What’s in the News?

SEHK has begun offering trading in Iron Ore Futures contracts as Iron Ore prices experience higher volatility.

Key advantages of SGX

What do we think?

SGX will remain a dominant venue for iron ore trading because of its well-entrenched position in offering a comprehensive range of iron ore related bulk products. The creation of the iron ore complex that includes coking coal and FFA was built over time and could not be simply pieced together to function as a “plug and play” platform. Recall that in our report on the acquisition of the Baltic Exchange in September 2016, we believed that the synergies between FFA and iron ore were remote as global trade was weak. But on hindsight, the purchase of the Baltic Exchange was an early stage strategy to create a credible product that would stack well with the iron ore ecosystem and enhance SGX’s competitive moat. So we believe that SGX’s insights in this area of the derivatives business places it ahead of its competitors. We also think that SEHK’s strategy to engage market participants through clearing members using screen based tools and trading fee waivers would appeal to price-taking market participants but that would be insufficient to create a robust market place.

Investment Actions

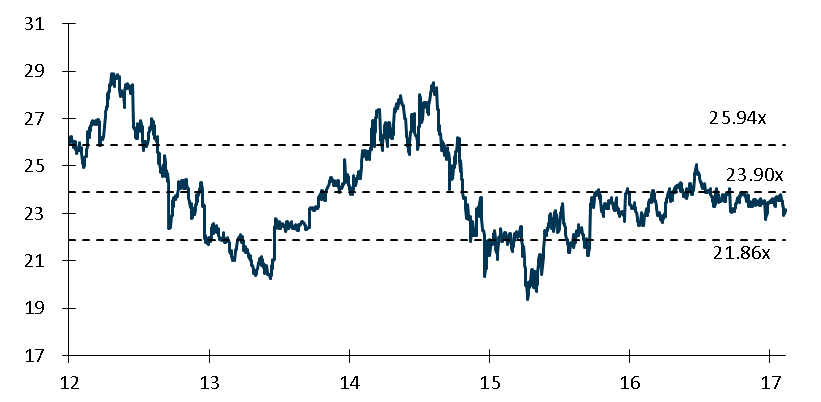

Maintain Accumulate with unchanged TP of S$8.31 (previous TP S$8.39) based on 23.9x. This pegs SGX to its historical 5-year average PE ratio.

5-year Historical Price Earnings Ratio

Jeremy covers primarily the Banking and Finance sector. He has 6 years’ experience in equities related dealing and research roles.

He graduated with Bachelors of Mechanical Engineering from Nanyang Technological University.