The Positives

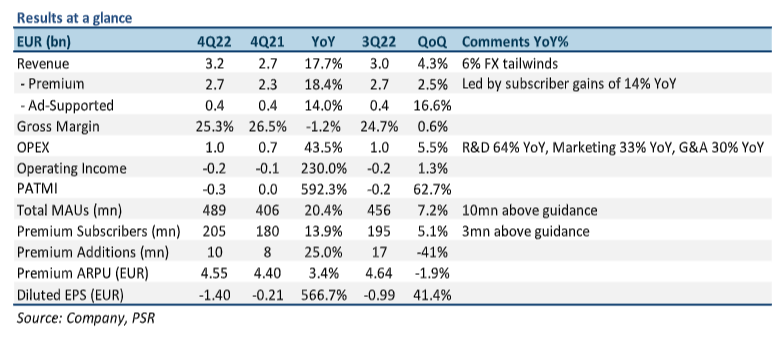

+ Premium subscriber base growing better than anticipated. SPOT ended 4Q22 with 205mn subscribers (14% YoY), with 10mn additions – 3mn more than it guided. Premium ARPU was up 3% YoY, with premium revenue hitting EUR2.7bn, 18% YoY. MAUs also hit 489mn for the quarter (20% YoY), with a record 33mn new users – 10mn above guidance. The strong set of subscriber/MAU numbers seemingly is validation of the company’s continuous investments in content and platform improvements over the last several years. SPOT guided 500mn MAUs, and 207mn premium subscribers by end 1Q23e.

+ Gross margin beat guidance by 0.8%, operating loss slightly ahead of guidance. Gross margin for 4Q22 was 25.3%, 0.8% above guidance primarily due to lower-than-expected podcast content spend and continued growth in its core music business. Operating loss of -EUR231mn was also slightly better than expected as SPOT benefitted from slowing expense growth. Guidance for 1Q23e is for slightly lower gross margin of 24.9% and operating loss of -EUR194mn due to some drag by severance-related charges and unfavourable FX impact.

The Negatives

– Operating expenses growth to slow, but still growing faster than revenue at 44% YoY. Operating expenses for 4Q22 came in at EUR1.0bn, or roughly 44% YoY, and 6% QoQ. Expenses growth was driven primarily due to higher headcount cost and increasing advertising expenses, with R&D up 64% YoY; Sales & Marketing up 33% YoY; and G&A up 30% YoY. However, expenses growth did slow from 65% YoY in 3Q22, and is expected to continue slowing for the remainder of FY23e with a 6% cut in headcount, reduced investments, and a shift in focus towards improving profitability.

Jonathan covers the US technology sector focusing on internet companies. Formerly a national and professional athlete, he graduated from the University of Oregon with a Bachelor’s Degree in Social Sciences.