Zhongmin Baihui Retail Group – Nanjing store closed; Return to home ground August 26, 2016 606

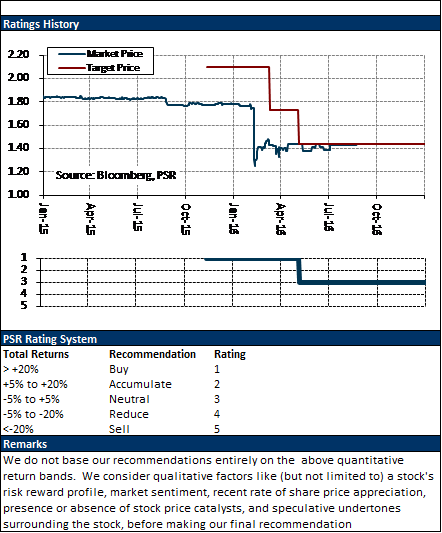

PSR Recommendation: NEUTRALStatus: Maintained

Target Price: 1.44

1H16 Revenue/PATMI met 55%/148% of our FY16 expectations; excluding impact from Nanjing store closure, PATMI met 60% of our FY16 forecast

Two new stores by 2H16; expect new stores to continue to support topline growth

Minimal impact from Nanjing Nanzhan store closure, financial gains are majorly non-cash in nature, while termination compensation costs should be manageable

Declared an interim dividend of 1.0 Singapore cents per share (same as 2Q15)

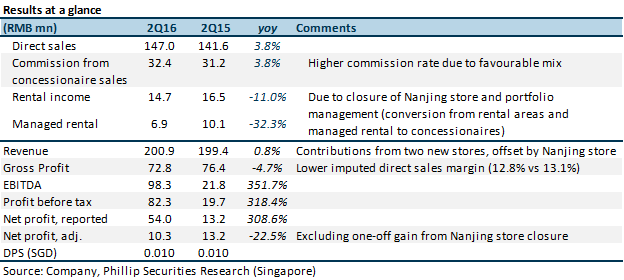

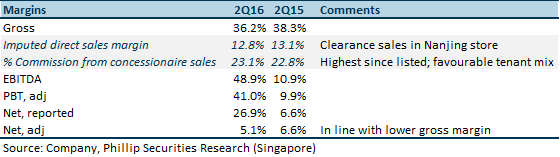

1H16 revenue growth at -0.4% year-on-year (yoy), dragged by soft 1Q16 and Nanjing Nanzhan store. Topline growth turnaround to 0.8% yoy in 2Q16 from -1.5% yoy in 1Q16. The two new stores, Putian Xianyou store (opened in December 2015) and Quanzhou Wanxiang (opened in January 2016) contributed about 3% to 4% yoy growth in 1H16; but were offset by slower turnover in Nanjing Nanzhan store at -2% yoy as it was in the process of ceasing its operation.

We expect minimal impact from closure of underperforming Nanjing Nanzhan store

Cutting losses and redeploying resources to increase shareholders value. Nanjing store is the second underperforming store shuttered, after Xiamen Zhongshan store last year. The store has remained unprofitable since its opening in September 2012 due to the slow development of its surrounding area. Nanjing store recorded RMB6.9mn losses in 1H16, c.7% lower yoy from its restructuring measures. 2H16 should see a better bottom line without Nanjing store losses weighing against it. The store-closing sales have ended around end-May 2016. The department store and supermarket sections of the store have ceased operation with the remaining tenants in the process of moving out.

Expect minimal termination compensation paid to landlord, tenants and staff. Management shared that compensation to landlord is still under negotiation, but the amount should be negligible as it was a termination by mutual consent. Meanwhile, only a small group of tenants are eligible for compensation – most of the tenants either have violated their lease agreements due to untimely rent payments, or have short term leases. Retrenchment cost are contained, as (i) the Group has been rightsizing manpower, and (ii) some of the staff could be redeployed to the new stores. Under Chinese law, severance pay amounts to one month’s pay per year of service and the number of employees in Nanjing store stood at 300 in 2Q16 (c.70% lesser compared to 2012’s).

Back to physical-stores-only model. Nanjing store was the only store that rolled out e-commerce services. Management will consider re-including online channel but not in near term. Nonetheless, the sales from e-commerce has been immaterial as it was still in gestation stage.

Redirect focus back to Fujian, expect two new stores by end-FY2016

One new self-owned store (16,900 sqm) to replace its existing managed store (4,000 sqm) in Quanzhou Quangang

The new store is expected to commence business in end-September 2016, a year earlier than expected (initial targeted date to open: by 2017/18). The new store is in line with its effort to wind down managed stores. It will be replacing the managed store in vicinity, with about a week’s transition period. The staff from the existing store will be redeployed to the new store.

Quanzhou Anxi new store (3,700 sqm)

A slight delay in store opening (initial targeted date to open: June 2016) as it is still undergoing renovation and pending government’s approval.

Total store count of 14 (11 self-owned stores and 3 managed stores) with GFA over 180,000 sqm (c. -8% yoy) by end-FY2016.

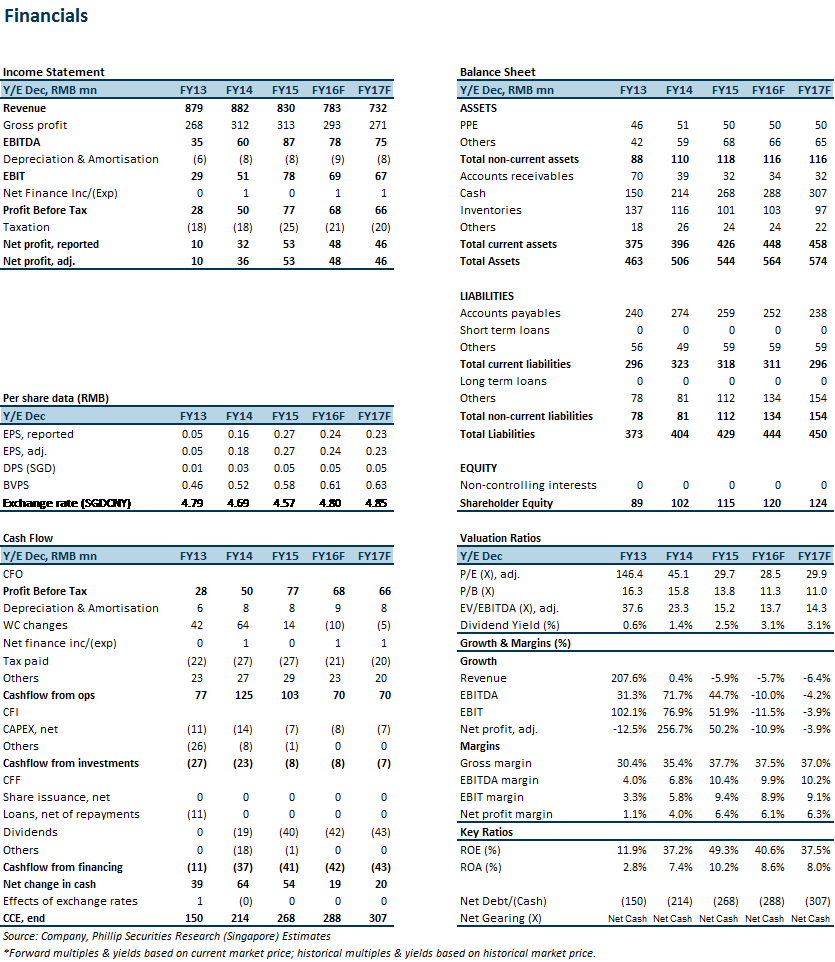

Maintain “Neutral” rating with unchanged TP of S$1.44, this implied a forward P/E multiple of 28.5x over 0.24 Singapore cents EPS.

Subscribe

0 Comments

Inline Feedbacks

View all comments

About the author

Soh Lin Sin Investment Analyst Phillip Securities Research Pte Ltd

Lin Sin has been an investment analyst in Phillip Securities Research since June 2014, where she started as an economist, focusing on China and ASEAN macroeconomics. Currently, she covers primarily the Consumers and Healthcare sectors in Singapore equities market.

She graduated with a Bachelor of Science in Mathematics and Economics from NTU.