The Positives

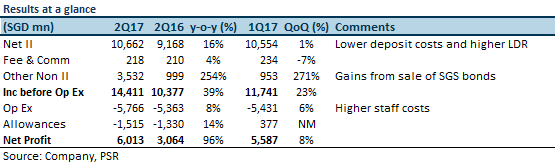

+ Net interest income (“NII”) growth continues to be supported by lower deposits costs. SIF expanded its Loan-to-Deposit Ratio (LDR) from a low base of 82% in 2016 to 89% by 2Q17 by cutting high-cost deposits.

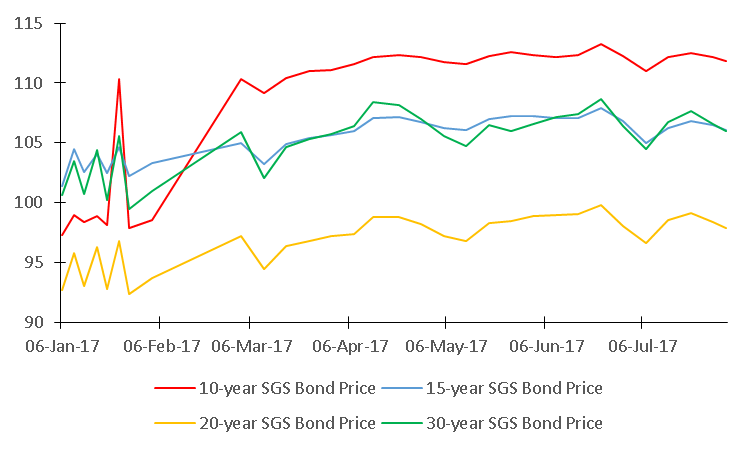

10-year SGS Bond Price exceeded the 15-year and 30-year SGS Bond Prices

Source: MAS, PSR

+ Provision expense remains manageable. We expect a moderate economic growth amid low macro volatility in Singapore for 2H17 which will keep NPL formation stable, so we do not expect negative surprises to provision expense this year.

The Negatives

– Perhaps some pressure on customer loans yields QoQ. The average rate on customer loans may have been lower QoQ as customer loan volumes remain relatively unchanged QoQ but interest income and hiring charges decreased c.6% QoQ.

Outlook

Interest income from Singapore Government Securities makes up c.11.5% of total interest income. We expect ample opportunities to reinvest the proceeds from the sale of 10-year SGS bonds into longer duration SGS bonds in the 2nd half of 2017 for higher yield. We are revising our FY17e NIM forecast upwards to 1.77% from the previous estimate of 1.7% because of better than expected deposit cost management and a lower average customer loans base than previously estimated for FY17e. FY17e Net interest income growth is projected to improve 7% (previous estimate was 9.9%) as we revised our customer loans rate lower in the 2H17 because 2Q17 customer loan rates may have showed some weakness. Our FY17e PATMI is unchanged.

Investment Actions

Maintain “Accumulate” with a target price of S$1.67 based on 0.8x P/BV. We expect upside in dividends following the stellar operating performance.

Jeremy covers primarily the Banking and Finance sector. He has 6 years’ experience in equities related dealing and research roles.

He graduated with Bachelors of Mechanical Engineering from Nanyang Technological University.