The Positives

The Negatives

Outlook

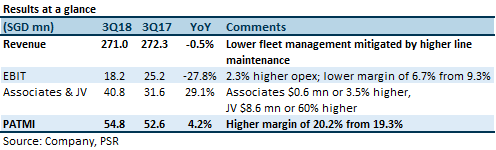

The outlook remains challenging. Despite the positive surprise for JV, we are not ready to call a return to historical normalised levels. The same level of 3Q18’s $22.9mn JV contribution was last seen in FY14, and we think such a V-shaped recovery is unlikely, in view of the structural issue mentioned above. While the worst may be over for JV contribution, we are inclined to believe that the long-term normalised contribution will still be lower than historical level.

Upgrade to Accumulate (from Neutral); higher target price of S$3.39 (previously $3.35)

Our FY18e/FY19e estimate for profit contribution from associates & JVs is 32%/16% higher than previous. Consequently, our FY18e/FY19e PATMI estimates are 15.6%/5.6% higher than previous.

FY17 dividend distribution of 13.0 cents should be sustainable for FY18e (3.9% yield), in view of the positive free cash flow, dividends received from associated & JV companies and a balance sheet that is in a net cash position. (1H18 interim dividend of 4 cents was unchanged from 1H17.)

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.