoY. Taking into account near-term uncertainties in trade and expectation of a more moderate pace in property transaction volumes, we are forecasting loans growth of 8.4% and 5.9% for FY18e and FY19e respectively.

Rising interest rates not expected to have near-term impact on NPL

The rising interest rate environment is not expected to have a significant impact on NPL. Housing loans made up 22% of total loans with unemployment being the driving factor on defaults on housing loans, not interest rates. Housing loans were also assessed using a 3.5% rate on loan repayment, higher than the current interest rate level. Average LTV in mortgages is 60%.

Credit considerations used to monitor loans to property developers

Some examples of credit considerations include approval of loan only upon certain percentage of units sold, disbursements according to % sales and completion, ring-fencing of proceeds from project (for servicing bank loan), track record of sales history of past projects from same developer to assess potential demand of current project, haircuts on LTV to determine loan amount etc.

Loan book pegged mainly to floating rates

Around 80% of the loan book is pegged to floating rate (30% belongs to SIBOR and SOR; and 50% belongs to prime rates and board rates etc.), and the remaining 20% is pegged to fixed rates. Certain corporations prefer to use SOR because they perceive SOR as much more transparent. Board rates are pegged to the bank’s own benchmark rate and differ from product to product and across different customers. Board rates are more popular as it is less volatile. The bank adjusts its board rates internally according to market conditions, cost of funding and the rates of its products to prevent product cannibalism.

O&G sector no longer a cause for asset quality concerns

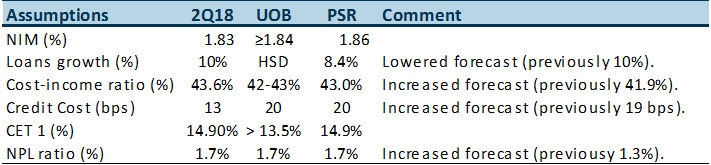

The O&G sector has stabilised, but it is unlikely to see consistent recoveries every quarter. Any recoveries for the sector would be a bonus for the bank. O&G non-performing assets were brought down to 10% of its asset value as the collateral value for recovery. Non-performing loans that have bounced back from the brink will be moved to performing loans, but collateral values cannot be marked up once it is marked down. Any gains can only be recognized in P&L when the asset is sold. UOB’s NPL ratio was 1.68% as of June-18, higher than DBS (1.56%) and OCBC (1.38%). We adjusted our NPL to be in line with management’s guidance of NPL ratio of 1.7% for the full year (previously 1.3%).

Lower credit costs

Historically, the long-term credit cost averages around 28bps, factoring in the peaks and troughs. Given the new accounting standards, banks are no longer allowed to use general provisions as buffers. Credit cost is currently at a low of 11bps for 1H18. Hence in the current benign environment coupled with the possibility of recoveries, management’s credit cost guidance of 20-25 bps is reasonable, and we put in our credit cost assumption at 20bps.

Funding pressure as bulk-up up on time deposits

In anticipation of steeper interest rates, UOB has been strengthening its funding position. Total deposits rose S$13.7bn QoQ in 2Q18, of which S$10.8bn came from fixed deposits. In comparison, 1Q18 total deposits only rose S$1bn QoQ. The aggressive sourcing of funds even resulted in lower LDR ratio in 2Q18 of 85.7% (1Q18 LDR: 86.7%). As the bulk of the deposits raised were pricier fixed deposit, it resulted in a squeeze in interest margins, albeit in the near term.

Expect operating costs to be slightly elevated

As UOB continues to invest in technology to enhance digital proficiencies in its business and the Digital Bank, we expect full year CIR to remain elevated at current levels (2Q18’s CIR was 43.6%). We adjusted operating expenses upwards to bring full year CIR to 43% (previously 42%).

Potential for higher dividends remain a catalyst

Guidance for full-year dividend payout is at 50% payout ratio (special dividend is part of this payout ratio), subject to a minimum CET1 ratio of 13.5%. UOB‘s 2Q18 fully loaded CET1 was already higher than its peers at 14.5%, and by adhering to a 50% dividend pay-out guidance, we increase our dividend forecast to S$1.20/share (previously S$1.05/share) to give dividend yield of 4.5%.

Least exposed to China and trade war repercussion

UOB’s exposure to trade war effects is relatively muted as compared to its peers. UOB has the largest percentage of Singapore loans (2Q18: 52% of total loans) as compared to DBS (47%) and OCBC (41%), and the least exposure to Greater China loans (2Q18: 15% of total loans) as compared to DBS (16%) and OCBC (26%).

Net trading income

UOB enjoys its net trading income from transaction spreads. Volatility has an influence on customer flows, as the need to hedge turns more acute. Between 60-70% of trading income comes from customer flows and the remaining 30-40% proprietary trading mainly belongs to derivatives to hedge structural positions. Every quarter’s marked to market changes in trading assets will flow to net trading income.

Table 1: UOB guidance vs. PSR estimates for FY18e

Source: Company, PSR

Investment Actions

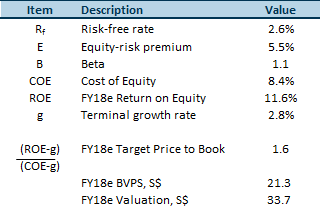

Maintain BUY with target price of S$33.70 (previous TP S$34.50) based on the Gordon Growth Model. The decrease in target price was due to our lower ROE assumption (previously 11.8%) and lower BVPS assumption (previously S$21.6).

Valuation: Gordon Growth Model

Important Information

This report is prepared and/or distributed by Phillip Securities Research Pte Ltd ("Phillip Securities Research"), which is a holder of a financial adviser’s licence under the Financial Advisers Act, Chapter 110 in Singapore.

By receiving or reading this report, you agree to be bound by the terms and limitations set out below. Any failure to comply with these terms and limitations may constitute a violation of law. This report has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this report by mistake, please delete or destroy it, and notify the sender immediately.

The information and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this report has been obtained from public sources which Phillip Securities Research believes to be reliable. However, Phillip Securities Research does not make any representation or warranty, express or implied that such information or Research is accurate, complete or appropriate or should be relied upon as such. Any such information or Research contained in this report is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this report are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this report is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This report should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this report has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this report is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this report involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this report should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this report, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this report.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold an interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this report. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, which is not reflected in this report, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this report.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction.

This report is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this report may not be suitable for all investors and a person receiving or reading this report should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

This report is not intended for distribution, publication to or use by any person in any jurisdiction outside of Singapore or any other jurisdiction as Phillip Securities Research may determine in its absolute discretion.

IMPORTANT DISCLOSURES FOR INCLUDED RESEARCH ANALYSES OR REPORTS OF FOREIGN RESEARCH HOUSE

Where the report contains research analyses or reports from a foreign research house, please note:

Min Ying covers the Banking and Finance sectors. She has experience in external audit and corporate tax roles.

She graduated with a Bachelor of Accountancy with a major in Finance from SMU.