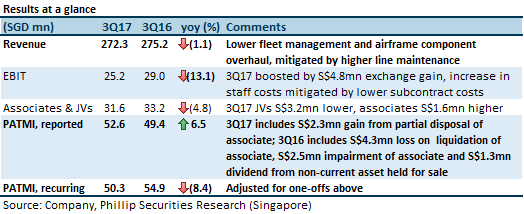

In spite of the 3.8% year-on-year (yoy) growth to 92,300 Commercial Aircraft Movements at Changi Airport during the quarter, revenue for the group was lower 1.1%. The associates & JVs, which contribute more than half of the bottom line also showed lower yoy results as well. We attribute these weaknesses to the structural changes to the industry, in which new aircraft and engines require less frequent maintenance and lighter work scopes.

Headline PATMI exceeded our expectations due to stronger Associates and JVs

We were expecting 44% yoy lower share of profits from Associates and JVs. The positive surprise was mainly from higher than expected contribution from JVs (Actual: S$14.3mn; Forecasted: S$4.9mn), with additional contribution from associated companies (Actual: S$17.3mn; Forecasted: S$12.7). Contribution from JVs had been single-digit for the past three quarters and bounced back in 3QFY17 to S$14.3mn. We have lifted our full year Associates & JVs forecast for FY17e and FY18e by 21% and 8.6% respectively.

Recurring PATMI still weak; expect flattish +2.3% growth in recurring PATMI for FY17e

While headline PATMI was 6.5% higher yoy, it was 8.4% lower yoy after stripping out the effects of one-offs in both 3QFY17 and 3QFY16. Headline PATMI for 3QFY17 was boosted by a S$2.3mn one-off gain from partial disposal of an associate. Conversely, 3QFY16 PATMI was dragged down by one-off losses from liquidation and impairment of an associate, offset by dividend from a non-current asset held for sale.

49:51 strategic partnership between SIAEC and Moog

As announced in December 2016, SIA Engineering Company Limited (SIAEC) is establishing a JV with Moog Incorporated (Moog) to provide maintenance, repair and overhaul services for components on flight control systems for new-generation aircraft, such as the Boeing 787 and the Airbus A350. The JV pending regulatory approvals from relevant jurisdictions.

Upgrade to “Neutral” rating with higher target price of S$3.38 (previous: S$3.28)

While work volume is expected to pick up in 2017, we believe work content will be lower compared to historical. This is due to better technology, which has led to better airframe and engine reliability. Our target price gives a FY17e forward P/E multiple of 20.5x and a 21.0x P/E multiple over next-twelve-months (NTM) earnings.

Richard covers the Transport Sector and Industrial REITs. He graduated with a Master of Science in Applied Finance from the Singapore Management University. He holds the CFTe and FRM certifications and is a CFA charterholder.

He was ranked #2 Top Stock Picker (Asia) for Real Estate Investment Trusts in the 2018 Thomson Reuters Analyst Awards, and ranked #2 Top Stock Picker (Singapore) for Resources & Infrastructure in the 2016 Thomson Reuters Analyst Awards.