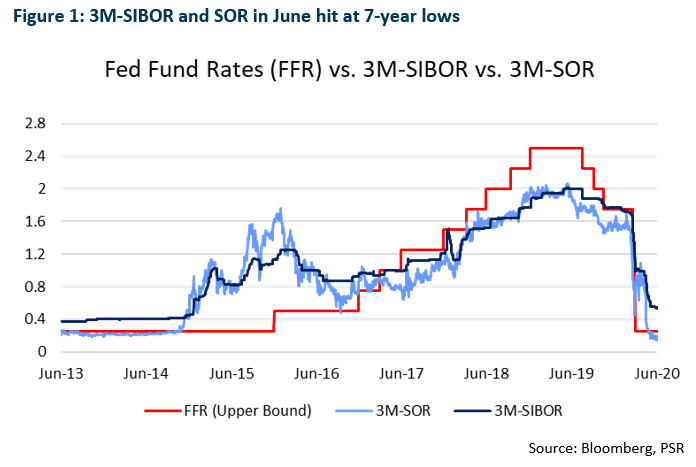

Local lending rates like to stay lower for longer

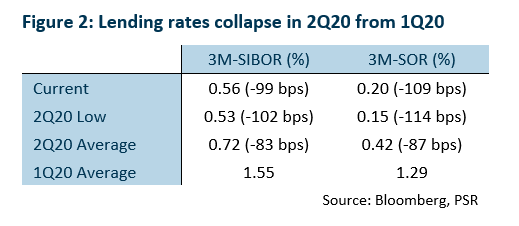

Interest rates in June remain suppressed, with 3M-SIBOR and 3M-SOR held at 0.56% and 0.20% respectively, similar to levels observed in May.

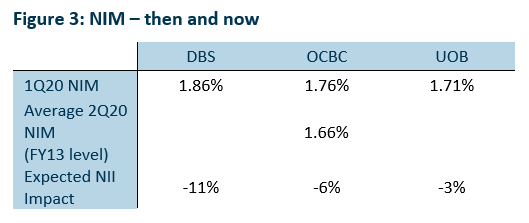

We expect rates to stabilise at current levels. Banks are expected to see NIM fall to 2013 levels (Figure 3) when similar interest rates were last observed. This will translate to an average of 7% impact of on NII for the banks in 2Q20.

Lower for longer interest rate environment will continue to weigh on bank earnings even as the economy looks to return to normalcy.

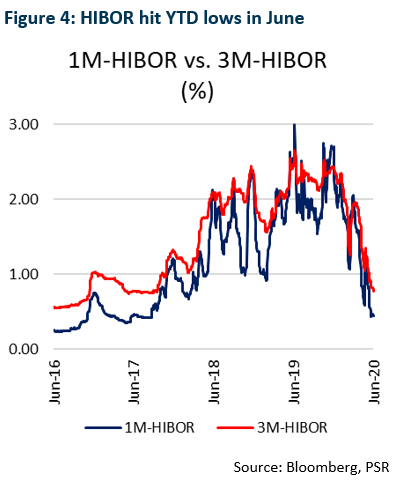

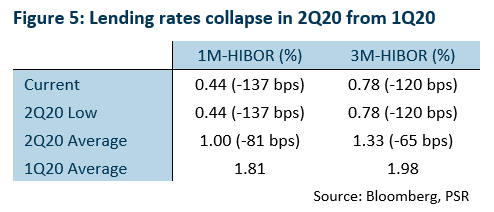

HIBOR hit new lows in June

1M and 3M-HIBOR dipped to YTD lows of 0.44% and 0.78% respectively in June, down 137 bps and 120 bps from 1.81% and 1.98% for 1M and 3M-HIBOR (Figure 5). Low HIBOR will further weigh in on the banks’ margins.

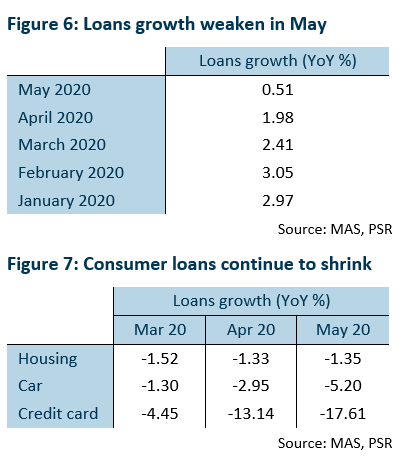

Loans growth suffer amidst Circuit Breaker period

With the Circuit Breaker measure in place, domestic loans growth slowed to 0.51% YoY in May (Figure 6).

Business loans grew 3.02% YoY in May, the slowest pace observed in 13 months as businesses withhold investments during the Circuit Breaker period. Short-term loans growth will continue facing headwinds as businesses manoeuvre the new business environment while the economy gradually reopens.

The implementation of the Circuit Breaker also saw consumer loans shrink further by 3.48% YoY in May, with housing loans, car loans and credit card loans shrinking across the board (Figure 7). While the reopening of retails in Phase 2, it will boost consumer spending, but spending on big-ticket items is expected to experience weakness.

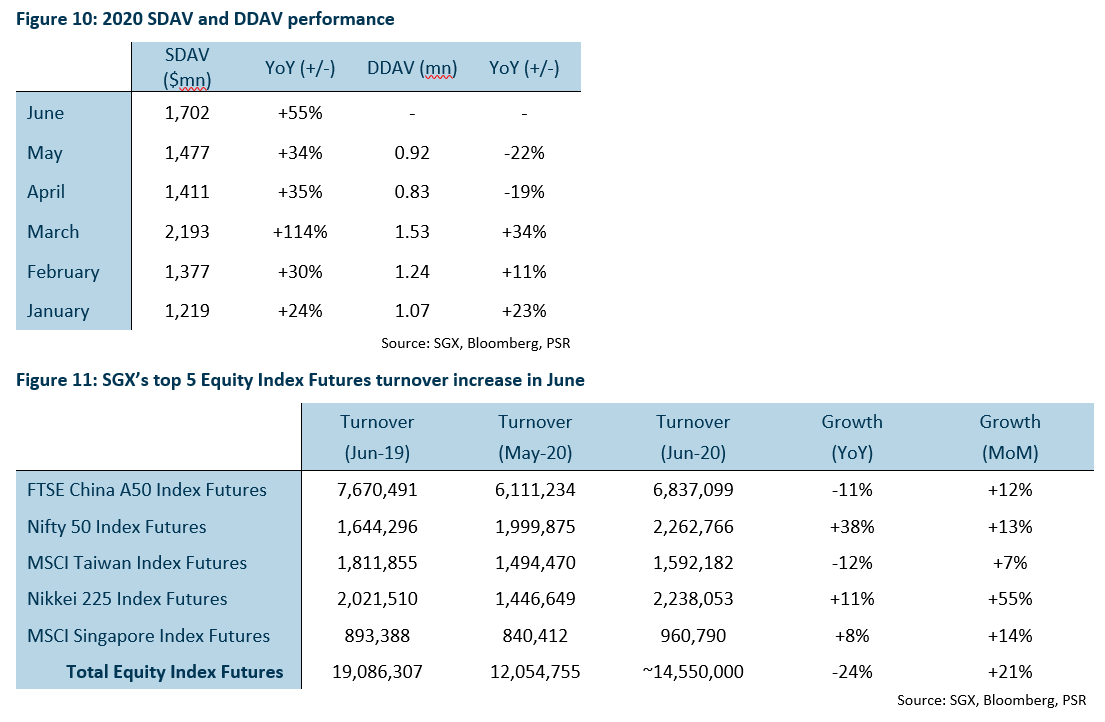

Improved market sentiments see SDAV and DDAV benefit in June

SDAV indicates a YoY improvement of 55% in June to $1,702mn (Figure 9). For 4Q20, SGX is likely to report quarterly SDAV of $1,540 mn, an improvement of 40% from 4Q19 of $1,100mn. Equity trading and clearing fee will potentially increase by 47% YoY for the quarter, but overall revenue will be weighed down by poorer derivative volumes for the quarter.

DDAV rebounded by 11% off April lows of 0.82mn to 0.92 mn contracts in May but remains down 22% YoY. However, preliminary June data of SGX’s top 5 equity index futures show turnover increasing by % YoY in June (Figure 11). The top 5 equity index futures contribute 70% of the total derivatives turnover in May.

SGX seemed to stave off pressures from impending cessation of the license agreement with MSCI on non-Singapore products, as turnover in June for various MSCI contracts grew, with turnover levels at multiple times of open positions in May (Appendix A).

We expect SGX’s 4Q20 revenue to come in at around $265mn, representing a 7% growth YoY, which is 5% above our expectations for 4Q20.

SGX launches FTSE Taiwan Index Futures to replace expiring MSCI licensed products

On 1 July, SGX announced that it will be introducing SGX FTSE Taiwan Index futures on 20 July. This marks SGX’s first move to launch products to replace MSCI’s suite of equity index products whose licensing will be expiring in February 2021.

The SGX FTSE Taiwan Index futures will be replacing MSCI Taiwan Index Futures as well as MSCI Taiwan NTR Index Futures. The MSCI Taiwan products combine to contribute 12.67% of total equity index turnover in May 2020. The Taiwan Index Futures also contribute more than 90% of the turnover from the 25 MSCI index futures that will be expiring.

Please refer to Appendix B for the list of MSCI futures that will be affected by the cessation of license in February 2021.

SGX acquires remaining 80% stake of BidFX for US$128mn

On 29 June, SGX announced plans to acquire the remaining 80% stake of cloud-based FX trading platform BidFX as the company expands its presence into the FX OTC market.

SGX first acquired 20% stake in BidFX in March 2019 but believes the move will complement SGX’s current FX futures offering as it continues to pursue a multi-asset strategy to expand regionally. Average daily volumes (ADV) by BidFX is reported to have grown at a CAGR of 57% since its establishment in 2017 to US$31bn in May 2020, with growth opportunities abound in the S$6.6tn ADV market.

SGX sees synergy in the G10 and Asian currency pairs offered by BidFX as well as its FX futures offering. There is also opportunities for cross-selling of products between its current suite of product offering and the OTC FX by BidFX.

The acquisition will be EPS accretive from FY21 but is not expected to have a material impact on SGX’s earnings in FY21.

We believe the revenue drivers with the acquisition of BidFX as well as the recent introduction of the FTSE Taiwan Index Futures will ease short term pains brought about by the cessation of the licensing agreement with MSCI and serve as a prospective growth catalyst for SGX in the longer term.

Investment Action

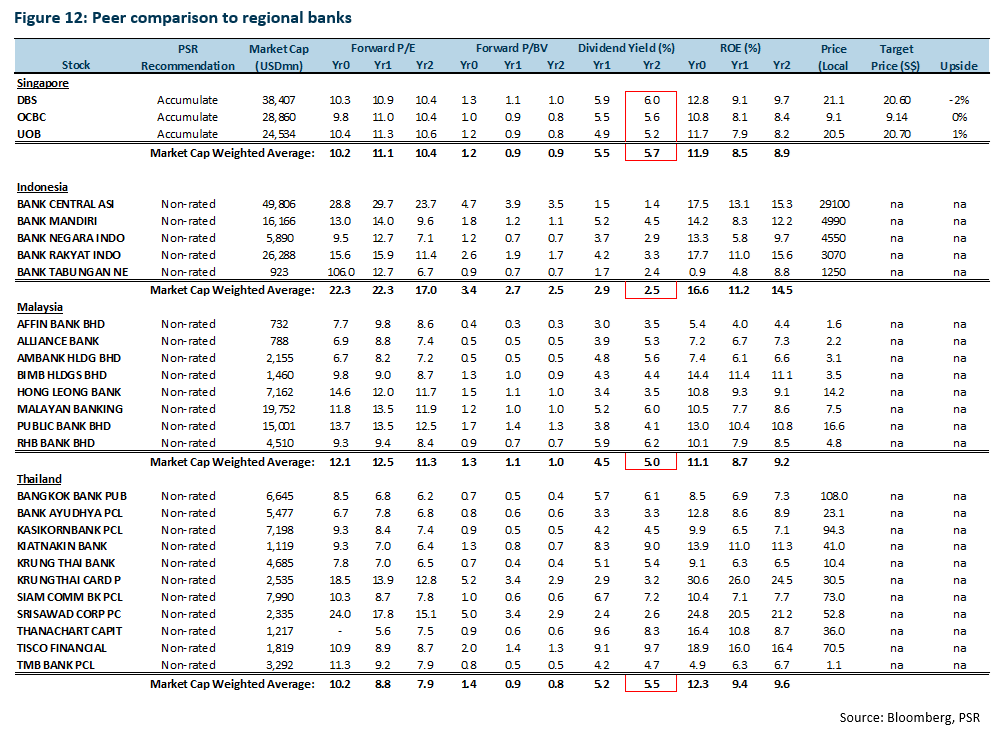

Maintain the Singapore Banking Sector at Neutral. We feel that the banks are fairly valued at current prices and upcoming re-rating catalyst will include business momentum from the generation of fee income as the economy enters phase 2 of re-opening. Yield remains attractive compared to regional peers at c.5-6%.